CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-75

PROBLEM 4-13A (Continued)

(b) TENFOUR TRUCKING COMPANY

STATEMENT OF RETAINED EARNINGS

FOR THE MONTH ENDED JANUARY 31, 2016

Beginning balance, January 1, 2016 ……………………………….. $ 40,470

(c) TENFOUR TRUCKING COMPANY

BALANCE SHEET

JANUARY 31, 2016

Assets

Current assets:

Cash …………………………………………………………….. $ 27,340

Accounts receivable ……………………………………….. 41,500

Liabilities

Current liabilities:

Accounts payable …………………………………………… $ 32,880

Notes payable ……………………………………………….. 50,000

Stockholders’ Equity

Capital stock ………………………………………………………. $100,000

4-76 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 4-13A (Concluded)

5. Current Ratio = Current Assets/Current Liabilities

$86,090/$106,692 = 0.81 to 1

6. Tenfour cannot compute a gross profit ratio because it does not report cost of sales.

It is a service business rather than a product company. One possible measure of

profitability for any company is the profit margin, which is net income divided by

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 3 DECISION CASE 4-1 COMPARING TWO COMPANIES IN THE SAME INDUSTRY:

CHIPOTLE AND PANERA BREAD

1. Chipotle recognizes revenue from restaurant sales at the time food and beverages

are sold. Panera Bread’s bakery-cafe sales are recognized when the products are

2. Chipotle reports $34,839,000 of accounts receivable on its balance sheet and this

represents $34,839/$878,479, or 4.0% of total current assets. Panera Bread reports

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-77

LO 3 DECISION CASE 4-2 READING AND INTERPRETING NORDSTROM’S NOTES—

REVENUE RECOGNITION

1. Revenue from retail stores is recognized at the point of sale. Revenue from sales to

customers shipped directly from stores, as well as from website and catalog sales, is

recorded as revenue upon estimated receipt by the customers. The way in which the

2. Nordstrom recognizes revenue from gift cards when they are redeemed. When a gift

card is purchased, Nordstrom debits Cash and credits a gift card liability. When the

friend redeems the card, Nordstrom debits this liability account and credits Revenue.

LO 3 DECISION CASE 4-3 READING AND INTERPRETING SEARS HOLDINGS

CORPORATION’S NOTES—REVENUE RECOGNITION

1. Under the accrual basis, revenue should be recognized when a performance obliga-

tion is satisfied rather than when cash is received. Over the life of a service contract,

2. Revenue to be recognized each year:

Year 1 Year 2 Year 3 Total

Sales revenue $2,320* $ 0 $ 0 $2,320

Service contract revenue 60** 60 60 180

Total revenue $2,380 $60 $60 $2,500

*$2,500 – $180

**$180/3 years

4-78 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MAKING FINANCIAL DECISIONS

LO 2,3,4 DECISION CASE 4-4 THE USE OF NET INCOME AND CASH FLOW TO

EVALUATE A COMPANY

1. DUKE INC.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Operating activities:

Cash received from services

provided to clients ………………………………… $1,020,000*

Cash paid for:

Salaries and wages ……………………………….. $440,000**

mentary schedule.

2. One important question to be asked is whether it is possible for the company to con-

tinue to generate service revenues in succeeding years at the level attained in its

first year. The ability to collect the revenues billed in 2016, but not yet collected

($230,000), should also be a concern. On the basis of the cash flows generated in

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-79

LO 4 DECISION CASE 4-5 DEPRECIATION

The decision to purchase or lease long-term assets is a difficult one for all businesses

and requires an analysis of all the relevant facts. Rapidly changing technology may

make it less risky to lease computer equipment than to purchase it. This is certainly a

key consideration in this particular case. Jensen also needs to consider maintenance

costs. The case does not indicate whether or not Jensen would be responsible for main-

tenance if it leases the equipment. Another relevant factor would be whether or not the

equipment would have any salvage value at the end of its useful life.

