CHAPTER 3

Adjusting the Accounts

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Explain the accrual basis of

accounting and the

reasons for adjusting

entries.

1, 2, 3, 4, 5, 6,

7, 8, 18

1, 2, 8

1

1, 2, 3, 4, 6,

10, 11

12, 13, 18, 19,

20, 23

10, 11, 12, 13,

4A, 5A, 6A

5A, 6A

*6. Discuss financial reporting

23, 24, 25, 26,

27, 28

12, 13, 14, 15

18, 19, 20, 21,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare adjusting entries, post to ledger accounts,

and prepare an adjusted trial balance.

Simple

40–50

2A

Prepare adjusting entries, post, and prepare adjusted

trial balance, and financial statements.

Simple

50–60

Prepare adjusting entries and financial statements.

Prepare adjusting entries.

cycle to preparation of financial statements.

Prepare adjusting entries, adjusted trial balance,

and financial statements using appendix.

40–50

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 3

ADJUSTING THE ACCOUNTS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

4–6

BE2

1–3

AN

Moderate

6–8

BE3

2

AN

Simple

3–5

BE4

2

AN

Simple

3–5

DI1

1

K

Simple

2–4

DI2

2

AN

Simple

6–8

DI3

3

AN

Simple

4–6

DI4

4

AN

Moderate

20–30

EX1

1

C

Simple

3–5

EX2

1

E

Moderate

10–15

EX3

1

AP

Simple

6–8

EX4

1–3

AN

Simple

5–6

EX5

2, 3

AN

Moderate

10–15

EX6

1–3

AN

Moderate

10–12

EX7

2, 3

AN

Moderate

8–10

EX8

2, 3

AN

Moderate

8–10

EX9

2, 3

AN

Simple

8–10

EX10

1–4

AN

Moderate

8–10

EX11

1–4

AN

Moderate

12–15

EX12

2–4

AN

Moderate

8–10

EX13

2–4

AN

Simple

8–10

BE5

2

AN

Simple

2–4

BE6

2

AN

Simple

2–4

BE7

3

AN

Simple

4–6

BE8

1–3

AN

Simple

5–7

BE9

4

AP

Simple

4–6

BE10

4

AP

Simple

2–4

BE11*

5

Moderate

3–5

BE12*

6

C

Simple

3–5

BE13*

6

C

Simple

2–4

BE14*

6

C

Simple

2–4

BE15*

6

C

Simple

1–2

ADJUSTING THE ACCOUNTS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX15

2, 3

AN, S

Moderate

8–10

EX16*

5

AN

Moderate

6–8

EX17*

5

AN

Moderate

10–12

EX18*

6

C

Simple

3–5

EX19*

6

C

Simple

3–5

EX20*

6

C

Simple

6–8

EX21*

6

Simple

EX22*

6

AN

Simple

10–20

P1A

AN

Simple

40–50

P2A

2–4

P3A

AN

Moderate

40–50

P4A

AN

Moderate

30–40

P5A

2–4

Moderate

P6A

AN

Moderate

40–50

AN

Simple

10–15

Simple

AN

Simple

10–15

AN

Simple

10–15

Moderate

S

Moderate

15–20

C

Simple

10–15

1–4

E

Moderate

E

Moderate

10–15

BYP10

E

Moderate

10–15

BYP11

K

Simple

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Explain the accrual basis of accounting and

the reasons for adjusting entries.

DI3-1

Q3-1

Q3-2

Q3-3

Q3-4

Q3-6

Q3-7

Q3-8

BE3-1

E3-1

Q3-5

E3-3

Q3–18

BE3-2

BE3-8

E3-4

E3-6

E3–10

E3–11

*2. Prepare adjusting entries for deferrals.

Q3-8

Q3-9

Q3–10

Q3–11

Q3–12

Q3–13

Q3–19

Q3–20

Q3–18

BE3-2

BE3-3

BE3-4

BE3-5

BE3-6

BE3-8

DI3-2

E3-5

E3-6

E3-7

E3-8

E3-9

E3–10

E3–11

E3–12

E3–13

E3–15

P3–1A

P3–2A

P3–3A

P3–4A

P3–5A

P3–6A

E3–15

Q3–21

E3–14

E3–10

E3–11

E3–12

E3–13

P3–2A

P3–3A

P3–5A

P3–6A

E3–16

P3–6A

E3-18 Q3–27

Broadening Your Perspective

Communication

ANSWERS TO QUESTIONS

4. Information presented on an accrual basis is more useful than on a cash basis because it reveals

Questions Chapter 3 (Continued)

*17. The entry is:

**23. (a) The primary objective of financial reporting is to provide financial information that is useful to

Questions Chapter 3 (Continued)

*25. Comparability results when different companies use the same accounting principles.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 3-1

payable.

