Chapter 3

Processing Accounting

Information

After studying this chapter, students should be able to:

◼ Explain the difference between external and internal events (Module 1–LO1).

◼ Explain the role of source documents in an accounting system (Module 1–LO2).

INSTRUCTOR’S MANUAL

3-2

Chapter Outline

MODULE 1 TRANSACTIONS AND THE ACCOUNTING

EQUATION

Module 1

LO 1

Transactions and the Accounting Equation

External and Internal Events

◼ An event is a happening of consequence to an entity.

◼ An event must be able to be measured reliably to be recognized.

Module 1

LO 2

The Role of Source Documents in Recording Transactions

A source document provides the evidence needed in an accounting system to record a transaction.

◼ Source documents take many different forms. They include:

Module 1

LO 3

Analyzing the Effects of Transactions on the Accounting Equation

Economic events are the basis for recording transactions in an accounting system.

◼ For every transaction, it is essential to analyze its effect on the accounting equation.

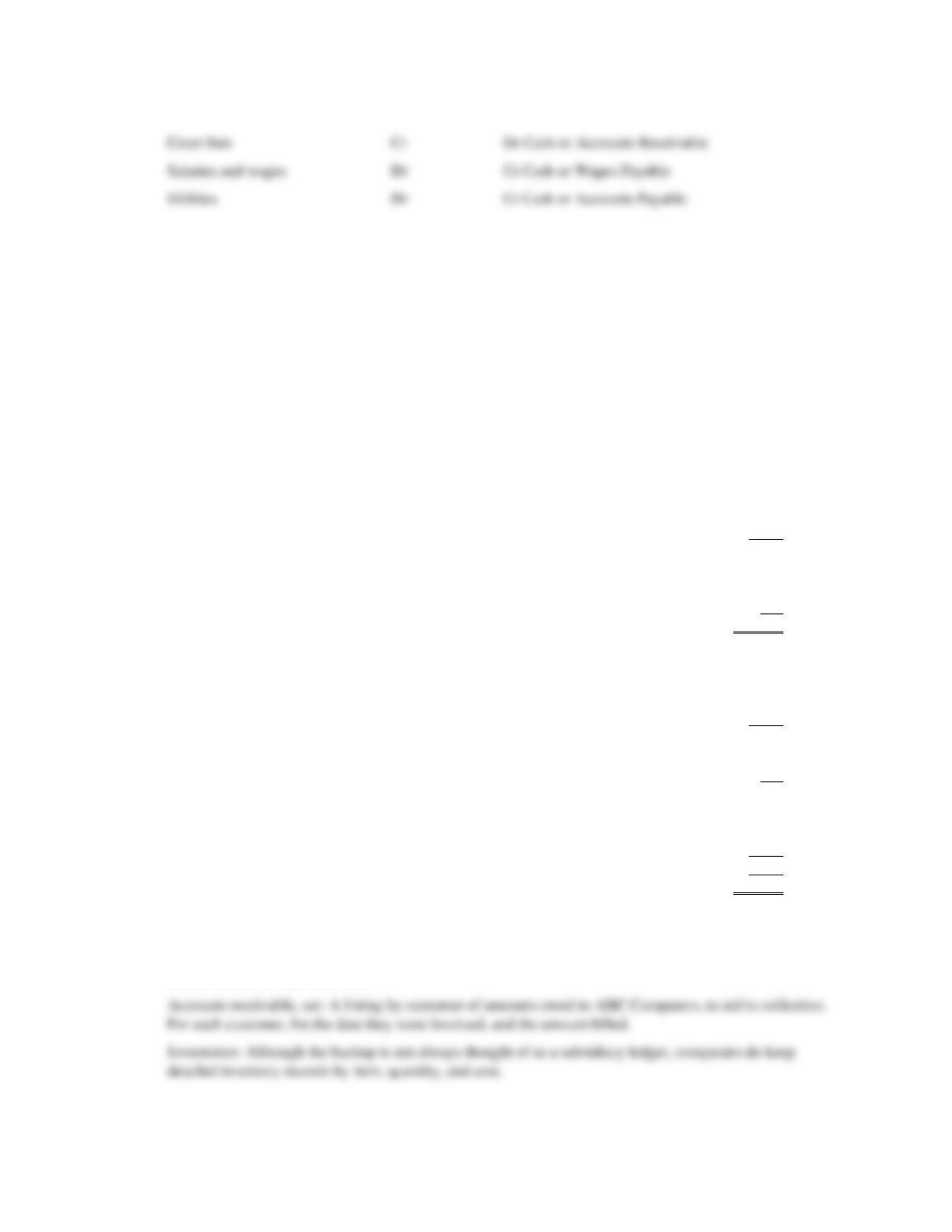

◼ (1) Issuance of capital stock. Increases both assets (Cash) and stockholders’ equity (Capital

Stock).

