4-1

CHAPTER 4

Income Measurement

and Accrual Accounting

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Explain the significance of recognition and measurement 35* 20 Diff

in the preparation and use of financial statements.

37* 15 Mod

Module 2

5. Identify the four major types of adjusting entries and prepare 4 10 Easy

them for a variety of situations. 5 10 Easy

6 20 Easy

7 10 Mod

8 20 Easy

4-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 3

6. Explain the steps in the accounting cycle and the significance 26 5 Easy

of each step.

Module 4

8. Understand how to use a work sheet as a basis for preparing 33 5 Mod

financial statements (Appendix). 34 10 Mod

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-3

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Explain the significance of recognition and measurement

in the preparation and use of financial statements.

Module 2

5. Identify the four major types of adjusting entries and prepare 1 20 Mod

them for a variety of situations. 2 20 Mod

3 20 Mod

Module 3

6. Explain the steps in the accounting cycle and the significance 12*# 60 Mod

of each step. 13* 90 Mod

Module 4

8. Understand how to use a work sheet as a basis for preparing 12* 60 Mod

financial statements (Appendix). 13* 90 Mod

4-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Explain the significance of recognition and measurement

in the preparation and use of financial statements.

7 45 Mod

Module 2

Module 3

6. Explain the steps in the accounting cycle and the significance

of each step.

Module 4

8. Understand how to use a work sheet as a basis for preparing

financial statements (Appendix).