BRIEF EXERCISE 3-2

Item

(a)

Type of Adjustment

(b)

Account Balances before Adjustment

Prepaid Expenses

Assets Overstated

Expenses Understated

Revenues Understated

Accrued Expenses

Expenses Understated

Liabilities Understated

Unearned Revenues

Liabilities Overstated

Revenues Understated

12/31 Bal. 2,500

BRIEF EXERCISE 3-3

BRIEF EXERCISE 3-4

BRIEF EXERCISE 3-5

BRIEF EXERCISE 3-6

BRIEF EXERCISE 3-7

BRIEF EXERCISE 3-8

Account

(a)

Type of Adjustment

(b)

Related Account

BRIEF EXERCISE 3-9

PARSONS COMPANY

Income Statement

For the Year Ended December 31, 2017

BRIEF EXERCISE 3-10

PARSONS COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2017

*BRIEF EXERCISE 3-11

BRIEF EXERCISE 3-12

BRIEF EXERCISE 3-13

BRIEF EXERCISE 3-14

BRIEF EXERCISE 3-15

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 3-1

DO IT! 3-2

DO IT! 3-3

DO IT! 3-4

(b) Total assets and liabilities are computed as follows:

SOLUTIONS TO EXERCISES

EXERCISE 3-1

EXERCISE 3-2

(a) Accrual-basis accounting records the transactions that change a

EXERCISE 3-2 (Continued)

(c) Dear Senator,

EXERCISE 3-3

EXERCISE 3-4

EXERCISE 3-5

EXERCISE 3-6

Item

(a)

Type of Adjustment

(b)

Accounts before Adjustment

EXERCISE 3-7

Revenues Understated

Expenses Understated

Liabilities Understated

Revenues Understated

Liabilities Understated

EXERCISE 3-8

EXERCISE 3-9

EXERCISE 3-9 (Continued)

EXERCISE 3-10

GOPITKUMAR CO.

Income Statement

For the Month Ended July 31, 2017

EXERCISE 3-11

Answer Computation

EXERCISE 3-11 (Continued)

EXERCISE 3-12

EXERCISE 3-13

EXERCISE 3-14

FRINZI COMPANY

Income Statement

For the Year Ended August 31, 2017

EXERCISE 3-14 (Continued)

