SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Nov. 1

Prepaid Rent

5,200

Cash

5,200

To record rent paid in advance.

Nov. 1

Prepaid Insurance

9,600

Cash

9,600

To record insurance paid in advance.

Dec. 1

5,400

Unearned Revenue

5,400

To record cash collected for future services.

Dec. 1

10,000

Unearned Revenue

10,000

To record cash collected for future services.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Rent Expense

2,600*

Prepaid Rent

2,600*

To record rent expense.

Dec. 31

Insurance Expense

3,200*

Prepaid Insurance

3,200*

To record insurance expense.

Dec. 31

Unearned Revenue

1,800

Service Revenue

1,800

advance.

Dec. 31

Unearned Revenue

2,000

Service Revenue

2,000

advance.

P3-44B, cont.

* Calculations:

Adjusting Journal Entry One:

$5,200

Rent prepaid on November 1 for 4 months

4

Months

$1,300

Rent expense per month

$1,300

Rent expense per month

Months

$2,600

Rent expense for November and December

Adjusting Journal Entry Two:

$9,600

Insurance prepaid on November 1 for 6 months

6

Months

$1,600

Insurance expense per month

$1,600

Insurance expense per month

Months

$3,200

Insurance expense for November and December

Requirement 3

Prepaid Rent

Rent Expense

Nov. 1 5,200

2,600 Dec. 31

Dec. 31 2,600

Bal. 2,600

Bal. 2,600

Insurance Expense

Nov. 1 9,600

3,200 Dec. 31

Dec. 31 3,200

Bal. 6,400

Bal. 3,200

Unearned Revenue

Dec. 31 1,800

5,400 Dec. 1

1,800 Dec. 31

Dec. 31 2,000

10,000 Dec. 1

2,000 Dec. 31

11,600 Bal.

3,800 Bal.

P3-44B, cont.

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Nov. 1

Rent Expense

5,200

Cash

5,200

To record rent paid in advance.

Nov. 1

Insurance Expense

9,600

Cash

9,600

To record insurance paid in advance.

Dec. 1

5,400

5,400

To record cash collected for future services.

Dec. 1

10,000

10,000

To record cash collected for future services.

Dec. 31

Prepaid Rent

2,600*

2,600*

To record prepaid rent.

Dec. 31

Prepaid Insurance

6,400*

6,400*

To record prepaid insurance.

Dec. 31

Service Revenue

3,600*

3,600*

To record unearned revenue.

Dec. 31

Service Revenue

8,000*

8,000*

To record unearned revenue.

P3-44B, cont.

* Calculations:

Adjusting Journal Entry One:

$5,200

Rent prepaid on November 1 for 4 months

4

Months

$1,300

Rent expense per month

$1,300

Rent expense per month

months

$2,600

Rent still prepaid on December 31

Adjusting Journal Entry Two:

$9,600

Insurance prepaid on November 1 for 6 months

6

Months

$1,600

Insurance expense per month

$1,600

Insurance expense per month

months

$6,400

Insurance still prepaid on December 31

Adjusting Journal Entry Three:

Collected in advance on December 1 for 3 months

Revenue earned during December

Revenue still unearned on December 31

Collected in advance on December 1 for 5 months

Revenue still unearned on December 31

P3-44B, cont.

Prepaid Rent

Rent Expense

Dec. 31 2,600

Nov. 1 5,200

2,600 Dec. 31

Bal. 2,600

Bal. 2,600

Insurance Expense

Dec. 31 6,400

Nov. 1 9,600

6,400 Dec. 31

Bal. 6,400

Bal. 3,200

Unearned Revenue

3,600 Dec. 31

5,400 Dec. 1

8,000 Dec. 31

10,000 Dec. 1

11,600 Bal.

3,800 Bal.

