Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-21

LO 5 EXERCISE 4-24 THE EFFECT OF ADJUSTING ENTRIES ON THE ACCOUNTING

EQUATION

Assets = Liabilities + Stockholders’ Equity

1. D NE D

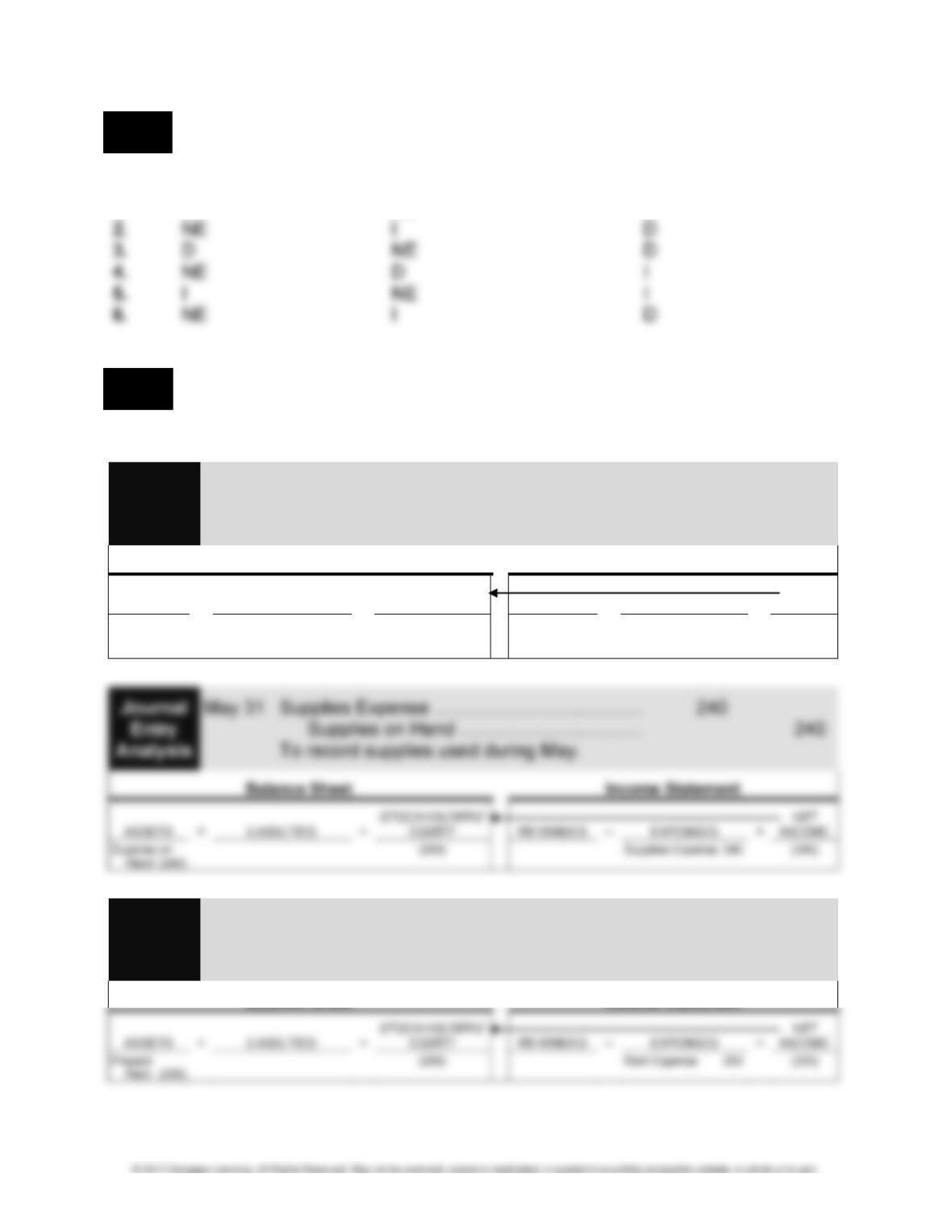

LO 5 EXERCISE 4-25 RECONSTRUCTION OF ADJUSTING ENTRIES FROM UNADJUSTED

AND ADJUSTED TRIAL BALANCES

1. Adjusting entries:

Journal May 31 Accounts Receivable .................................... 2,350

Entry Service Revenue .................................... 2,350

Analysis To accrue revenue during May.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts

Receiv-

able 2,350

2,350

Service Rev-

enue 2,350

2,350

Journal May 31 Rent Expense............................................... 200

Entry Prepaid Rent ........................................... 200

Analysis To record rent expense for the month of May.

Balance Sheet Income Statement

4-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 4-25 (Concluded)

Journal May 31 Depreciation Expense .................................. 400

Entry Accumulated Depreciation ...................... 400

Analysis To record depreciation for the month of May.