ETHICAL DECISION MAKING

LO 2,3,4,5 DECISION CASE 4-6 REVENUE RECOGNITION AND THE MATCHING

PRINCIPLE

1. Recognize an ethical dilemma:

If sales are recorded but the commissions associated with these sales are not rec-

orded during the month of June, net income will be larger by the understatement of

commissions expense. The failure to record advertising expense for the month of

June will also result in an understatement of expense and an overstatement or

increase in net income. Finally, an increase in the estimated useful life of the auto-

4-80 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

estimated useful lives of depreciable assets, but the changes must be justified on

sound economic grounds. For example, changes in technology might prompt a com-

pany to decrease the estimated useful lives of its computers. The need to increase

the net income for the year is certainly not an acceptable reason under GAAP to

change the estimated useful lives of depreciable assets.

Each of the three suggestions involves a question of ethics. You must decide

whether to confront the two owners with your concerns about the proper treatment

for these items.

2. Analyze the key elements in the situation:

a. The owners of the company may benefit in the short term, because the bank may

be more likely to give them a loan based on the inflated net income. The bank

will be harmed, because the financial information it receives does not represent

the underlying reality of the situation.

3. List alternatives and evaluate the impact of each on those affected:

As controller, your options are to either go along with the changes proposed by the

owners or confront them with your concerns. If the proposed changes are made, the

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-81

4. Select the best alternative:

You should confront the owners with your concerns about the proper treatment for

these items. All three proposed changes involve an attempt to consciously overstate

income for the purpose of obtaining a loan. There is an attempt on the part of the

vice president of sales to deceive a user of the accounting information. The banker

relies on the trustworthiness of the company to accurately report its income, and

each of the three suggestions would violate that trust. The company would not be

acting in good faith if it were to report income as has been suggested.

First, each of the suggestions for improving profits for the month of June is a

clear violation of generally accepted accounting principles. The recognition of June

sales, but the deferral of commission expenses on these same sales until July vi-

olates the matching principle. Similarly, the deferral of advertising expense, which is

directly related to the month of June, until the following fiscal year in July is likewise

at odds with the matching principle. Finally, it is not acceptable practice under ac-

counting standards to alter the estimated useful lives of depreciable assets for the

sole purpose of increasing income. We would need to be able to justify the changes

on sound economic grounds.

4-82 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 DECISION CASE 4-7 ADVICE TO A POTENTIAL INVESTOR

The financial statements contain two major errors that prevent them from being in ac-

cordance with generally accepted accounting principles. First, if the normal balance of

supplies on hand is $1,000, Century should recognize supplies expense on its income