Requirement 5

Continuing Problem

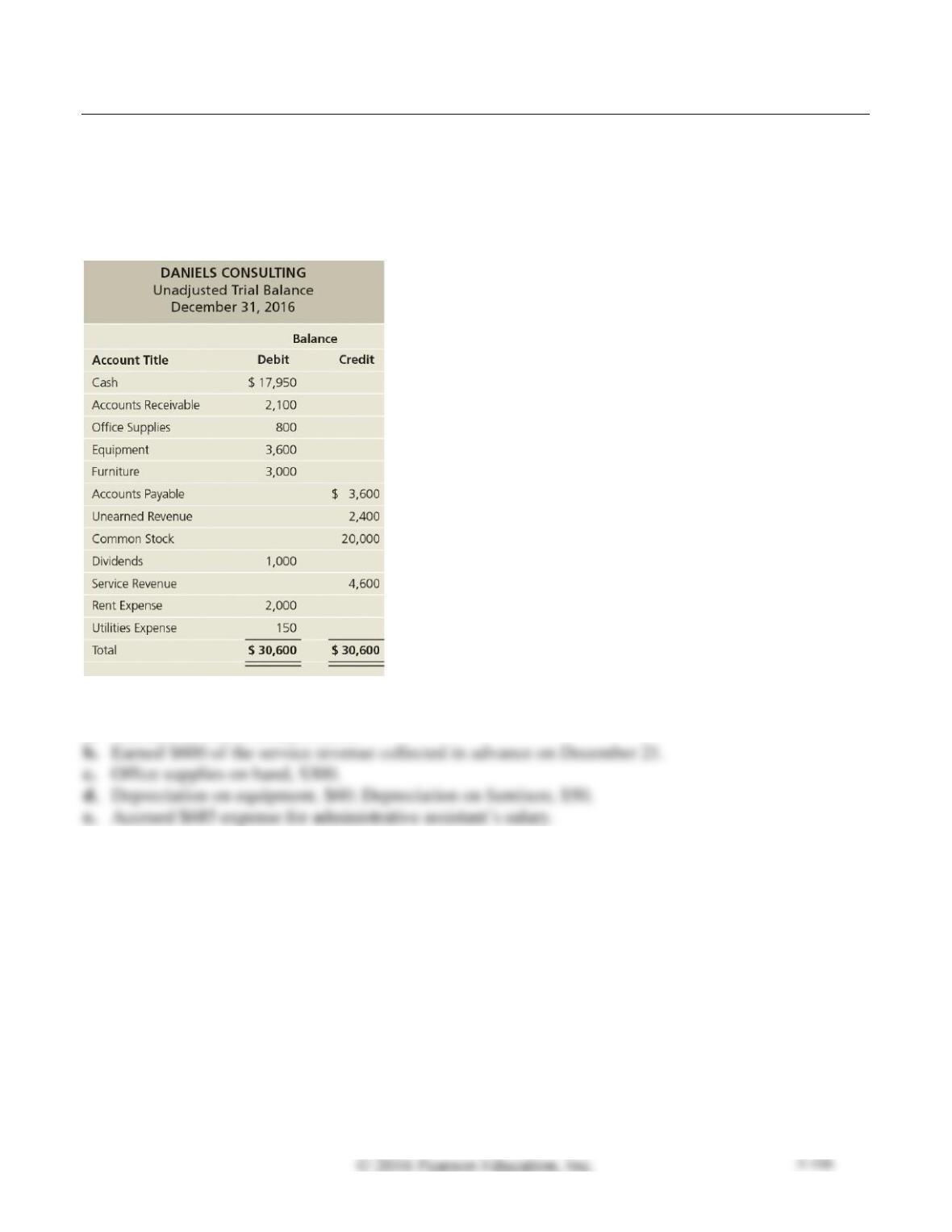

P3-45 Preparing adjusting entries and preparing an adjusted trial balance

This problem continues the Daniels Consulting situation from Problem P2-41 of Chapter 2. You will

need to use the unadjusted trial balance and posted T-accounts that you prepared in Problem P2-41. The

unadjusted trial balance at December 31, 2016, is duplicated below:

At December 31, the business gathers the following information for the adjusting entries:

a. Accrued service revenue, $1,500.

Requirements

1. Journalize and post the adjusting entries using the T-accounts that you completed in Problem P2-41.

In the T-accounts, denote each adjusting amount as Adj. and an account balance as Balance.

