CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-21

PROBLEM 3-3 (Concluded)

2. EXPERT CONSULTING SERVICES INC.

INCOME STATEMENT

FOR THE MONTH OF MARCH

Revenues:

Computer installation services ………………………………. $4,000

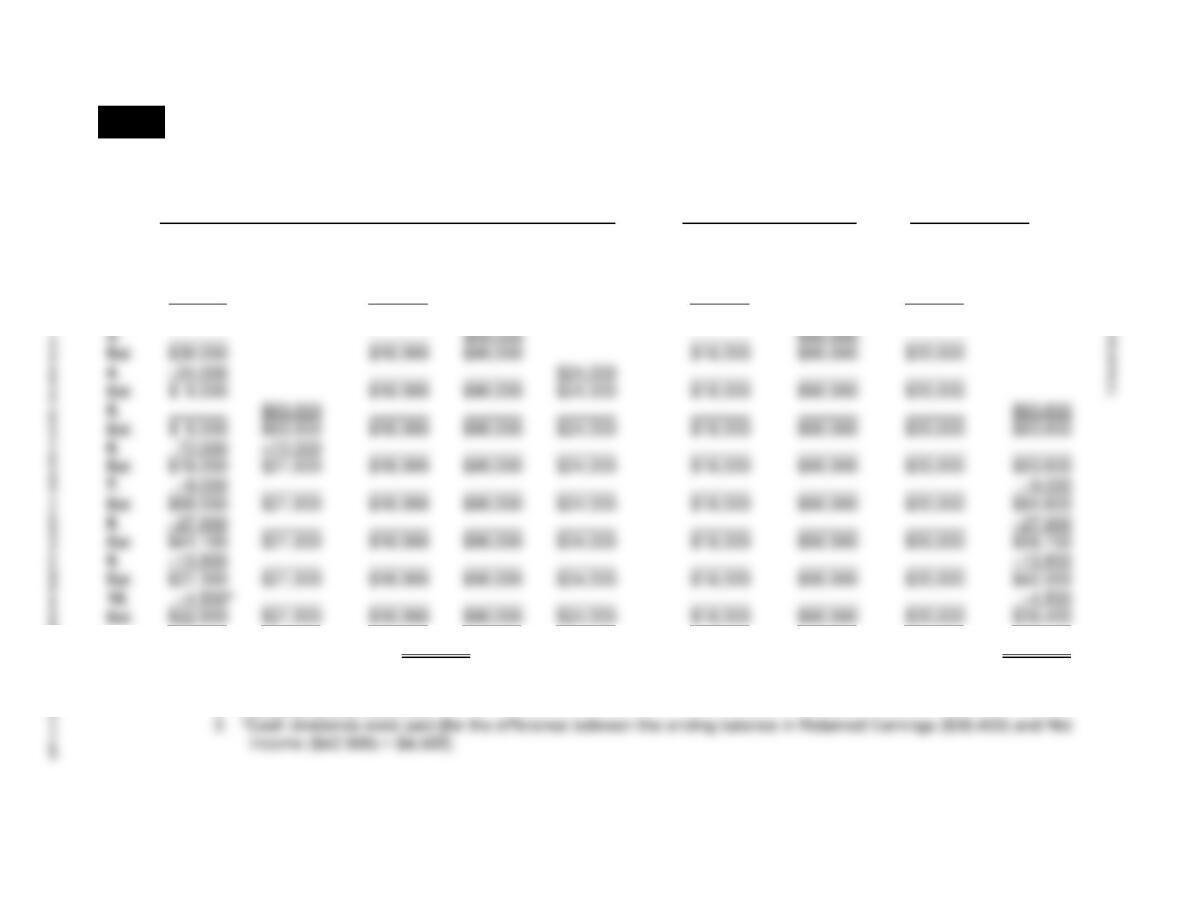

3. EXPERT CONSULTING SERVICES INC.

BALANCE SHEET

MARCH 31

Assets

Current assets:

Cash …………………………………………………………………. $44,800

Accounts receivable ……………………………………………. 3,000

Supplies …………………………………………………………….. 700

Total current assets …………………………………………………. $48,500

4. Trade accounts often have a 30-day collection or payment period. For example,

cash should be received in April from the services provided on account on March 19.

Cash will most likely be paid in April for the $700 of miscellaneous supplies bought

on account on March 12.

