Comprehensive Problem 2, cont.

Requirement 2, 5, cont.

Salaries Expense

Jan. 15

1,500

Adj.

1,000

Bal.

2,500

250

250

Jan. 24

Bal.

Rent Expense

Jan. 28

1,600

Bal.

1,600

Bal.

Comprehensive Problem 2, cont.

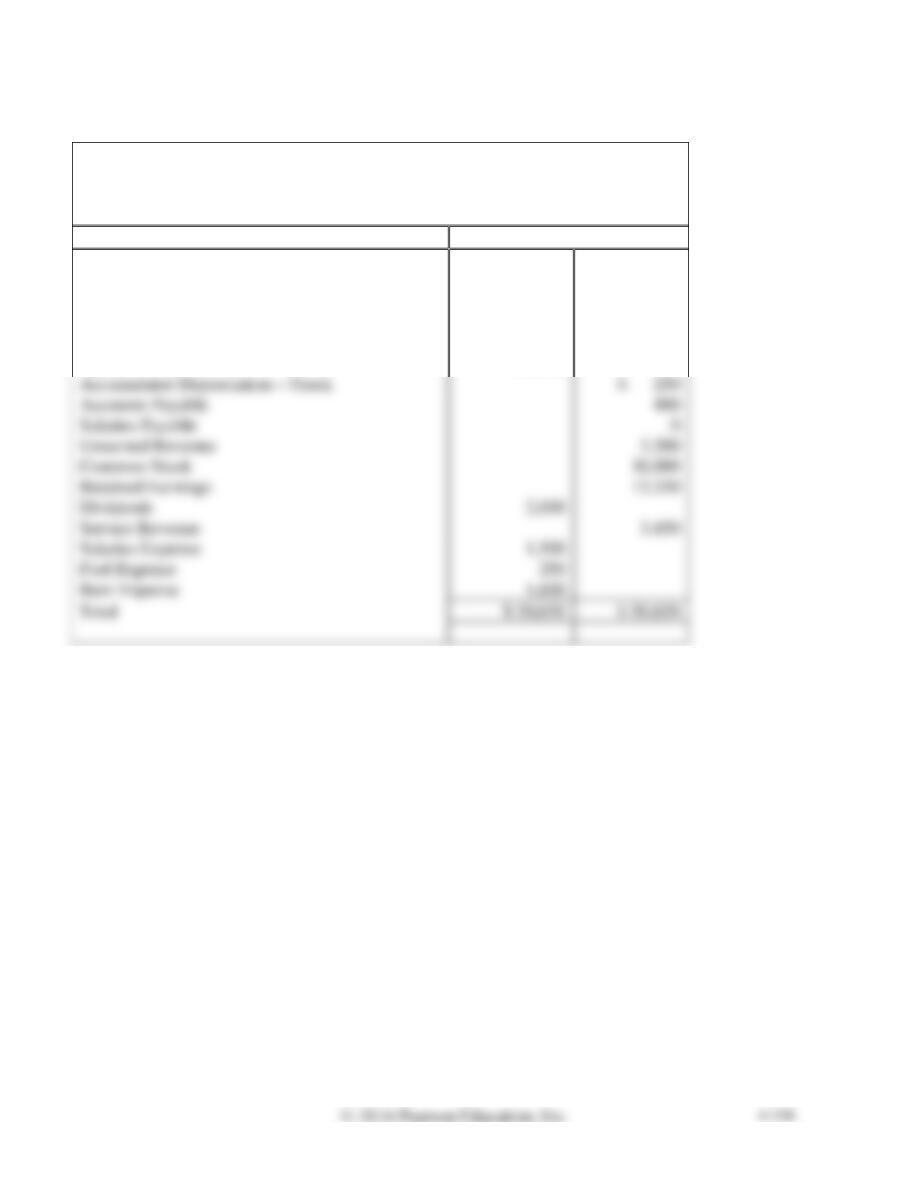

Requirement 3

MILLER DELIVERY SERVICE

Unadjusted Trial Balance

January 31, 2017

Account Title

Balance

Debit

Credit

Cash

$ 22,550

Accounts Receivable

1,300

Office Supplies

700

Prepaid Insurance

750

Truck

20,000

Accumulated Depreciation—Truck

