Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 4

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 4-1 “Data flow diagrams and systems flowcharts provide redundant pictures of an

information system (or business process). We don’t need both.” Discuss fully.

ANS. Logical data flow diagrams (DFDs) present only the logical elements of an

information system. By excluding the physical elements, the logical DFD allows

us to concentrate on what a system is doing without being distracted by how the

DQ 4-2 “It is easier to learn to prepare data flow diagrams, which use only a few

symbols, than it is to learn to prepare systems flowcharts, which use a number of

different symbols.” Discuss fully.

2 Solutions for Chapter 4

ANS. Compare the DFD symbols in Figure 4.1 to the flowcharting symbols in Figure

4.6 and you will probably conclude that it is easy to learn the DFD symbols.

Examine Figure 4.7 and see that there are several standard routines used in

DQ 4-3 Describe the who, what, where, and how of the following scenario. A customer

gives his purchase to a sales clerk, who enters the sale in a cash register and puts

the money in the register drawer. At the end of the day, the sales clerk gives the

cash and the register tape to the cashier.

ANS. Who: The sales clerk performs the information processing activities.

What: (1) Give purchase to sales clerk.

DQ 4-4 Why are many correct logical DFD solutions possible? Why is only one correct

physical DFD solution possible?

ANS. For each sensible grouping of logical activities, there is a correct logical DFD.

And, because many sensible groupings are possible, multiple correct solutions

DQ 4-5 Explain why a flow from a higher– to a lower-numbered bubble on a logical DFD

is a physical manifestation of the system. Give an example.

Accounting Information Systems, 10e 3

ANS. If we feel that we must send a data flow from one bubble on a logical DFD to a

bubble on that diagram with a lower number, then we must have a picture in our

DQ 4-6 Compare and contrast the purpose of and techniques used in drawing physical

DFDs and logical DFDs.

ANS. We draw physical DFDs to depict a system’s entities—both internal and

external—and to characterize the communications between those entities. We

DQ 4-7 “If we document a system with a system flowchart and data flow diagrams, we

have overdocumented the system.” Discuss fully.

ANS. We don’t agree with this statement. Each tool depicts different aspects of a system

and is used for different purposes.

DQ 4-8 “Preparing a table of entities and activities as the first step in documenting

systems seems to be unnecessary and unduly cumbersome. It would be a lot easier

to bypass this step and get right to the necessary business of actually drawing the

diagrams.” Do you agree? Discuss fully.

4 Solutions for Chapter 4

ANS. We don’t agree. With practice, preparation of a table of entities and activities is

DQ 4-9 “PCAOB Audit Standard No. 5 (AS5) paragraph 37 and Statement on Auditing

Standard Section 319 (AU 319) paragraph 75 suggest that management, business

process owners, and auditors prepare and analyze systems documentation to

understand the flow of transactions through a process and to identify and assess

the effectiveness of the design of internal controls. However, organizations,

internal audit departments, and public accounting firms have developed their own

methods for documenting systems. Therefore, I am not going to learn to prepare

systems documentation until I know exactly what technique I will need to use in

my job.” Do you agree? Discuss fully.

ANS. We don’t agree. After you learn any systems documentation technique, learning

the next technique will be easier. There are several skills that are developed while

DQ 4-10 “Because there are computer-based documentation products that can draw data

flow diagrams and systems flowcharts, learning to draw them manually is a waste

of time.” Do you agree? Discuss fully.

ANS. We disagree, partly. We have used several computer-based documentation

packages and believe that you must know something about drawing DFDs and

Short Problems

Accounting Information Systems, 10e 5

Note to Instructors: Additional problems can be created from the diagrams and

solutions for these problems. For example, you could provide the students with a

narrative and a partially completed diagram requiring that the students fill in the

missing parts of the diagram. Or you could provide the diagram and a partially

completed narrative and require that the students fill in the blanks in the narrative.

Finally, you can provide students with a table of entities and activities and require

that they prepare one or more diagrams.