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

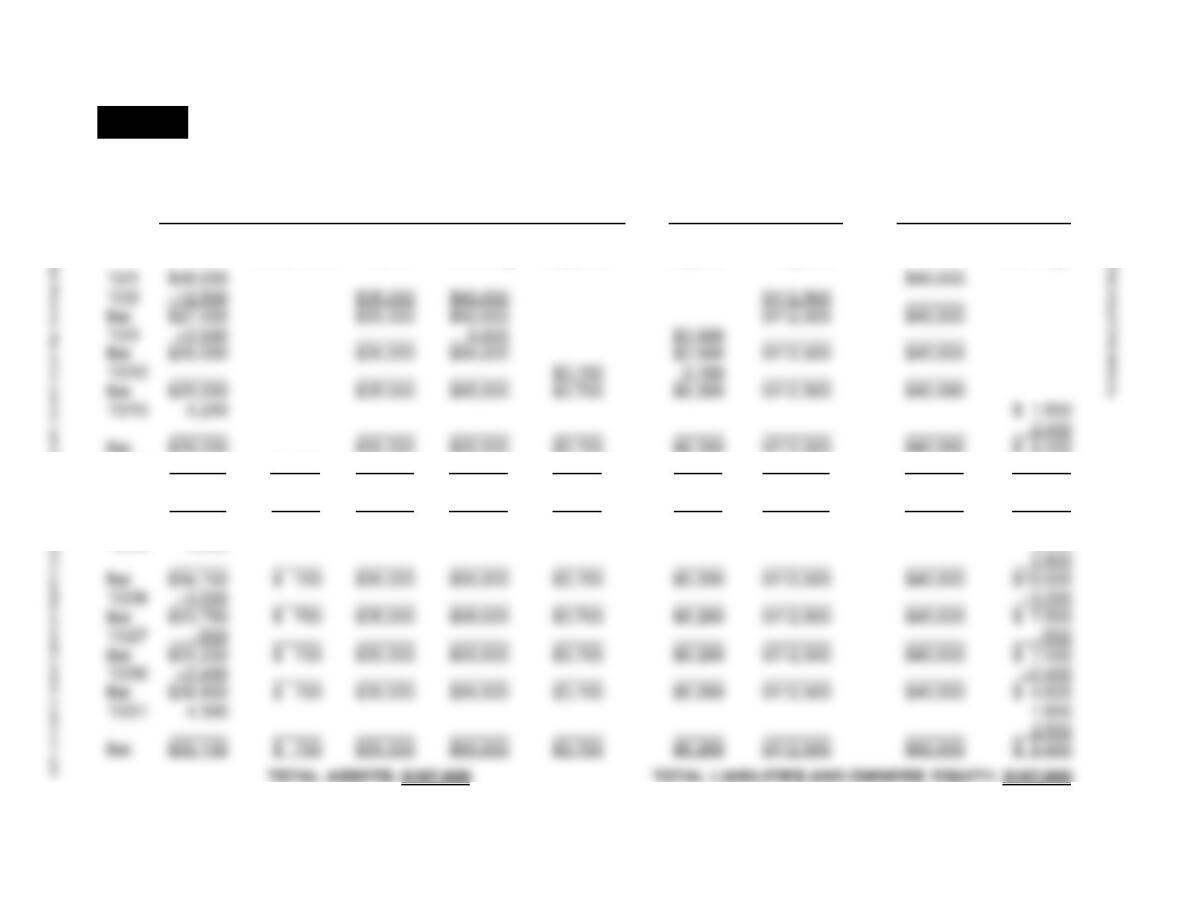

LO 3 PROBLEM 3-4 TRANSACTIONS RECONSTRUCTED FROM FINANCIAL STATEMENTS

ELM CORPORATION

TRANSACTIONS FOR THE MONTH OF JUNE

Assets = Liabilities + Owners’ Equity

Accounts Accounts Notes Capital Retained

Cash Receivable Equipment Building Land Payable Payable Stock Earnings

1. $30,000 $30,000

2. $18,000 $18,000

Bal. $30,000 $18,000 $18,000 $30,000

TOTAL ASSETS: $176,400 TOTAL LIABILITIES AND OWNERS’ EQUITY: $176,400

Assumptions: 1. The land was acquired for cash.

2. All sales were on account.

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-23

MULTI-CONCEPT PROBLEMS

LO 1,2 PROBLEM 3-5 IDENTIFICATION OF EVENTS WITH SOURCE DOCUMENTS

All of these events would be recorded in the entity’s accounts.

a. Payment of the insurance policy would be recorded with the use of the invoice from

the insurance company. The amount and period covered would be used to record

the event.

d. Source documents are needed to record the reduction in supplies and the amount of

loss from the fire. Invoices for supplies purchased and requisition forms for supplies

are important source documents for this purpose. By deducting the amount used (as

shown on the requisition forms) from the amount bought (per the invoices), one

could determine the amount of loss.

h. The lease agreement itself serves as the source document to record this event. The

amounts paid for taxes, title, and license are recorded on the basis of the lease

agreement.

LO 3,5 PROBLEM 3-6 ACCOUNTS USED TO RECORD TRANSACTIONS

Accounts

Accounts

Debited Credited Debited Credited

a. 1 10 f. 1 2

b. 5 1, 9 g. 13 1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3,4,5 PROBLEM 3-7 TRANSACTION ANALYSIS AND JOURNAL ENTRIES RECORDED DIRECTLY IN T ACCOUNTS

1. BEVERLY ENTERTAINMENT ENTERPRISES

TRANSACTIONS FOR THE MONTH OF OCTOBER

Assets = Liabilities + Owners’ Equity

Accounts Concession Accounts Notes Capital Retained

Cash Receivable Land Building Supplies Payable Payable Stock Earnings

10/17 $1,500 1,500

Bal. $29,200 $1,500 $35,000 $95,000 $3,700 $6,200 $112,500 $40,000 $ 5,700

10/23 750 –750

Bal. $29,950 $ 750 $35,000 $95,000 $3,700 $6,200 $112,500 $40,000 $ 5,700

10/24 4,800 2,000

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-25

PROBLEM 3-7 (Concluded)