2. Prepare an adjusted trial balance as of December 31, 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Accounts Receivable

1,500

Service Revenue

1,500

To accrue service revenue.

Dec. 31

Unearned Revenue

Service Revenue

advance.

Dec. 31

Supplies Expense

To record supplies used.

Dec. 31

Depreciation Expense— Equipment

Depreciation Expense—Furniture

To record depreciation on equipment and furniture.

Dec. 31

Salaries Expense

To accrue salaries expense.

* Calculations:

$800

Office Supplies prior to adjustment

(300)

Office Supplies remaining

$500

Supplies Expense (cost of supplies used)

P3-45, cont.

Requirement 1

Accounts Payable

2,000 Dec. 2

3,000 Dec. 4

3,600 Dec. 3

800 Dec. 5

150 Dec. 12

3,600 Balance

200 Dec. 26

1,000 Dec. 30

685 Adj.

685 Balance

Accounts Receivable

Unearned Revenue

Dec. 9 2,500

400 Dec. 28

Adj. 600

2,400 Dec. 21

Adj. 1,500

1,800 Balance

Balance 3,600

Dec. 5 800

500 Adj.

20,000 Dec. 2

Balance 300

20,000 Balance

Dec. 3 3,600

Balance 3,600

Balance 1,000

Furniture

Service Revenue

Dec. 4 3,000

2,500 Dec. 9

Balance 3,000

2,100 Dec. 18

1,500 Adj.

Accumulated Depreciation—Equipment

600 Adj.

60 Adj.

6,700 Balance

60 Balance

50 Adj.

Balance 2,000

50 Balance

P3-45, cont.

Supplies Expense

Adj. 500

Balance 500

Salaries Expense

Adj. 685

Balance 685

P3-45, cont.