6 Solutions for Chapter 4

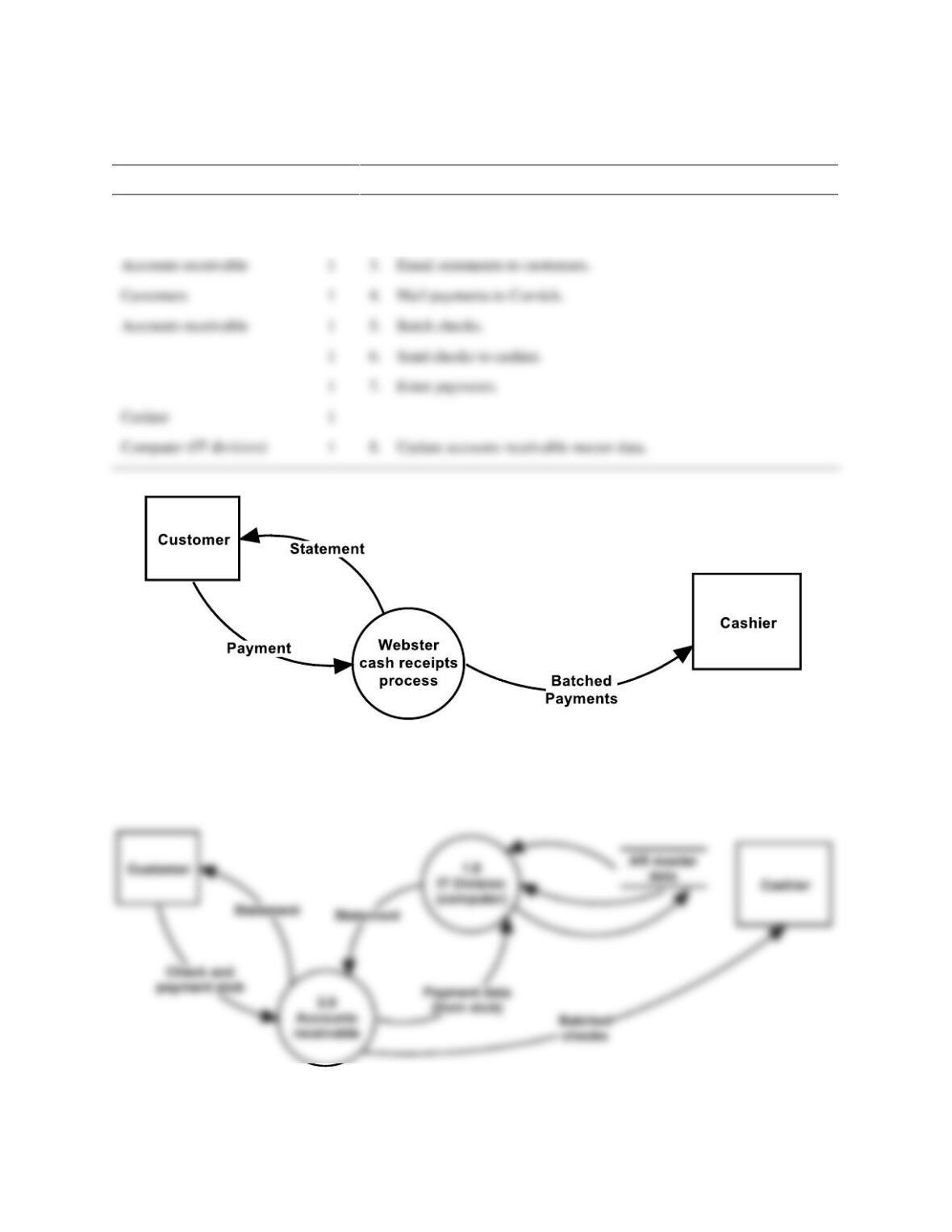

SP 4-1 ANS. a. Table of Entities and Activities for Cornick, Inc.

Entities

Para

Activities

IT division

1

1. Print statements.

1

2. Send statements to accounts receivable department.

FIGURE SM-4.1 Short Problem 1 part b solution—context diagram—for Cornick, Inc.

FIGURE SM-4.2 Short Problem 2 solution—physical DFD—for Cornick, Inc.

Accounts receivable

1

3. Email statements to customers.

Customers

1

4. Mail payments to Cornick.

Accounts receivable

1

5. Batch checks.

1

6. Send checks to cashier.

Cashier

1

Computer (IT division)