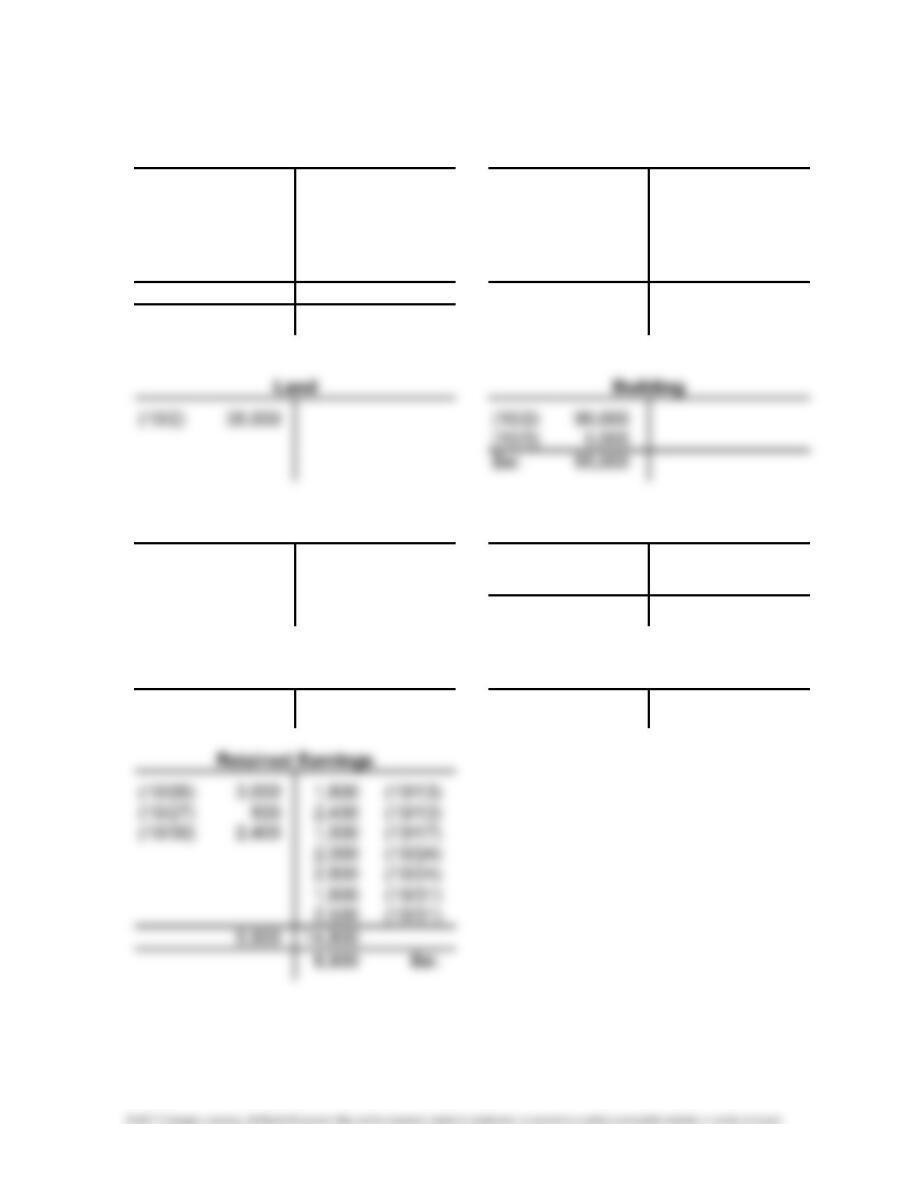

2. Cash Accounts Receivable

(10/1) 40,000 12,500 (10/2) (10/17) 1,500 750 (10/23)

(10/13) 4,200 2,500 (10/3)

(10/23) 750 3,000 (10/26)

(10/24) 4,800 500 (10/27)

(10/31) 4,300 2,400 (10/30)

54,050 20,900 Bal. 750

Bal. 33,150

Concession Supplies Accounts Payable

(10/12) 3,700 2,500 (10/3)

3,700 (10/12)

6,200 Bal.