Balance Sheet Income Statement

Journal May 31 Wage Expense ............................................. 1,100

Entry Wages Payable ....................................... 1,100

Analysis To accrue wages payable at May 31.

Balance Sheet Income Statement

LO 6 EXERCISE 4-26 THE ACCOUNTING CYCLE

4 Prepare a work sheet.

7 Close the accounts.

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-23

LO 5 EXERCISE 4-27 TRIAL BALANCE

HADLEY REALTY CORPORATION

ADJUSTED TRIAL BALANCE

DECEMBER 31

Debits Credits

Cash ............................................................................. $ 2,460

Accounts Receivable .................................................... 21,230

Office Supplies ............................................................. 1,680

Interest Payable ........................................................... 200

Wages and Salaries Payable ....................................... 470

Notes Payable .............................................................. 20,000

Capital Stock ................................................................ 25,000

Retained Earnings ........................................................ 85,445

Dividends .................................................................... 1,500

4-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 7 EXERCISE 4-28 CLOSING ENTRIES

1. Closing entries:

Advertising Fees Revenue ................................................ 58,500

Interest Revenue ............................................................... 2,700

Income Summary ........................................................ 61,200

To close revenue accounts.

2. If the accountant forgets to close the revenue and expense accounts at the end of

the year, the net income of the following year will be overstated by the amount of net

income of the current year, $4,950. In addition, all the revenue and expense account

balances will carry over to the following year making it very hard to compare finan-

cial statements from one year to the next.

LO 7 EXERCISE 4-29 PREPARATION OF A STATEMENT OF RETAINED EARNINGS

FROM CLOSING ENTRIES

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-25

LO 7 EXERCISE 4-30 RECONSTRUCTION OF CLOSING ENTRIES

Dec. 31 Maintenance Revenue ........................................... 90,000

Income Summary .............................................. 90,000

To close revenue account.

LO 7 EXERCISE 4-31 CLOSING ENTRIES FOR NORDSTROM

Net Sales ................................................................................ 12,166

Credit Card Revenues ............................................................ 374

Income Summary .............................................................. 12,540

To close Net Sales and Credit Card Revenues accounts.

4-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 7 EXERCISE 4-32 CLOSING ENTRIES

1. Closing entries:

Commissions Revenue ..................................................... 54,000

Income Summary ........................................................ 54,000

To close revenue account.

2. Closing entries serve two purposes. First, the balances in revenue, expense, and

dividend accounts are returned to zero to start the following period. Second, the net

income and the dividends of the period are transferred to Retained Earnings. Clos-

ing entries are recorded at the end of the period.

LO 8 EXERCISE 4-33 THE DIFFERENCE BETWEEN A FINANCIAL STATEMENT AND A

WORK SHEET (APPENDIX)

Total debits on the work sheet .......................................................... $255,000