Accounts Payable

Salaries Payable

Unearned Revenue

Common Stock

Retained Earnings

Dividends

2,000

1,500

250

1,600

$ 50,650

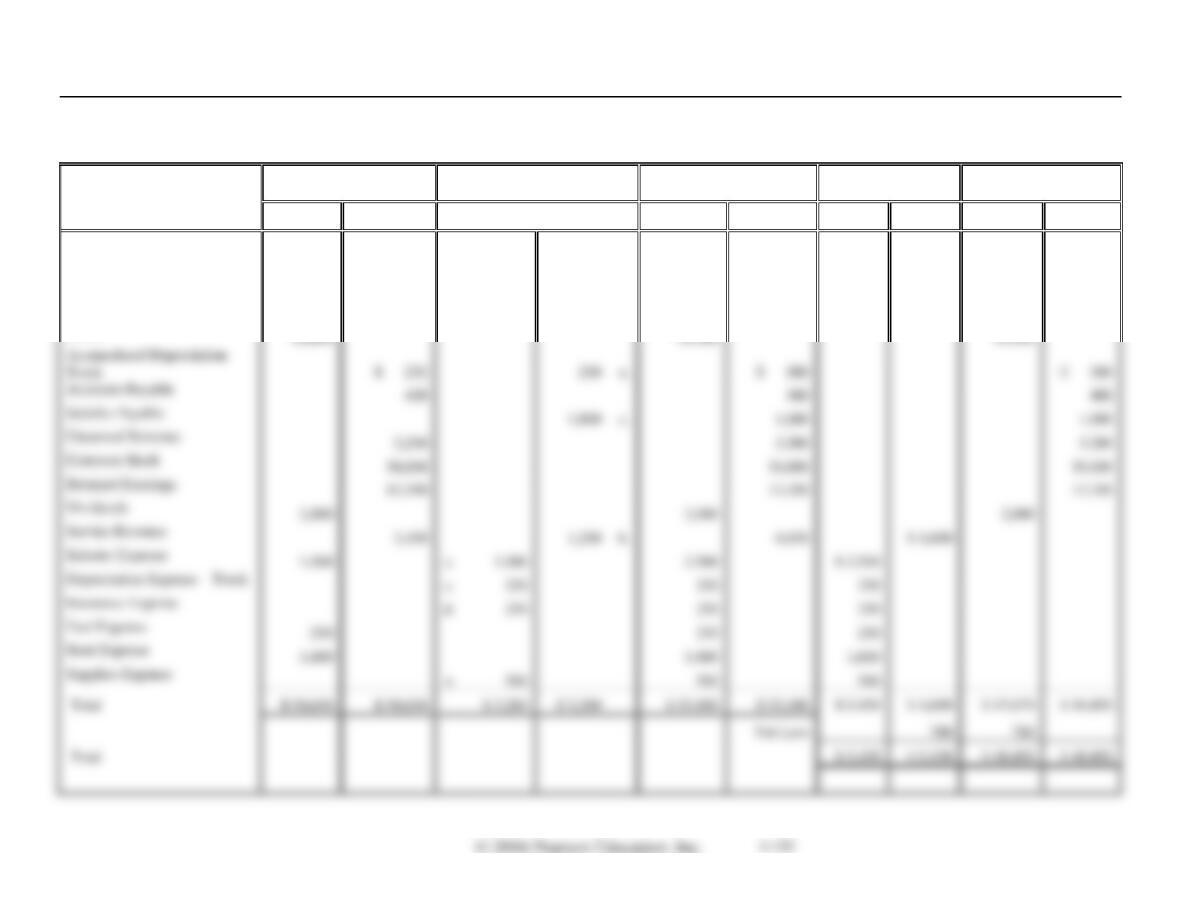

Comprehensive Problem 2, cont., Requirement 4

MILLER DELIVERY SERVICE

Worksheet

January 31, 2017

Account Names

Unadjusted Trial

Balance

Adjustments

Adjusted Trial Balance

Income Statement

Balance Sheet

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Cash

$ 22,550

$ 22,550

$ 22,550

Accounts Receivable

1,300

b.