Requirement 2

DANIELS CONSULTING

Adjusted Trial Balance

December 31, 2016

Account Title

Balance

Debit

Credit

Cash

$ 17,950

Accounts Receivable

3,600

Office Supplies

Equipment

3,600

Accumulated Depreciation—Equipment

Accumulated Depreciation—Furniture

50

Accounts Payable

Unearned Revenue

Salaries Payable

Common Stock

Dividends

1,000

Service Revenue

Rent Expense

2,000

Utilities Expense

Supplies Expense

Salaries Expense

Depreciation Expense—Equipment

Depreciation Expense—Furniture

Practice Set

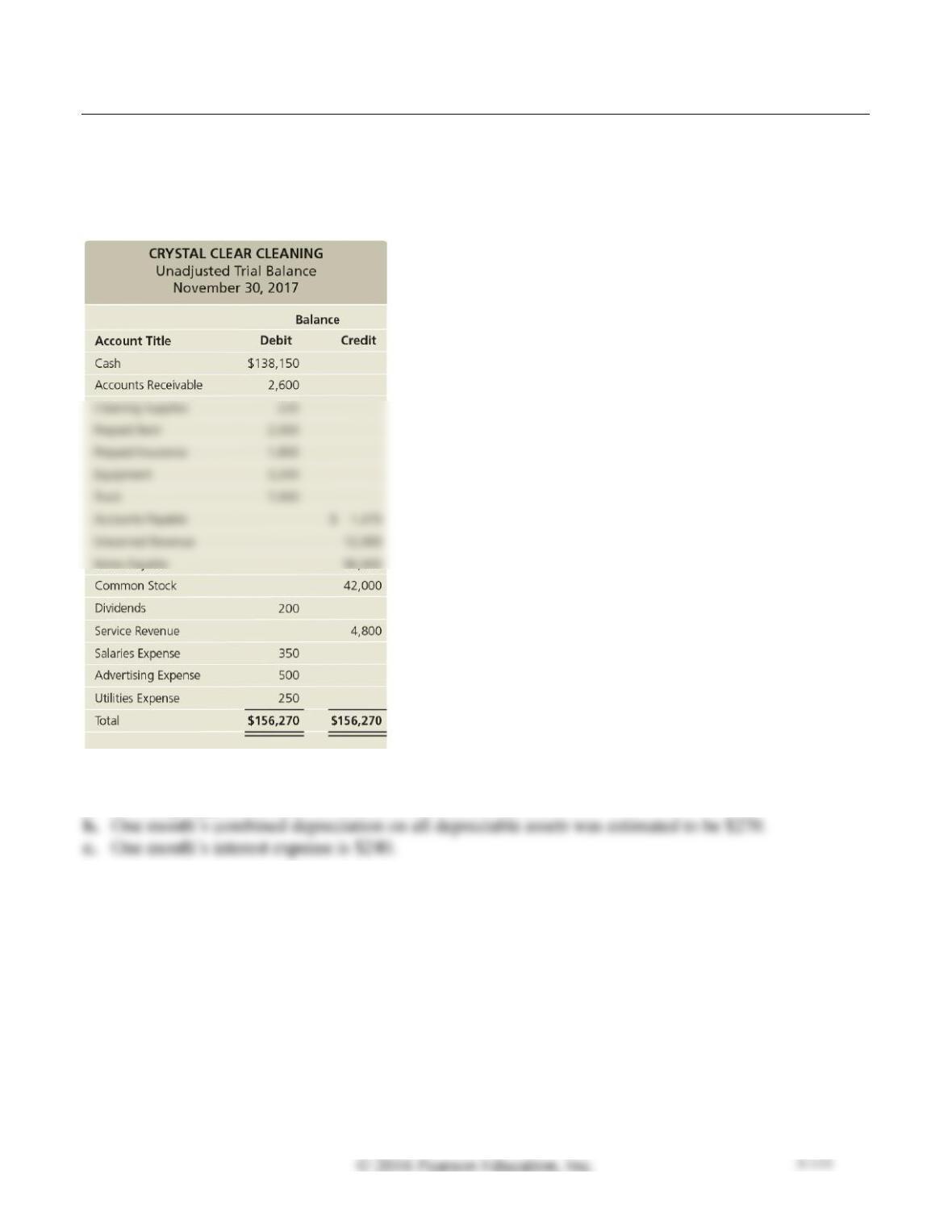

P3-46 Preparing adjusting entries and preparing an adjusted trial balance

This problem continues the Crystal Clear Cleaning situation from Problem P2-42 of Chapter 2. Start

from the unadjusted trial balance that Crystal Clear Cleaning prepared at November 30, 2017:

Consider the following adjustment data:

a. Cleaning supplies on hand at the end of November were $30.

Requirements

1. Using the data provided from the trial balance, the previous adjustment information, and the

information from Chapter 2 (P2-42), prepare all required adjusting journal entries at November 30.

2. Prepare an adjusted trial balance as of November 30 for Crystal Clear Cleaning.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Nov. 30

Supplies Expense

190*

Cleaning Supplies

190*

To record supplies used.

Nov. 30

Depreciation Expense

To record depreciation on depreciable assets.

Nov. 30

Rent Expense

500*

Prepaid Rent

500*

To record rent expense.

Nov. 30

Insurance Expense

150*

Prepaid Insurance

150*

To record insurance expense.

Nov. 30

Unearned Revenue

500*

500*

advance.

Nov. 30

Interest Expense

240*

Interest Payable

240*

To accrue interest expense.

* Calculations:

Adjusting Journal Entry One:

$220

Cleaning Supplies prior to adjustment

Cleaning Supplies remaining

$190

Supplies Expense (cost of supplies used)

P3-46, cont.

Adjusting Journal Entry Three:

$2,000

Rent prepaid on November 2 for 4 months

4

Months

$ 500

Rent expense for November

$1,800

Insurance prepaid on November 3 for 12 months

$ 150

Insurance expense for November

Collected in advance on November 16 for one year

Months

Service revenue earned per month

Thus,

$1,000

Service revenue earned per month

2

$ 500

Service revenue earned November 16 through November 30

Adjusting Journal Entry Six:

$96,000 borrowed on Nov. 20, 9% interest rate per year

Thus,

= $240 interest expense for Nov. 20 through Nov. 30

P3-46, cont.