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-5

EXERCISES

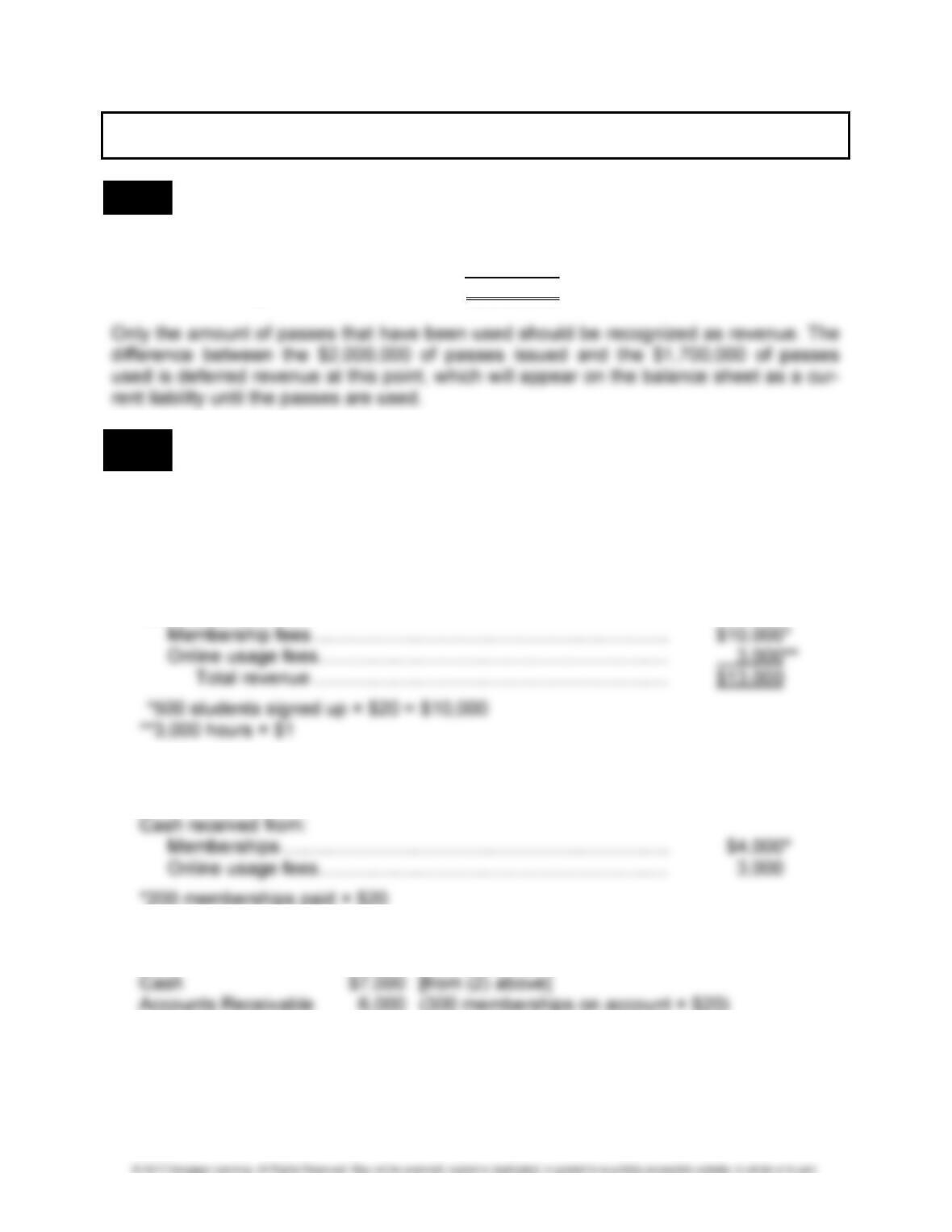

LO 3 EXERCISE 4-1 REVENUE RECOGNITION

Cash collected at toll booth $3,000,000

Passes redeemed 1,700,000

Revenue recognized $4,700,000

LO 2 EXERCISE 4-2 COMPARING THE INCOME STATEMENT AND THE STATEMENT OF

CASH FLOWS

1. The income statement for Campus Internet Connection would show the following:

CAMPUS INTERNET CONNECTION

INCOME STATEMENT

FOR THE MONTH ENDED JANUARY 31

Revenues:

2. A partial statement of cash flows for Campus Internet Connection would show the

following:

3. On Campus’s balance sheet at the end of January, two accounts will appear:

4-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 EXERCISE 4-3 THE MATCHING PRINCIPLE

