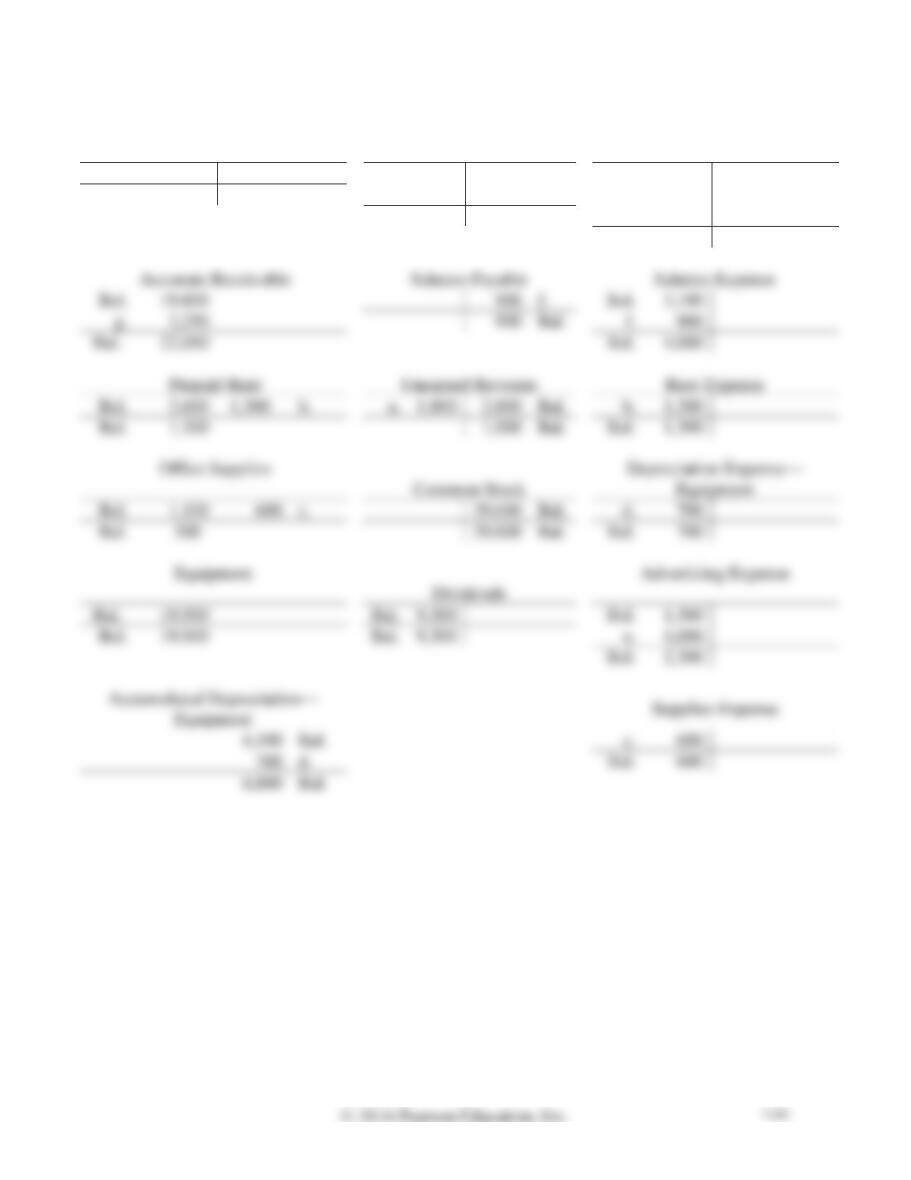

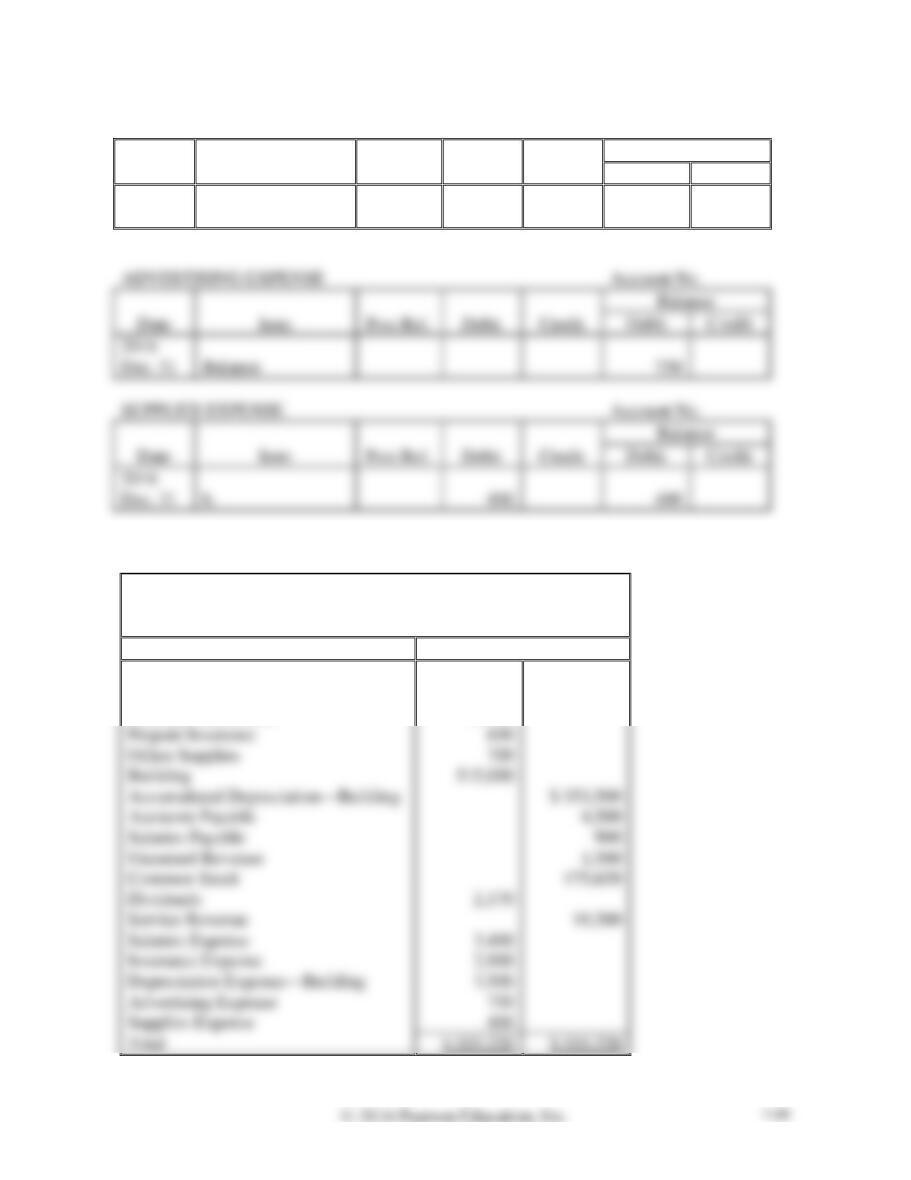

P3-35A, cont.

Requirement 2

Cash

Accounts Payable

Service Revenue

Bal.

7,800

3,000

Bal.

15,400

Bal.

Bal.

7,800

1,000

e.

1,800

a.

4,000

Bal.

2,250

g.

19,450

Bal.

Salaries Payable

Salaries Expense

Bal.

2,250

Bal.

900

4,000

Unearned Revenue

Rent Expense

Bal.

2,600

1,300

b.

1,800

2,800

Bal.

1,300

Bal.

1,300

1,000

Bal.

1,300

Bal.

1,100

600

c.

39,600

Bal.

700

Bal.

500

39,600

Bal.

700

Bal.

Bal.

9,300

1,000

2,300

Bal.

600

d.

600

Bal.

P3-35A, cont.

Requirement 3

AURORA AIR PURIFICATION SYSTEM

Adjusted Trial Balance

December 31, 2016

Account Title

Balance

Debit

Credit

Cash

$ 7,800

Accounts Receivable

22,050

Prepaid Rent

1,300

Office Supplies

500

Equipment

19,900

Accounts Payable

4,000

Salaries Payable

900

Unearned Revenue

1,000

Common Stock

39,600

Dividends

9,300

Service Revenue

19,450

Salaries Expense

4,000

Rent Expense

1,300

Depreciation Expense—Equipment

700

Advertising Expense

2,300

Supplies Expense

600

Requirement 4

Aurora will use the adjusted trial balance to prepare its financial statements. (Additionally, the purpose

of any trial balance is to ensure that total debits equal total credits.)

P3-36A Journalizing and posting adjustments to the four-column accounts and preparing an

