3-1

CHAPTER 3

Processing Accounting Information

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Explain the difference between external and internal events. 1 10 Easy

Module 2

4. Define the concept of a general ledger and understand the 5 10 Easy

use of the T account as a method for analyzing transactions. 10* 20 Mod

11* 10 Mod

12* 10 Mod

13* 10 Easy

Module 3

6. Explain the purposes of a journal and the posting process. 14* 20 Mod

15* 30 Mod

16* 20 Mod

17* 15 Mod

3-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Explain the difference between external and internal events. 1 20 Easy

5* 45 Mod

Module 2

4. Define the concept of a general ledger and understand the 7* 60 Mod

use of the T account as a method for analyzing transactions. 8* 60 Mod

10* 45 Mod

11** 30 Diff

Module 3

6. Explain the purposes of a journal and the posting process. 9* 30 Mod

12* 75 Mod

13* 75 Mod

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Explain the difference between external and internal events. 3* 20 Mod

Module 2

4. Define the concept of a general ledger and understand the use 1 20 Mod

of the T account as a method for analyzing transactions.

Module 3

6. Explain the purposes of a journal and the posting process. 2* 15 Mod

3* 20 Mod

3-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 1 EXERCISE 3-1 TYPES OF EVENTS

1. E 3. NR 5. I 7. E

LO 2 EXERCISE 3-2 SOURCE DOCUMENTS MATCHED WITH TRANSACTIONS

LO 3 EXERCISE 3-3 THE EFFECT OF TRANSACTIONS ON THE ACCOUNTING EQUATION

Assets = Liabilities + Owners’ Equity

1. NE* NE NE

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-5

LO 3 EXERCISE 3-4 TYPES OF TRANSACTIONS

Type Examples of Transactions

1. a. Purchase supplies on credit.

b. Purchase land in exchange for promissory note.

4. a. Pay dividend to stockholders.

b. Pay wages to employees.

Many other examples exist; those given are representative of possible answers.

LO 4 EXERCISE 3-5 BALANCE SHEET ACCOUNTS AND THEIR USE

1. Notes Payable 7. Accounts Payable

LO 5 EXERCISE 3-6 NORMAL ACCOUNT BALANCES

1. Debit 7. Credit

3-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 3-7 NORMAL ACCOUNT BALANCES FOR VAIL RESORTS

Item Classified as Normal Balance

1. Trade receivables, net of allowances A D

2. Segment operating expense—Lodging E D

LO 5 EXERCISE 3-8 DEBITS AND CREDITS

The debits and credits are reversed in this entry. The correct entry is:

Journal June 5 Cash ………………………………………………. 12,450

Entry Accounts Receivable …………………… 10,000

Analysis Sales Revenue …………………………… 2,450

To record cash received on June 5:

$10,000 on account and $2,450 in

cash sales.