FRINZI COMPANY

Retained Earnings Statement

For the Year Ended August 31, 2017

EXERCISE 3-15

*EXERCISE 3-16

*EXERCISE 3-17

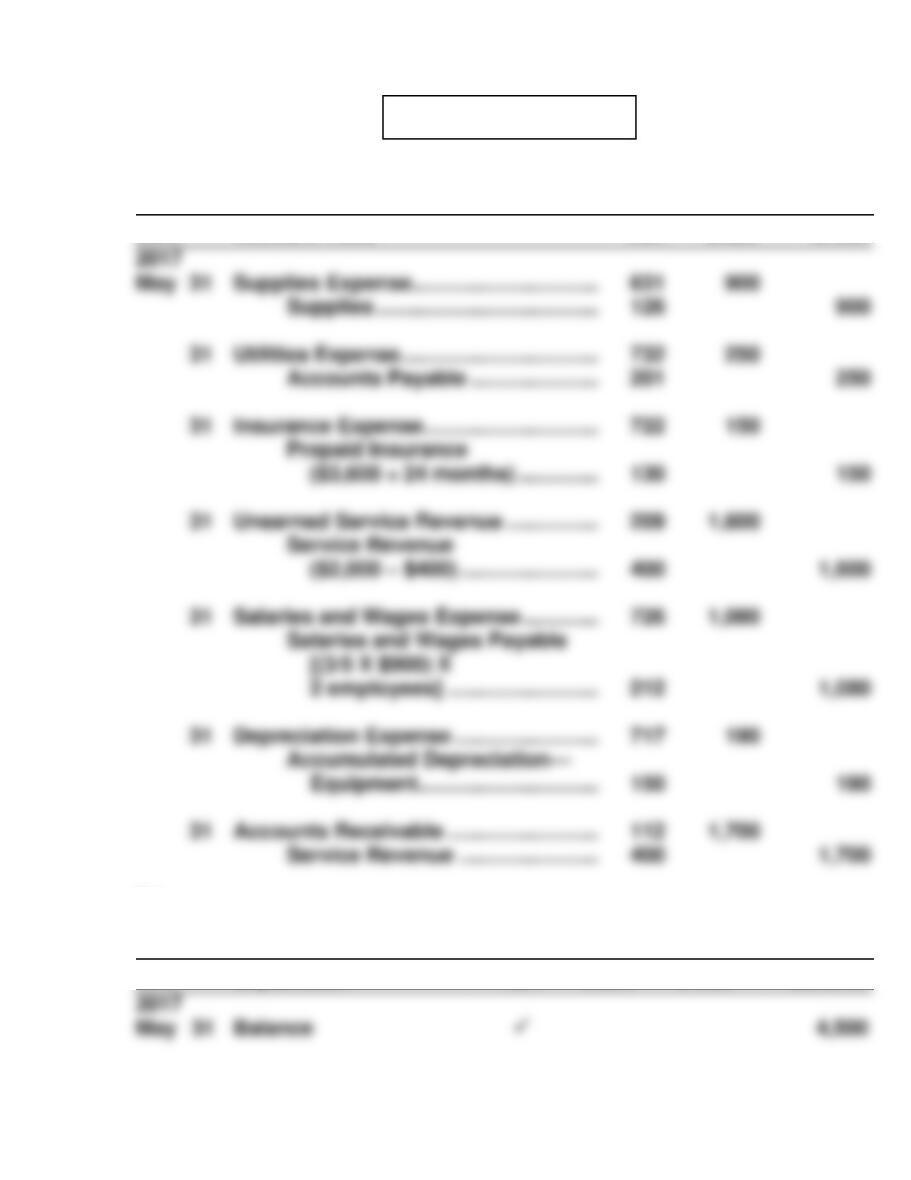

(b) Jan. 31 Prepaid Insurance ($160 X 11 months) …… 1,760

Insurance Expense ………………………… 1,760

*EXERCISE 3-18

*EXERCISE 3-19

(a) This is a violation of the historical cost principle. The inventory was

