CASE 3

Kering SA: Probing the Performance Gap with LVMH

TEACHING NOTE

■ SYNOPSIS ■

Strategy is about creating the conditions for the success of an organization: for business enterprises this means

profitability. Hence, diagnosis of a firm’s financial performance is an essential foundation for evaluating and

developing its strategy.

■ TEACHING OBJECTIVES ■

The purpose of the case is to give students practice and develop their expertise in diagnosing company

performance as a tool of strategic analysis. As a result of studying and discussing this case, students

will be better equipped to:

Use a company’s financial statements to evaluate its financial performance

probing of financial data is a core component of performance diagnosis.

■ POSITION IN THE COURSE ■

I like to devote at least one session early in my strategy course to performance analysis—partly to reinforce the

message that strategy is not simply about “looking at the big picture”—it is also about the detailed probing of

financial data in order to diagnose a company’s current and recent performance in order to establish a

foundation both for evaluating the current strategy and providing a basis for strategy recommendations.

■ ASSIGNMENT QUESTIONS ■

1. How well is Kering performing relative to LVMH?

■ READING ■

R. M. Grant, Contemporary Strategy Analysis (9th edn.), Wiley, 2016, Chapter 2, especially the section on

“Putting Performance Analysis into Practice” (pages. 43 to 51).

■ CASE DISCUSSION AND ANALYSIS ■

How well is Kering performing relative to LVMH

To assess a company’s financial performance, we need some benchmarks. These can be:

1. Comparisons over time, i.e. comparing current performance with previous performance

companies that make up the S&P500, the FTSE 100, or the CAC40)

In the case of Kering (1) is difficult: the transformation in Kering’s business means that comparisons over time

are not very meaningful, especially given the costs on transition in terms of “non–recurring net expenses” and

“net income from discontinued operations” (which comprised losses of about € 1.5 billion during 2012 to

2014).

In terms of (2) absolute benchmarks: Kering’s performance has been far from outstanding:

In terms of (3), compared to its close competitor LVMH, Kering’s performance was markedly inferior:

Kering

LVMH

Revenue growth 2011-14

24.5%

29.5%

Operating margin 2012-14*

15.6%

19.4%

14.9%

18.0%

ROA 2012-14**

11.0%

Identifying the sources of Kering’s inferior performance

Focusing upon the comparison between Kering and LVMH allows for a detailed exploration of the sources of

Kering’s modest profit performance.