adjusted trial balance

Learning Objectives 3, 4

3. Adjusted trial balance $555,220 total

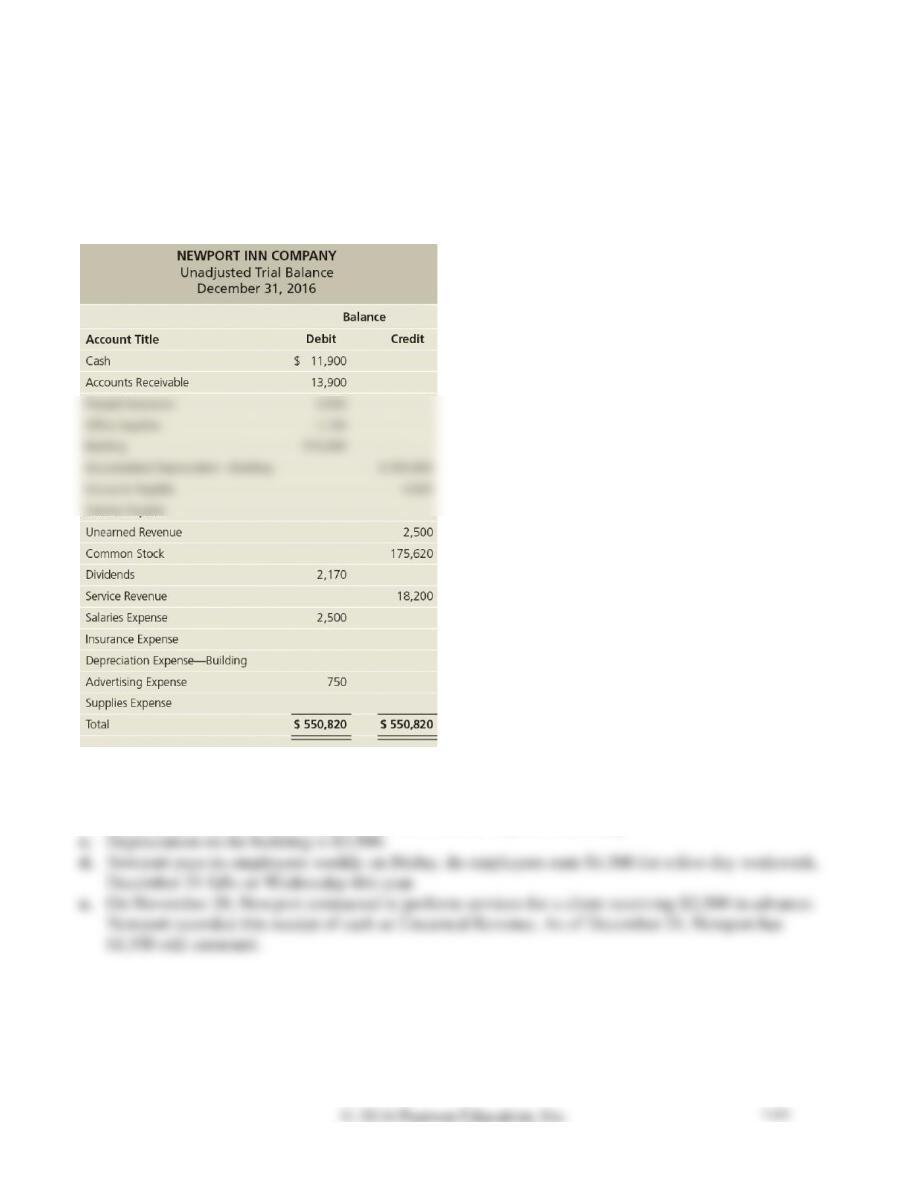

The unadjusted trial balance of Newport Inn Company at December 31, 2016, and the data needed for

the adjustments follow.

Adjustment data at December 31 follow:

a. As of December 31, Newport had $600 of Prepaid Insurance remaining.

b. At the end of the month, Newport had $700 of office supplies remaining.

Requirements

1. Journalize the adjusting entries on December 31.

2. Using the unadjusted trial balance, open the accounts (use a four-column ledger) with the unadjusted

balances. Post the adjusting entries to the ledger accounts.

3. Prepare the adjusted trial balance.

4. Assuming the adjusted trial balance has total debits equal to total credits, does this mean that the

adjusting entries have been recorded correctly? Explain.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

a. Dec. 31

Insurance Expense

2,900*

Prepaid Insurance

2,900*

To record insurance expense.

b. Dec. 31

Supplies Expense

400*

Office Supplies

400*

To record office supplies used.

c. Dec. 31

Depreciation Expense—Building

To record depreciation on building.

d. Dec. 31

Salaries Expense

900*

Salaries Payable

900*

To accrue salaries expense.

e. Dec. 31

Unearned Revenue

1,000*

1,000*

advance.

$3,500

$2,900

P3-35A, cont.

b:

$1,100

Office Supplies prior to adjustment

(700)

Office Supplies remaining

$ 400

Supplies Expense (cost of office supplies used)

d:

$1,500

Salaries for a five-day work week

$ 300

Salaries Expense per work day

Salaries Expense per work day

work days

Salaries Expense for Monday through Wednesday

Unearned Revenue prior to adjustment

Unearned Revenue still unearned

Service Revenue earned

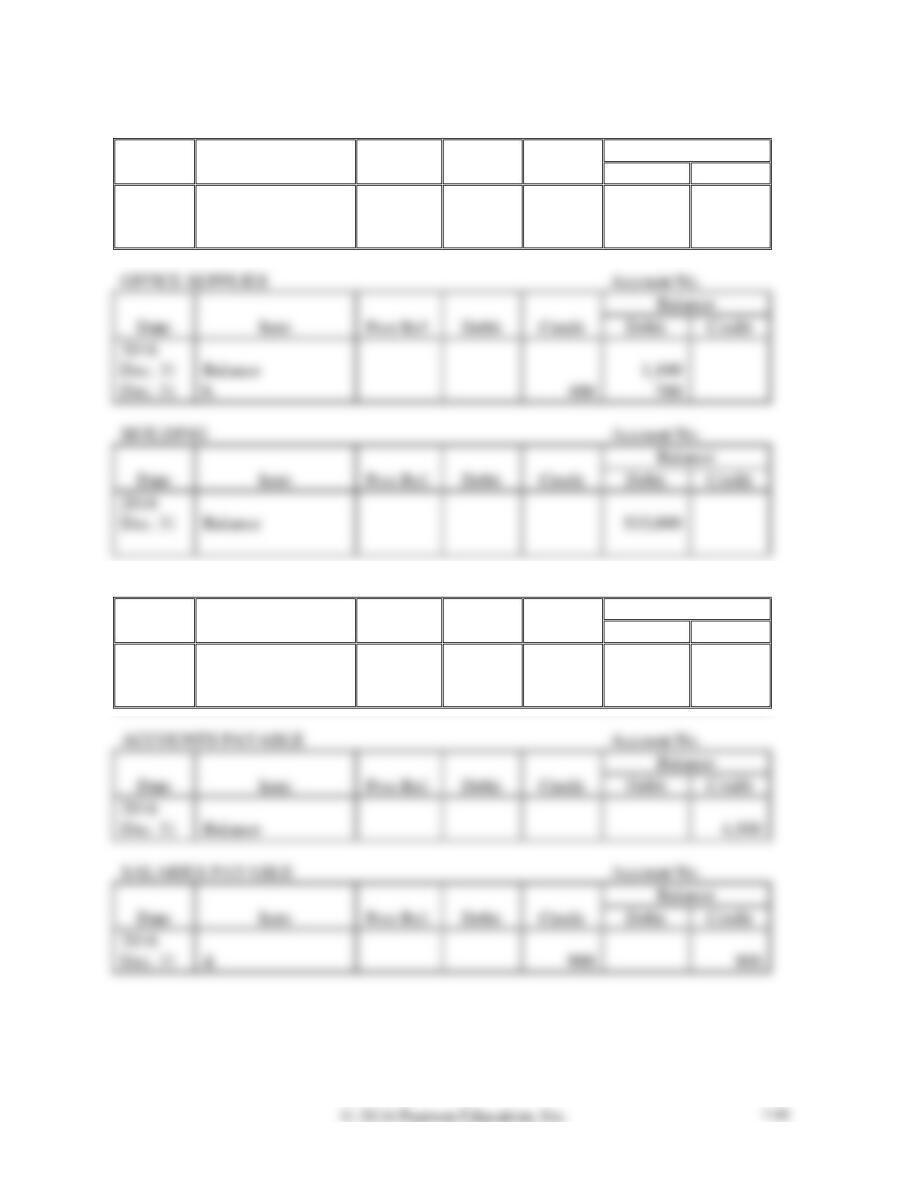

Requirement 2

CASH

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

11,900

ACCOUNTS RECEIVABLE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

13,900

P3-36A, cont.

PREPAID INSURANCE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

3,500

Dec. 31

a.

2,900

600

OFFICE SUPPLIES

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

1,100

Dec. 31

b.

700

BUILDING

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

ACCUMULATED DEPRECIATION—BUILDING

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

350,000

Dec. 31

c.

3,500

353,500

ACCOUNTS PAYABLE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

SALARIES PAYABLE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

d.

P3-36A, cont.