$ 1,200

2,500

2,500

Office Supplies

700

$ 580

a.

120

120

Prepaid Insurance

750

250

d.

500

500

Truck

250

e.

$ 500

Accounts Payable

400

c.

Unearned Revenue

Common Stock

Retained Earnings

13,350

Dividends

2,000

2,000

Service Revenue

b.

Salaries Expense

1,500

2,500

Depreciation Expense—Truck

250

Insurance Expense

d.

250

Fuel Expense

250

Rent Expense

Supplies Expense

580

$ 50,650

$ 3,280

$ 3,280

$ 53,100

$ 4,650

$ 48,450

Net Loss

780

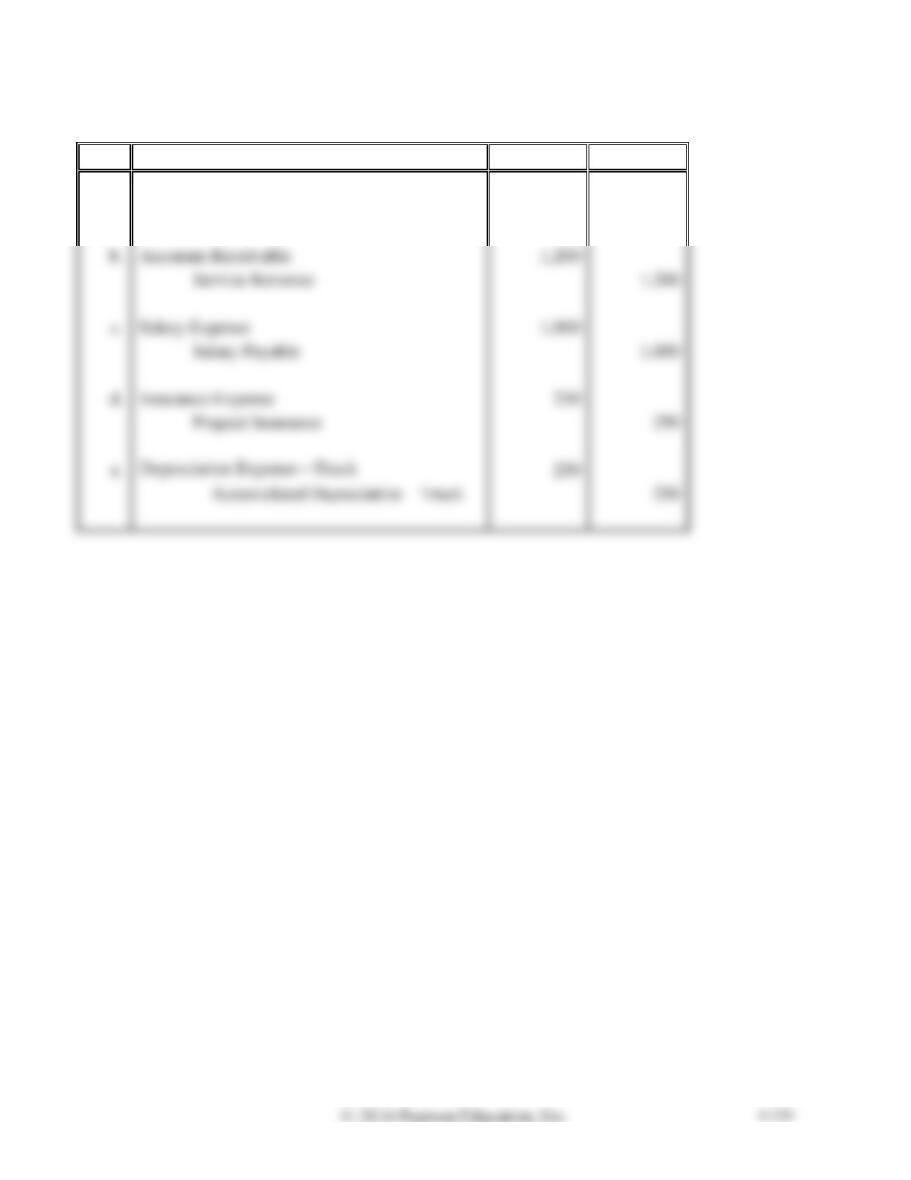

Comprehensive Problem 2, cont.

Requirement 5

Date

Accounts

Debit

Credit

a.

Supplies Expense

580

Office Supplies

580

Accounts Receivable

Service Revenue

c.

Salary Expense

Salary Payable

Insurance Expense

250

e.