Notes Payable Capital Stock

112,500 (10/2) 40,000 (10/1)

3-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4,7 PROBLEM 3-8 TRIAL BALANCE AND FINANCIAL STATEMENTS

1. BEVERLY ENTERTAINMENT ENTERPRISES

TRIAL BALANCE

OCTOBER 31

Debits Credits

Cash ……………………………………………………………………… $ 33,150

Accounts Receivable ……………………………………………….. 750

2. BEVERLY ENTERTAINMENT ENTERPRISES

INCOME STATEMENT

FOR THE MONTH OF OCTOBER

Revenues:

Ticket sales………………………………………………………… $5,600*

Concession sales ……………………………………………….. 7,700**

3. BEVERLY ENTERTAINMENT ENTERPRISES

STATEMENT OF RETAINED EARNINGS

FOR THE MONTH OF OCTOBER

Beginning balance, October 1 ……………………………………………………….. $ 0

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-27

PROBLEM 3-8 (Concluded)

4. BEVERLY ENTERTAINMENT ENTERPRISES

BALANCE SHEET

OCTOBER 31

Assets

Current assets:

Cash …………………………………………………………………. $33,150

Accounts receivable ……………………………………………. 750

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable ……………………………………………….. $ 6,200

Long-term debt:

Notes payable …………………………………………………….. 112,500

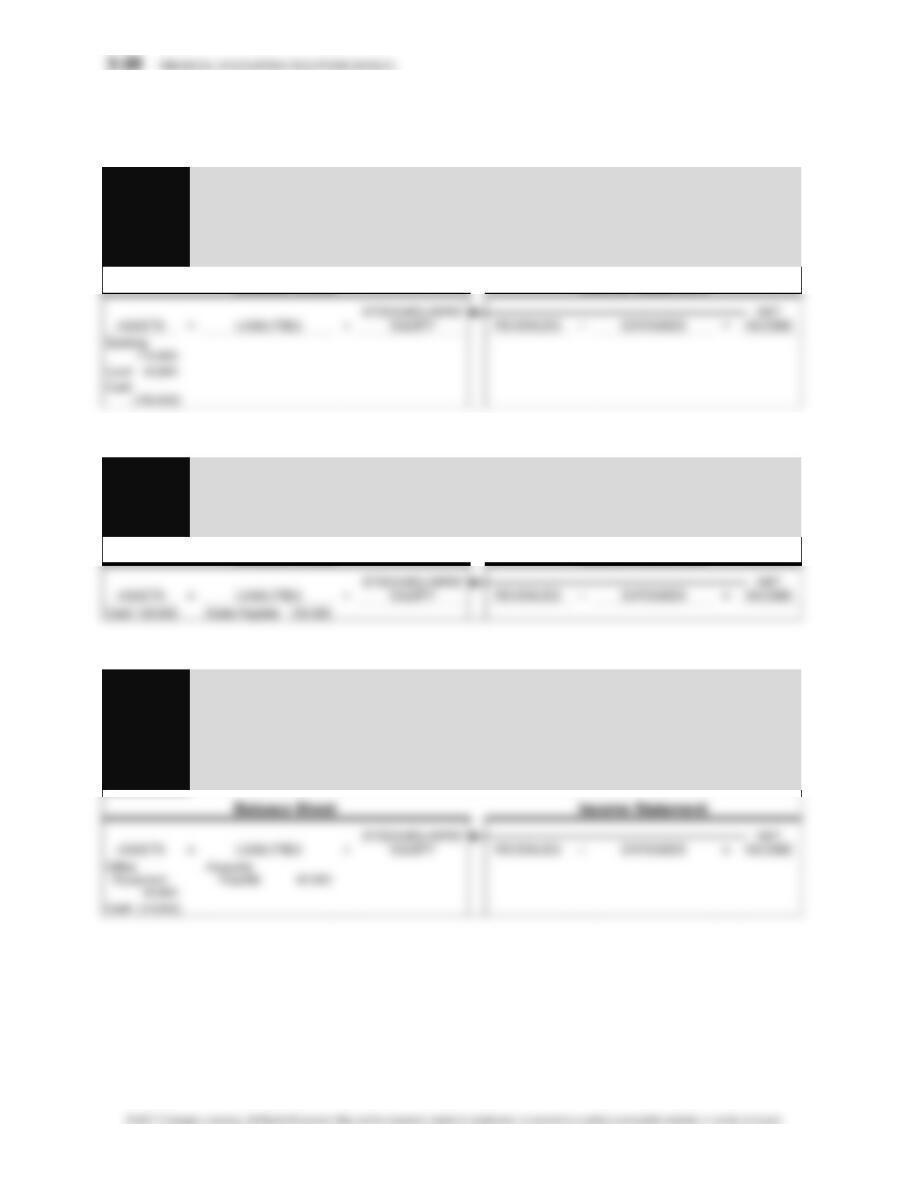

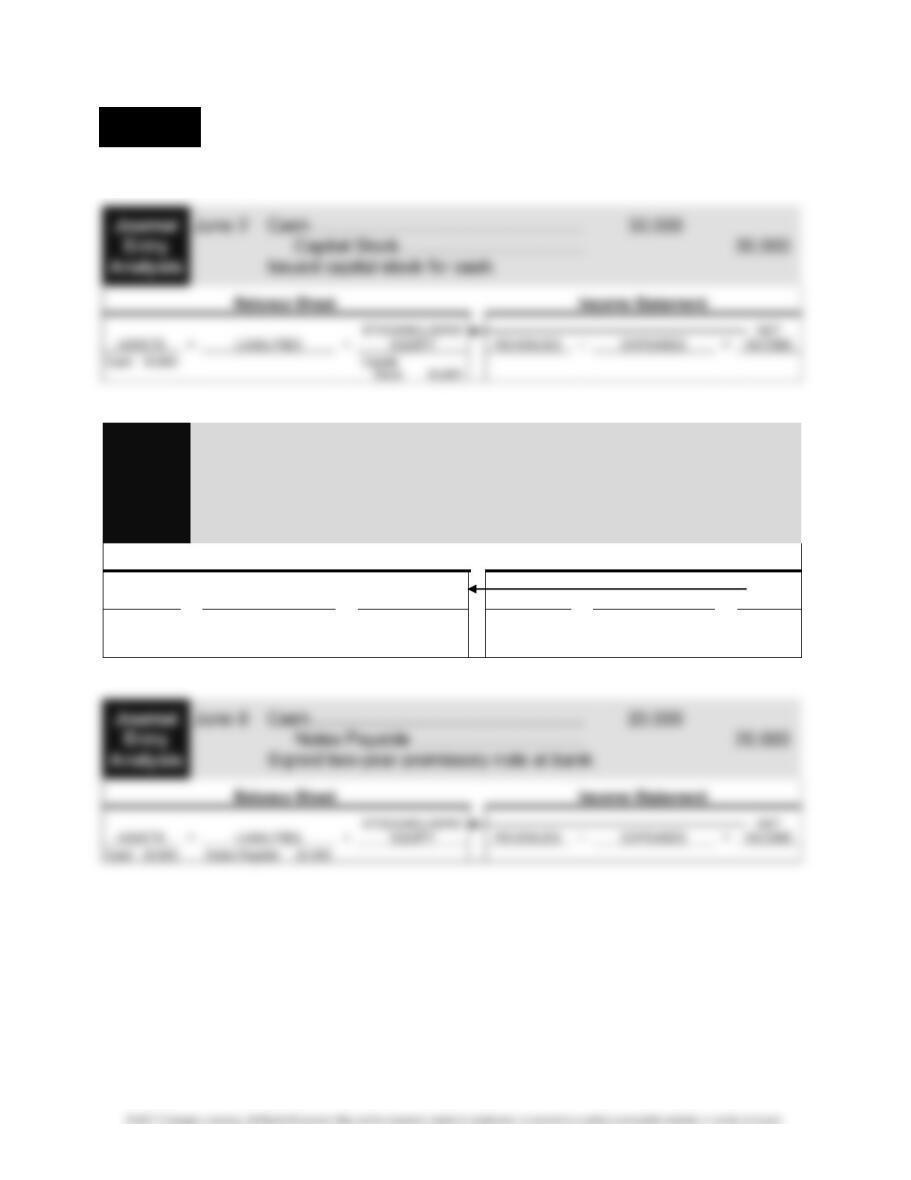

LO 3,5,6 PROBLEM 3-9 JOURNAL ENTRIES

a.

Journal Cash …………………………………………………………. 200,000

Entry Capital Stock ………………………………………… 200,000

Analysis Issued 100,000 shares of capital stock for cash.

PROBLEM 3-9 (Continued)

b.

Journal Building ……………………………………………………… 110,000

Entry Land ………………………………………………………….. 40,000

Analysis Cash ……………………………………………………. 150,000

Acquired building and land for cash.

Balance Sheet Income Statement

c.

Journal Cash …………………………………………………………. 125,000

Entry Notes Payable ………………………………………. 125,000

Analysis Signed three-year promissory note.

Balance Sheet Income Statement

d.

Journal Office Equipment ………………………………………… 50,000

Entry Cash ……………………………………………………. 10,000

Analysis Accounts Payable …………………………………. 40,000

Purchased equipment, with down payment

and balance due in ten days.

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-29

PROBLEM 3-9 (Continued)

e.

Journal Wage and Salary Expense …………………………… 13,000

Entry Cash ……………………………………………………. 13,000

Analysis Paid payroll for first half of month.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (13,000

)

(13,000)

Wage and Salary

Expense 13,000

(13,000)

f.

)