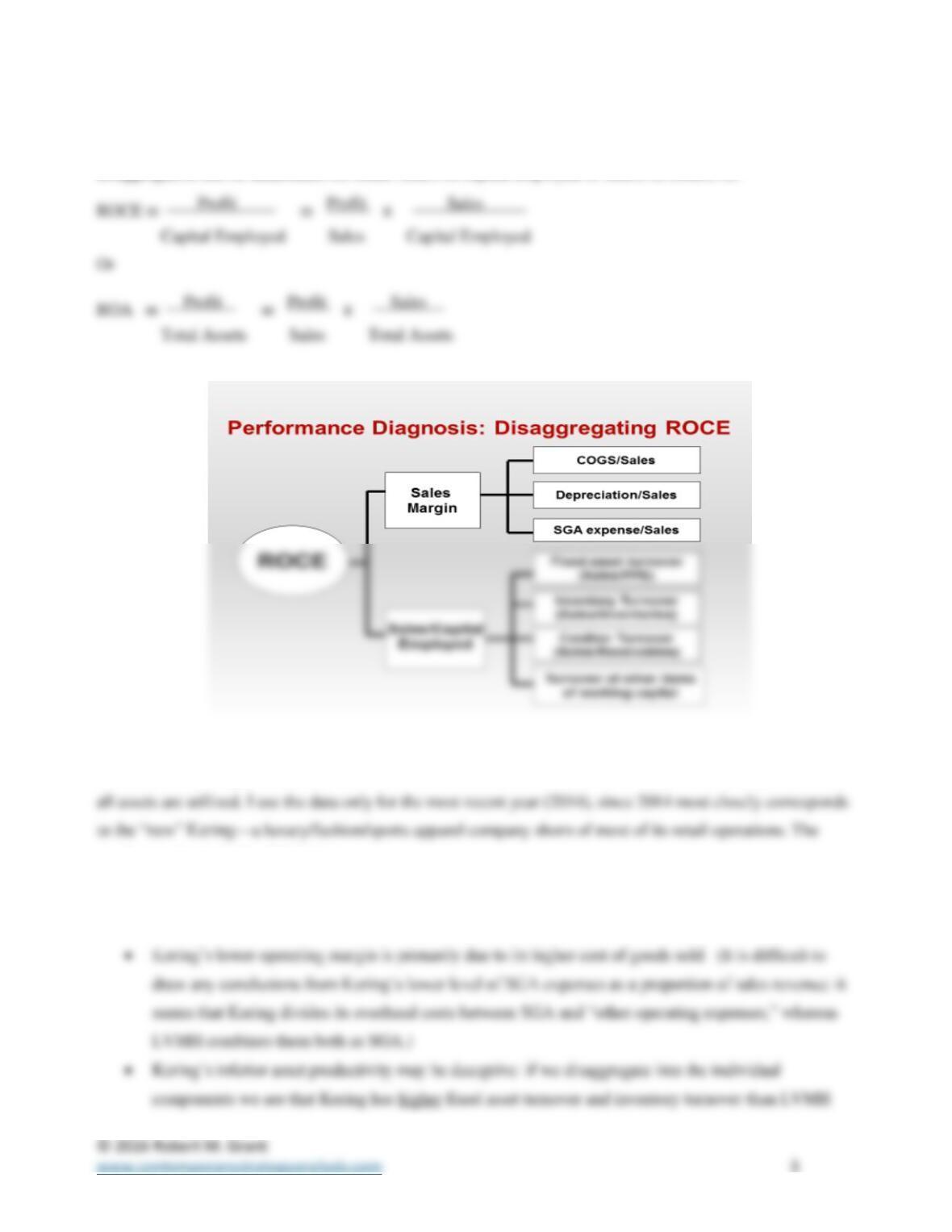

We follow the ratio disaggregation procedure outlined in Figure 2.1 (shown in the slide below). This

disaggregation can be undertaken for either return on capital employed or return on assets, i.e.

In the case of Kering, I use ROA rather an ROCE because this allows us to consider the efficiency with which

results are shown in the slide below.

The main observations are:

Kering’s inferior ROA reflects both a lower operating margin and lower rate of asset turnover.

(although its turnover of receivables and cash are lower). The reason for Kering’s lower turnover of

total assets can be attributed to the fact that it has proportionately higher levels of intangibles—