*EXERCISE 3-20

*EXERCISE 3-21

(a) The primary objective of financial reporting is to provide financial

*EXERCISE 3-22

(a) Accounting information is the compilation and presentation of

SOLUTIONS TO PROBLEMS

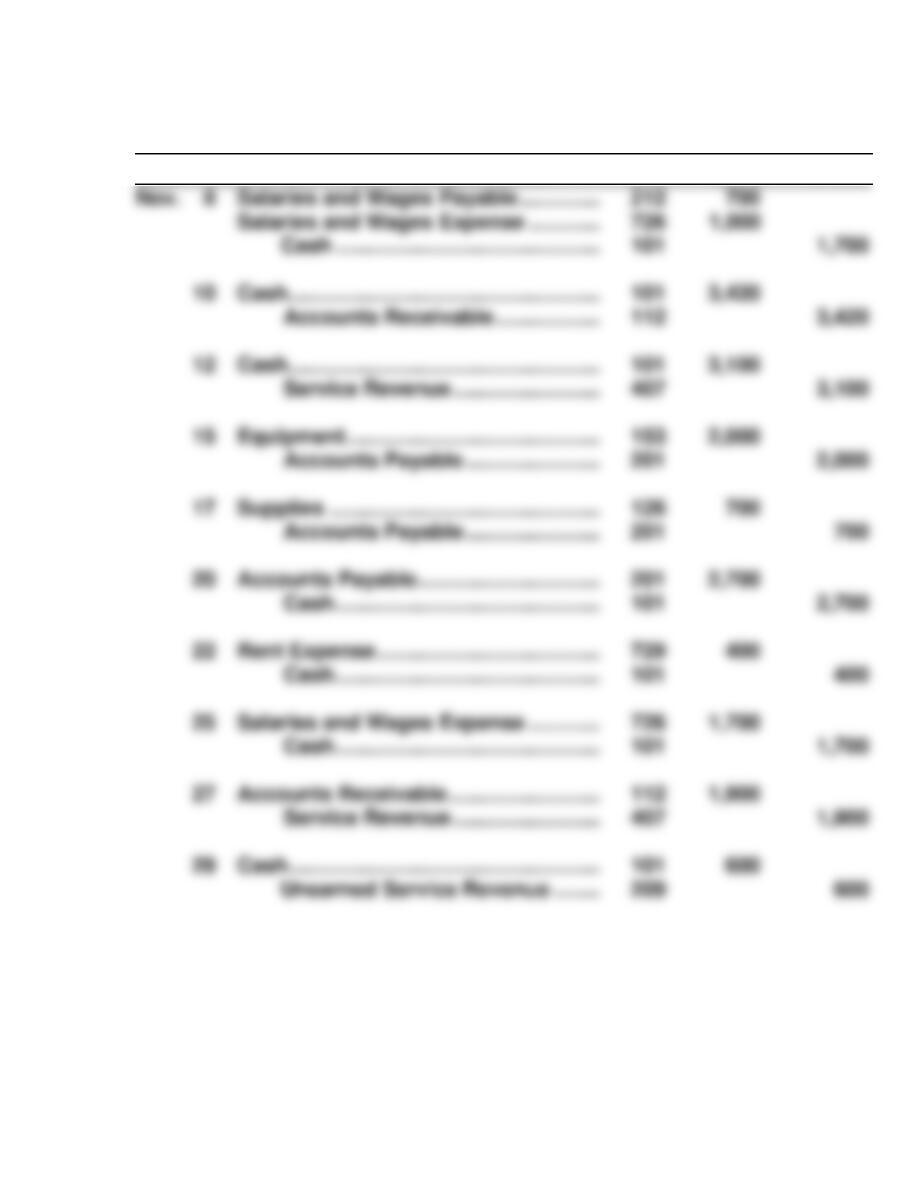

PROBLEM 3-1A

(a) J4

Date

Account Titles

Ref.

Debit

Credit

(b)