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-27

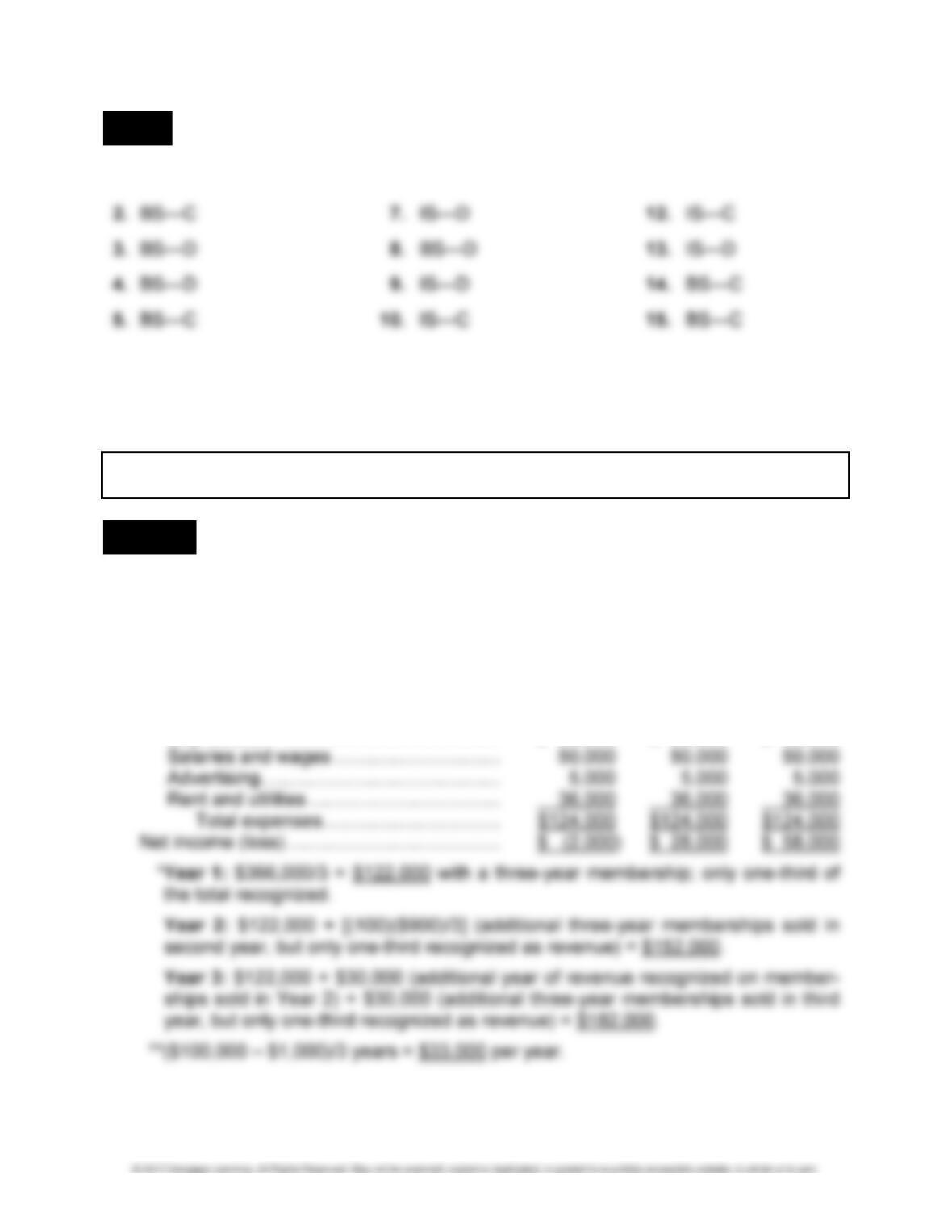

LO 8 EXERCISE 4-34 TEN-COLUMN WORK SHEET (APPENDIX)

1. BS—C 6. BS—D 11. BS—D

MULTI-CONCEPT EXERCISES

LO 1,2,3 EXERCISE 4-35 REVENUE RECOGNITION, CASH AND ACCRUAL BASES

1. Accrual-basis income statements:

HATHAWAY HEALTH CLUB

INCOME STATEMENTS

Year 1 Year 2 Year 3

Sales* .......................................................... $122,000 $152,000 $182,000

Expenses:

Depreciation** ......................................... $ 33,000 $ 33,000 $ 33,000

4-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 4-35 (Concluded)

2. Under the revenue recognition principle, revenue is recognized not when cash is re-

ceived but rather when the performance obligation is satisfied. It is satisfied with the

LO 4,5 EXERCISE 4-36 DEPRECIATION EXPENSE

1. Depreciation expense for 2016:

2. Certainly, it would be less costly in terms of the time spent by the accountant to ex-

pense all costs rather than treat certain ones as assets to be written off over their

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-29

LO 4,5 EXERCISE 4-37 ACCRUAL OF INTEREST ON A LOAN

1.

Journal July 1 Cash ............................................................. 50,000

Entry Notes Payable ........................................ 50,000

Analysis To record two-month, 12% bank loan.

Balance Sheet Income Statement

Journal Aug. 31 Interest Payable ........................................... 500

Entry Notes Payable .............................................. 50,000

Analysis Interest Expense .......................................... 500

Cash ....................................................... 51,000

To record repayment of principal and

interest on bank loan.