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-83

SOLUTION TO INTEGRATIVE PROBLEM

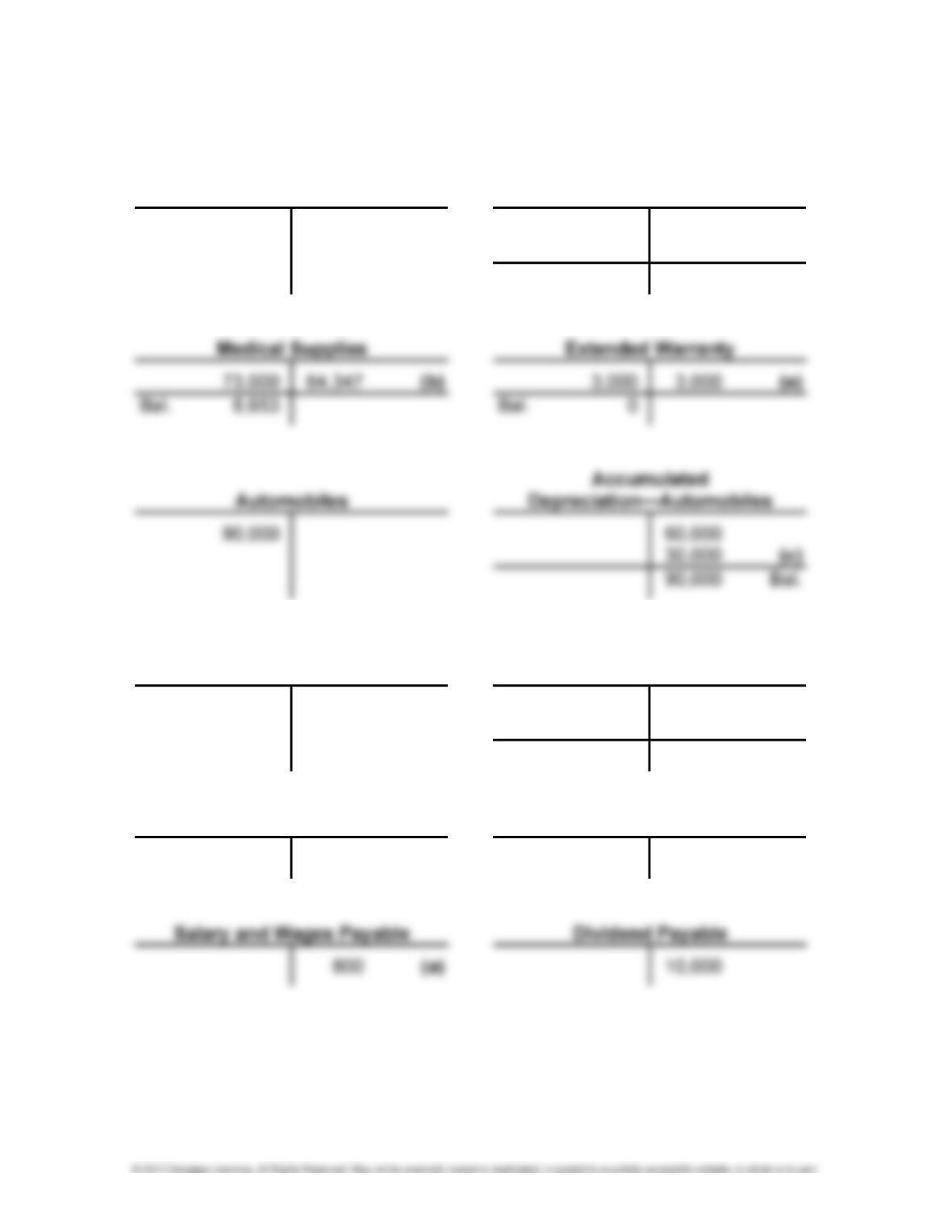

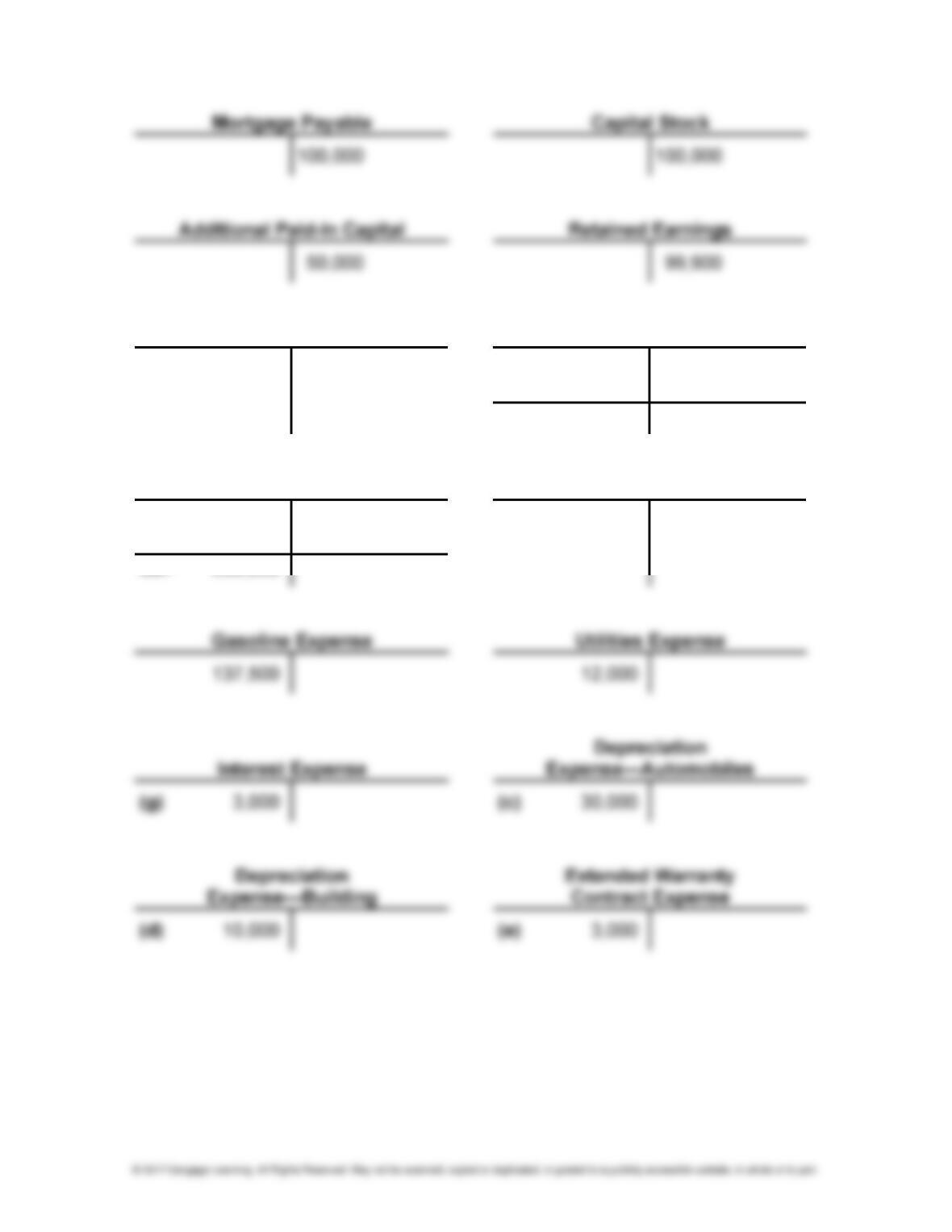

1. and 2. T accounts:

Cash Billings Receivable (net)

77,400 151,000

(f) 16,000

Bal. 167,000

Building

Accumulated

Depreciation—Building

200,000 50,000

10,000 (d)

60,000 Bal.

Accounts Payable Interest Payable

22,000 3,000 (g)

4-84 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Dividends Medical Services Revenue

10,000 550,000

16,000 (f)

566,000 Bal.

Salary and Wages Expense Supplies Expense

288,000 (b) 64,347

(a) 800

Bal. 288,800

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-85

3. MOUNTAIN HOME HEALTH INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Revenues:

Medical services revenue …………………………………….. $566,000

Expenses:

Salary and wages expense ………………………………….. $288,800

Supplies expense ……………………………………………….. 64,347

Gasoline expense ……………………………………………….. 137,500

Utilities expense …………………………………………………. 12,000

4-86 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

4. MOUNTAIN HOME HEALTH INC.

BALANCE SHEET

AS OF DECEMBER 31, 2016

Assets

Current assets:

Cash ………………………………………………………… $ 77,400

Billings receivable (net) ………………………………. 167,000

Medical supplies ………………………………………… 8,653

Total current assets ……………………………….. $253,053

Total liabilities ……………………………………………. $135,800

Stockholders’ Equity

Capital stock ………………………………………………….. $100,000

Additional paid-in capital ………………………………….. 50,000

Retained earnings …………………………………………… 107,253

Total stockholders’ equity ……………………………. 257,253

Total liabilities and stockholders’ equity ……………… $393,053

5. a. Working capital: $253,053 – $35,800 = $217,253

b. Current ratio: $253,053/$35,800 = 7.07 to 1

6. By their nature, all adjusting entries cause a difference between the amount of in-

come recognized on an accrual basis and that recognized on a cash basis. The ad-

justing entries for wages and salaries and interest result in decreases in income in

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-87

7. Supply of cash needed:

Salaries: $800 per day × 7 days per week × 7 weeks = $39,200