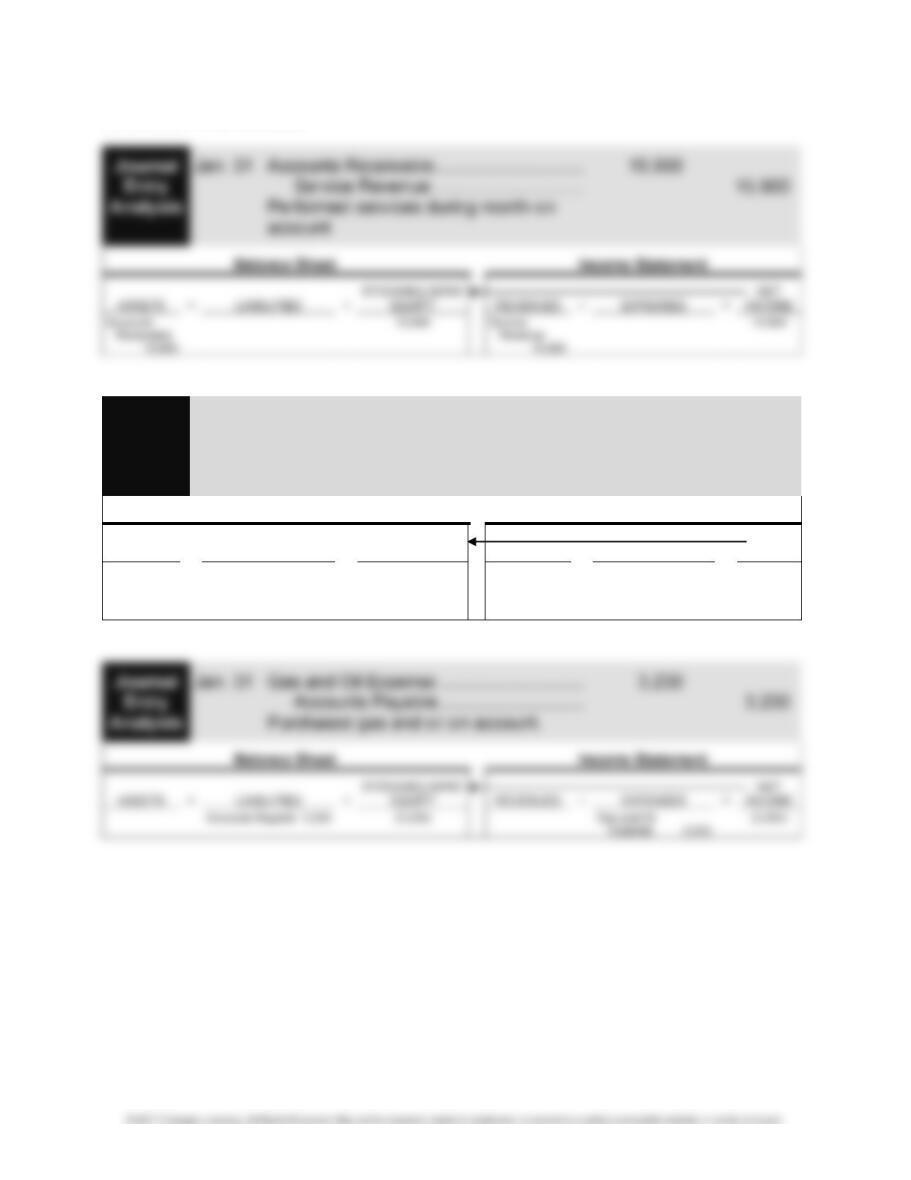

g.

Journal Accounts Receivable …………………………………… 24,000

Entry Advertising Revenue ……………………………… 24,000

Analysis Sold advertising during January, due by

February 15.