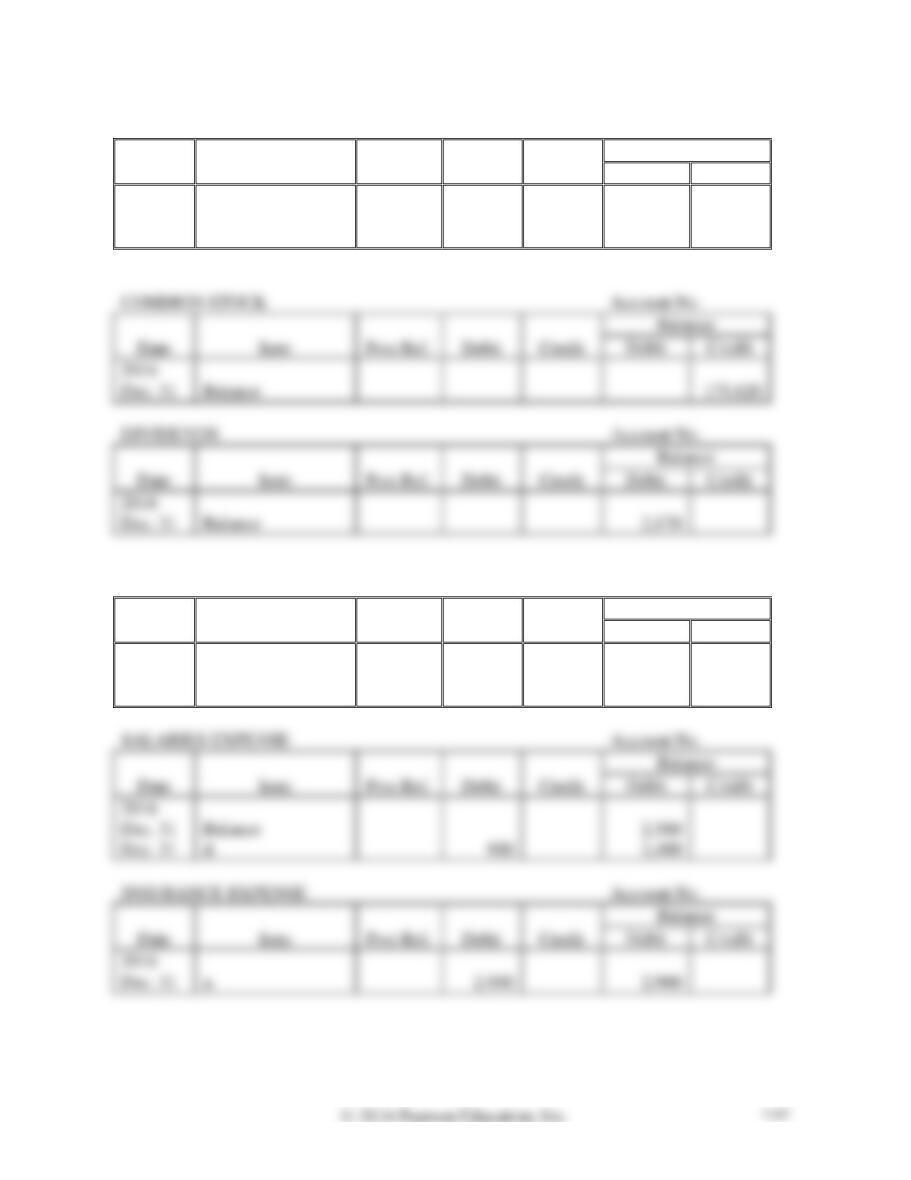

UNEARNED REVENUE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

2,500

Dec. 31

e.

1,000

1,500

COMMON STOCK

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

DIVIDENDS

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

SERVICE REVENUE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

18,200

Dec. 31

e.

1,000

19,200

SALARIES EXPENSE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

Balance

Dec. 31

d.

INSURANCE EXPENSE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

a.

2,900

P3-36A, cont.

DEPRECIATION EXPENSE—BUILDING

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

c.

3,500

3,500

ADVERTISING EXPENSE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

SUPPLIES EXPENSE

Account No.

Date

Item

Post Ref.

Debit

Credit

Balance

Debit

Credit

2016

Dec. 31

b.

Requirement 3

NEWPORT INN COMPANY

Adjusted Trial Balance

December 31, 2016

Account Title

Balance

Debit

Credit

Cash

$ 11,900

Accounts Receivable

13,900

Prepaid Insurance

600

Office Supplies

700

Building

Accumulated Depreciation—Building

Accounts Payable

Salaries Payable

900

Unearned Revenue

Common Stock

Dividends

Service Revenue

19,200

Salaries Expense

Insurance Expense

Depreciation Expense—Building

Advertising Expense

750

P3-36A, cont.

Requirement 4

No. Even if total debits equals total credits on the adjusted trial balance, this does not mean that the