1

8. Update accounts receivable master data.

Accounting Information Systems, 10e 7

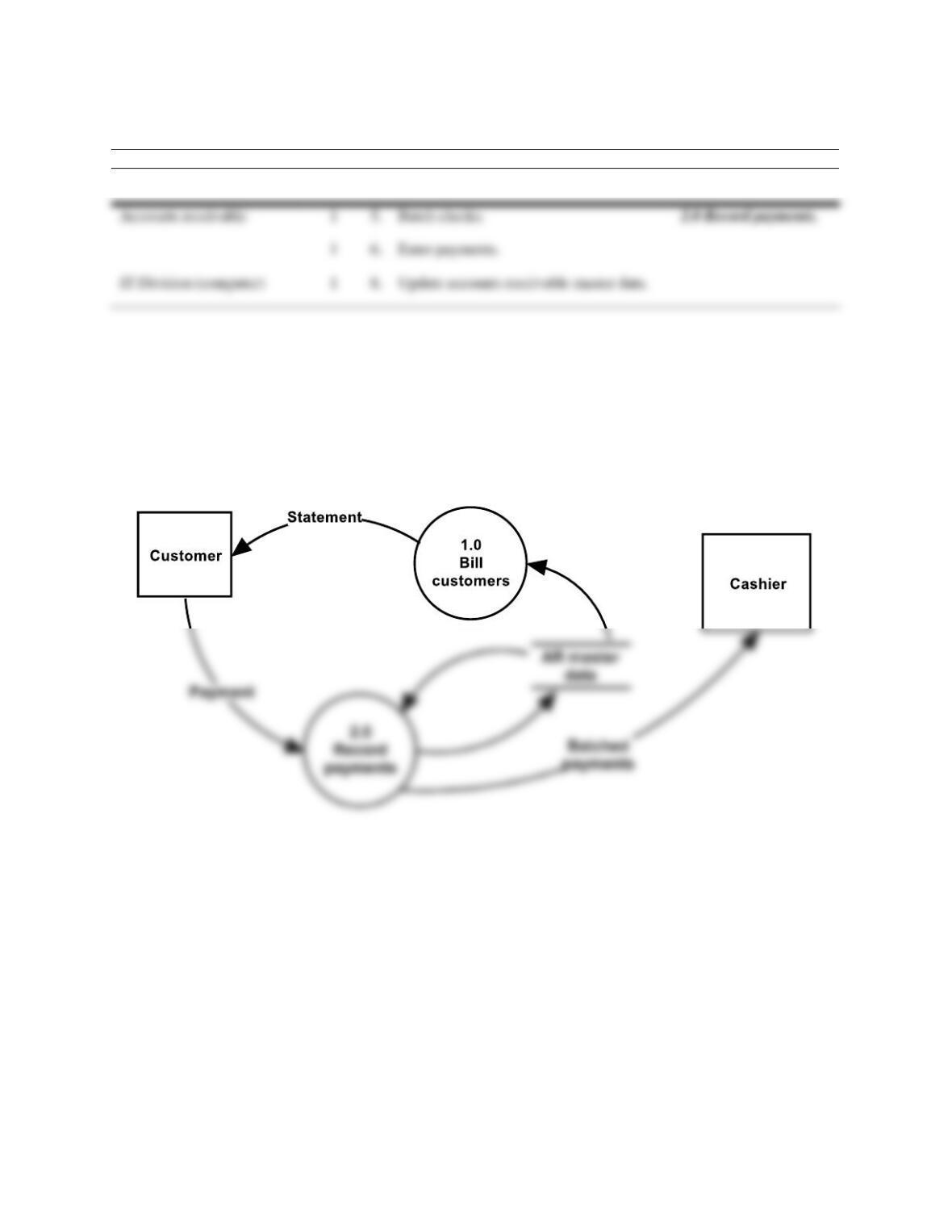

SP 4-3 ANS. a. Annotated Table of Entities and Activities for Cornick, Inc.

Entities

Para

Activities

Process

IT Division (computer)

1

1. Print statements.

1.0 Bill customers.

FIGURE SM-4.3 Short Problem 3 part b solution—logical DFD—for Cornick, Inc.