3-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

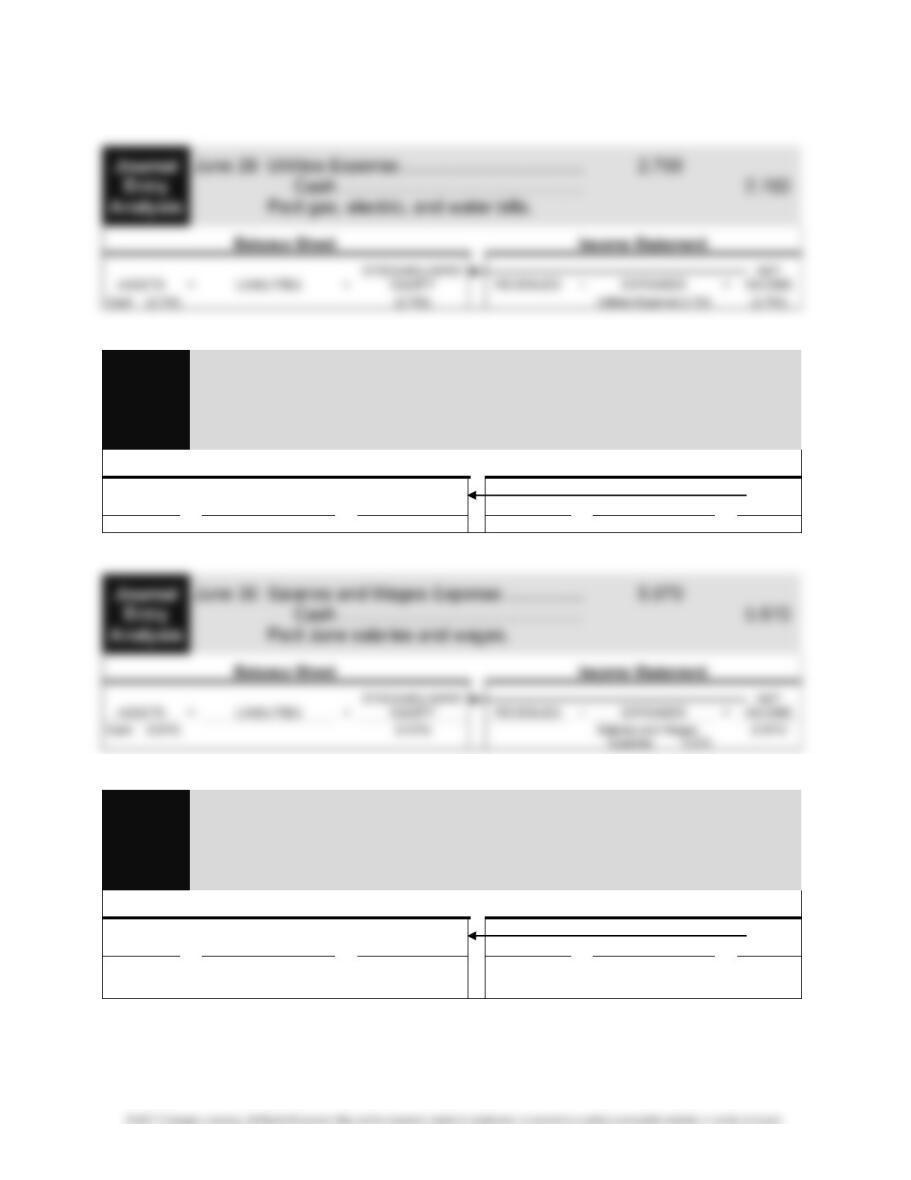

PROBLEM 3-9 (Concluded)

h.

Journal Wage and Salary Expense …………………………… 15,000

Entry Cash ……………………………………………………. 15,000

Analysis Paid payroll for second half of month.

Balance Sheet Income Statement

i.

Journal Commissions Expense ………………………………… 3,500

Entry Commissions Payable ……………………………. 3,500

Analysis Commissions earned by salespeople during

January, to be paid on February 5.

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-31

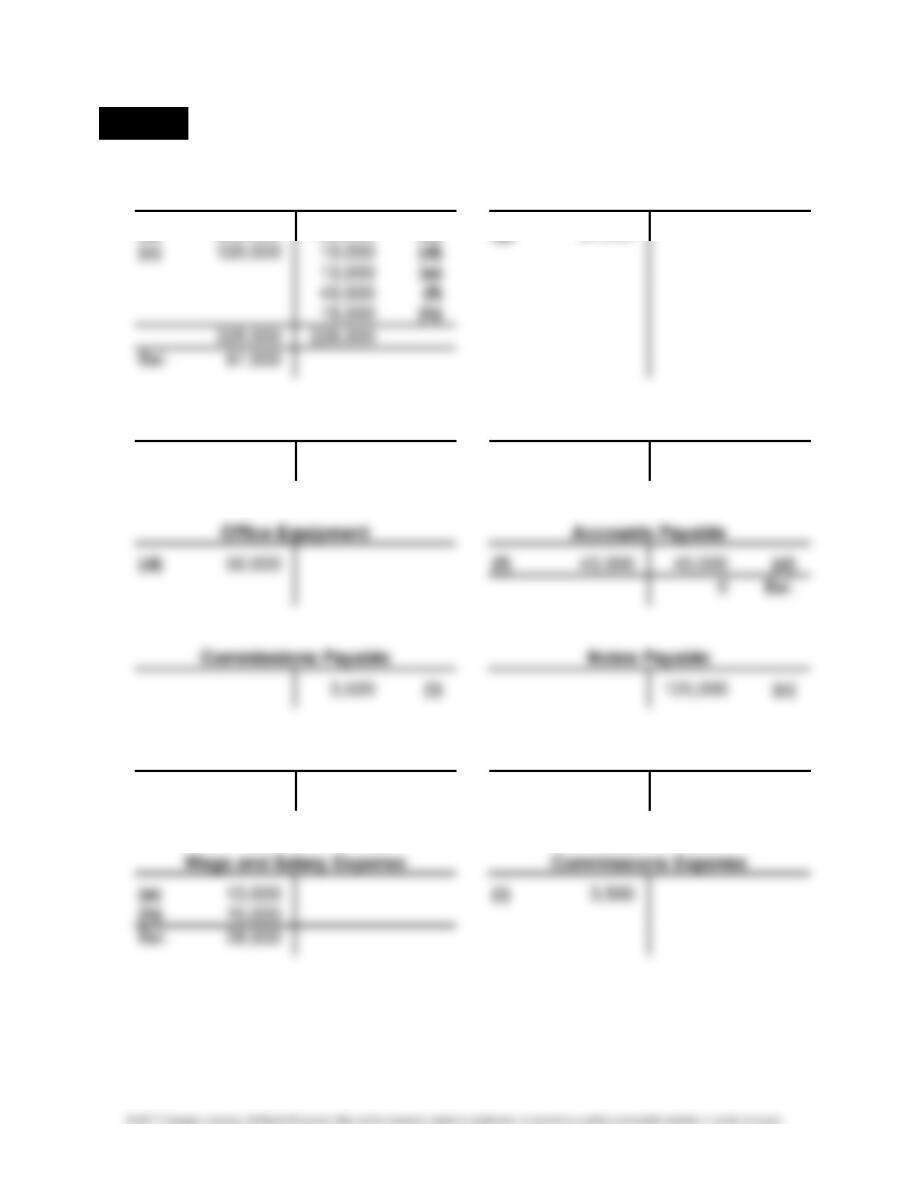

LO 3,4,5 PROBLEM 3-10 JOURNAL ENTRIES RECORDED DIRECTLY IN T ACCOUNTS

1. T Accounts

Cash Accounts Receivable

(a) 200,000 150,000 (b) (g) 24,000

Land Building

(b) 40,000 (b) 110,000

Capital Stock Advertising Revenue

200,000 (a) 24,000 (g)