Balance Sheet Income Statement

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-7

LO 7 EXERCISE 3-9 TRIAL BALANCE

SPENCER CORPORATION

TRIAL BALANCE

DECEMBER 31

Debits Credits

Cash ………………………………………………………………….. $ 10,500

Accounts Receivable ……………………………………………. 5,325

Office Supplies ……………………………………………………. 500

Land ………………………………………………………………….. 50,000

Automobiles ……………………………………………………….. 9,200

Buildings …………………………………………………………….. 150,000

3-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT EXERCISES

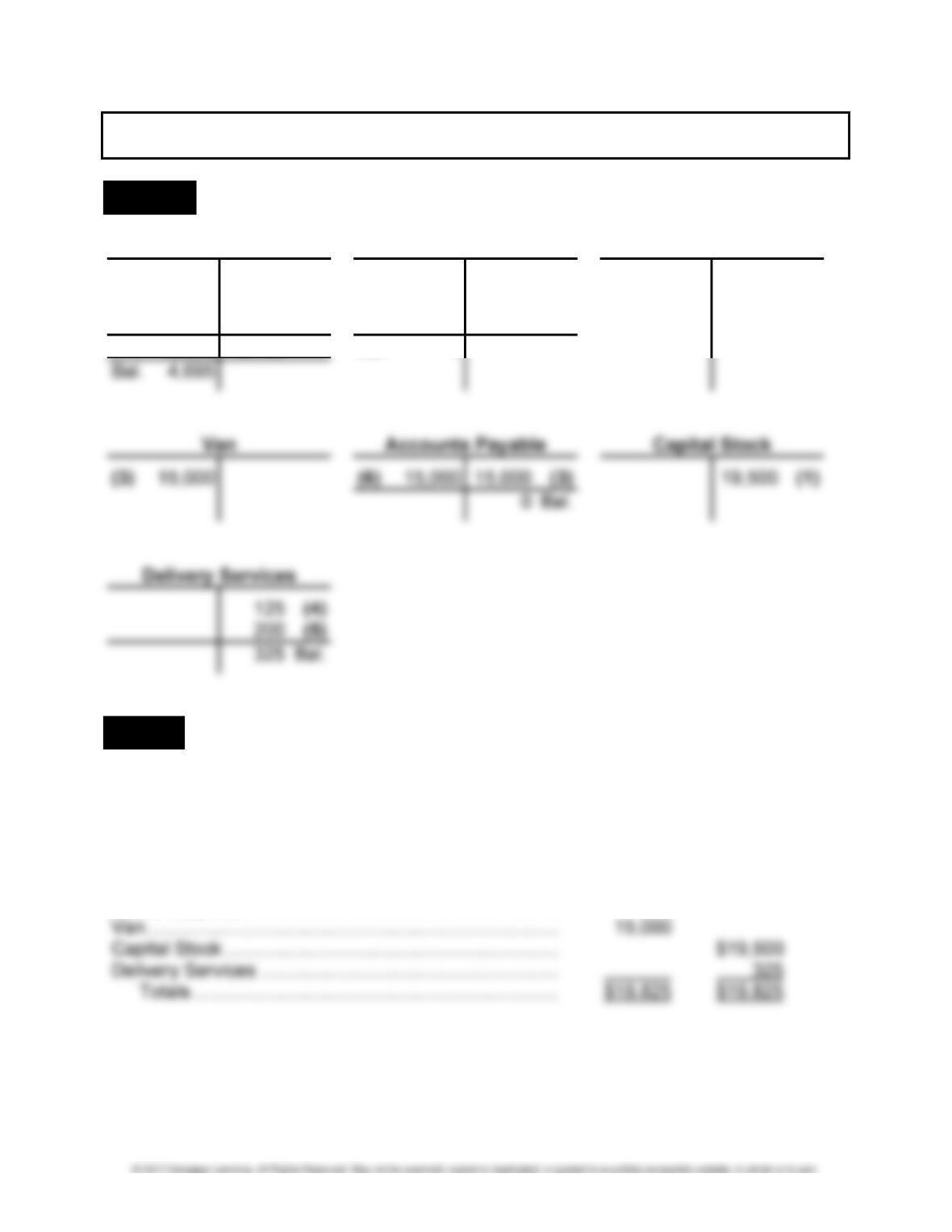

LO 3,4,5 EXERCISE 3-10 JOURNAL ENTRIES RECORDED DIRECTLY IN T ACCOUNTS

Cash Accounts Receivable Office Supplies

(1) 19,500 130 (2) (5) 200 200 (7) (2) 130

(4) 125 15,000 (6)