250

Accumulated Depreciation—Truck

250

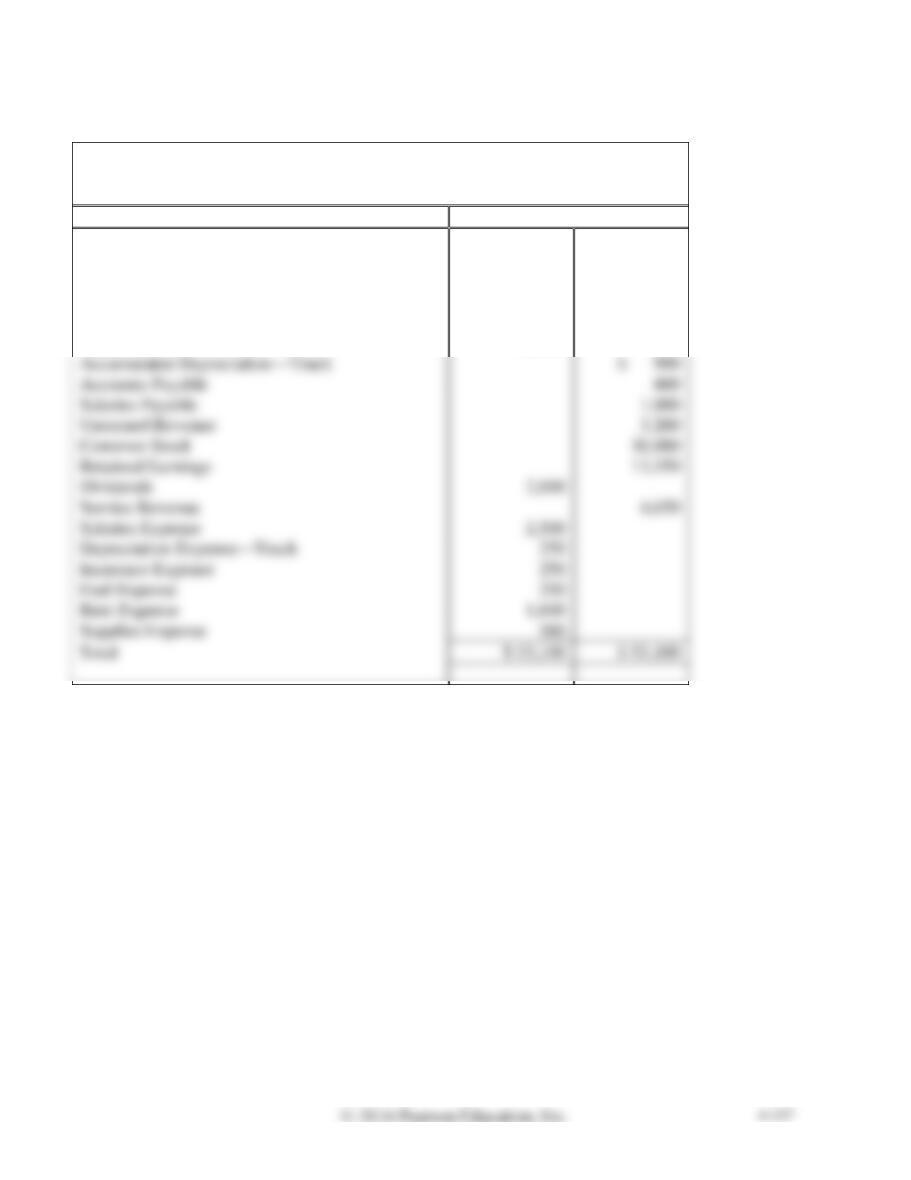

Comprehensive Problem 2, cont.

Requirement 6

MILLERS DELIVERY SERVICE

Adjusted Trial Balance

January 31, 2017

Account Title

Balance

Debit

Credit

Cash

$ 22,550

Accounts Receivable

2,500

Office Supplies

120

Prepaid Insurance

500

Truck

20,000

Accumulated Depreciation—Truck

Accounts Payable

Salaries Payable

Unearned Revenue

Common Stock

Retained Earnings

Dividends

2,000

Service Revenue

Salaries Expense

2,500

Depreciation Expense—Truck

250

Insurance Expense

250

Fuel Expense

250

Rent Expense

1,600

Supplies Expense

580

Total

$ 53,100

Comprehensive Problem 2, cont.

Requirement 7

MILLER DELIVERY SERVICE

Income Statement

Month Ended January 31, 2017

Revenues:

Service Revenue

$ 4,650

Expenses:

Total Expenses

MILLER DELIVERY SERVICE

Statement of Retained Earnings

Month Ended January 31, 2017

Retained Earnings, January 1, 2017

Comprehensive Problem 2, cont.

Requirement 7, cont.

MILLER DELIVERY SERVICE

Balance Sheet

January 31, 2017

Assets

Current Assets:

Cash

$ 22,550

Accounts Receivable

2,500

Office Supplies

120

Prepaid Insurance

500

Plant Assets:

Truck

Less: Accumulated Depreciation—Truck

Total Plant Assets

Total Assets

Current Liabilities:

$ 400

Salaries Payable

1,000

Unearned Revenue

3,200

Total Current Liabilities

Total Liabilities

Common Stock

Retained Earnings

Total Liabilities and Stockholders’ Equity

Requirement 8

Return On Assets = Net income / Average total assets

= $(780) / $45,010 = (1.7%)

Average Total Assets = ($44,850 + $45,170) / 2 = $45,010

Critical Thinking

Ethical Issue 4-1

Grant Film Productions wishes to expand and has borrowed $100,000. As a condition for making this

loan, the bank requires that the business maintain a current ratio of at least 1.50.

Business has been good but not great. Expansion costs have brought the current ratio down to 1.40 on

December 15. Rita Grant, owner of the business, is considering what might happen if she reports a

current ratio of 1.40 to the bank. One course of action for Grant is to record in December $10,000 of

revenue that the business will earn in January of next year. The contract for this job has been signed.

Requirements

1. Journalize the revenue transaction, and indicate how recording this revenue in

December would affect the current ratio.

2. Discuss whether it is ethical to record the revenue transaction in December. Identify the accounting

principle relevant to this situation, and give the reasons underlying your conclusion.

SOLUTION

Requirement 1

Date

Accounts

Debit

Credit

Requirement 2

Recording this transaction in December violates the revenue recognition principle, which states that

revenue should be recorded when it is earned. On December 31, the business has not performed the

service for the client, and therefore has not earned the revenue. Recording the transaction in December is

unethical because it deliberately misrepresents the facts.