1. b

LO 5 EXERCISE 4-4 ACCRUALS AND DEFERRALS

1. AL 5. DE

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-7

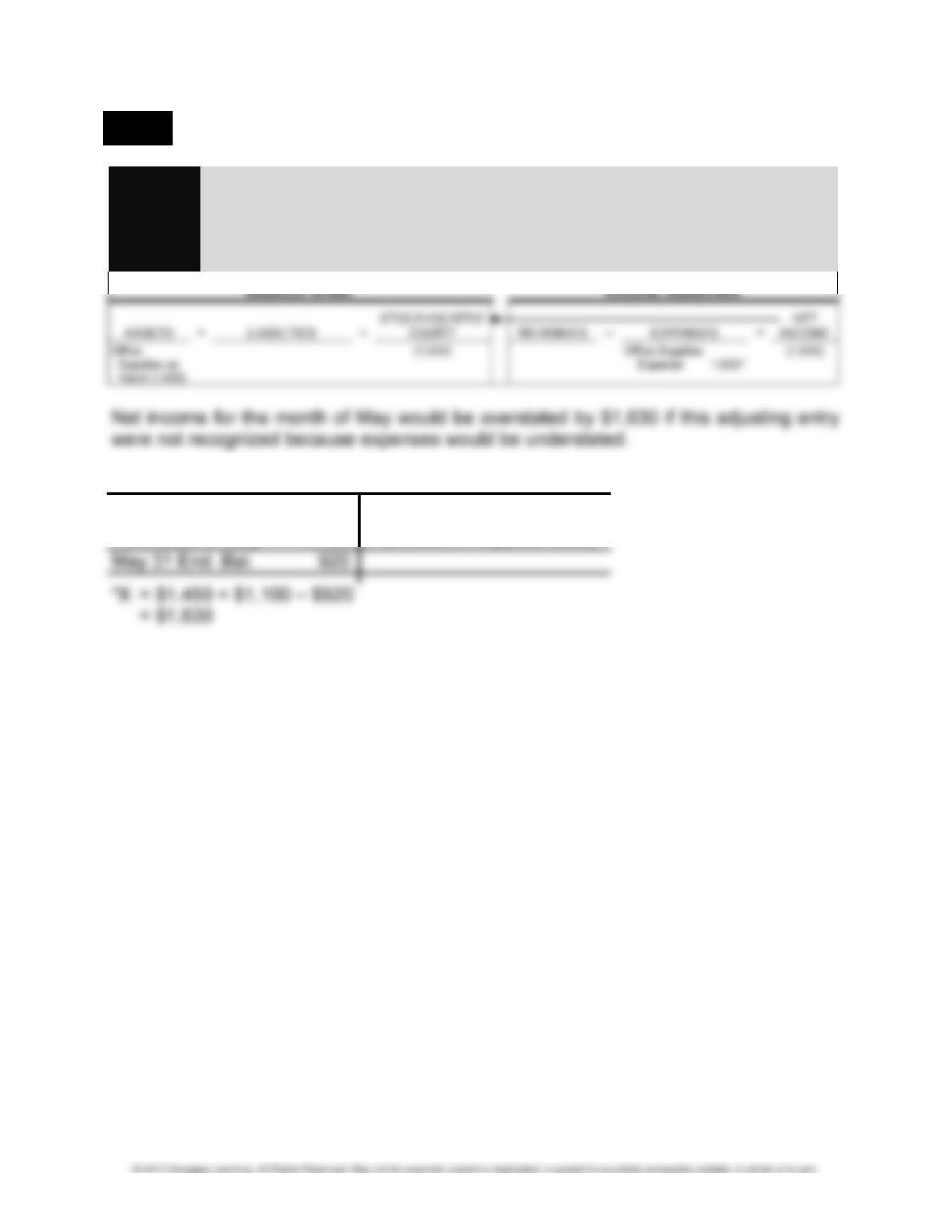

LO 5 EXERCISE 4-5 OFFICE SUPPLIES

Journal May 31 Office Supplies Expense ………………………… 1,630

Entry Office Supplies on Hand ……………………. 1,630

Analysis To record office supplies used:

$1,450 + $1,100 – $920.

Supplies

May 1 Beg. Bal. 1,450

Purchased in May 1,100 X (amount of supplies used)*

4-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 4-6 PREPAID RENT—QUARTERLY ADJUSTMENTS

2.

Journal Sept. 1 Prepaid Rent ………………………………………… 12,000

Entry Cash ………………………………………………. 12,000

3.

Journal Sept. 30 Rent Expense……………………………………….. 2,000

Entry Prepaid Rent ……………………………………. 2,000

Analysis To record one month of rent expense:

$12,000/6.

Balance Sheet Income Statement

LO 5 EXERCISE 4-7 WORKING BACKWARD: PREPAID INSURANCE

1. Baxter will recognize $24,000/12 = $2,000 each month in insurance expense.

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-9

LO 5 EXERCISE 4-8 DEPRECIATION

1.

Journal July 1 Computer …………………………………………….. 260,000

Entry Cash ………………………………………………. 260,000

Analysis To record purchase of computer.

2. Purchase price $260,000

Estimated salvage value 20,000

Depreciable cost $240,000

4.

Journal July 31 Depreciation Expense ……………………………. 5,000

Entry Accumulated Depreciation—

Analysis Computer System ………………………….. 5,000

To record one month’s depreciation expense.

Balance Sheet Income Statement

5. Equipment ………………………………………………………………………… $260,000

4-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 4-9 WORKING BACKWARD: DEPRECIATION

1. Accumulated depreciation on the fixtures is $15,000 on December 31, 2016, which

LO 5 EXERCISE 4-10 PREPAID INSURANCE—ANNUAL ADJUSTMENTS

1. Monthly cost: $72,000/24 months = $3,000

2.

Journal Apr. 1 Prepaid Insurance …………………………………. 72,000

Entry Cash ………………………………………………. 72,000

Analysis To record purchase of 24-month policy.

3.

Journal Dec. 31 Insurance Expense ……………………………….. 27,000

Entry Prepaid Insurance …………………………….. 27,000

Analysis To record expiration of nine months

of insurance (9 months × $3,000).

4. Net income will be overstated by $27,000 if the accountant forgets to record an entry

on December 31, 2016, to recognize an expense (insurance used/expired).

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-11

LO 5 EXERCISE 4-11 SUBSCRIPTIONS

1.

Journal Aug. 1 Cash ……………………………………………………. 27,000

Entry Subscriptions Received in Advance …….. 27,000

2.

Journal Aug. 31 Subscriptions Received in Advance …………. 7,500

Entry Subscription Revenue ……………………….. 7,500

Analysis To record subscriptions for the month of August:

$40,500 + $27,000 – $60,000.

3. If the August 31 adjusting entry for subscription revenue is not recorded, net income

for the month will be understated by $7,500.