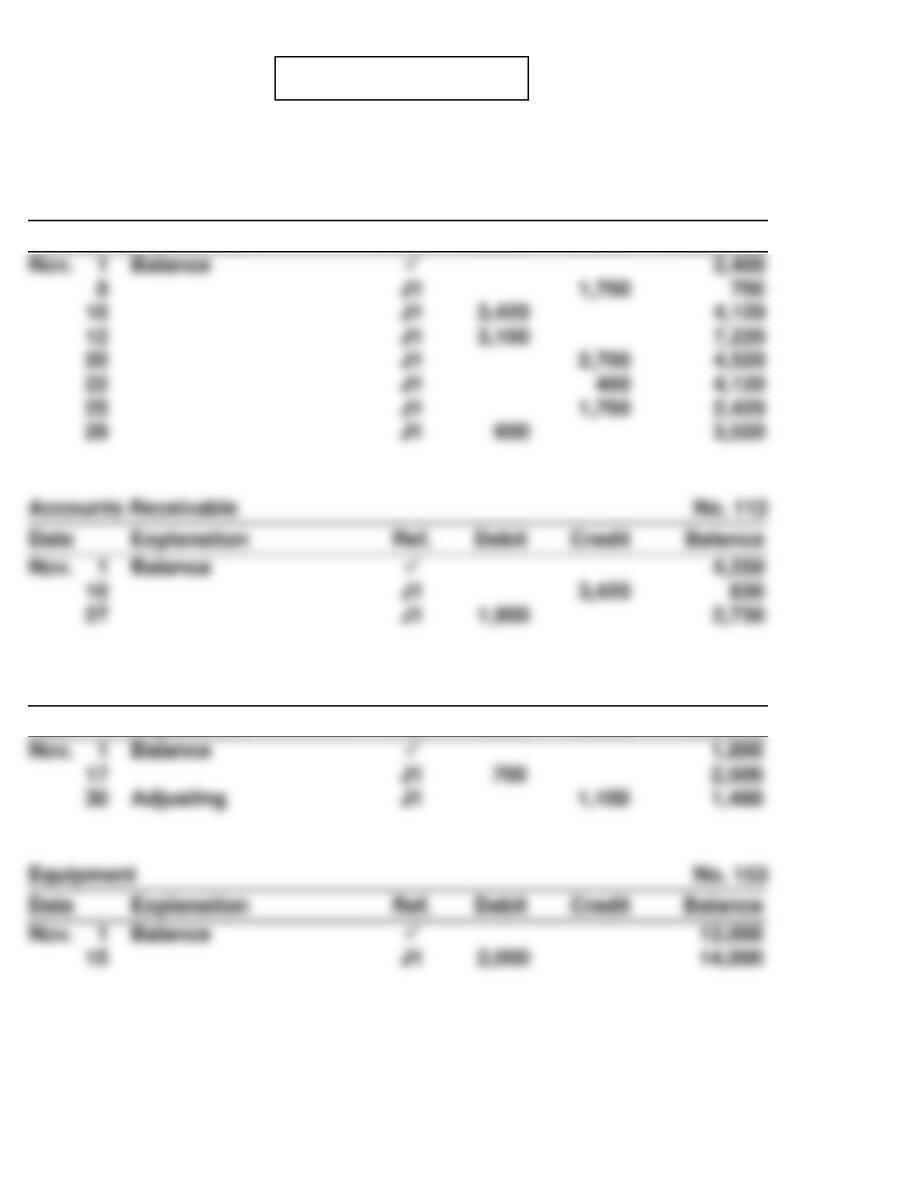

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 3-1A (Continued)

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

Prepaid Insurance No. 130

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 3-1A (Continued)

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Common Stock No. 311

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Date

Explanation

Ref.

Debit

Credit

Balance

Depreciation Expense No. 717

Rent Expense No. 729

PROBLEM 3-1A (Continued)