Fraud Case 4-1

Arthur Chen, a newly minted CPA, was on his second audit job in the Midwest with a new client called

Parson Farm Products. He was looking through the past four years of financials and doing a few ratios

when he noticed something odd. The current ratio went from 1.9 in 2016 down to 0.3 in 2017, despite

the fact that 2017 had record income. He decided to sample a few transactions from December 2017. He

found that many of Parson’s customers had returned products to the company because of substandard

quality. Chen discovered that the company was clearing the receivables (i.e., crediting Accounts

Receivable) but “stashing” the debits in an obscure long–term asset account called “grain reserves”

rather than debiting Sales Returns and Allowances to keep the company’s income “in the black” (i.e.,

positive income).

Requirements

1. How did the fraudulent accounting just described affect the current ratio?

2. Can you think of any reasons why someone in the company would want to take this kind of action?

SOLUTION

Requirement 1

This transaction should decrease the current ratio, because Accounts Receivable decreases by the retail

Financial Statement Case 4-1

This case, based on the balance sheet of Starbucks Corporation, will familiarize you with some of the

assets and liabilities of that company. Visit http://www.pearsonhighered.com/Horngren to view a link

to the Starbucks Corporation Fiscal 2013 Annual Report. Use the Starbucks Corporation balance sheet

to answer the following questions.

Requirements

1. Which balance sheet format does Starbucks use?

2. Name the company’s largest current asset and largest current liability at September 29, 2013.

3. Compute Starbucks’s current ratios at September 29, 2013, and September 30, 2012. Did the current

ratio improve, worsen, or hold steady?

4. Under what category does Starbucks report furniture, fixtures, and equipment?

5. What was the cost of the company’s fixed assets at September 29, 2013? What was the amount of

accumulated depreciation? What was the book value of the fixed assets? See Note 7 for the data.

SOLUTION

Requirement 1

Financial Statement Case 4-1, cont.

Requirement 3

September 29, 2013

Current ratio = Total current assets / Total current liabilities

= $5,471.4 million / $5,377.3 million = 1.02

September 30, 2012

Current ratio = Total current assets / Total current liabilities

= $4,199.6 million / $2,209.8 million = 1.9

The ratio worsened from 2012 to 2013.

Requirement 4

Team Project 4-1

Kathy Wintz formed a lawn service business as a summer job. To start the corporation on May 1, 2016,

she deposited $1,000 in a new bank account in the name of the business. The $1,000 consisted of a $600

loan from Bank One to her company, Wintz Lawn Service, and $400 of her own money. The company

issued $400 of common stock to Wintz. Wintz rented lawn equipment, purchased supplies, and hired

other students to mow and trim customers’ lawns.

Requirements

1. As a team, prepare the income statement and the statement of retained earnings of Wintz Lawn

Service for the four months May 1 through August 31, 2016.

2. Prepare the classified balance sheet (report form) of Wintz Lawn Service at August 31, 2016.

3. Was Wintz’s summer work successful? Give your team’s reason for your answer.

SOLUTION

Requirement 1

WINTZ LAWN SERVICE, INC.

Income Statement

Four Months Ended August 31, 2016

Revenues:

Service Revenue ($5,500 + $750)

$ 6,250

Retained Earnings, May 1, 2016

Dividends

Team Project 4-1, cont.

Requirement 2

WINTZ LAWN SERVICE, INC.

Balance Sheet

August 31, 2016

Assets

Current Assets:

Cash

$ 2,000

Accounts Receivable

750

Prepaid Equipment Rent

200

Supplies

50

Total Current Assets

$ 3,000

Plant Assets:

Trailer

Less: Accumulated Depreciation—Trailer

Total Plant Assets

Total Assets

$ 3,200

Current Liabilities:

Total Current Liabilities

$ 300

Common Stock

Retained Earnings

Total Liabilities and Stockholders’ Equity

$ 3,200