(7) 200

19,825 15,130 Bal. 0

LO 4,7 EXERCISE 3-11 TRIAL BALANCE

WE-GO DELIVERY SERVICE

TRIAL BALANCE

DECEMBER 31

Debits Credits

Cash ………………………………………………………………….. $ 4,695

Office Supplies ……………………………………………………. 130

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-9

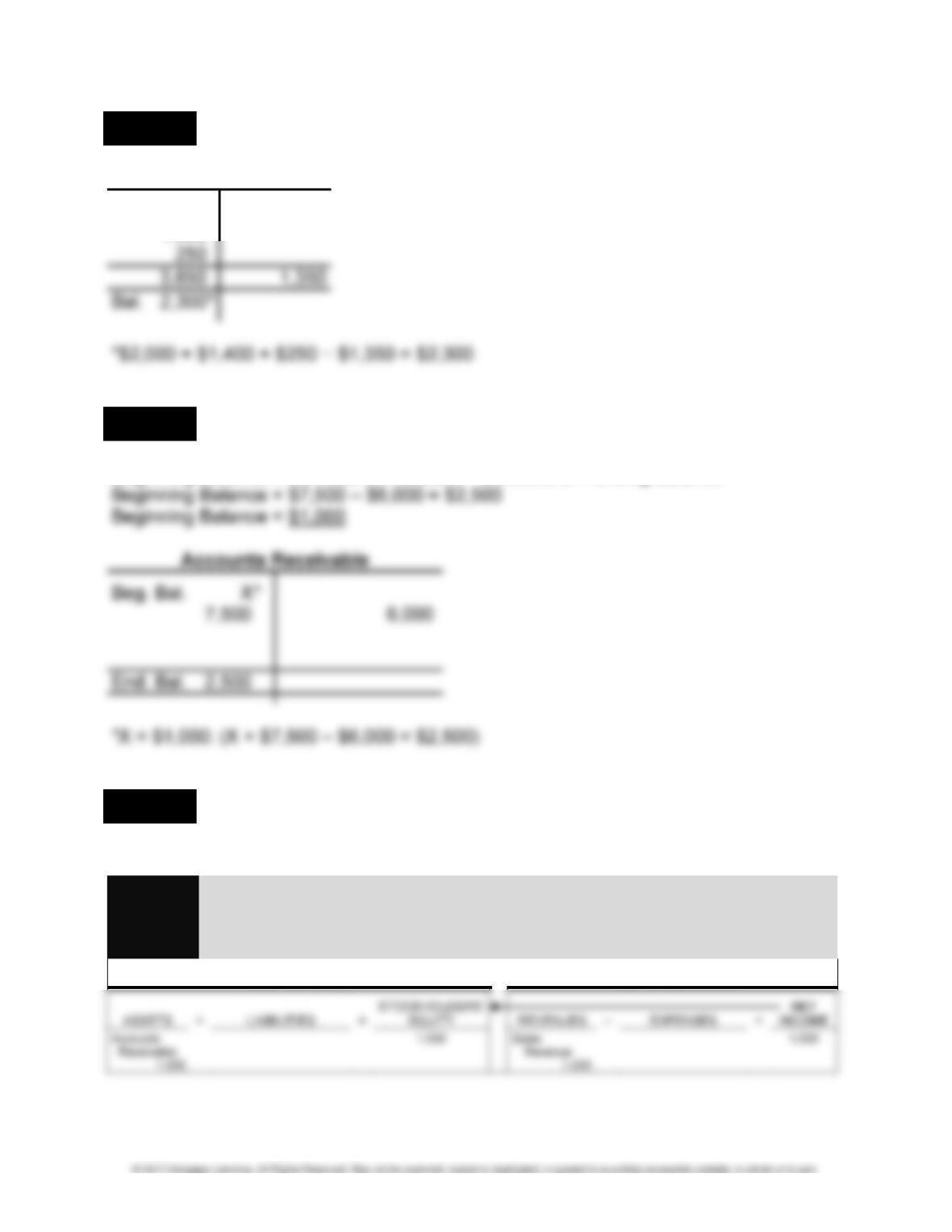

LO 3,4,5 EXERCISE 3-12 DETERMINING AN ENDING ACCOUNT BALANCE

Cash

2,000 1,350

1,400

LO 3,4,5 EXERCISE 3-13 RECONSTRUCTING A BEGINNING ACCOUNT BALANCE

Beginning Balance + Services on Account – Collections = Ending Balance

LO 3,5,6 EXERCISE 3-14 JOURNAL ENTRIES

1.

Journal Accounts Receivable …………………………………… 1,530

Entry Sales Revenue ……………………………………… 1,530

Analysis Made sales on open account.

Balance Sheet Income Statement

3-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 3-14 (Continued)

2.

Journal Supplies …………………………………………………….. 1,365

Entry Accounts Payable …………………………………. 1,365

Analysis Purchased supplies on open account.

Balance Sheet Income Statement

3.

Journal Cash …………………………………………………………. 750

Entry Sales Revenue ……………………………………… 750

Analysis Made cash sales.

Balance Sheet Income Statement

4.

Journal Equipment …………………………………………………. 4,240

Entry Cash ……………………………………………………. 4,240

Analysis Purchased equipment with cash.

Balance Sheet Income Statement

5.

Journal Cash …………………………………………………………. 2,500

Entry Notes Payable ………………………………………. 2,500

Analysis Issued promissory note for cash.

EXERCISE 3-14 (Concluded)

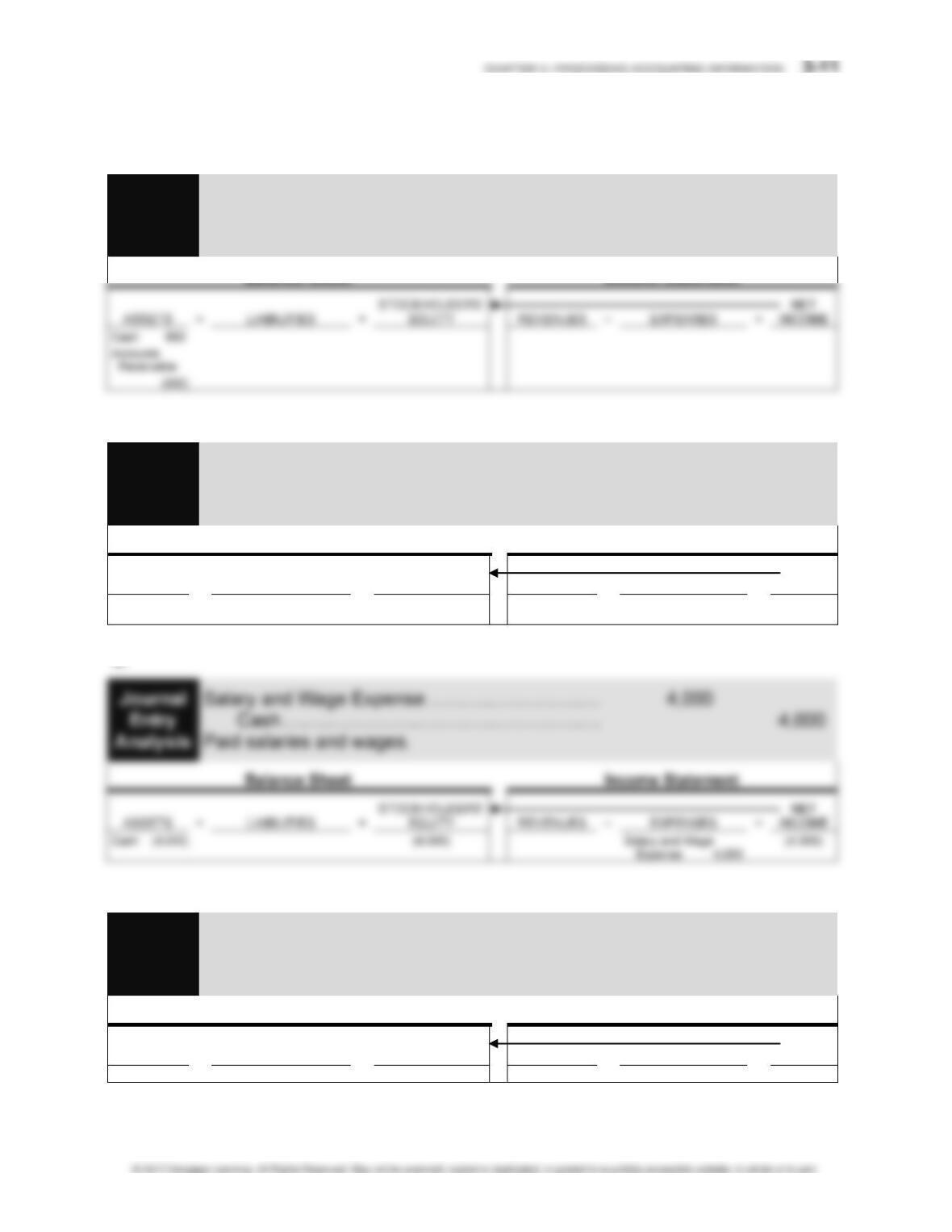

6.