4-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

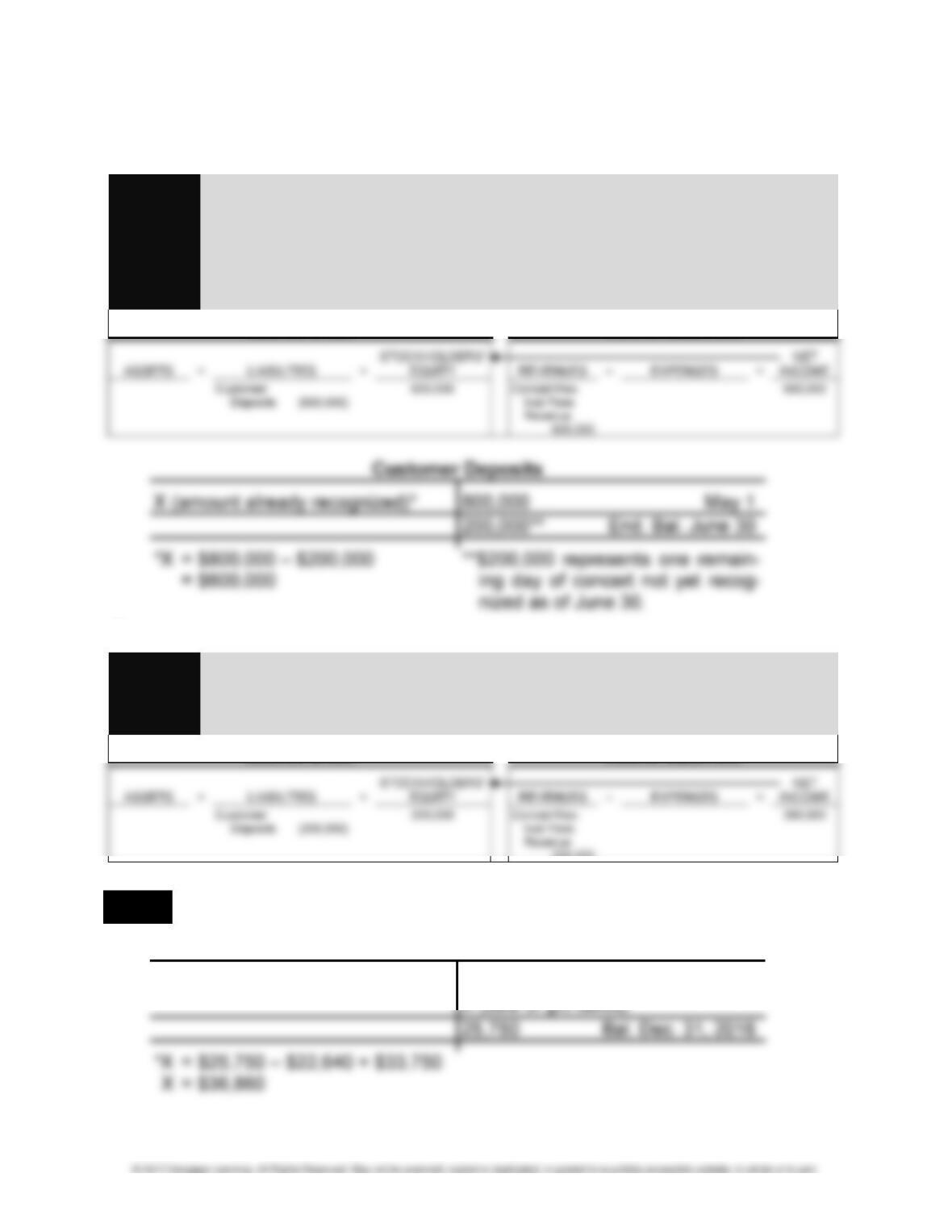

LO 5 EXERCISE 4-12 CUSTOMER DEPOSITS

1.

Journal Apr. 1 Cash ……………………………………………………. 9,000

Entry Customer Deposits …………………………… 9,000

2.

Journal Apr. 30 Customer Deposits ………………………………… 3,000

Entry Legal Fees Revenue …………………………. 3,000

3. If the April 30 adjusting entry is not recorded, net income will be understated by

$3,000.

LO 5 EXERCISE 4-13 CONCERT TICKETS SOLD IN ADVANCE

1.

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-13

EXERCISE 4-13 (Concluded)

2.

Journal June 30 Customer Deposits ………………………………… 600,000*

Entry Concert Festival Fees Revenue ………….. 600,000

Analysis To record concert fees for three days.

*$800,000/4 days = $200,000 per day;

$200,000 × 3 days = $600,000

Balance Sheet Income Statement

3.