Balance Sheet Income Statement

4-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEMS

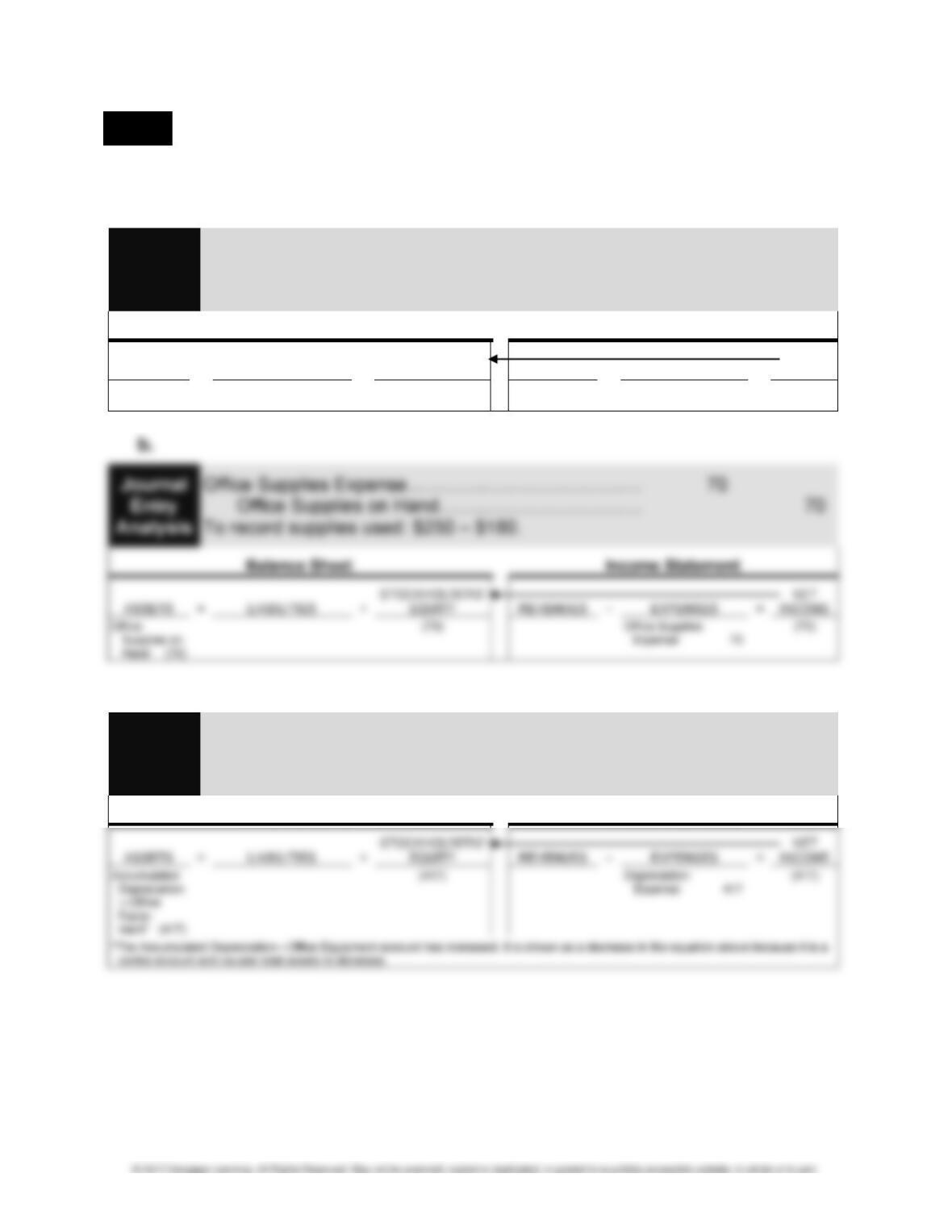

LO 5 PROBLEM 4-1 ADJUSTING ENTRIES

Adjusting entries on March 31, 2016:

a.

b.

Journal Supplies Expense ....................................................... 660

Entry Office Supplies on Hand ....................................... 660

Analysis To record supplies used: $1,280 + $750 – $1,370.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Office

Supplies on

Hand (660)

(660)

Supplies

Expense 660*

(660)

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-31

PROBLEM 4-1 (Continued)

c.

Journal Depreciation Expense—Office Equipment .................. 800

Entry Accumulated Depreciation—Office Equipment .... 800

Analysis To record depreciation: ($62,600 – $5,000) × 1/72.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

d.

Journal Wages Expense ......................................................... 3,800

Entry Wages Payable .................................................... 3,800

Analysis To accrue wages: $950 × 4 days = $3,800.

Balance Sheet Income Statement

e.

Journal Rent Collected in Advance ......................................... 2,500

Entry Rent Revenue ...................................................... 2,500

Analysis To recognize rent.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Rent Collected in

Advance (2,500)

2,500

Rent Rev-

enue 2,500

2,500

f.

4-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 4-1 (Concluded)

g.

Journal Income Tax Expense .................................................. 3,900

Entry Income Tax Payable ............................................. 3,900

Analysis To record estimated income taxes.