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

3-3

◼ (2) Acquisition of property in exchange for a note. Increases both assets (Land and Building) and

liabilities (Notes Payable).

⚫ A promissory note is a liability.

◼ (5) Sale of court time for cash. Both assets (Cash) and stockholders’ equity (Retained Earnings)

increase.

◼ (6) Payment of wages and salaries.

⚫ Expense: outflow of assets resulting from the sale of goods or services.

⚫ Expenses decrease stockholders’ equity (specifically Retained Earnings).

⚫ Both assets (Cash) and stockholders’ equity (Retained Earnings) decrease.

◼ (7) Payment of utilities. Both assets (Cash) and stockholders’ equity (Retained Earnings) decrease.

The Cost Principle

◼ The cost principle requires that an asset be recorded at the cost to acquire it and continue to be

shown at this amount on all balance sheets until the asset is disposed of.

⚫ Generally do not use market value because of subjectivity.

⚫ Cost of an asset can be verified by an independent observer and is therefore more objective

INSTRUCTOR’S MANUAL

3-4

Balance Sheet and Income Statement for Glengarry Health Club

◼ See Exhibits 3-1 through 3-3 in the text.

MODULE 2 LEDGER ACCOUNTS AND DEBITS AND CREDITS

Module 2

LO 4

Ledger Accounts and Debits and Credits

An account is used to record changes in individual items in the financial statements.

◼ The basic unit for recording transactions.

Chart of Accounts

◼ The chart of accounts is a numerical list of all the accounts an entity uses.

The General Ledger

◼ File, book, hard drive, or another device containing all of the accounts.

The Double-Entry System

◼ Concept introduced in 1494 by a Franciscan monk, Luca Pacioli.

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

The T Account

◼ The T account is a simplified form of general ledger account that shows left and right side entries

to each individual account on a big “T.”

Module 2

LO 5

Debits and Credits

Debits and credits are tools to record increases and decreases in accounts.

◼ Left side of any account is called the debit side; the right side of any account is called the credit

side.

⚫ Debit and credit can also be used as verbs: we debit (enter an amount on the left side of the

account) or credit (enter an amount on the right side) an account.

◼ Based on the accounting equation, the conventions for using T accounts for assets and liabilities

are opposite.

⚫ An increase to an asset account is recorded as a debit and a decrease is recorded as a credit.

Debits Aren’t Bad and Credits Aren’t Good

◼ In accounting, debit means one thing: an entry made on the left side of the account.

INSTRUCTOR’S MANUAL

3-6

Debits and Credits for Revenues, Expenses, and Dividends

◼ Each revenue item is maintained in a separate account rather than being recorded directly in

Retained Earnings.

⚫ Retained Earnings is increased with a credit.

⚫ Revenue is an increase in Retained Earnings; therefore revenue is increased with a credit.

⚫ Because revenue is increased with a credit, it is decreased with a debit.

⚫ Because dividends are increased with a debit, they are decreased with a credit.

