CHAPTER 3

WORKING WITH FINANCIAL

STATEMENTS

Answers to Concepts Review and Critical Thinking Questions

1. a. If inventory is purchased with cash, then there is no change in the current ratio. If inventory is

purchased on credit, then there is a decrease in the current ratio if it was initially greater than 1.0.

b. Reducing accounts payable with cash increases the current ratio if it was initially greater than 1.0.

c. Reducing short-term debt with cash increases the current ratio if it was initially greater than 1.0.

2. The firm has increased inventory relative to other current assets; therefore, assuming current liability

levels remain mostly unchanged, liquidity has potentially decreased.

3. A current ratio of .50 means that the firm has twice as much in current liabilities as it does in current

assets; the firm potentially has poor liquidity. If pressed by its short-term creditors and suppliers for

4. a. Quick ratio provides a measure of the short-term liquidity of the firm, after removing the effects

of inventory, generally the least liquid of the firm’s current assets.

b. Cash ratio represents the ability of the firm to completely pay off its current liabilities balance with

its most liquid asset (cash).

CHAPTER 3 – 2

d. Total asset turnover measures how much in sales is generated by each dollar of firm assets.

e. Equity multiplier represents the degree of leverage for an equity investor of the firm; it measures

the dollar worth of firm assets each equity dollar has a claim to.

f. Times interest earned ratio provides a relative measure of how well the firm’s operating earnings

can cover current interest obligations.

5. Common size financial statements express all balance sheet accounts as a percentage of total assets

and all income statement accounts as a percentage of total sales. Using these percentage values rather

than nominal dollar values facilitates comparisons between firms of different size or business type.

6. Peer group analysis involves comparing the financial ratios and operating performance of a particular

firm to a set of peer group firms in the same industry or line of business. Comparing a firm to its peers

7. Return on equity is probably the most important accounting ratio that measures the bottom-line

performance of the firm with respect to the equity shareholders. The Du Pont identity emphasizes the

role of a firm’s profitability, asset utilization efficiency, and financial leverage in achieving a ROE

figure. For example, a firm with ROE of 20% would seem to be doing well, but this figure may be

misleading if it were a marginally profitable (low profit margin) and highly levered (high equity

multiplier). If the firm’s margins were to erode slightly, the ROE would be heavily impacted.

CHAPTER 3 – 3

10. a. For an electric utility such as Con Ed, expressing costs on a per kilowatt-hour basis would be a

way of comparing costs with other utilities of different sizes.

b. For a retailer such as JC Penney, expressing sales on a per square foot basis would be useful in

comparing revenue production against other retailers.

11. As with any ratio analysis, the ratios themselves do not necessarily indicate a problem, but simply

indicate that something is different and it is up to us to determine if a problem exists. If the cost of

goods sold as a percentage of sales is increasing, we would expect that EBIT as a percentage of sales

would decrease, all else constant. An increase in the cost of goods sold as a percentage of sales occurs

because the cost of raw materials or other inventory is increasing at a faster rate than the sales price.

12. If we assume that the cause is negative, the two reasons for the trend of increasing cost of goods sold

as a percentage of sales are that costs are becoming too high or the sales price is not increasing fast

enough. If the cause is an increase in the cost of goods sold, the manager should look at possible

actions to control costs. If costs can be lowered by seeking lower cost suppliers of similar or higher

quality, the cost of goods sold as a percentage of sales should decrease. Another alternative is to

increase the sales price to cover the increase in the cost of goods sold. Depending on the industry, this

CHAPTER 3 – 4

Solutions to Questions and Problems

NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

1. To find the current assets, we must use the net working capital equation. Doing so, we find:

NWC = Current assets – Current liabilities

$1,965 = Current assets – $5,460

Current assets = $7,425

2. To find the return on assets and return on equity, we need net income. We can calculate the net income

using the profit margin. Doing so, we find the net income is:

Profit margin = Net income / Sales

.07 = Net income / $13,500,000

Net income = $945,000

Now we can calculate the return on assets as:

CHAPTER 3 – 5

3. The receivables turnover for the company was:

Receivables turnover = Credit sales / Receivables

Receivables turnover = $6,787,626 / $583,174

Receivables turnover = 11.64 times

4. The inventory turnover for the company was:

Inventory turnover = COGS / Inventory

Inventory turnover = $8,543,132 / $527,156

Inventory turnover = 16.21 times

5. To find the debt–equity ratio using the total debt ratio, we need to rearrange the total debt ratio

equation. We must realize that the total assets are equal to total debt plus total equity. Doing so, we

find:

Total debt ratio = Total debt / Total assets

.19 = Total debt / (Total debt + Total equity)

.81(Total debt) = .19(Total equity)

CHAPTER 3 – 6

6. We need to calculate the net income before we calculate the earnings per share. The sum of dividends

and addition to retained earnings must equal net income, so net income must have been:

Net income = Addition to retained earnings + Dividends

Net income = $534,000 + 185,000

Net income = $719,000

So, the earnings per share were:

The book value per share was:

Book value per share = Total equity / Shares outstanding

Book value per share = $7,450,000 / 365,000

Book value per share = $20.41 per share

The market-to-book ratio is:

Market-to-book ratio = Share price / Book value per share

Market-to-book ratio = $49 / $20.41

Market-to-book ratio = 2.40 times

The P/S ratio is:

P/S ratio = Share price / Sales per share

P/S ratio = $49 / $42.19

P/S ratio = 1.16 times

CHAPTER 3 – 7

7. With the information given, we must use the Du Pont identity to calculate return on equity. Doing so,

we find:

8. We can use the Du Pont identity and solve for the equity multiplier. With the equity multiplier we can

find the debt–equity ratio. Doing so we find:

ROE = (Profit margin)(Total asset turnover)(Equity multiplier)

9. To find the days’ sales in payables, we first need to find the payables turnover. The payables turnover

was:

Payables turnover = Cost of goods sold / Payables balance

Payables turnover = $87,386 / $19,472

Payables turnover = 4.49 times

10. With the information provided, we need to calculate the return on equity using an extended return on

equity equation. We first need to find the equity multiplier, which is:

Equity multiplier = 1 + Debt–equity ratio

Equity multiplier = 1 + .75

Equity multiplier = 1.75

CHAPTER 3 – 8

11. To find the internal growth rate, we need the plowback, or retention, ratio. The plowback ratio is:

b = 1 – .25

b = .75

Now, we can use the internal growth rate equation to find:

12. To find the sustainable growth rate we need the plowback, or retention, ratio. The plowback ratio is:

b = 1 – .20

b = .80

Now, we can use the sustainable growth rate equation to find:

13. We need the return on equity to calculate the sustainable growth rate. To calculate return on equity,

we need to realize that the total asset turnover is the inverse of the capital intensity ratio and the equity

multiplier is one plus the debt–equity ratio. So, the return on equity is:

ROE = (Profit margin)(Total asset turnover)(Equity multiplier)

CHAPTER 3 – 9

14. We need the return on equity to calculate the sustainable growth rate. Using the Du Pont identity, the

return on equity is:

ROE = (Profit margin)(Total asset turnover)(Equity multiplier)

ROE = (.057)(2.80)(1.47)