Journal July 31 Customer Deposits ………………………………… 200,000

Entry Concert Festival Fees Revenue ………….. 200,000

Analysis To record concert fees for three days.

Balance Sheet Income Statement

200,000

LO 5 EXERCISE 4-14 WORKING BACKWARD: GIFT CARD LIABILITY

Gift Card Liability

Gift cards redeemed 33,750 22,640 Bal. Dec. 31, 2015

4-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 4-15 WAGES PAYABLE

1. Weekly payroll: $10 per hour × 7 hours per day × 5 days × 50 employees = $17,500

2.

Journal Sept. 26 Wages Expense ……………………………………. 17,500

Entry Cash ………………………………………………. 17,500

Analysis To record payment of weekly payroll.

3.

Journal Sept. 30 Wages Expense ……………………………………. 7,000

Entry Wages Payable ………………………………… 7,000

4.

Journal Oct. 3 Wages Expense ……………………………………. 10,500

Entry Wages Payable …………………………………….. 7,000

Analysis Cash ………………………………………………. 17,500

To record payment of weekly payroll.

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-15

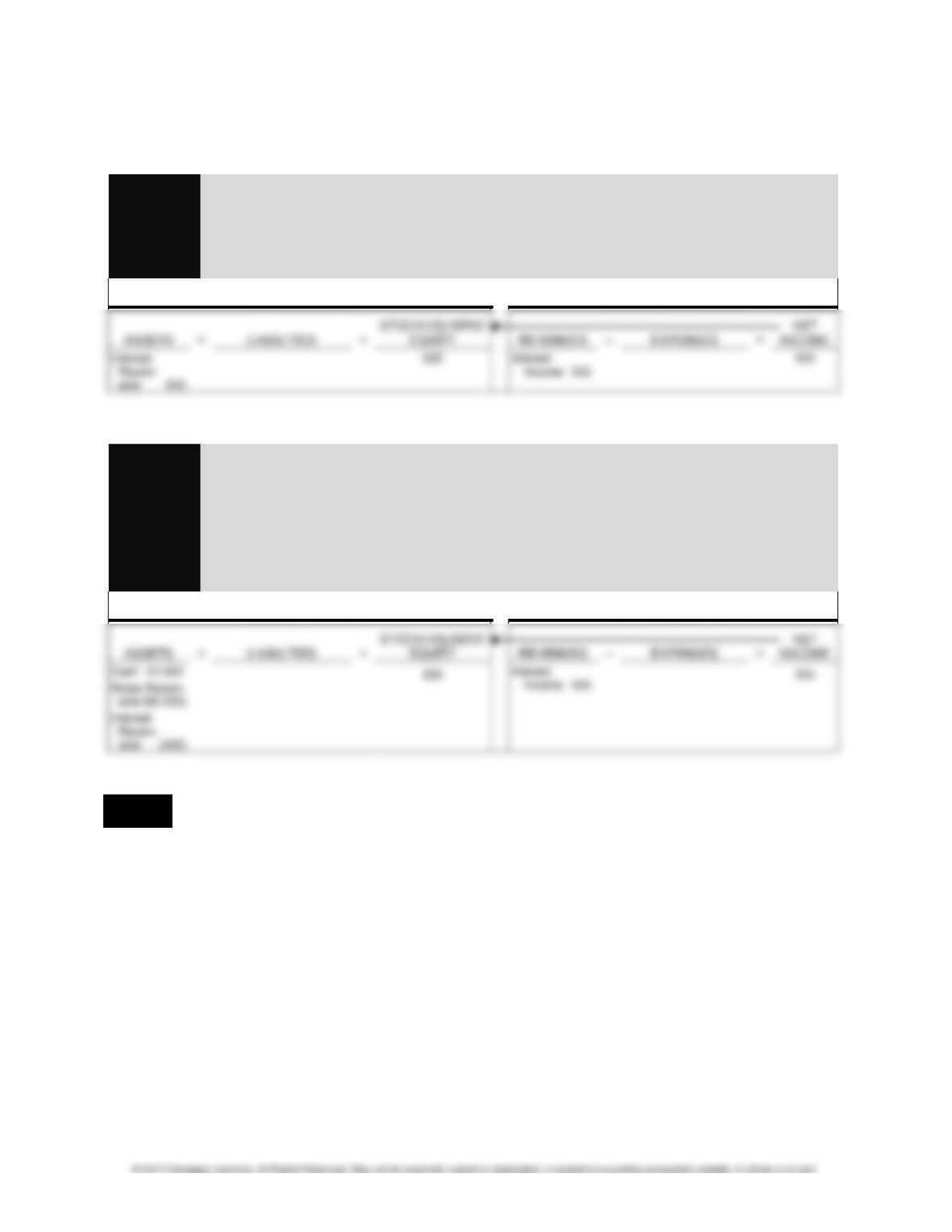

LO 5 EXERCISE 4-16 INTEREST PAYABLE

1.