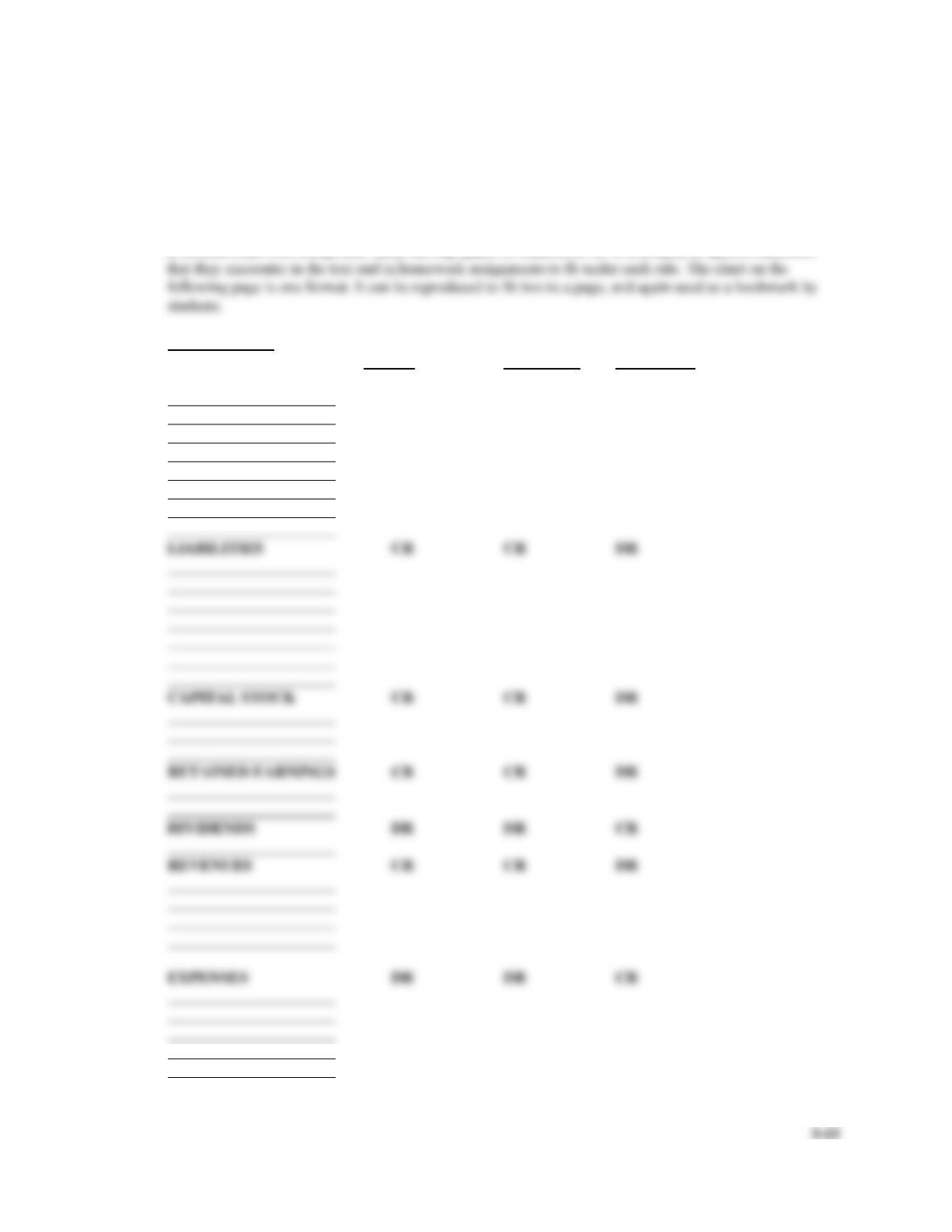

Summary of the Rules for Increasing and Decreasing Accounts and Normal Account

Balances

Asset

Liability

Capital

Stock

& Retained

Earnings

Revenue

Expense

Dividend

Increase

Dr

Cr

Cr

Cr

Dr

Dr

Decrease

Dr

Dr

Cr

Normal balance

Dr

Cr

Cr

Cr

Dr

Dr

Normal Account Balances

◼ A “normal” balance is usually the way the account is increased, or the balance we usually expect

the account to have.

Debits and Credits Applied to Transactions

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

3-7

Transactions for Glengarry Health Club

Three steps are involved in recording a transaction in the accounts:

◼ Analyze the transaction. Decide what accounts are increased or decreased and by how much.

MODULE 3 JOURNAL ENTRIES AND TRIAL BALANCES

Module 3

LO 6

Journal Entries and Trial Balances

A journal is a chronological record of a company’s transactions.

◼ Record of each transaction.

⚫ Transactions are first recorded in chronological order in the journal.

◼ Journalizing is the process of recording entries in a journal. The standard format for a journal

entry:

⚫ Date on the first line.

⚫ Account debited on the first line, followed by amount debited in a column labeled Debit.

⚫ Account credited indented to the right on next line followed by amount credited in Credit

column to right of Debit column.

Accounts credited are indented to distinguish them from accounts debited.

⚫ Explanation of entry on last line.

INSTRUCTOR’S MANUAL

3-8

◼ Journal entries and ledger accounts are tools used by accountants.

◼ Posting is the process of transferring (copying) amounts from the journal to the proper ledger

account (EXAMPLE 3-6).

⚫ Cross-referencing between the journal and the ledger:

As amounts are entered in the ledger accounts, the Posting Reference column is filled in

with the page number of the journal.