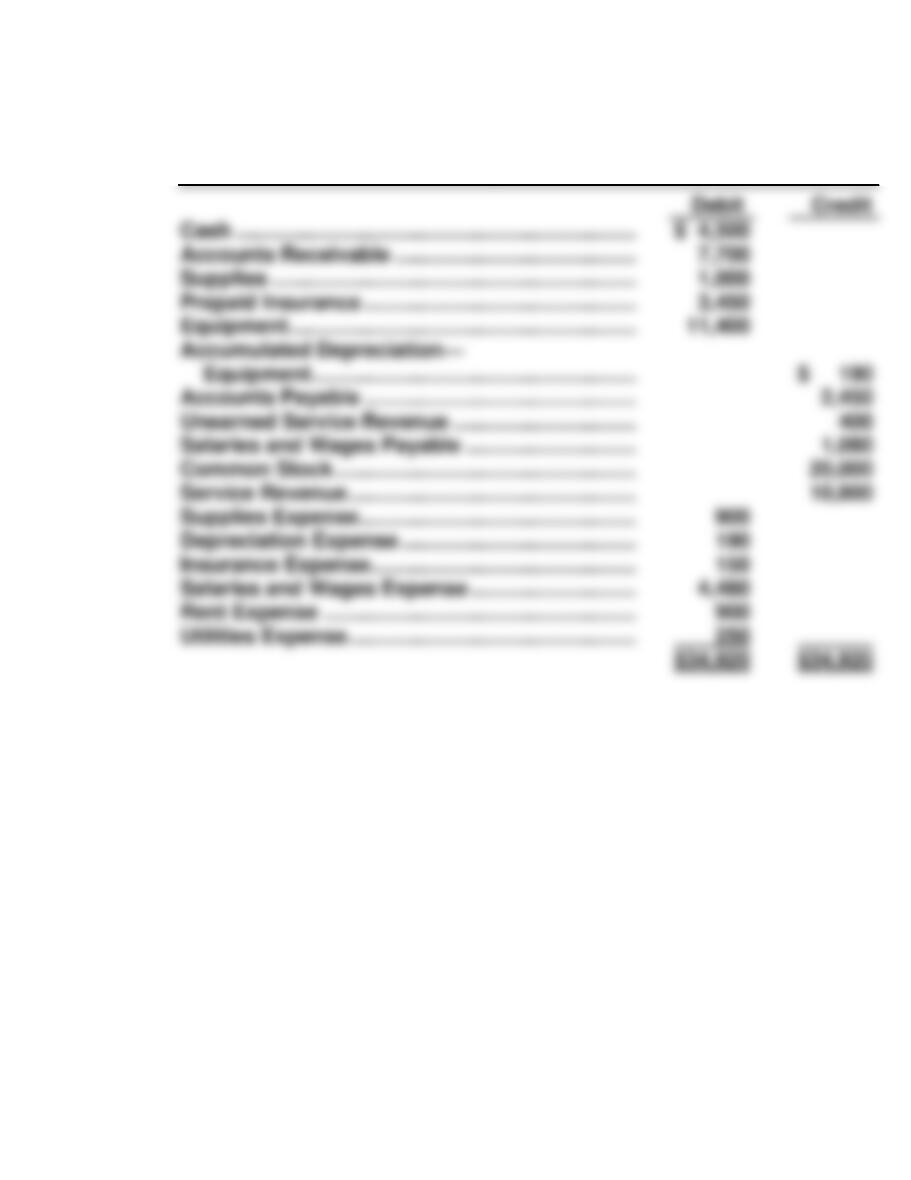

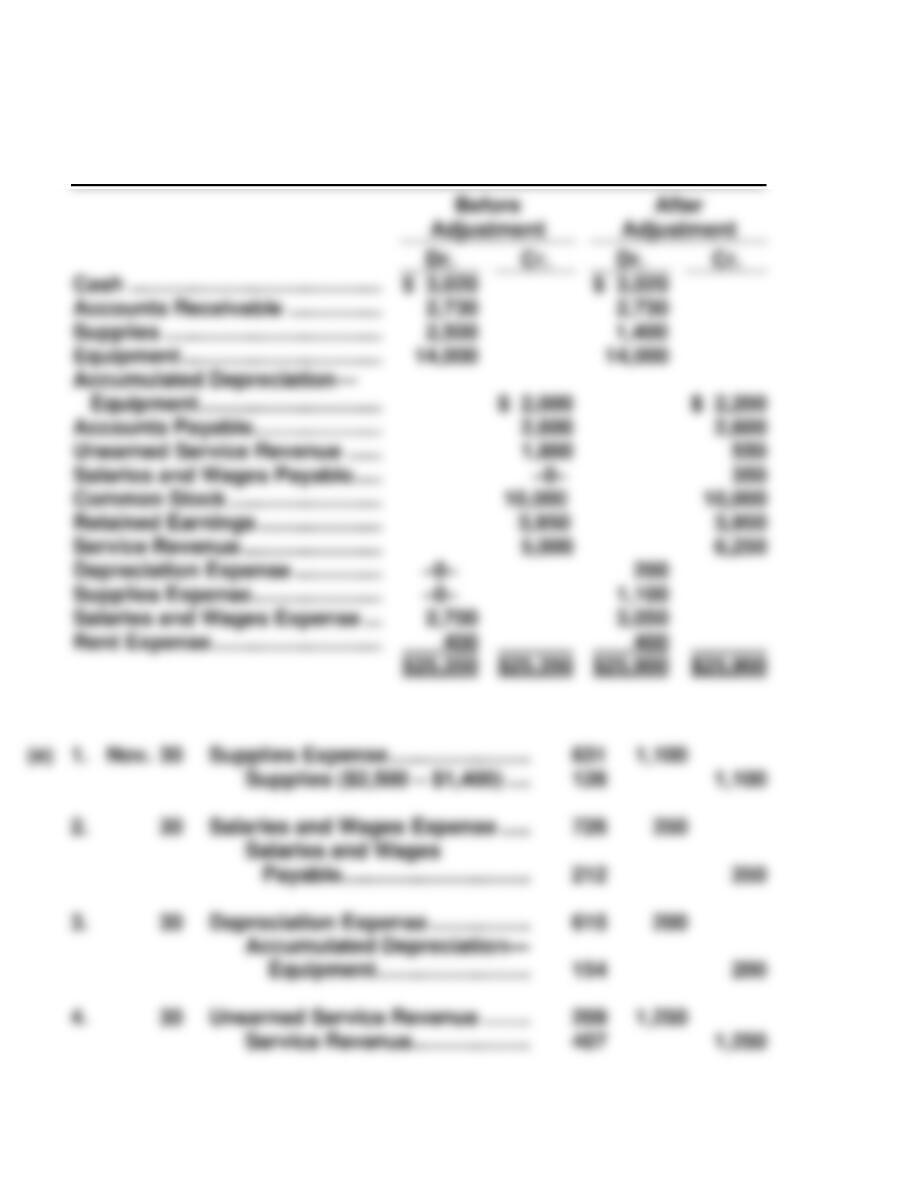

(c) NARDELLI CONSULTING

Adjusted Trial Balance

May 31, 2017

PROBLEM 3-2A

(a) J1

Date

Account Titles

Ref.