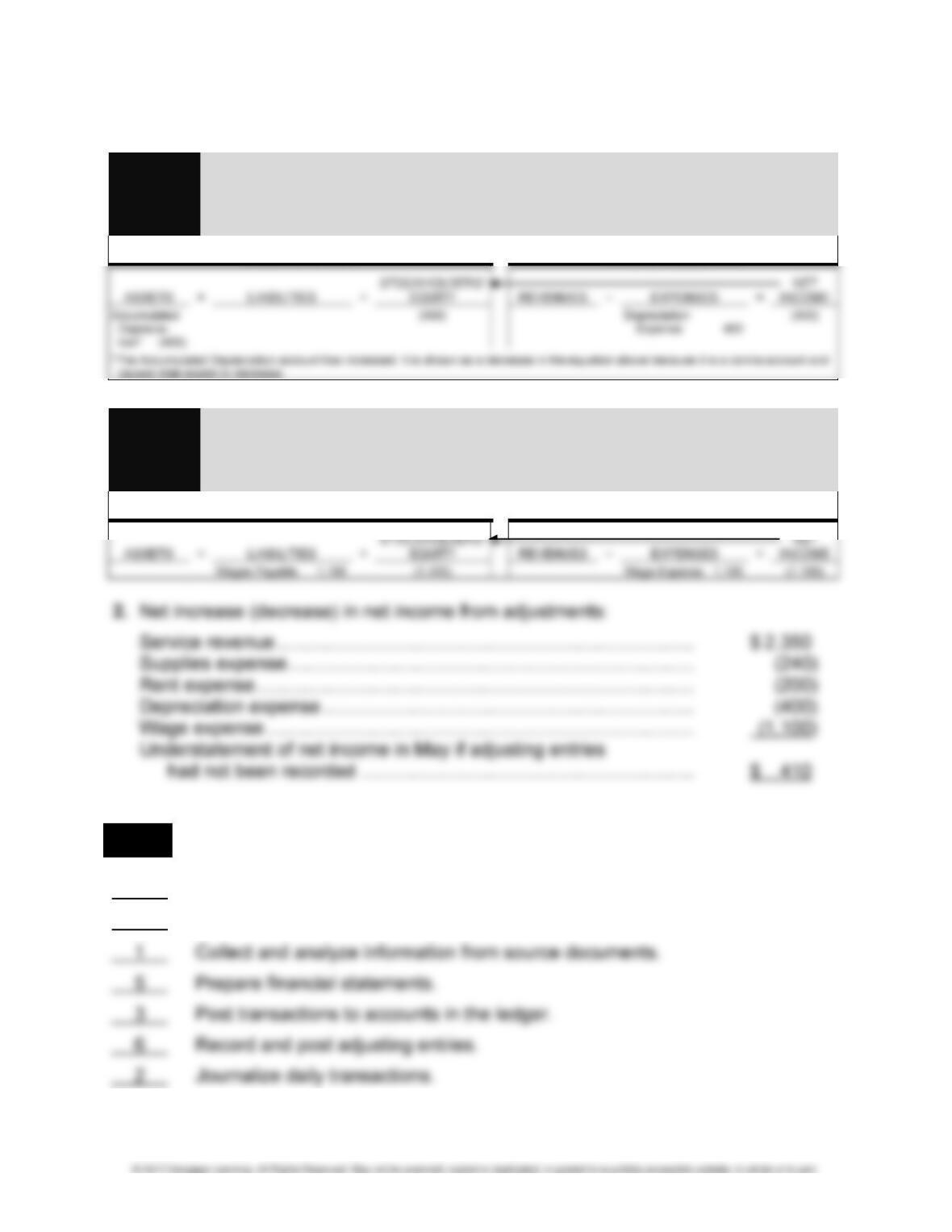

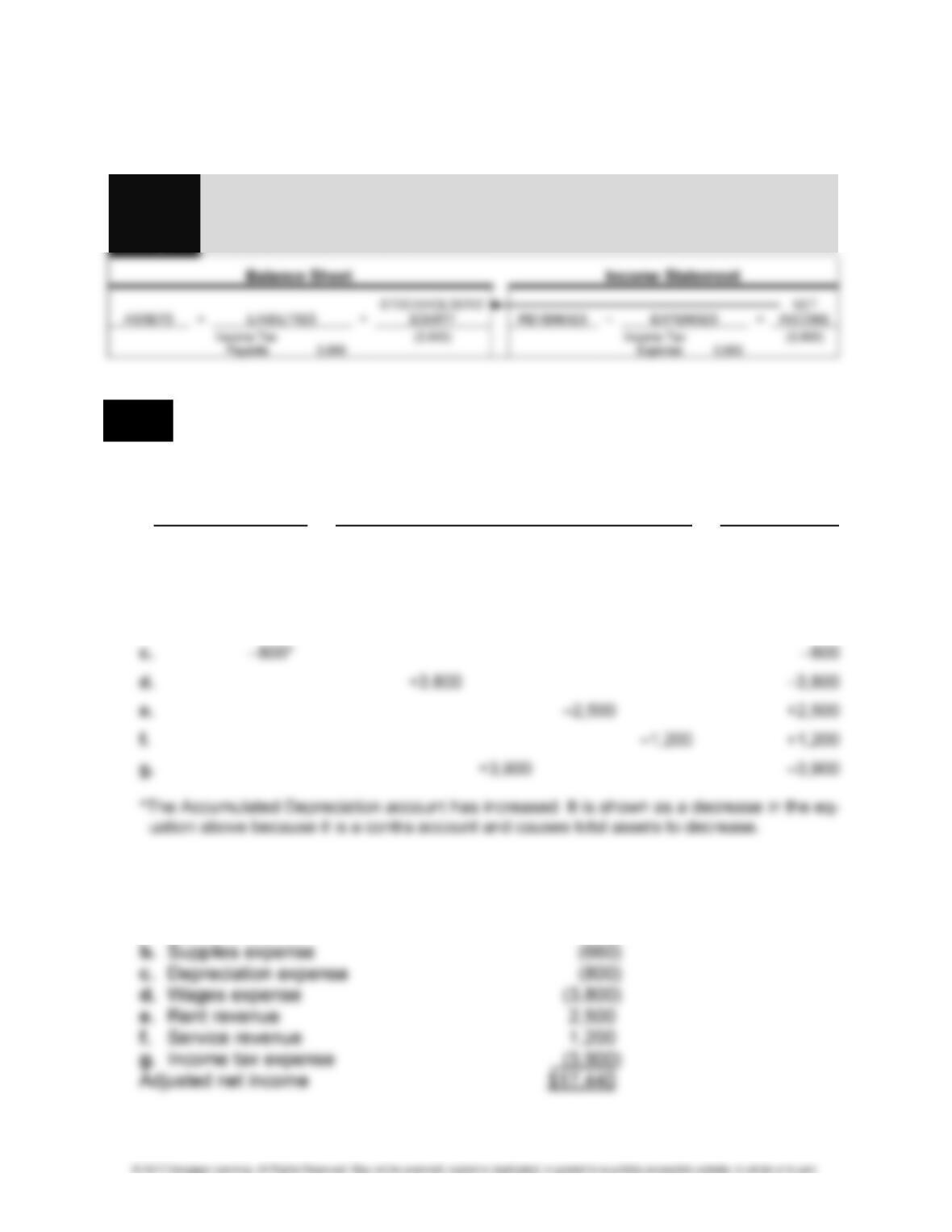

LO 5 PROBLEM 4-2 EFFECTS OF ADJUSTING ENTRIES ON THE ACCOUNTING

EQUATION

1. Effects of adjusting entries on the accounting equation:

Owners’

Assets = Liabilities + Equity

Rent

Office Accumulated Interest Wages Income Tax Collected Customer Capital Retained

Supplies Depreciation Payable Payable Payable in Advance Deposits Stock Earnings

a. +100 –100

b. –660 –660

2. Unadjusted net income $23,000 (Amount given in problem)

Effect of adjustments:

a. Interest expense (100)

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-33

LO 5 PROBLEM 4-3 ADJUSTING ENTRIES—ANNUAL ADJUSTMENTS

1. Adjusting entries:

a.

Journal Depreciation Expense—Computer ............................. 2,950

Entry Accumulated Depreciation—Computer ................ 2,950

Analysis To record annual depreciation expense:

($15,000 – $250)/5 years.

Balance Sheet Income Statement

b.

Journal Supplies Expense ....................................................... 19,350

Entry Office Supplies on Hand ....................................... 19,350

Analysis To record supplies used during year:

$3,600 + $17,600 – $1,850.

Balance Sheet Income Statement

4-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 4-3 (Continued)