Requirement 2

CRYSTAL CLEAR CLEANING

Adjusted Trial Balance

November 30, 2017

Account Title

Balance

Debit

Credit

Cash

$ 138,150

Accounts Receivable

2,600

Cleaning Supplies

Prepaid Rent

1,500

Prepaid Insurance

1,650

Equipment

3,200

Truck

7,000

Accumulated Depreciation

Accounts Payable

1,470

Unearned Revenue

Interest Payable

Notes Payable

Common Stock

Dividends

Service Revenue

5,300

Salaries Expense

Advertising Expense

Utilities Expense

Supplies Expense

Depreciation Expense

Rent Expense

Insurance Expense

Interest Expense

Critical Thinking

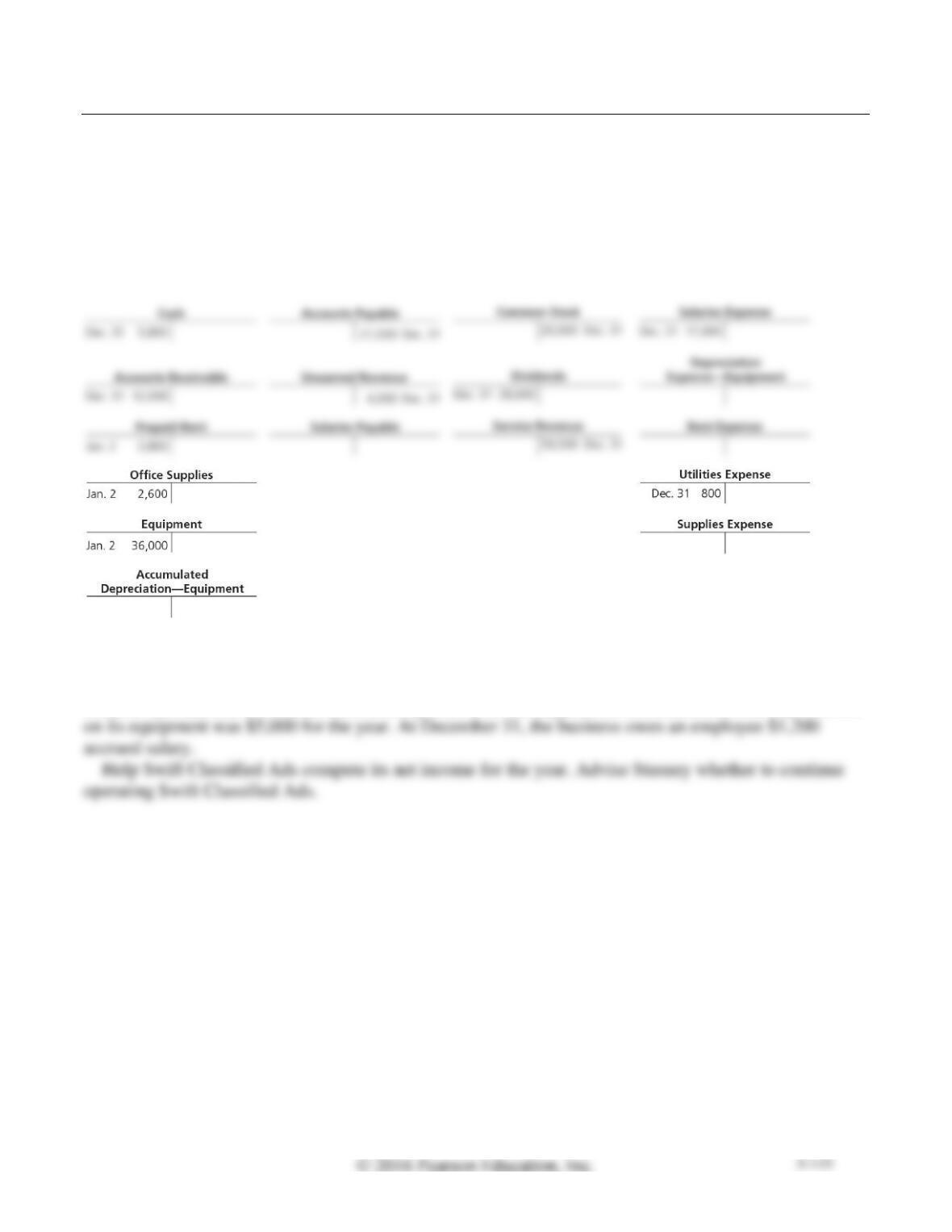

Decision Case 3-1

One year ago, Tyler Stasney founded Swift Classified Ads. Stasney remembers that you took an

accounting course while in college and comes to you for advice. He wishes to know how much net

income his business earned during the past year in order to decide whether to keep the company going.