3-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 3-10 (Concluded)

2. ATKINS ADVERTISING AGENCY

TRIAL BALANCE

JANUARY 31

Debits Credits

Cash ……………………………………………………………………… $ 97,000

Accounts Receivable ……………………………………………….. 24,000

Land ………………………………………………………………………. 40,000

LO 3,5,7 PROBLEM 3-11 THE DETECTION OF ERRORS IN A TRIAL BALANCE AND

PREPARATION OF A CORRECTED TRIAL BALANCE

1. The trial balance is out of balance by $220,640 – $208,840, or $11,800. The differ-

ence can be accounted for as follows:

Amount by which trial balance is out of balance: $ 11,800

Dividends account should be a debit balance, not a credit balance;

removing a credit balance and replacing it with a debit balance

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-33

PROBLEM 3-11 (Concluded)

2. MALCOLM INC.

REVISED TRIAL BALANCE

JANUARY 31

Debits Credits

Cash ……………………………………………………………………… $ 9,980

Accounts Receivable ……………………………………………….. 8,640

Land ………………………………………………………………………. 80,000

LO 3,5,6,7 PROBLEM 3-12 JOURNAL ENTRIES, TRIAL BALANCE, AND FINANCIAL

STATEMENTS

1. Journal entries:

Journal Jan. 2 Cash ………………………………………………. 100,000

Entry Capital Stock ………………………………. 100,000

Analysis Issued 100,000 shares of capital stock

for cash.

3-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 3-12 (Continued)

Journal Jan. 3 Warehouse ……………………………………… 60,000

Entry Land ………………………………………………. 20,000

Analysis Cash …………………………………………. 80,000

Purchased warehouse and land for cash.

Balance Sheet Income Statement

Journal Jan. 4 Cash ………………………………………………. 50,000

Entry Notes Payable ……………………………. 50,000

Analysis Signed three-year promissory note

at Third State Bank.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 50,000 Notes Payable 50,000

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-35

PROBLEM 3-12 (Continued)

Journal Jan. 31 Cash ………………………………………………. 7,490

Entry Accounts Receivable …………………… 7,490

Analysis Received cash from customers on

account.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 7,490

Accounts

Receivable

(7,490

)

3-36 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 3-12 (Continued)

2. BLUE JAY DELIVERY SERVICE

TRIAL BALANCE

JANUARY 31

Debits Credits

Cash ……………………………………………………………………… $ 32,490

Warehouse …………………………………………………………….. 60,000

Land ………………………………………………………………………. 20,000

Delivery Trucks ……………………………………………………….. 45,000

3. BLUE JAY DELIVERY SERVICE

INCOME STATEMENT

FOR THE MONTH OF JANUARY

Service revenue ………………………………………………………………………….. $15,900

Gas and oil expense ……………………………………………………………………. 3,230

Net income …………………………………………………………………………………. $12,670

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-37

PROBLEM 3-12 (Concluded)

4. BLUE JAY DELIVERY SERVICE

BALANCE SHEET

JANUARY 31

Assets

Current assets:

Cash …………………………………………………………………. $ 32,490

Accounts receivable ……………………………………………. 8,410

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable ……………………………………………….. $ 3,230

Long-term debt:

Notes payable …………………………………………………….. 50,000

5. Additional information needed:

Jan. 3: Is the warehouse new?

How large is it?

What volume of business can it support?

Is it insured?

Jan. 4: What is the interest rate on the loan?

Are there any restrictions on the company’s operations in the debt

3-38 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3,5,6,7 PROBLEM 3-13 JOURNAL ENTRIES, TRIAL BALANCE, AND FINANCIAL

STATEMENTS

1. Journal entries:

Journal June 5 Computer ……………………………………….. 12,000

Entry Cash …………………………………………. 2,500

Analysis Accounts Payable ……………………….. 9,500

Purchased computer with down payment;

balance due in 60 days.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Computer

12,000

Cash (2,500

)

Accounts Payable 9,500

CHAPTER 3 • PROCESSING ACCOUNTING INFORMATION 3-39

PROBLEM 3-13 (Continued)

Journal June 17 Advertising Expense ………………………… 900

Entry Cash …………………………………………. 900

Analysis Paid for June advertising.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (900

)

(900)

Advertising

Expense 900

(900)

3-40 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 3-13 (Continued)

Journal June 29 Rent Expense………………………………….. 2,200

Entry Rent Payable ……………………………… 2,200

Analysis Received bill for June rent to be paid

by July 10.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Rent Payable 2,200 (2,200) Rent Expense 2,200 (2,200)

Journal June 30 Accounts Receivable ………………………… 18,400

Entry Service Revenue ………………………… 18,400

Analysis Billed customers for services rendered

during the second half of June.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts

Receivable

18,400

18,400

Service

Revenue

18,400

18,400