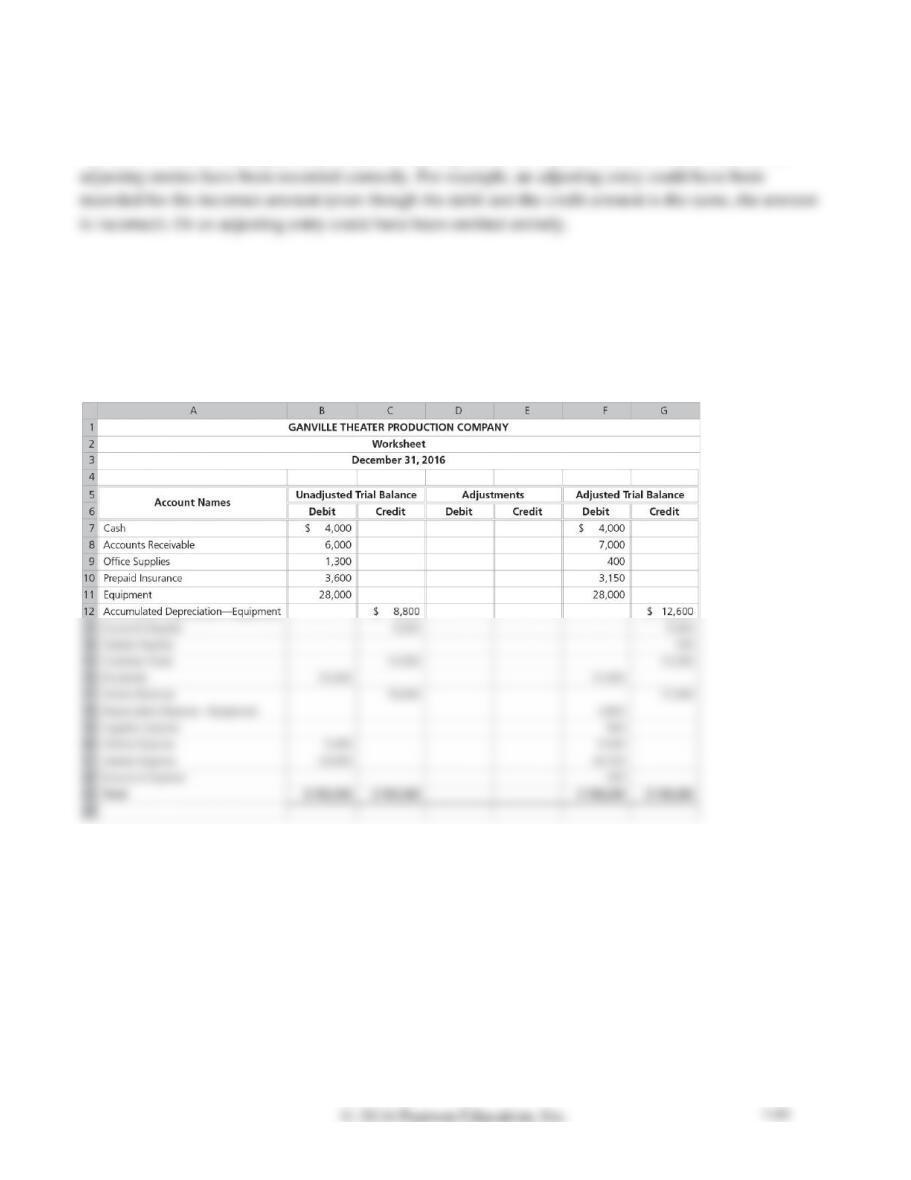

P3-37A Using the worksheet to record the adjusting journal entries

Learning Objective 6

2. d. CR Accumulated Depreciation $3,800

Ganville Theater Production Company’s partially completed worksheet as of December 31, 2016,

follows.

Requirements

1. Analyze the worksheet to determine the adjusting entries that account for the differences between the

unadjusted trial balance and the adjusted trial balance. Complete the worksheet. Use letters a through

e to label the five adjustments.

2. Journalize the adjusting entries.

SOLUTION

Requirement 1

GANVILLE THEATER PRODUCTION COMPANY

Worksheet

December 31, 2016

Account

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Debit

Credit

Debit

Credit

Debit

Credit

Cash

$ 4,000

$ 4,000

Accounts Receivable

6,000

a.

$ 1,000

7,000

Office Supplies

1,300

$ 900

b.

Prepaid Insurance

3,600

3,150

Equipment

Accumulated Depreciation—Equipment

3,800

d.

$ 12,600

Accounts Payable

5,000

Salaries Payable

Dividends

Service Revenue

1,000

Depreciation Expense—Equipment

3,800

3,800

Supplies Expense

Utilities Expense

5,400

5,400

Salaries Expense

e.

Insurance Expense

c.

450

P3-37A, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

a. Dec. 31

Accounts Receivable

1,000

Service Revenue

1,000

To accrue service revenue.

b. Dec. 31

Supplies Expense

Office Supplies

To record office supplies used.

c. Dec. 31

Insurance Expense

Prepaid Insurance

To record insurance expense.

d. Dec. 31

Depreciation Expense—Equipment

3,800

3,800

To record depreciation on equipment.

e. Dec. 31

Salaries Expense

Salaries Payable

To accrue salaries expense.