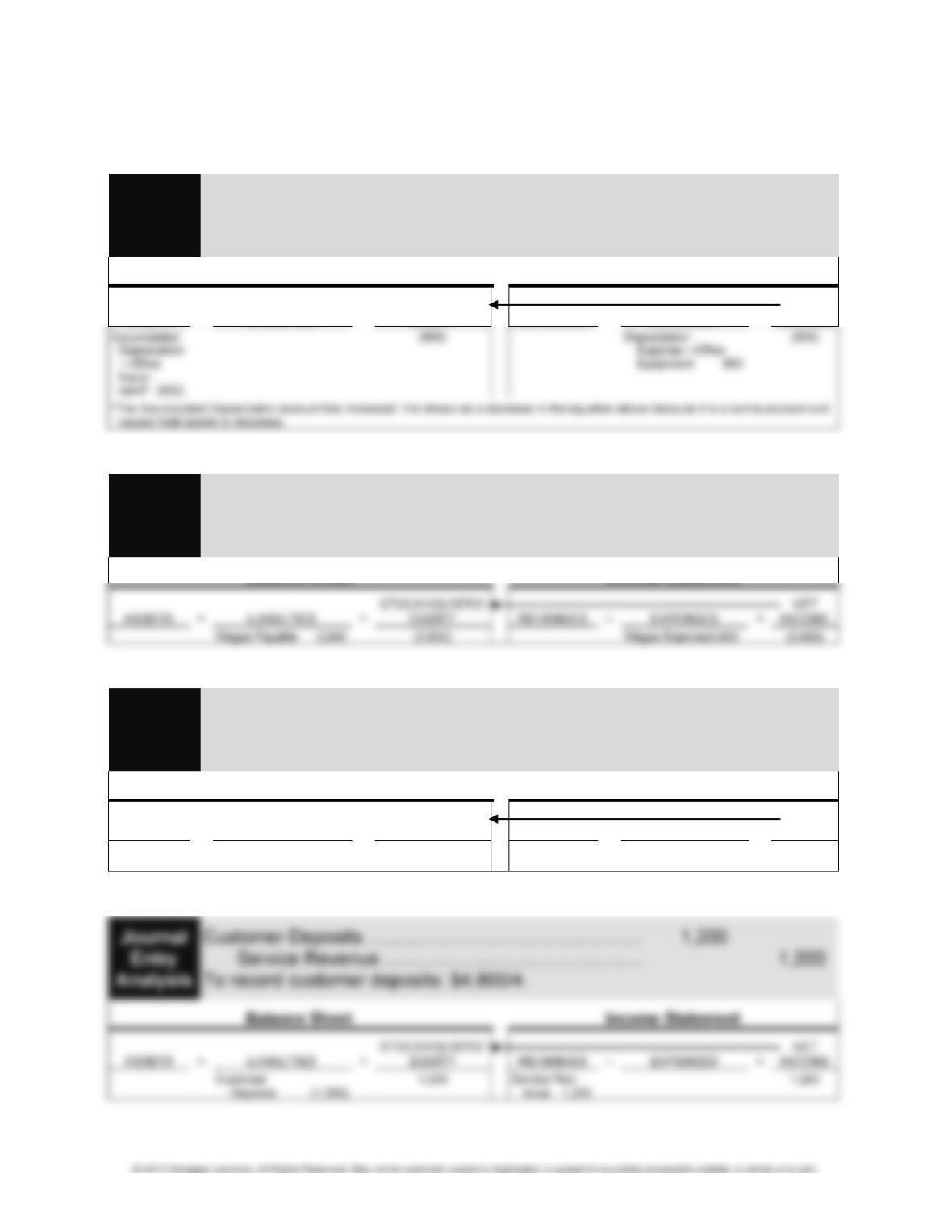

c.

Journal Customer Deposits ..................................................... 20,000

Entry Fees Revenue ...................................................... 20,000

Analysis To record customer deposits between August

and December: ($24,000/6 months) × 5 months.

d.

Journal Rent Expense ............................................................. 5,400

Entry Prepaid Rent ........................................................ 5,400

Analysis To record rent expense for November through

December: $2,700 × 2.

Balance Sheet Income Statement

PROBLEM 4-3 (Concluded)

f.

Journal Wage Expense ........................................................... 500

Entry Wages Payable .................................................... 500

Analysis To accrue wages payable at year-end for one day:

Friday.

Balance Sheet Income Statement

LO 5 PROBLEM 4-4 RECURRING AND ADJUSTING ENTRIES

Debit Credit Debit Credit

a. 1 12, 13 i. 8 1

b. 5 1 j. 17 9

4-36 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 4-5 USE OF ACCOUNT BALANCES AS A BASIS FOR ADJUSTING

ENTRIES—ANNUAL ADJUSTMENTS

1. Adjusting entries on December 31, 2016:

a.

b.

Journal Rent Collected in Advance ......................................... 3,500

Entry Rent Revenue ...................................................... 3,500

Analysis To recognize rent: $6,000 × 7/12.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Rent Collected in

Advance (3,500)