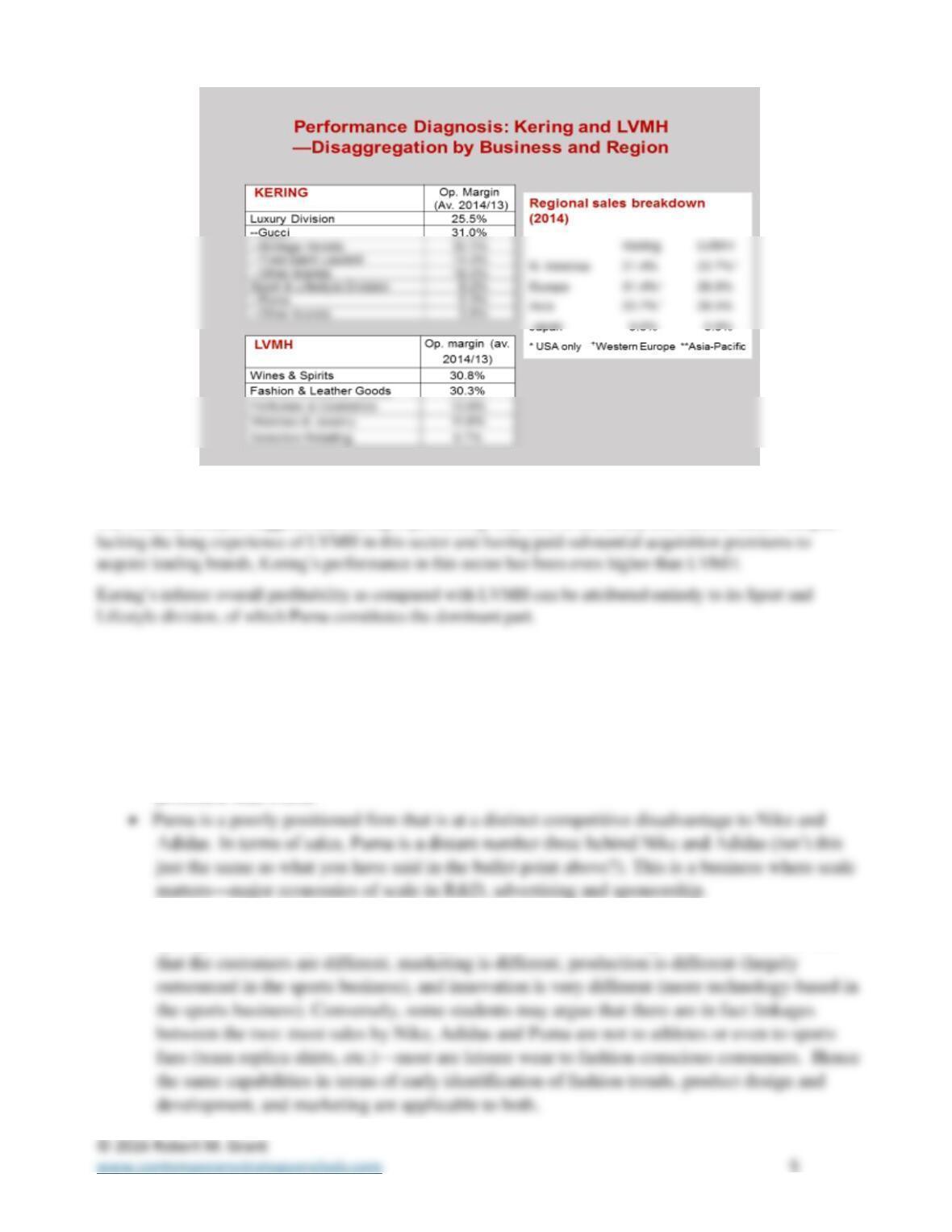

To delve deeper, we need to disaggregate Kering’s performance in a different way: by business sector and by

geographic region.

Disaggregation by business. Kering has two divisions: Luxury and Sport and Lifestyle. The

breakdown of revenues and profits for these two reveals distinctly different performance, with

Luxury having almost five times the operating margin of Sport and Lifestyle.

What can Kering’s management do?

The financial analysis suggests that Kering is performing very well in the luxury and fashion sector. Despite

Here, making recommendations for Sport and Lifestyle is fraught with difficulty. A key issue is: Why is Puma

performing so poorly? Here we need to go beyond the financial information in the case and explore some

features of this business sector. Possible explanations include:

Sports apparel, footwear, and equipment is a low-profit industry. The case provides little

information on this business, but it is likely that margins are generally lower than those earned

in the fashion and luxury sector. It seems likely that Nike and Adidas are much more

profitable than Puma.

The sports business is strategically very different from fashion and luxury—there are few

synergies; essentially Puma is a strategic misfit. The lack of strategic fit arises from the fact

This last issue is especially relevant to whether Kering keeps or divests Puma. Resolving this issue would

■ KEY TAKE-AWAYS FROM THE CASE DISCUSSION ■