His accounting records consist of the T-accounts from his ledger, which were prepared by an accountant

who moved to another city. The ledger at December 31 follows. The accounts have not been adjusted.

Stasney indicates that at year-end, customers owe the business $1,600 for accrued service revenue.

These revenues have not been recorded. During the year, Swift Classified Ads collected $4,000 service

revenue in advance from customers, but the business earned only $900 of that amount. Rent expense for

the year was $2,400, and the business used up $1,700 of the supplies. Swift determines that depreciation

SOLUTION

Swift Classified Ads

Income Statement

Year Ended December 31

Revenues:

Service Revenue [$59,500 + $1,600 adj + $900 adj]

$ 62,000

Expenses:

Salaries Expense [$17,000 + $1,200 adj]

$ 18,200

Depreciation Expense [adj]

Rent Expense [adj]

Utilities Expense

Supplies Expense [adj]

Ethical Issue 3-1

The net income of Steinbach & Sons, a landscaping company, decreased sharply during 2016. Mort

Steinbach, owner and manager of the company, anticipates the need for a bank loan in 2017. Late in

2016, Steinbach instructs the company’s accountant to record $2,000 service revenue for landscape

services for the Steinbach family, even though the services will not be performed until January 2017.

Steinbach also tells the accountant not to make the following December 31, 2016, adjusting entries:

Requirements

1. Compute the overall effects of these transactions on the company’s reported net income for 2016.

2. Why is Steinbach taking this action? Is his action ethical? Give your reason, identifying the parties

helped and the parties harmed by Steinbach’s action.

3. As a personal friend, what advice would you give the accountant?

SOLUTION

Requirement 1

Net income is overstated by $3,300.

Requirement 2

Students’ responses will vary. Illustrative answers follow.

Requirement 3

Students’ responses will vary. Illustrative answers follow.

Fraud Case 3-1

XM, Ltd. was a small engineering firm that built high-tech robotic devices for electronics

manufacturers. One very complex device was partially completed at the end of 2016. Barb McLauren,

head engineer, knew the experimental technology was a failure and XM would not be able to complete

the $20,000,000 contract next year. However, the corporation was getting ready to be sold in January.

She told the controller that the device was 80% complete at year-end and on track for successful

completion the following spring; the controller accrued 80% of the contract revenue at December 31,

2016. McLauren sold the company in January 2017 and retired. By mid-year, it became apparent that

XM would not be able to complete the project successfully and the new owner would never recoup his

investment.

Requirements

1. For complex, high-tech contracts, how does a company determine the percentage of completion and

the amount of revenue to accrue?

2. What action do you think was taken by XM in 2017 with regard to the revenue that had been accrued

the previous year?

SOLUTION

Requirement 1

Financial Statement Case 3-1

Starbucks Corporation—like all other businesses—makes adjusting entries at year-end in order to

measure assets, liabilities, revenues, and expenses properly.

Requirements

1. Which asset accounts might Starbucks record adjusting entries for?

2. Which liability accounts might Starbucks record adjusting entries for?

3. Review Note 1 (Property, Plant, and Equipment) in the Notes to Consolidated Financial Statements.

How are property, plant, and equipment carried on the balance sheet? How is depreciation of these

assets calculated? What is the range of useful lives used when depreciating these assets?

SOLUTION

Requirement 1

Starbucks Corporation might record adjusting entries for the following assets: Accounts receivables,

Communication Activity 3-1

In 75 words or fewer, explain adjusting journal entries.

SOLUTION

Under accrual basis accounting, adjusting entries are completed at the end of the accounting period to