3,500

Rent Rev-

enue 3,500

3,500

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-37

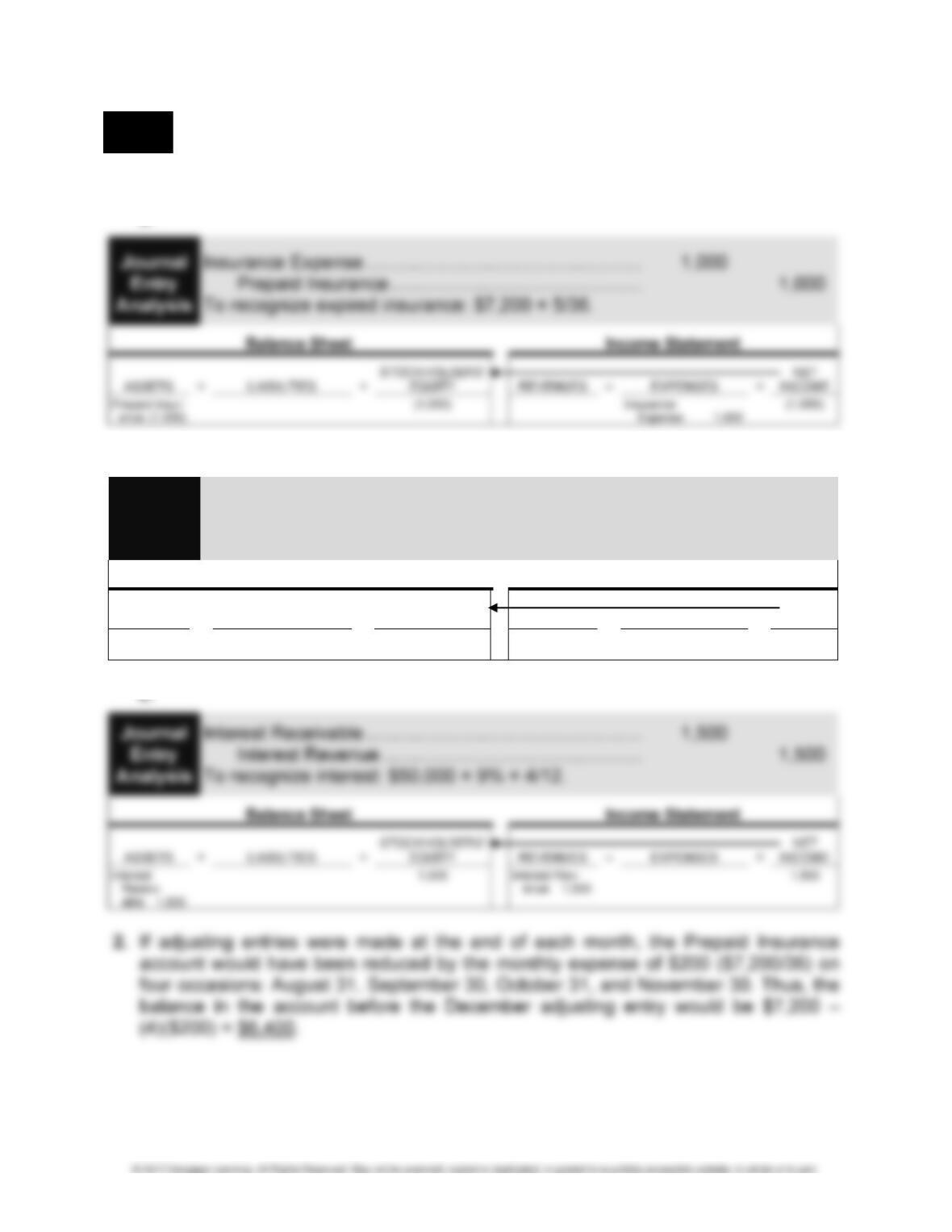

LO 5 PROBLEM 4-6 USE OF A TRIAL BALANCE AS A BASIS FOR ADJUSTING ENTRIES

1. Adjusting entries on April 30, 2016:

a.

Journal Insurance Expense ..................................................... 50

Entry Prepaid Insurance ................................................ 50

Analysis To recognize one month’s insurance expense.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Prepaid Insur-

ance (50)

(50)

Insurance

Expense 50

(50)

c.

Journal Depreciation Expense ................................................. 417

Entry Accumulated Depreciation—Office Equipment .... 417

Analysis To record depreciation: $50,000 × 1/120.

Balance Sheet Income Statement

4-38 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 4-6 (Continued)

d.

Journal Depreciation Expense ................................................. 200

Entry Accumulated Depreciation—Auto ........................ 200

Analysis To record depreciation: $12,000 × 1/60.

e.

Journal Deferred Commissions ............................................... 4,500

Entry Commissions Revenue ........................................ 4,500

Analysis To record commissions revenue: $9,500 – $5,000.

Balance Sheet Income Statement

g.

Journal Interest Expense ......................................................... 20

Entry Interest Payable ................................................... 20

Analysis To record interest on note payable.

Balance Sheet Income Statement

CHAPTER 4 • INCOME MEASUEMENT AND ACCRUAL ACCOUNTING 4-39

PROBLEM 4-6 (Concluded)

h.

Journal Salaries Expense ........................................................ 2,500

Entry Salaries Payable .................................................. 2,500

Analysis To record salaries not yet paid.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Salaries Payable 2,500

(2,500)

Salaries

Expense 2,500

(2,500)

2. The office equipment was purchased on April 1, 2015, and has been depreciated for

LO 5 PROBLEM 4-7 EFFECTS OF ADJUSTING ENTRIES ON THE ACCOUNTING

EQUATION

1. Effects of adjusting entries on accounting equation:

Assets = Liabilities + Equity

Accounts Office Prepaid Accumulated Deferred Interest Salaries Capital Retained

Receivable Supplies Insurance Depreciation Commissions Payable Payable Stock Earnings

a. –50 –50

b. –70 –70

2. Net increase (decrease) in net income from adjustments:

a. ............................................................................................... $ (50)

b. ............................................................................................... (70)

4-40 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 4-8 RECONSTRUCTION OF ADJUSTING ENTRIES FROM ACCOUNT

BALANCES

1.

Journal June 30 Insurance Expense ........................................... 150

Entry Prepaid Insurance ........................................ 150

2. Cost of policy was $150 × 36 months = $5,400.

3.

Journal June 30 Depreciation Expense ............................................ 80

Entry Accumulated Depreciation—Equipment ........... 80

Analysis To record depreciation expense: $1,360 – $1,280.

4. Estimated useful life in months: $9,600/$80 month = 120 months.

5.

Journal June 30 Interest Expense .......................................... 144

6. Interest rate: ($144 per month × 12 months)/$9,600 = 18%. The monthly rate is

18%/12 months = 1.5%.