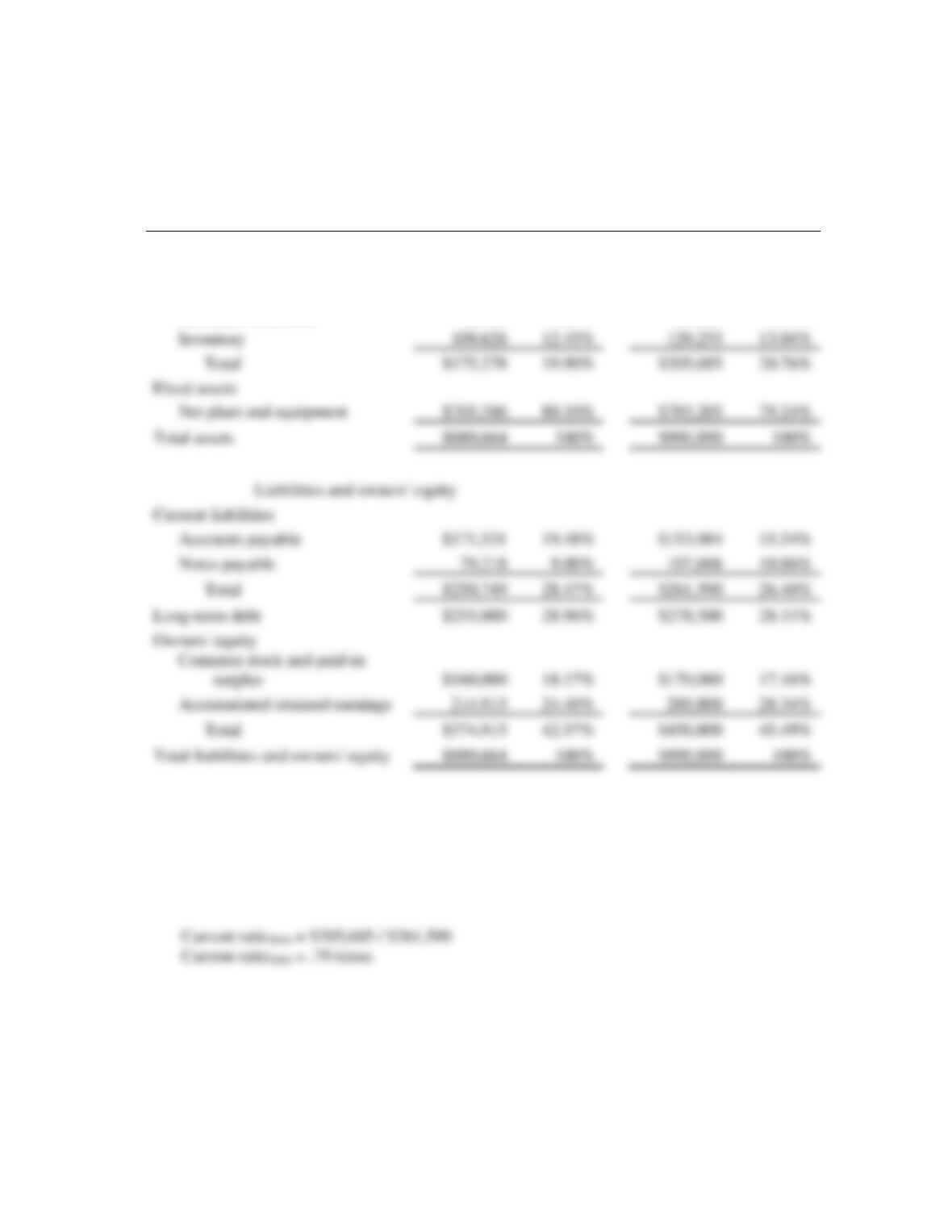

15. To calculate the common-size balance sheet, we divide each asset account by total assets, and each

liability and equity account by total liabilities and equity. For example, the common-size cash

percentage for 2015 is:

Cash percentage = Cash / Total assets

Cash percentage = $19,256 / $880,664

CHAPTER 3 – 10

Repeating this procedure for each account, we get:

2015

2016

Assets

Current assets

Cash

$19,256

2.19%

$21,946

2.21%

Accounts receivable

46,396

5.27%

54,486

5.50%

16. a. The current ratio is calculated as:

Curent ratio = Current assets / Current liabilities

Current ratio2015 = $175,278 / $250,749

Current ratio2015 = .70 times

Inventory

109,626

129,253

Fixed assets

Net plant and equipment

Current liabilities

Accounts payable

Total

Owners’ equity

Accumulated retained earnings

214,915

280,800

Total liabilities and owners’ equity

CHAPTER 3 – 11

b. The quick ratio is calculated as:

Quick ratio = (Current assets – Inventory) / Current liabilities

c. The cash ratio is calculated as:

Cash ratio = Cash / Current liabilities

d. The debt–equity ratio is calculated as:

Debt–equity ratio = Total debt / Total equity

Debt–equity ratio = (Current liabilities + Long-term debt) / Total equity

Debt–equity ratio2015 = ($250,749 + 255,000) / $374,915

Debt–equity ratio2015 = 1.35 times

e. The total debt ratio is calculated as:

Total debt ratio = Total debt / Total assets

Total debt ratio = (Current liabilities + Long-term debt) / Total assets

CHAPTER 3 – 12

Total debt ratio2016 = ($261,590 + 278,500) / $990,890

Total debt ratio2016 = .55 times

17. Using the Du Pont identity to calculate ROE, we get:

18. One equation to calculate ROA is:

ROA = (Profit margin)(Total asset turnover)