Journal Cash …………………………………………………………. 890

Entry Accounts Receivable ……………………………… 890

Analysis Collected open accounts.

Balance Sheet Income Statement

7.

Journal Land ………………………………………………………….. 50,000

Entry Capital Stock ………………………………………… 50,000

Analysis Issued capital stock in exchange for land.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Land 50,000

Capital

Stock 50,000

8.

9.

Journal Accounts Payable ……………………………………….. 500

Entry Cash ……………………………………………………. 500

Analysis Paid open account.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (500

)

Accounts Payable (500)

3-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3,5,6 EXERCISE 3-15 JOURNAL ENTRIES

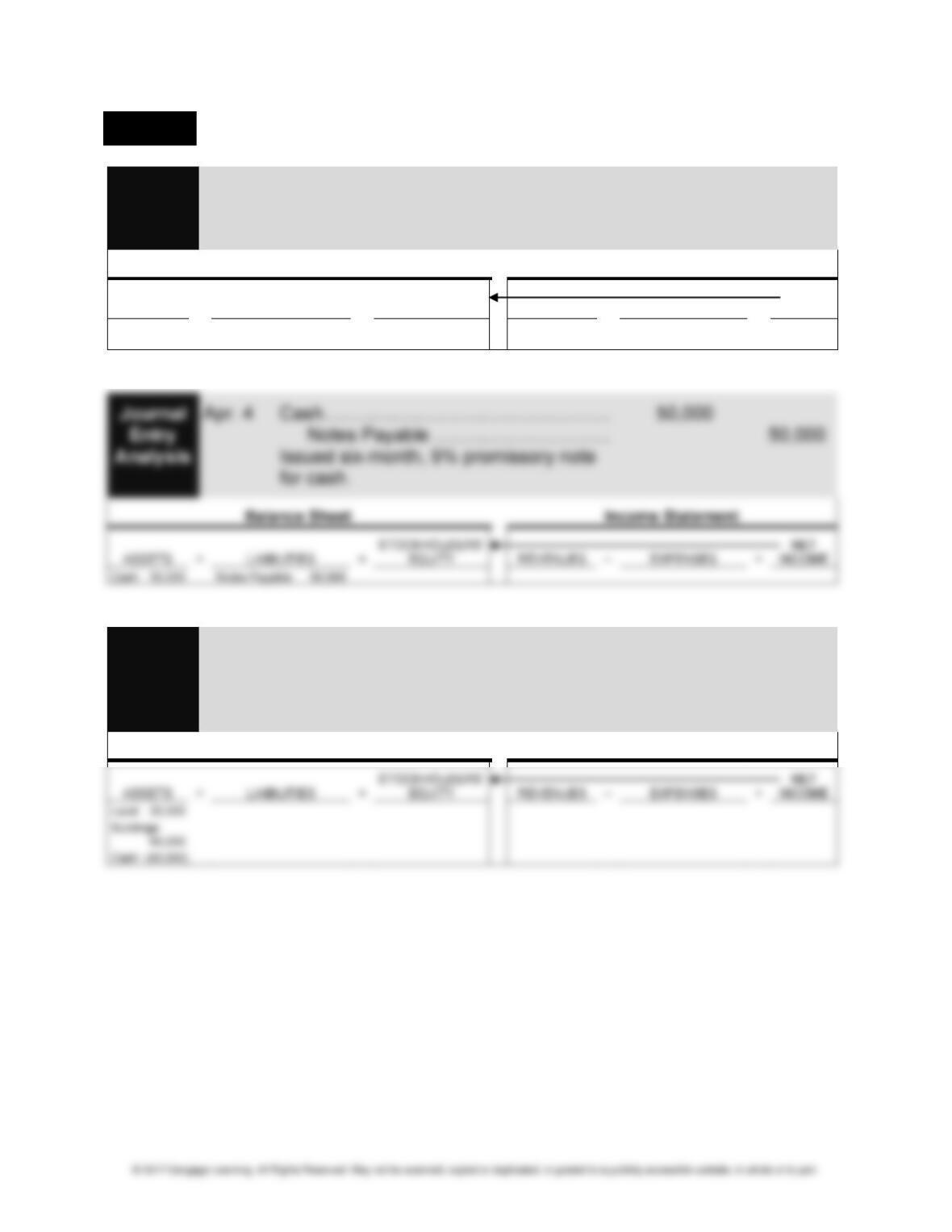

Journal Apr. 1 Cash ………………………………………………. 100,000

Entry Capital Stock ………………………………. 100,000

Analysis Issued 100,000 shares of capital stock.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 100,000

Capital

Stock 100,000

Journal Apr. 8 Land ………………………………………………. 20,000

Entry Buildings ………………………………………… 60,000

Analysis Cash …………………………………………. 80,000

Purchased land and a storage shed.