Module 3

LO 7

The Trial Balance

The trial balance is a list of each account and its balance at a specific point in time. (Example 3-7)

◼ Not a financial statement, but a convenient device to prove the equality of the debit and credit

balances in the accounts

⚫ Used to facilitate the preparation of the financial statements.

◼ Proves that total debits equals the total credits in the ledger.

A Final Note: Processing Accounting Information

In the text, whenever a journal entry is shown, it will also show how the transaction affects the financial

statements.

◼ This is called Journal Entry Analysis.

⚫ The journal entry presents the changes in the accounts in debit and credit form.

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

3-9

Lecture Suggestions

Module 1

LO 1

and

LO 2

Have the students list some possible transactions that would affect a business. Then sort the list by

internal and external events. Finally, have the students determine what, if any, source documents

would be available for each transaction. Does every event that affects a business need to be

recorded?

Module 2

LO 4

Compare the general ledger cash account to a checkbook register. Both represent a location at

which a user can view both the details and the account balance of a single account.

Module 2

LO 5

Module 2

LO 5

Accounting is beginning to be confusing. Just when students thought they understood what was

happening, these rules of recording appear. The rules take time and practice to become second

nature, and in the meantime, students can be saved the frustration of repeatedly flipping through

Students may be grumbling about this “crazy accounting system” and wondering who came up

with all of these rules. The answer is Luca Pacioli, who is often considered the founder of modern

accounting. Luca Pacioli was born around 1445 in Tuscany, Italy. He was a Franciscan monk, a

true “Renaissance man,” who had an extensive knowledge and love of many subjects – religion,

business, mathematics, and art. He believed in the harmony and interrelatedness of these

problem at the end of the chapter. Using new numbers prevents the class from responding to your

questions with the numbers in the book, instead of thinking through the transactions themselves. A

pro forma balance sheet and income statement might also be included in the handout, so that a

discussion of statement preparation from the transaction record can follow.

INSTRUCTOR’S MANUAL

3-10

Module 2

LO 5

disciplines. He was good friends with Leonardo da Vinci.

Although Luca Pacioli did not invent double-entry bookkeeping, his treatise was the first known

published work on that topic. Around 1494, he published, Summa de Arithmetica, Geometria,

Proportioni et Proportionalita. The Summa’s 36 short chapters on bookkeeping, entitled De

Computis et Scripturis (Of Reckonings and Writings) were added “in order that the subjects of

Some students use the “DEAD” mnemonic to remember the rules of debits and credits: Debits

increase Expenses, Assets, and Dividends.

Emphasize the definitions of debit and credit. Debit is the left side of the account, and credit is the

right side. Some instructors make a game out of it by having the whole class raise their left hands

when a debit account is mentioned and their right hands when a credit account is mentioned.

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

Module 3

LO 6

Complete the in-class example begun previously by distributing a pro forma journal and preparing

the entries for Problem 3-2A in general journal form.

Stress to students that the proper order is to prepare the journal entry and then to post to the T

account. Many students want to go directly from analyzing a transaction to posting it to the T

account.

What type of errors would a trial balance not detect?

INSTRUCTOR’S MANUAL

3-12

Projects and Activities

Module 1

LO 3

Analyzing the Effects of Transactions on the Accounting Equation

In-class discussion: What accounts will our business need?

The transition from seeing accounts listed in the text to choosing accounts to use in a real business is not

always obvious. An interesting and informative exercise involves inventing a small business, and asking

students to suggest a list of accounts (chart of accounts) that the business will need as it begins operations.

Use very simple examples like a lemonade stand, a babysitting service, or newspaper delivery.

Solution

Encourage students to think about what it is that a business has to “keep track of.” A lemonade stand, for

Module 2

LO 4

Accounts

In-class exercise: Chart of Accounts

Have the students choose a business and develop a chart of accounts for the business. Then ask them to

assign a number to each account.

Solution

The solution will vary based on the business students choose. Stress that some accounts are common to all

Module 2

LO 4

The General Ledger

In-class exercise: Glengarry Health Club income statement

Examine the income statement (EXHIBIT 3-3) for Glengarry Health Club in your textbook. All the

accounts listed are summarized from the journal entries prepared by the company during the month of

January 2016. You have learned that accounting is a “double–entry” system: for every debit there is a

corresponding amount of credit. What is the normal balance of each account you see on the income

statement, a debit or a credit? Which account(s) do you think the company credited (debited) when they

debited (credited) each of the income statement accounts? In other words, to which account(s) was the

other half of the entry made?