Debit

Credit

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 3-2A (Continued)

Supplies No. 126

Accumulated Depreciation—Buildings No. 142

PROBLEM 3-2A (Continued)

Accounts Payable No. 201

Interest Payable No. 230

PROBLEM 3-2A (Continued)

Advertising Expense No. 610

Insurance Expense No. 722

PROBLEM 3-2A (Continued)

(c) SKYLINE MOTEL

Adjusted Trial Balance

May 31, 2017

PROBLEM 3-2A (Continued)

(d) SKYLINE MOTEL

Income Statement

For the Month Ended May 31, 2017

SKYLINE MOTEL

Retained Earnings Statement

For the Month Ended May 31, 2017

PROBLEM 3-2A (Continued)

SKYLINE MOTEL

Balance Sheet

May 31, 2017

PROBLEM 3-3A

(b) EVERETT CO.

Income Statement

For the Quarter Ended September 30, 2017

PROBLEM 3-3A (Continued)

EVERETT CO.

Retained Earnings Statement

For the Quarter Ended September 30, 2017

EVERETT CO.

Balance Sheet

September 30, 2017

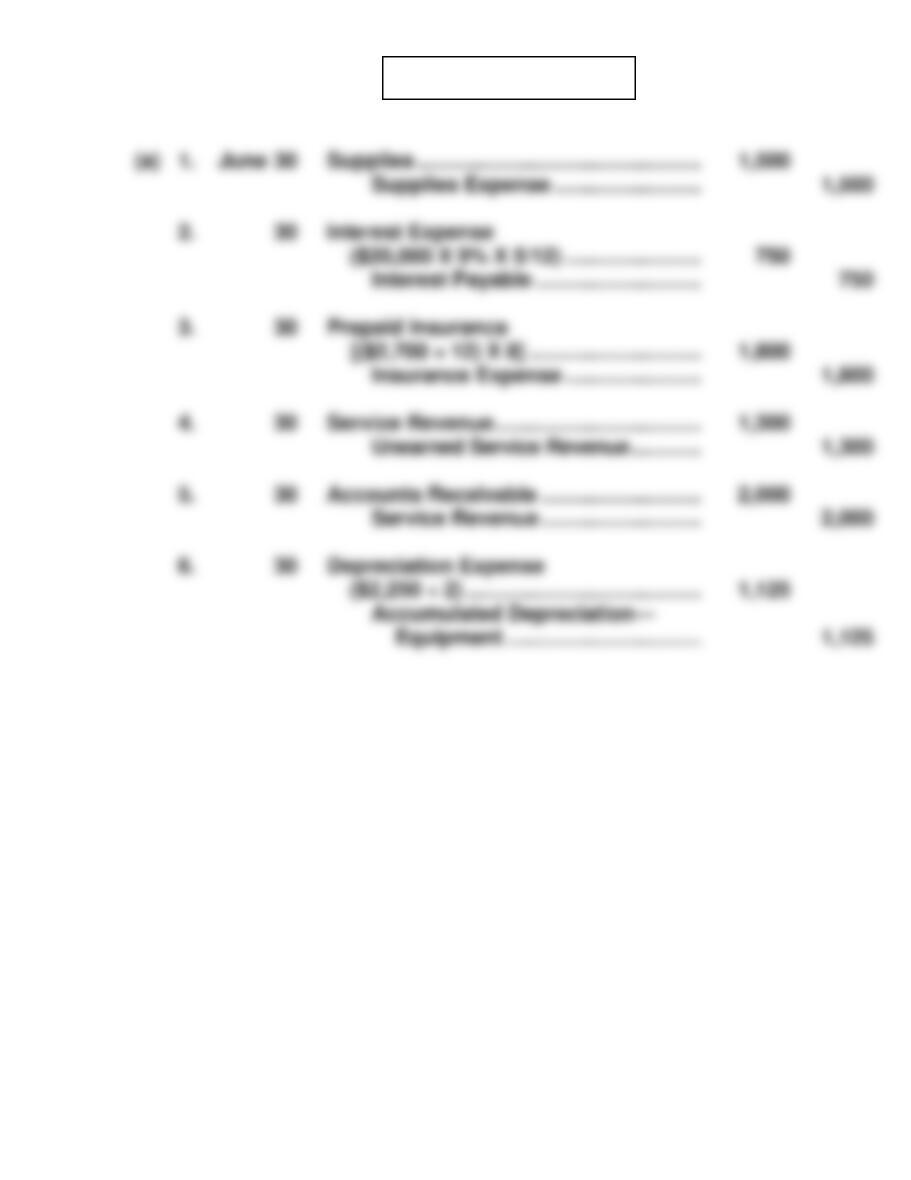

PROBLEM 3-4A

PROBLEM 3-5A

(a), (c) & (e)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

Supplies No. 126

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

PROBLEM 3-5A (Continued)

Accumulated Depreciation—Equipment No. 154

Unearned Service Revenue No. 209

PROBLEM 3-5A (Continued)

Service Revenue No. 407

Date

Explanation

Ref.

Debit

Credit

Balance

Salaries and Wages Expense No. 726

Date

Explanation

Ref.

Debit

Credit

Date

Explanation

Ref.

Debit

Credit

Date

Explanation

Ref.

Debit

Credit

PROBLEM 3-5A (Continued)

(b) General Journal

J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

PROBLEM 3-5A (Continued)

(d) & (f) SCHILLING EQUIPMENT REPAIR

Trial Balances

November 30, 2017

PROBLEM 3-5A (Continued)

(g) SCHILLING EQUIPMENT REPAIR

Income Statement

For the Month Ended November 30, 2017

SCHILLING EQUIPMENT REPAIR

Retained Earnings Statement

For the Month Ended November 30, 2017

PROBLEM 3-5A (Continued)

SCHILLING EQUIPMENT REPAIR

Balance Sheet

November 30, 2017

*PROBLEM 3-6A

*PROBLEM 3-6A (Continued)

(b) SOMMER GRAPHICS COMPANY

Adjusted Trial Balance