Balance Sheet Income Statement

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-13

EXERCISE 3-15 (Continued)

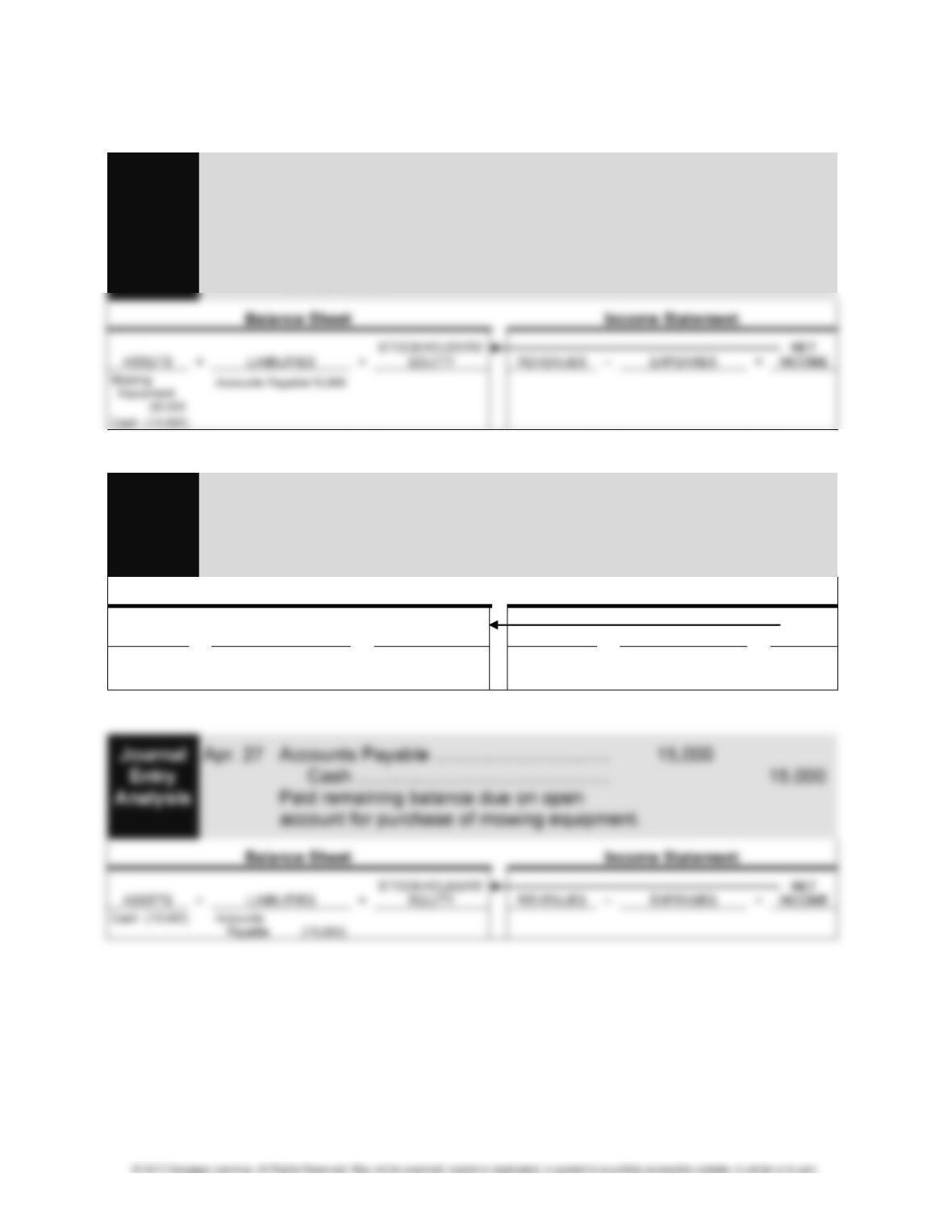

Journal Apr. 10 Mowing Equipment …………………………… 25,000

Entry Cash …………………………………………. 10,000

Analysis Accounts Payable ……………………….. 15,000

Purchased mowing equipment with

down payment and remainder due by

end of month.

Journal Apr. 18 Accounts Receivable ………………………… 5,500

Entry Service Revenue ………………………… 5,500

Analysis Billed customers for services provided

on account; amounts due within ten days.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts

Receivable

5,500

5,500

Service

Revenue

5,500

5,500

3-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 3-15 (Concluded)