Journal Mar. 1 Cash ……………………………………………………. 100,000

Entry Notes Payable …………………………………. 100,000

2.

Journal Mar. 31 Interest Expense …………………………………… 1,000

Entry Interest Payable ……………………………….. 1,000

Analysis To accrue interest due on note for one

month: $100,000 × 12% × 30/360.

Journal Apr. 30 Interest Expense …………………………………… 1,000

Entry Interest Payable ……………………………….. 1,000

Analysis To accrue interest due on note for one month.

Balance Sheet Income Statement

4-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 4-16 (Concluded)

3.

Journal May 30 Notes Payable ………………………………………. 100,000

Entry Interest Payable ……………………………………. 2,000

Analysis Interest Expense …………………………………… 1,000

Cash ………………………………………………. 103,000

To record payment of note and interest

at maturity date.

LO 5 EXERCISE 4-17 WORKING BACKWARD: INTEREST PAYABLE

1. The interest rate on the loan is the monthly interest of ($500 × 12 months)/$100,000

= 6%.

2.

Journal Aug. 31 Notes Payable ………………………………………. 100,000

Entry Interest Payable ……………………………………. 500

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-17

LO 5 EXERCISE 4-18 INTEREST PAYABLE—QUARTERLY ADJUSTMENTS

1.

Journal Mar. 1 Cash ……………………………………………………. 100,000

Entry Notes Payable …………………………………. 100,000

2.

Journal Mar. 31 Interest Expense …………………………………… 1,000

Entry Interest Payable ……………………………….. 1,000

Analysis To accrue interest due on note for

one month: $100,000 × 12% × 30/360.

Balance Sheet Income Statement

3.

Journal May 30 Notes Payable ………………………………………. 100,000

Entry Interest Payable ……………………………………. 1,000

Analysis Interest Expense …………………………………… 2,000

4-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 4-19 PROPERTY TAXES PAYABLE—ANNUAL ADJUSTMENTS

1.

Journal 2016

Entry Dec. 31 Property Tax Expense ………………………. 52,500

Analysis Property Taxes Payable ………………. 52,500

2.

Journal 2017

Entry June 1 Property Taxes Payable ………………………. 52,500

1.

Journal June 1 Notes Receivable ………………………………….. 60,000

Entry Cash ………………………………………………. 60,000

Analysis To record 10%, 60-day loan to MaxiDriver Inc.

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-19

EXERCISE 4-20 (Concluded)

2.

Journal June 30 Interest Receivable ……………………………….. 500

Entry Interest Income ………………………………… 500

Analysis To accrue interest due on note for one

month: $60,000 × 10% × 30/360.

Balance Sheet Income Statement

3.

Journal July 31 Cash ……………………………………………………. 61,000

Entry Notes Receivable ……………………………… 60,000

Analysis Interest Receivable …………………………… 500

Interest Income ………………………………… 500

To record collection of note and interest at

maturity date.

Balance Sheet Income Statement

LO 5 EXERCISE 4-21 RENT RECEIVABLE

1. On September 30, Hudson should record $2,000 of rent revenue. Another $2,000 of

revenue should be recorded on October 31.

2.

Journal Oct. 5 Cash ………………………………………………………… 2,000

Entry Rent Receivable …………………………………… 2,000

Analysis To record receipt of cash for rent revenue

in September, but payment received in October.

Journal Oct. 31 Rent Receivable ……………………………………. 2,000

Entry Rent Revenue ………………………………….. 2,000

Analysis To accrue rent revenue for one month.

LO 5 EXERCISE 4-22 WORKING BACKWARD: RENT RECEIVABLE

The amount of cash collected can be determined by examining the T account for Rent

Receivable:

LO 5 EXERCISE 4-23 THE EFFECT OF IGNORING ADJUSTING ENTRIES ON NET INCOME