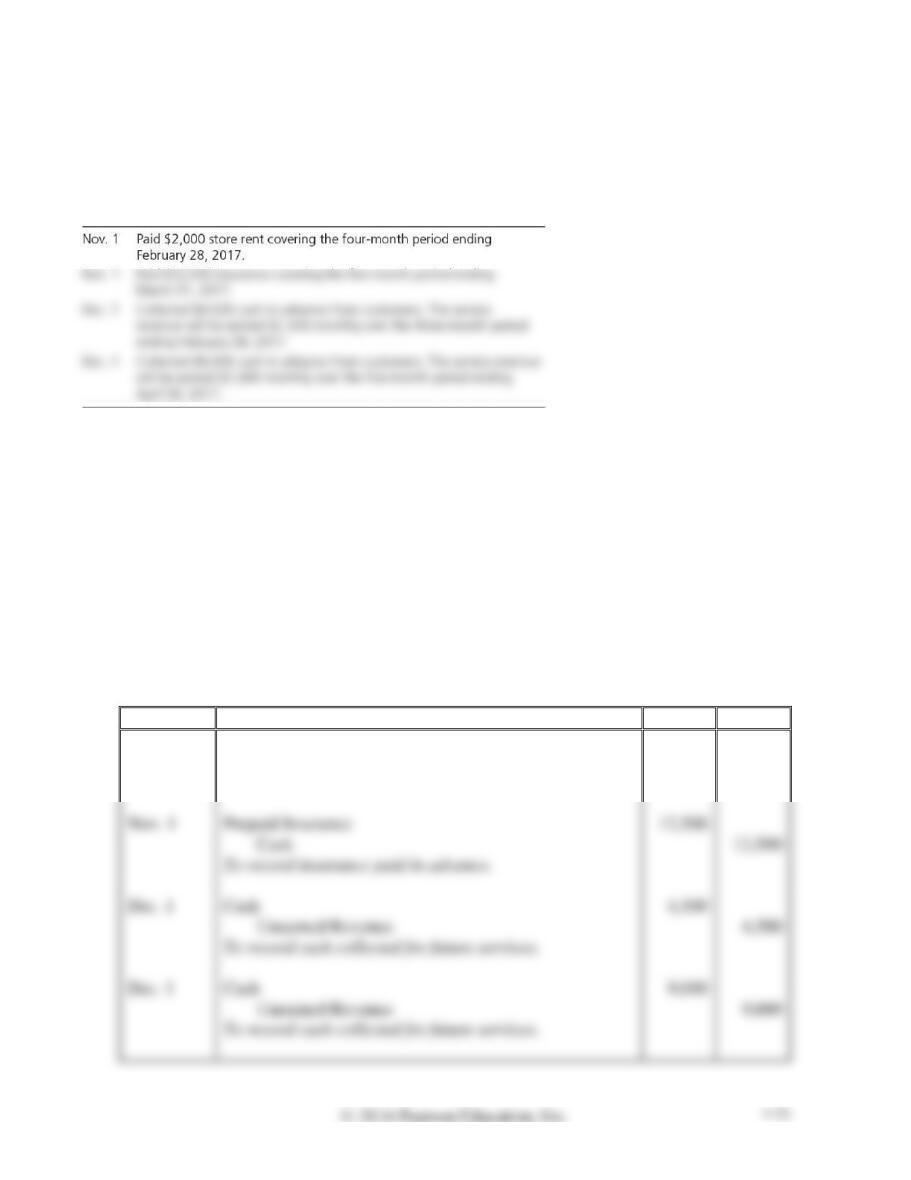

P3A-38A Understanding the alternative treatment of prepaid expenses and unearned revenues

Learning Objectives 3, 7

Appendix 3A

4. Dec 31, CR Insurance Expense $7,500

Night Flyer Pack’n Mail completed the following transactions during 2016:

Requirements

1. Journalize the transactions assuming that Night Flyer debits an asset account for prepaid expenses

and credits a liability account for unearned revenues.

2. Journalize the related adjusting entries at December 31, 2016.

3. Post the journal and adjusting entries to the T-accounts, and show their balances at December 31,

2016. (Ignore the Cash account.)

4. Repeat Requirements 1–3. This time, debit an expense account for prepaid expenses and credit a

revenue account for unearned revenues.

5. Compare the account balances in Requirements 3 and 4. They should be equal.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Nov. 1

Prepaid Rent

2,000

Cash

2,000

To record rent paid in advance.

Nov. 1

Prepaid Insurance

12,500

Cash

12,500

Dec. 1

4,500

4,500

To record cash collected for future services.

Dec. 1

9,000

9,000

P3A–38A, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Rent Expense

1,000*

Prepaid Rent

1,000*

To record rent expense.

Dec. 31

Insurance Expense

5,000*

Prepaid Insurance

5,000*

To record insurance expense.

Dec. 31

Unearned Revenue

Service Revenue

Dec. 31

Unearned Revenue

Service Revenue

advance.

* Calculations:

Adjusting Journal Entry One:

$2,000

Rent prepaid on November 1 for 4 months

4

months

$ 500

Rent expense per month

$ 500

Rent expense per month

months

$1,000

Rent expense for November and December

P3A–38A, cont.