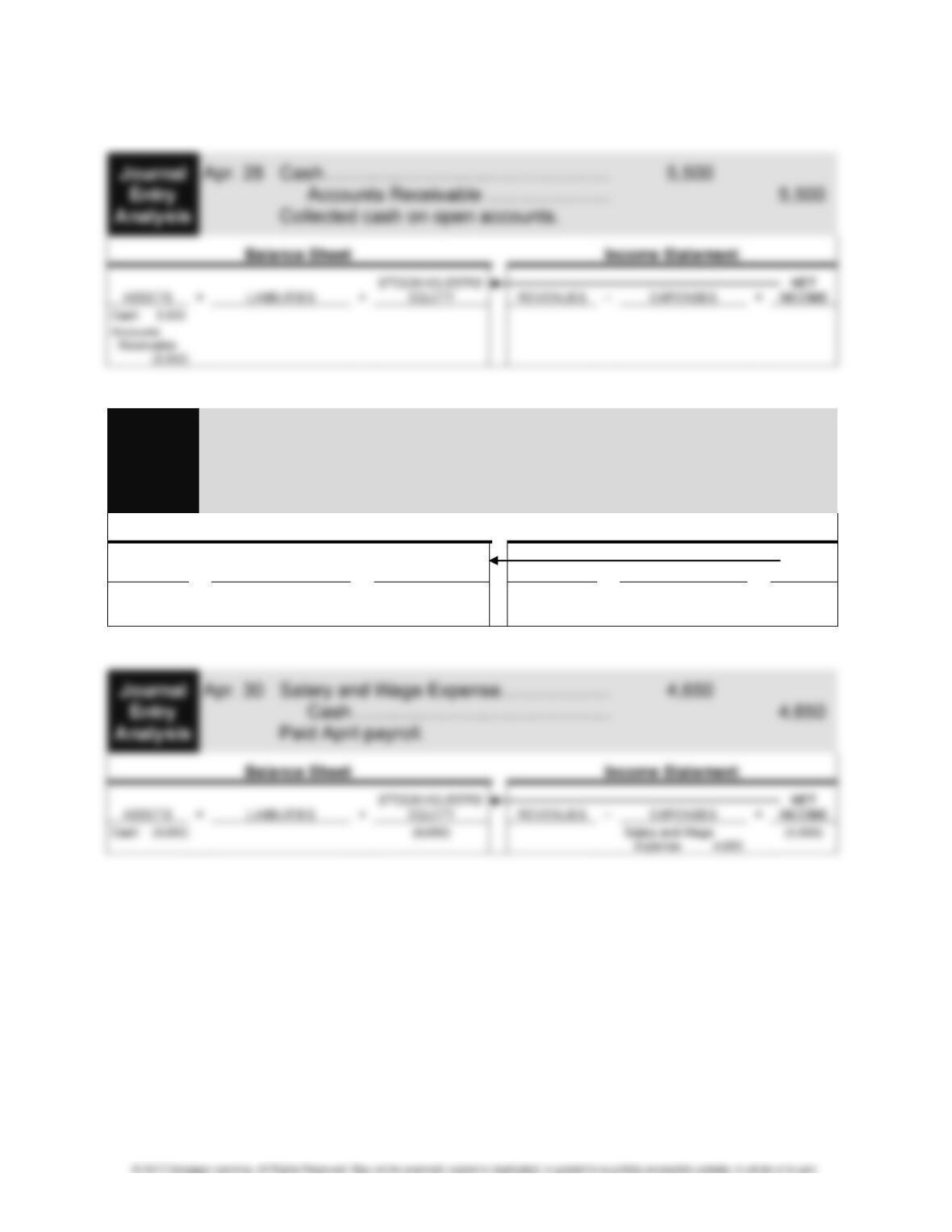

Journal Apr. 30 Accounts Receivable ………………………… 9,850

Entry Service Revenue ………………………… 9,850

Analysis Billed customers for services provided

on account.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts

Receivable

9,850

9,850

Service

Revenue

9,850

9,850

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-15

LO 3,5,6 EXERCISE 3-16 JOURNAL ENTRIES FOR VAIL RESORTS

1.

2.

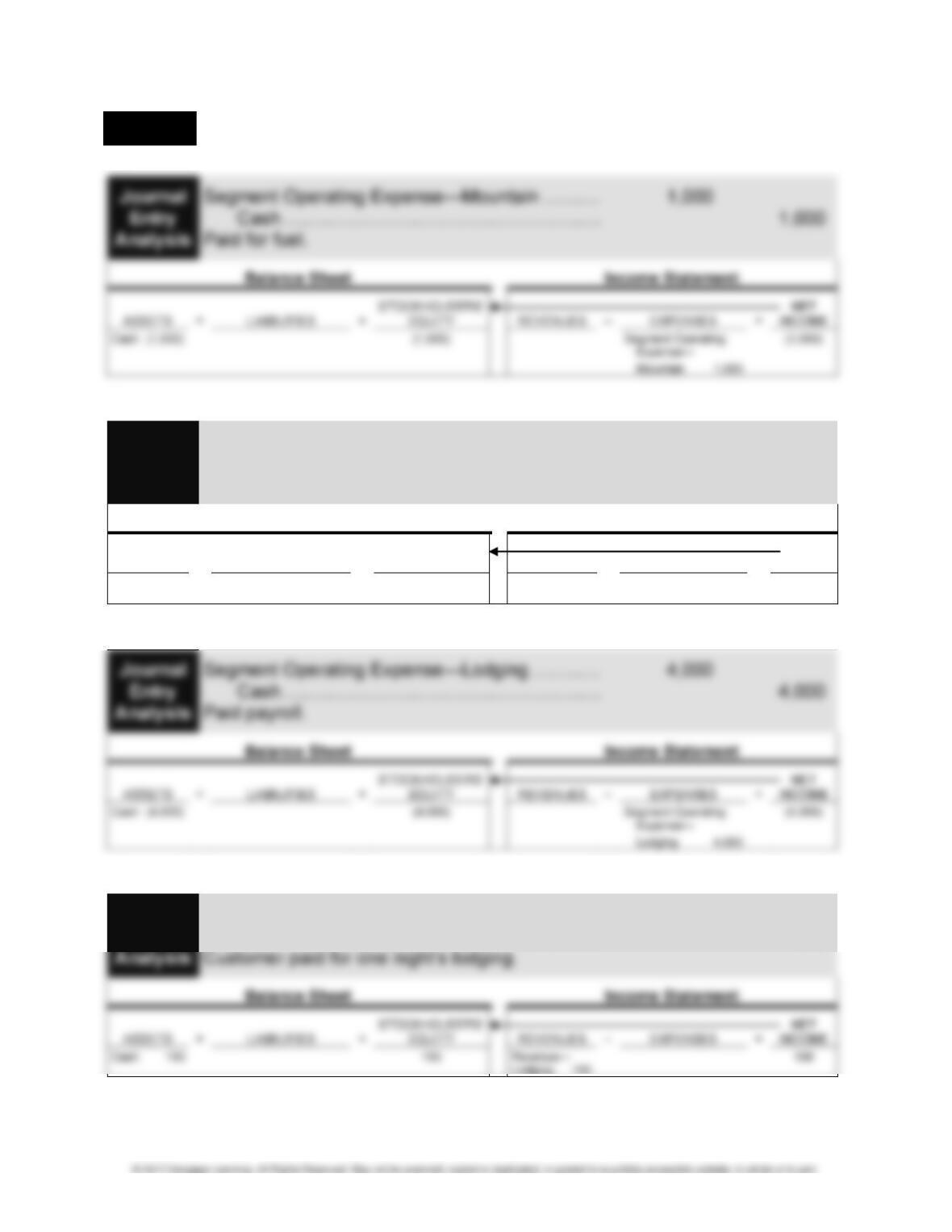

Journal Cash …………………………………………………………. 80

Entry Revenue—Mountain………………………………. 80

Analysis Made cash sales for lift tickets.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 80

80

Revenue—

Mountain 80

80

3.