Solution

The numbers do not matter for this exercise, only the accounts themselves:

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

3-13

Outside assignment: Subsidiary ledgers

Subsidiary ledgers are also discussed in Chapter 7. The inclusion of this assignment in Chapter 3 helps

students see how companies manage large amounts of information.

Examine the balance sheet for ABC Computers, Inc. (a fictitious company), shown below. List the accounts

you believe have a subsidiary ledger to back them up. For each item you name, explain why the account

requires a subsidiary ledger, and what information would be given for each entry in this subsidiary ledger.

Assets Current assets:

Cash $ 4,743

Marketable securities 774

Accounts receivable, net 3,976

Inventories 1,423

Other current assets 1,416

Total current assets 12,332

Property and equipment, net 2,698

Investments 3,144

Other 475

Total Assets $18,649

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable $ 7,075

Accrued and other 2,698

Total current liabilities 9,773

Long-term debt 1,784

Deferred revenue on warranty contracts 878

Total liabilities 12,435

Stockholders’ equity:

Common stock 2,496

Retained earnings 3,718

Total stockholders’ equity 6,214

Total Liabilities and Stockholders’ Equity $18,649

Solution

Marketable securities: A list containing the cost and purchase date of each investment purchased, and a

similar record for each one sold.

INSTRUCTOR’S MANUAL

3-14

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

Module 2

LO 5

The Rules of Debit and Credit

In-class exercise: Another debit/credit chart

Debit and credit rules slow many students down. Another way to approach learning the rules is to make up

a handout chart with the general rules, leaving space for students to fill in examples of specific accounts

Type of account Normal

balance Increase by Decrease by

ASSETS debit (DR) debit (DR) credit (CR)

INSTRUCTOR’S MANUAL

3-16

Comment

Students use this chart in a number of ways. Some add more lines and list every account they encounter,

until the rules of debit and credit are second nature to them. Others use it only to remind themselves of

Module 2

LO 5

Debits and Credits

In-class discussion: Understanding the terms debit and credit

Students are often confused about debits and credits because they tend to think of debits as bad and credits

as good. This misconception may arise from their dealings with bank accounts and debit cards. If a debit

increases an asset, why does the teller at the bank tell you that she will “credit your account” when you

deposit money? What entry will the bank make when you deposit money? Similarly, when you purchase

something with your debit card, why does your account at the bank get debited? What journal entry does

the bank make now?

Solution

The answer, of course, is that the bank looks at the amount of money you have in the bank as a liability. On

Module 3

LO 6

The Format of a Journal Entry

In-class discussion: Special journals

Companies use “special journals” for repetitive transactions that always debit (or credit) the same account.

Which transactions can you think of that fall into this category? What general journal entry do you make to

record each transaction? How would you design a special journal for these that would cut down on the

amount of writing required to record them? Do you think it would be significantly different on a

computerized system? Explain.

Solution

This exercise gives students another opportunity to design an accounting system as they would do, for

CHAPTER 3 PROCESSING ACCOUNTING INFORMATION

3-17

Module 3

LO 6

The Journal and the Ledger

In-class discussion: The need for journals and ledgers

An accounting system requires the use of both journals and ledgers. It is important that students understand

the difference between the two.

What is a journal?

What is a ledger?

Is the same information in both the journal and the ledger? If it is, then why do we need both? Doesn’t this

just make more work for the accountants?

If you wanted to see both the debit and credit side of an entry where would you look?

If you wanted to see the balance of an account, where would you look?

In a computerized accounting system, does a company still need a journal and a ledger?

Solution

A journal is a chronological record of a company’s transactions. Since transactions are first recorded in the

journal, it is sometimes called the book of original entry.

Module 3

LO 7

The Trial Balance

In-class discussion: Does the trial balance have to be perfect?

Does a trial balance have to balance perfectly? What if you prepare a trial balance with totals in the

hundreds of thousands of dollars, and the two columns differ by a dollar? Can you say, as we often do in

everyday life for a situation like this, “close enough!” and go on from there? Discuss the pros and cons of

this decision. What would you do if you were responsible for preparing statements? Are there any ethical

considerations involved here?

Solution

The trial balance does have to balance perfectly. Accountants hesitate to “write off” a minor imbalance

because they’ve seen instances where a small imbalance masks a big problem. For example, two