8 Solutions for Chapter 4

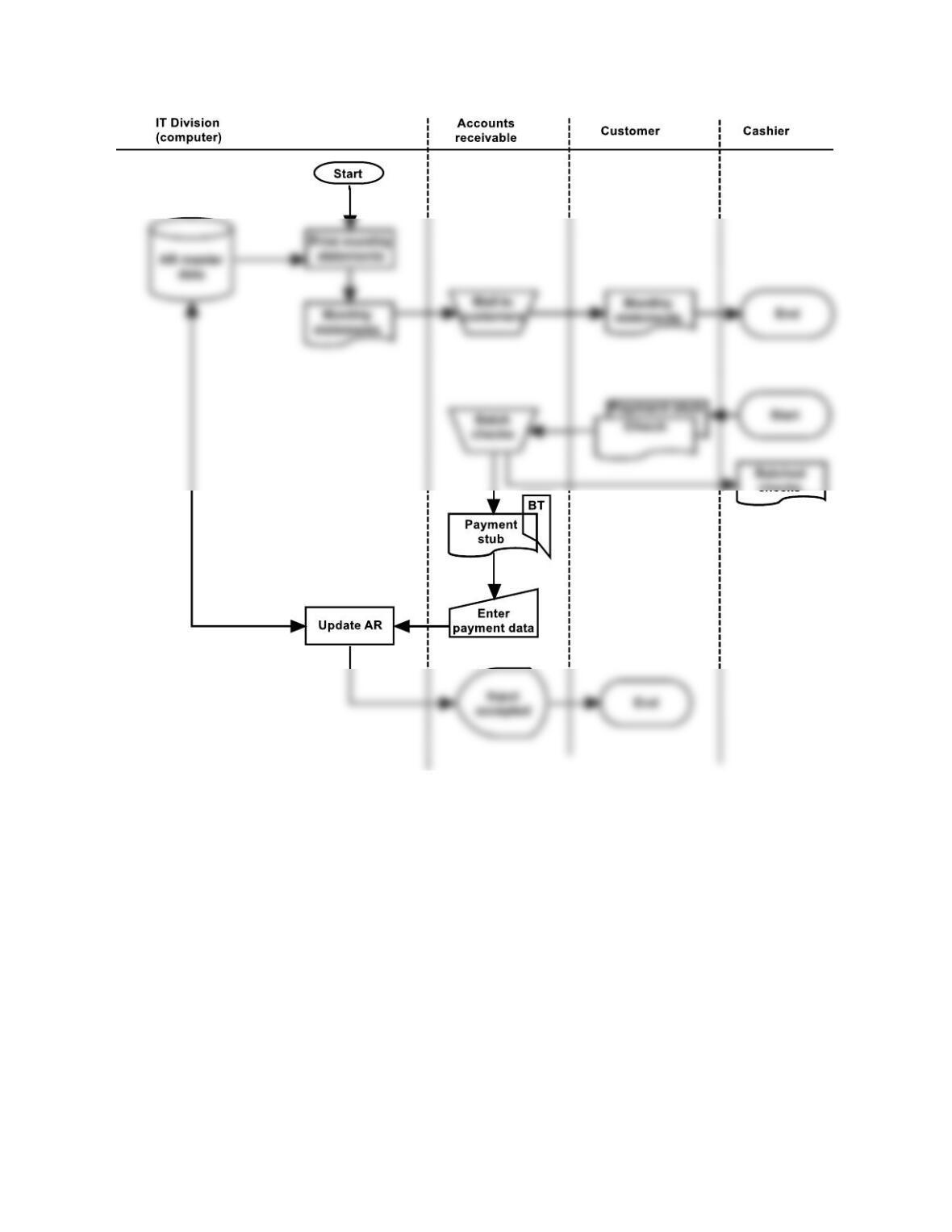

FIGURE SM-4.4 Short Problem 4 solution—systems flowchart—for Cornick, Inc.

Accounting Information Systems, 10e 9

SP 4-5 ANS.

a. 7

h. 9

b. no match

i. no match

Problems

P 4-1 ANS. At the company’s sales office, sales representatives answer customer calls and

enter customer orders into the computer. The computer accesses the Inventory

master data (on disk) to determine the availability and prices for the items

requested. Also, the computer accesses the Customer master data (on disk) to

P 4-2 ANS. Customers contact this company with a request for services. A contract is

prepared and filed in the Contract file, and a copy of the contract is given to the

customer.

Using an Hours Worked report received from the Operations office, the hours

worked are recorded into the Hours Worked file.

c. 8

j. 3

d. no match

k. 10

e. 4

l. 2

f. 1

m. no match

g. 6

n. 5

10 Solutions for Chapter 4

P 4-3 ANS. As a customer order is received at the Central sales office, a sales clerk enters the

order into the computer. The computer reviews the order, checks the customer’s

credit (by comparing the credit limit in the Customer master data to the amount of

the order plus the balance outstanding on the Accounts receivable master data and

the orders outstanding on the Sales order master data) and logs the order on the

System log.

Problems 4 through 7 Solutions for Good Buy, Inc.