4.

Journal Cash …………………………………………………………. 150

Entry Revenue—Lodging ……………………………….. 150

3-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

LO 5,6 EXERCISE 3-17 THE PROCESS OF POSTING JOURNAL ENTRIES TO GENERAL

LEDGER ACCOUNTS

General Journal Page No. 7

Post.

Date Account Title and Explanation Ref. Debit Credit

June 1 Land 17 50,000

The purpose of the journal is to provide a chronological record of a company’s transac-

tions. In addition, it shows the complete transaction in one place. Thus, if you wanted to

review this particular transaction in the future, you would look at the general journal.

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-17

PROBLEMS

LO 1 PROBLEM 3-1 EVENTS TO BE RECORDED IN ACCOUNTS

1. E Not recorded

2. E Recorded: Supplies, Accounts Payable

3-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

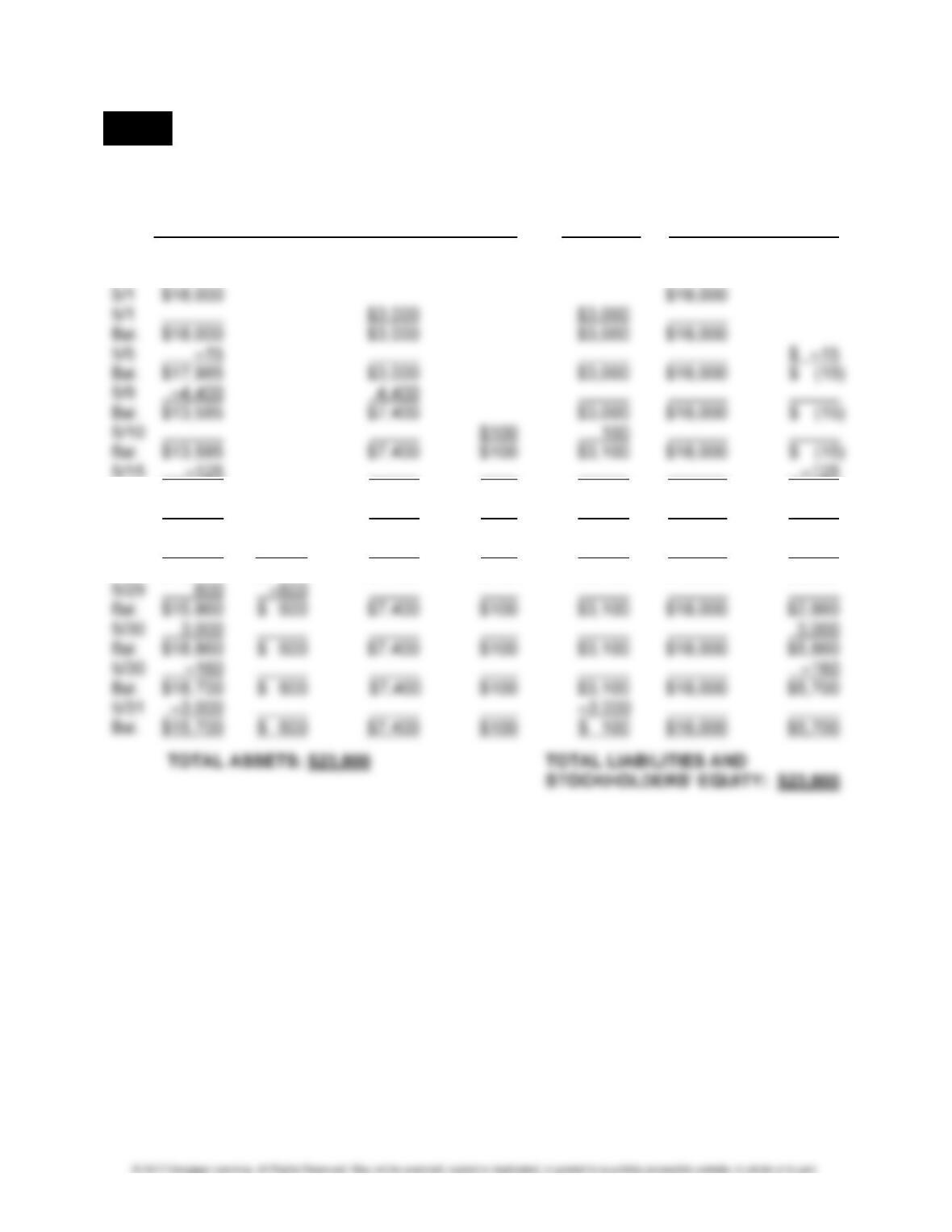

LO 3 PROBLEM 3-2 TRANSACTION ANALYSIS AND FINANCIAL STATEMENTS

1. JUST ROLLING ALONG INC.

TRANSACTIONS FOR THE MONTH OF MAY

Assets = Liabilities + Stockholders’ Equity

Accounts Accounts Capital Retained

Date Cash Receivable Equipment Supplies Payable Stock Earnings

Bal. $13,460 $7,400 $100 $3,100 $18,000 $ (140)