Adjusting Journal Entry Two:

$12,500

Insurance prepaid on November 1 for 5 months

5

Months

$ 2,500

Insurance expense per month

Insurance expense per month

Months

Insurance expense for November and December

Requirement 3

Prepaid Rent

Rent Expense

Nov. 1 2,000

1,000 Dec. 31

Dec. 31 1,000

Bal. 1,000

Bal. 1,000

Insurance Expense

Nov. 1 12,500

5,000 Dec. 31

Dec. 31 5,000

Bal. 7,500

Unearned Revenue

Dec. 31 1,500

4,500 Dec. 1

1,500 Dec. 31

Dec. 31 1,800

9,000 Dec. 1

1,800 Dec. 31

10,200 Bal.

3,300 Bal.

P3A-38A, cont.

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Nov. 1

Rent Expense

2,000

Cash

2,000

To record rent paid in advance.

Nov. 1

Insurance Expense

12,500

Cash

12,500

To record insurance paid in advance.

Dec. 1

4,500

Service Revenue

4,500

To record cash collected for future services.

Dec. 1

9,000

Service Revenue

9,000

To record cash collected for future services.

Dec. 31

Prepaid Rent

1,000*

Rent Expense

1,000*

To record prepaid rent.

Dec. 31

Prepaid Insurance

7,500*

Insurance Expense

7,500*

To record prepaid insurance.

Dec. 31

Service Revenue

3,000*

Unearned Revenue

3,000*

To record unearned revenue.

Dec. 31

Service Revenue

7,200*

Unearned Revenue

7,200*

To record unearned revenue.

P3A–38A, cont.

* Calculations:

Adjusting Journal Entry One:

$2,000

Rent prepaid on November 1 for 4 months

$ 500

Rent expense per month

Thus,

$ 500

Rent expense per month

× 2

Months

$1,000

Rent still prepaid on December 31

Insurance prepaid on November 1 for 5 months

Insurance expense per month

Thus,

$2,500

Insurance expense per month

× 3

Months

Adjusting Journal Entry Three:

$ 4,500

Collected in advance on December 1 for 3 months

(1,500)

Revenue earned during December

$ 3,000

Revenue still unearned on December 31

(1,800)

Revenue earned during December

Revenue still unearned on December 31

P3A–38A, cont.

Prepaid Rent

Rent Expense

Dec. 31 1,000

Nov. 1 2,000

1,000 Dec. 31

Bal. 1,000

Bal. 1,000

Insurance Expense

Dec. 31 7,500

Nov. 1 12,500

7,500 Dec. 31

Bal. 7,500

Bal. 5,000

Unearned Revenue

3,000 Dec. 31

4,500 Dec. 1

7,200 Dec. 31

9,000 Dec. 1

10,200 Bal.

3,300 Bal.

Requirement 5

P3-39B Journalizing adjusting entries and subsequent journal entries

Learning Objective 3

1. b. DR Insurance Expense $2,000

Lorring Landscaping has the following data for the December 31 adjusting entries:

a. Each Friday, Lorring pays employees for the current week’s work. The amount of the weekly payroll

is $6,000 for a five-day workweek. This year, December 31 falls on a Tuesday. Lorring will pay its

employees on January 3.

b. On January 1 of the current year, Lorring purchases an insurance policy that covers two years,

$4,000.

Requirements

1. Journalize the adjusting entry needed on December 31 for each of the previous items affecting

Lorring Landscaping. Assume Lorring records adjusting entries only at the end of the year.

2. Journalize the subsequent journal entries for adjusting entries a, d, and g.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

a. Dec. 31

Salaries Expense

2,400*

Salaries Payable

2,400*

To accrue salaries expense.

b. Dec. 31

Insurance Expense

2,000*

Prepaid Insurance

2,000*

To record insurance expense.

c. Dec. 31

Supplies Expense

7,400*

Office Supplies

7,400*

To record office supplies used.

d. Dec. 31

Unearned Revenue

2,000*

Service Revenue

2,000*

advance.

e. Dec. 31

Accounts Receivable

Service Revenue

To accrue service revenue.

f. Dec. 31

Depreciation Expense—Equipment

Depreciation Expense—Trucks

To record depreciation on equipment and trucks.

g. Dec. 31

Interest Expense

Interest Payable

To accrue interest expense.

P3-39B, cont.

* Calculations:

a:

$6,000

Payroll for a 5-day work week

5

work days

$1,200

Salaries expense per work day

Thus,

$1,200

Salaries expense per work day

× 2

work days

$2,400

Salaries expense for Monday through Tuesday

Insurance prepaid on January 1 for two years

years

Insurance expense for one year

$4,100

Beginning balance of office supplies

Office supplies on hand

$7,400

Supplies expense (cost of office supplies used)

$4,000

Collected in advance during December

Percentage earned during December

$2,000

Revenue earned during December