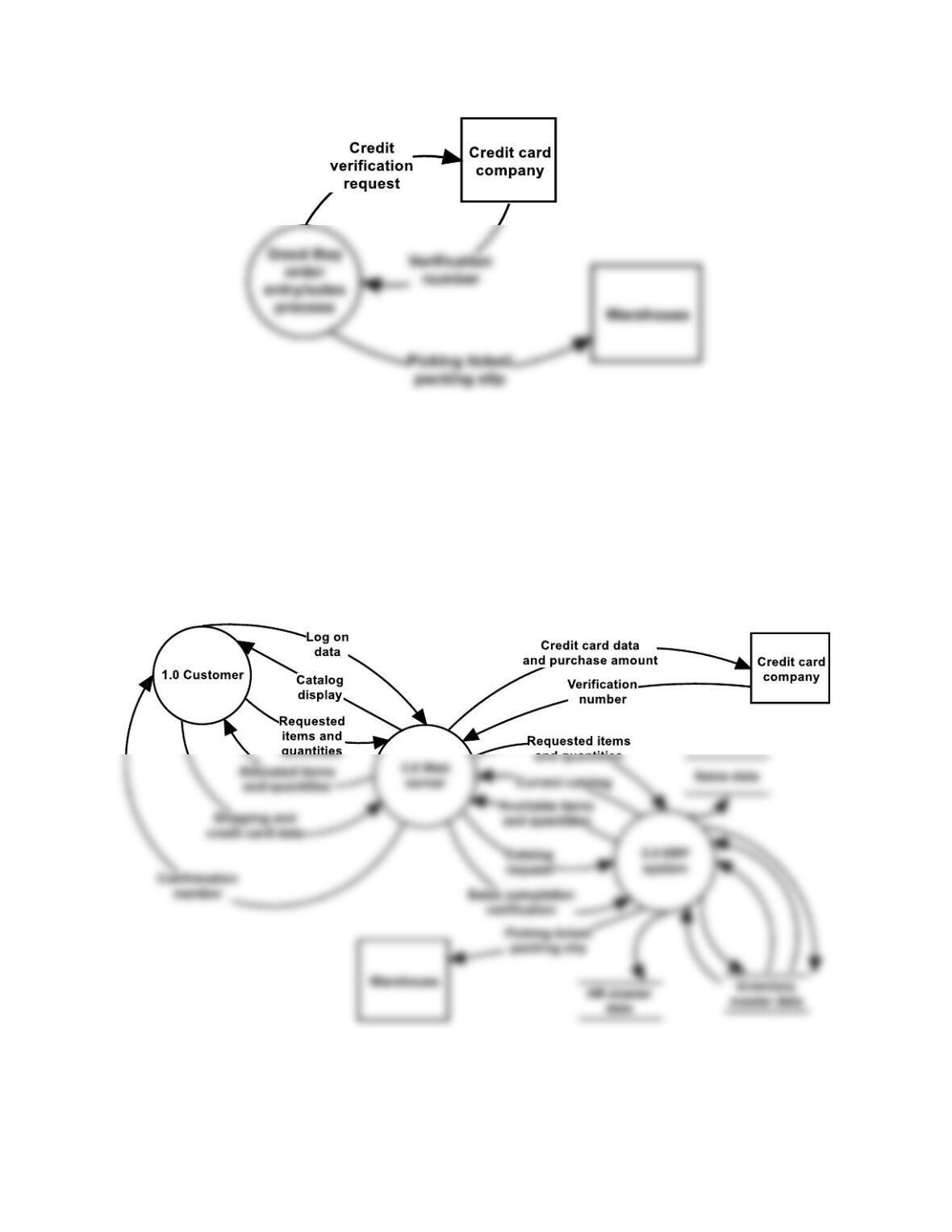

P 4-4 ANS. a. Table of Entities and Activities for Good Buy, Inc.

Entities

Para

Activities

Customer

1

1. Log on to Web site.

Web server

1

2. Request current catalog.

ERP system

1

3. Send current catalog (assumes read and format catalog data).

Web server

1

4. Display catalog.

Web server

1

6. Edit customer input (items and quantities) for accuracy.

1

7. Send requested items and quantities to ERP system.

ERP system

1

8. Allocate inventory.

1

9. Send allocated items and quantities to Web server.

Web server

1

10. Display allocated items and quantities on customer screen.

Customer

1

11. Verify that order is correct.

1

12. Enter shipping and credit card information.

Credit card company

1

15. Send verification number to Web server.

Web server

1

16. Display confirmation number on customer screen.

1

17. Notify ERP system that sales have been completed.

ERP system

1

18. Change inventory status from allocated to sold.

1

19. Print picking ticket/packing slip in warehouse.

1

20. Record sale and accounts receivable.

Warehouse

12 Solutions for Chapter 4

FIGURE SM-4.5 Problem 4 part b solution—context diagram—for Good Buy, Inc.

FIGURE SM-4.6 Problem 5 solution—physical DFD—for Good Buy, Inc.