June 30, 2017

*PROBLEM 3-6A (Continued)

(c) SOMMER GRAPHICS COMPANY

Income Statement

For the Six Months Ended June 30, 2017

SOMMER GRAPHICS COMPANY

Retained Earnings Statement

For the Six Months Ended June 30, 2017

*PROBLEM 3-6A (Continued)

SOMMER GRAPHICS COMPANY

Balance Sheet

June 30, 2017

BYP 3-1 FINANCIAL REPORTING PROBLEM

(a) Items that may result in adjusting entries for prepayments are:

BYP 3-2 COMPARATIVE ANALYSIS PROBLEM

BYP 3-3 COMPARATIVE ANALYSIS PROBLEM

1.

2. Cash flow from operations is the difference between cash receipts

BYP 3-4 REAL–WORLD FOCUS

BYP 3-5 REAL-WORLD FOCUS

(a) Many large companies, big accounting firms, and accounting standard

(d) Condorsement (a word invented by the SEC) represents a

BYP 3-6 DECISION MAKING ACROSS THE ORGANIZATION

(a) HAPPY CAMPER PARK

Income Statement

For the Quarter Ended March 31, 2017

(b) The generally accepted accounting principles pertaining to the income

BYP 3-7 COMMUNICATION ACTIVITY

Dear Ms. Hall:

Adjusting entries are needed because the trial balance may not contain an

up–to-date and complete record of transactions and events for the

following reasons:

There are four types of adjusting entries:

BYP 3-7 (Continued)

Signature

BYP 3-8 ETHICS CASE

(a) The stakeholders in this situation are:

(b) 1. It is unethical for the president to place pressure on Melissa to

BYP 3-9 ALL ABOUT YOU

We address the issue of contingent liabilities in greater detail in Chapter

10. Our primary interest in this exercise is to engage students in a

discussion regarding the general nature of the financial statement

elements (assets, liabilities, equity, revenues and expenses).

BYP 3-10 CONSIDERING PEOPLE, PLANET, AND PROFIT

The balance sheet should provide a fair representation of what a company

BYP 3-11 FASB CODIFICATION ACTIVITY

(a) Revenue earned by an entity from its direct distribution, exploitation,

IFRS 3-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Note 3.7 indicates that revenue is measured as the fair value of