We can solve this equation to find total asset turnover as:

19. To calculate the ROA, we first need to find the net income. Using the profit margin equation, we find:

Profit margin = Net income / Sales

.058 = Net income / $14,500,000

Net income = $841,000

20. To calculate the internal growth rate, we need to find the ROA and the plowback ratio. The ROA for

the company is:

ROA = Net income / Total assets

ROA = $15,112 / $120,400

ROA = .1255, or 12.55%

CHAPTER 3 – 13

21. To calculate the sustainable growth rate, we need to find the ROE and the plowback ratio. The ROE

for the company is:

ROE = Net income / Equity

22. The total asset turnover is:

Total asset turnover = Sales / Total assets

Total asset turnover = $13,800,000 / $7,100,000

Total asset turnover = 1.94 times

23. To find the ROE, we need the equity balance. Since we have the total debt, if we can find the total

assets we can calculate the equity. Using the total debt ratio, we find total assets as:

Debt ratio = Total debt / Total assets

.75 = $353,000 / Total assets

Total assets = $470,667

CHAPTER 3 – 14

24. The earnings per share are:

EPS = Net income / Shares

EPS = $8,400,000 / 4,600,000

EPS = $1.83

The price–sales ratio is:

P/S = Price / Sales per share

P/S = $58 / $11.48

P/S = 5.05 times

The book value per share is:

CHAPTER 3 – 15

25. To find the profit margin, we need the net income and sales. We can use the total asset turnover to find

the sales and the return on assets to find the net income. Beginning with the total asset turnover, we

find sales are:

Total asset turnover = Sales / Total assets

1.80 = Sales / $7,450,000

Sales = $13,410,000

26. First, we need the enterprise value, which is:

Enterprise value = Market capitalization + Debt – Cash

Enterprise value = $635,000 + 215,000 – 39,000

Enterprise value = $811,000

27. We can rearrange the Du Pont identity to calculate the profit margin. So, we need the equity multiplier

and the total asset turnover. The equity multiplier is:

Equity multiplier = 1 + Debt–equity ratio

Equity multiplier = 1 + .25

Equity multiplier = 1.25

CHAPTER 3 – 16

28. This is a multi-step problem in which we need to calculate several ratios to find the fixed assets. If we

know total assets and current assets, we can calculate the fixed assets. Using the current ratio to find

the current assets, we get:

Current ratio = Current assets / Current liabilities

1.30 = Current assets / $2,435

Current assets = $3,165.50

And using this net income figure in the return on equity equation to find the equity, we get:

ROE = Net income / Total equity

.128 = $1,044.90 / Total equity

Total equity = $8,163.28

CHAPTER 3 – 17

Inverting both sides we get:

1 / Long-term debt ratio = 1 + (Total equity / Long-term debt)

1 / .45 = 1 + (Total equity / Long-term debt)

Total equity / Long-term debt = 1.222

$8,163.28 / Long-term debt = 1.222

Long-term debt = $6,679.05

29. The child’s profit margin is:

Profit margin = Net income / Sales

Profit margin = $2 / $50

Profit margin = .04, or 4%

And the store’s profit margin is:

CHAPTER 3 – 18

30. To calculate the profit margin, we first need to calculate the sales. Using the days’ sales in receivables,

we find the receivables turnover is:

Days’ sales in receivables = 365 days / Receivables turnover

29.38 days = 365 days / Receivables turnover

Receivables turnover = 12.42 times

The total asset turnover is:

Total asset turnover = Sales / Total assets

Total asset turnover = $1,805,744 / $794,350

Total asset turnover = 2.27 times

We need to use the Du Pont identity to calculate the return on equity. Using this relationship, we get:

31. Here, we need to work the income statement backward to find the EBIT. Starting at the bottom of the

income statement, we know that the taxes are the taxable income times the tax rate. The net income is

the taxable income minus taxes. Rearranging this equation, we get:

Net income = Taxable income – (TC)(Taxable income)

Net income = (1 – TC)(Taxable income)

CHAPTER 3 – 19

32. To find the times interest earned, we need the EBIT and interest expense. EBIT is sales minus costs

minus depreciation, so:

EBIT = Sales – Costs – Depreciation

EBIT = $534,000 – 241,680 – 60,400

EBIT = $231,920

Now, we need the interest expense. We know the EBIT, so if we find the taxable income (EBT), the

difference between these two is the interest expense. To find EBT, we must work backward through

the income statement. We need total dividends paid. We can use the dividends per share equation to

find the total dividends. Doing so, we find:

We know that the taxes are the taxable income times the tax rate. The net income is the taxable income

minus taxes. Rearranging this equation, we get:

Net income = Taxable income – (TC)(EBT)

Net income = (1 – TC)(EBT)

$99,800 = (1 – .34)(EBT)

EBT = $151,212

CHAPTER 3 – 20

33. To find the return on equity, we need the net income and total equity. We can use the total debt ratio

to find the total assets as:

Total debt ratio = Total debt / Total assets

.37 = $673,000 / Total assets

Total assets = $1,818,919

We have the return on equity and the equity. We can use the return on equity equation to find net

income is:

ROE = Net income / Equity

.1290 = Net income / $1,145,919

Net income = $147,824

ROA = .0813, or 8.13%

34. The currency is generally irrelevant in calculating any financial ratio. The company’s profit margin is:

Profit margin = Net income / Sales

Profit margin = –£27,860 / £512,621

Profit margin = –.0543, or –5.43%

CHAPTER 3 – 21

35. Here, we need to calculate several ratios given the financial statements. The ratios are:

Short-term solvency ratios:

Current ratio = Current assets / Current liabilities

Quick ratio = (Current assets – Inventory) / Current liabilities

Quick ratio2015 = ($28,666 – 17,357) / $6,319

Quick ratio2015 = 1.79 times

Quick ratio2016 = ($32,409 – 19,350) / $7,427

Quick ratio2016 = 1.76 times

Asset utilization ratios:

Total asset turnover = Sales / Total assets

Total asset turnover = $205,227 / $109,219

Total asset turnover = 1.88 times

Inventory turnover = COGS / Inventory

Inventory turnover = $138,383 / $19,350

Inventory turnover = 7.15 times

CHAPTER 3 – 22

Long-term solvency ratios:

Total debt ratio = (Current liabilities + Long-term debt) / Total assets

Debt–equity ratio = (Current liabilities + Long-term debt) / Total equity

Debt–equity ratio2015 = ($6,319 + 22,500) / $58,535

Debt–equity ratio2015 = .49 times

Equity multiplier2016 = 1 + .32

Equity multiplier2016 = 1.32 times

Times interest earned = EBIT / Interest

Times interest earned = $60,934 / $1,617

Times interest earned = 37.68 times

Profitability ratios:

Profit margin = Net income / Sales

Profit margin = $38,557 / $205,227

Profit margin = .1879, or 18.79%

CHAPTER 3 – 23

36. The Du Pont identity is:

ROE = (PM)(Total asset turnover)(Equity multiplier)

37. To find the price–earnings ratio we first need the earnings per share. The earnings per share are:

EPS = Net income / Shares outstanding

EPS = $38,557 / 10,000 shares

EPS = $3.86

So, the price–sales ratio is:

P/S ratio = Share price / Sales per share

P/S ratio = $73 / $20.52

P/S ratio = 3.56 times

The dividends per share are:

38. The current ratio appears to be relatively high when compared to the median; however, it is below the

upper quartile, meaning that at least 25 percent of firms in the industry have a higher current ratio.

Overall, it does not appear that the current ratio is out of line with the industry. The total asset turnover

is low when compared to the industry. In fact, the total asset turnover is in the lower quartile. This

39. To find the profit margin, we can solve the Du Pont identity. First, we need to find the retention ratio.

The retention ratio for the company is:

b = 1 – .30

b = .70

Now, we can use the sustainable growth rate equation to find the ROE. Doing so, we find:

40. The earnings per share is the net income divided by the shares outstanding. Since all numbers are in

millions, the earnings per share for Abercrombie & Fitch was:

EPS = $51.821 / 68.98

EPS = $.75

And the earnings per share for American Eagle Outfitters was:

CHAPTER 3 – 25

The market-to-book ratio is the stock price divided by the book value per share. To find the book value

per share, we divide the total equity by the shares outstanding. The book value per share and market–

to-book ratio for Abercrombie & Fitch was:

Book value per share = $5.83

Market-to-book = $13.84 / $5.83

Market-to-book = 2.37 times

And the price–earnings ratio for Abercrombie & Fitch was:

PE = $24.81 / $.75

PE = 33.03 times

41. To find the total asset turnover, we can solve the ROA equation. First, we need to find the retention

ratio. The retention ratio for the company is:

b = 1 – .25

b = .75

Now, we can use the internal growth rate equation to find the ROA. Doing so, we find:

CHAPTER 3 – 26

42. To calculate the sustainable growth rate, we need to calculate the return on equity. We can use the Du

Pont identity to calculate the return on equity if we can find the equity multiplier. Using the total debt

ratio, we can find the debt–equity ratio is:

So, the equity multiplier is:

Equity multiplier = 1 + Debt–equity ratio

Equity multiplier = 1 + .43

Equity multiplier = 1.43 times

Using the Du Pont identity, the ROE is:

To calculate the sustainable growth rate, we also need the retention ratio. The retention ratio is:

b = 1 – .15

b = .85

Now we can calculate the sustainable growth rate as:

CHAPTER 3 – 27

43. To find the sustainable growth rate, we need the retention ratio and the return on equity. The payout

ratio is the dividend payment divided by net income, so:

b = 1 – ($8,100 / $19,000)

b = .5737

And the return on equity is:

The total assets of the company are equal to the total debt plus the total equity. The total assets will

increase at the sustainable growth rate, so the total assets next year will be:

New total assets = (1 + Sustainable growth rate)(Total assets)

New total assets = (1 + .1361)($67,000 + 91,000)

New total assets = $179,500.62

The additional borrowing is the difference between the new total debt and the current total debt, so:

Additional borrowing = New total debt – Current total debt

Additional borrowing = $76,117.35 – 67,000

Additional borrowing = $9,117.35

CHAPTER 3 – 28

So, the internal growth rate is:

44. We can find the payout ratio from the sustainable growth rate formula. First, we need the return on

equity. Using the Du Pont identity, we find the return on equity is:

ROE = (Profit margin)(Total asset turnover)(Equity multiplier)

ROE = (.06)(1.10)(1 + .35)

ROE = .0891, or 8.91%

Now we can use the sustainable growth rate equation to find the retention ratio, which is:

This is a dividend payout ratio of –29%, which is impossible; the growth rate is not consistent with

the other constraints. The lowest possible payout rate is zero, which corresponds to retention ratio of

one, or total earnings retention. The maximum sustainable growth rate for this company is:

45. Using the beginning of period total assets, the ROA is:

ROABegin = $1,233 / $14,013

ROABegin = .0880, or 8.80%

Using the end of period total assets, the ROA is:

CHAPTER 3 – 29

The ROE using the end of period equity is:

ROEEnd = $1,233 / $4,995

ROEEnd = .2468, or 24.68%

The retention ratio, which is one minus the dividend payout ratio, is:

And the sustainable growth rate is:

Sustainable growth rate = [(ROE)(b)] / [1 – (ROE)(b)]

Sustainable growth rate = [(.2468)(.7964)] / [1 – (.2468)(.7964)]

Sustainable growth rate = .2447, or 24.47%

Using ROA × b and end of period assets to find the internal growth rate, we find:

Using ROA × b and beginning of period assets to find the internal growth rate, we find:

Internal growth rate = ROABegin × b

Internal growth rate = .0880 × .7964

Internal growth rate = .0701, or 7.01%

And, using ROE × b and the beginning of period equity to find the sustainable growth rate, we find:

CHAPTER 3 – 30

46.

Return on

equity

58.20%

Return on

multiplied

Equity

assets

By

multiplier

15.04%

3.869

subtracted

from

Total costs

Sales

Fixed assets

plus

Current

assets

$6,574.856

$7,421.768

$3,382.469

$2,247.047

Cash

Cost of goods sold

Depreciation

Accounts rec.

Inventory

Interest

$1,077.607

$83.532

Profit margin

11.41%

Net income

Sales

Sales

$7,421.768

$7,421.768

$5,629.516