5/17 1,800 1,800

Bal. $15,260 $7,400 $100 $3,100 $18,000 $1,660

5/24 $1,200 1,200

Bal. $15,260 $1,200 $7,400 $100 $3,100 $18,000 $2,860

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-19

PROBLEM 3-2 (Concluded)

2. JUST ROLLING ALONG INC.

INCOME STATEMENT

FOR THE MONTH OF MAY

3. JUST ROLLING ALONG INC.

BALANCE SHEET

MAY 31

Assets

Current assets:

Cash …………………………………………………………………. $15,700

Accounts receivable ……………………………………………. 600

Supplies …………………………………………………………….. 100

4. Given the line of business that they are in, the two college students may be con-

cerned about their liability. One of the advantages of incorporating is the limited

liability of the stockholders. Generally, a stockholder is liable only for the amount

contributed to the business.

3-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

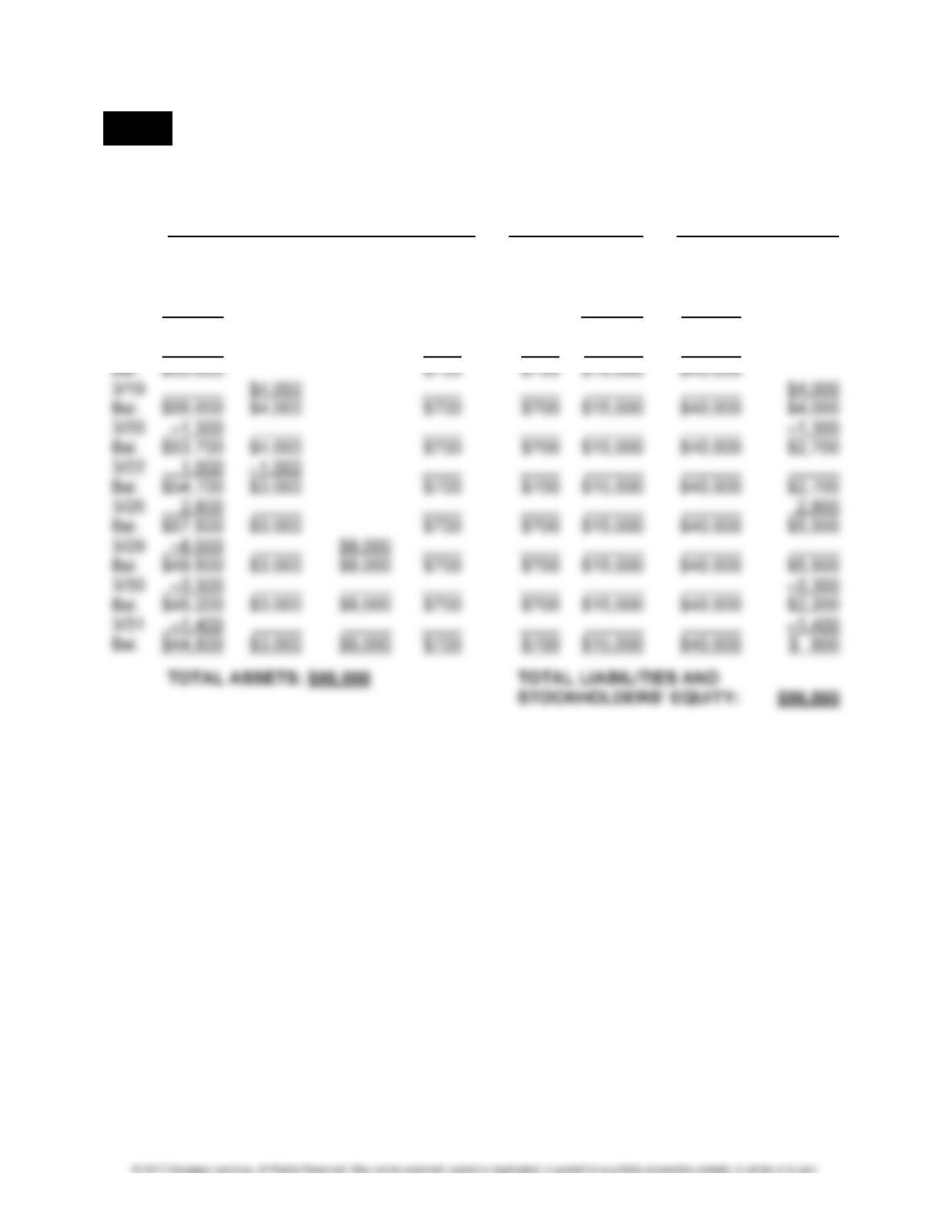

LO 3 PROBLEM 3-3 TRANSACTION ANALYSIS AND FINANCIAL STATEMENTS

1. EXPERT CONSULTING SERVICES INC.

TRANSACTIONS FOR THE MONTH OF MARCH

Assets = Liabilities + Stockholders’ Equity

Accounts Accounts Notes Capital Retained

Date Cash Receivable Computer Supplies Payable Payable Stock Earnings

3/2 $40,000 $40,000

3/7 15,000 $15,000

Bal. $55,000 $15,000 $40,000

3/12 $700 $700