Unitron Corporation

Teaching Commentary

OVERVIEW

This is an excellent short case to introduce the managerial accounting issues related to the “joint cost” problem. Classic

microeconomics argues unequivocally that attempts to assign cost to individual products in a “joint” set constitute a

complete waste of time—”just maximize the total revenue over the batch.” Like the comparable adage to “price so that

marginal cost equals marginal revenue,” the economists’ advice about joint costing is certainly accurate, given the

TEACHING STRATEGY

We teach the case in one (ninety minute) class period early in the required managerial accounting course. Questions 1

through 5 will easily fill one class period with useful discussion. We push hard to cover these questions in about

seventy-five minutes so that we can also spend some time on Question 6. This last question raises strategic positioning

ANSWERS TO ASSIGNMENT QUESTIONS

Question 1

The idea here is to construct a “Produced As/Sold As Matrix” (400,000 400,000). Obviously, the possible

combinations are endless, so how does one choose a “best” approach? The “best” solution is to start with demand for the

highest value product (405) and work back unsold production to the next lowest value product (404) to fill sales demand

and so forth until 401 sales demand is filled (see Exhibit A).

The idea is to minimize potential revenue loss. In a static sense [$246,000 Revenue], any tableau is as good as

34-2

Question 2

There are two basic accounting methods for

allocating joint cost to the five joint products: the

The physical units method is straightforward:

joint cost of $200,000 divided by 400,000 total units

produced = $0.50 per unit. All rectifiers are assigned

identical unit costs. Since sales prices increase with

increasing technical attributes across the five categories,

gross margins will also increase from the low to high end

products (negative 25% for 401 to 50% for 405).

If the “by–product” units (400s) are considered a

joint product, the average cost is $.40 per unit ($200,000

÷ 500,000 units).

The RSV method has a number of twists that can

result in many different unit costs for the five products.

For inventory costing purposes, any systematic cost

Here are the resulting unit cost numbers:

Unit Costs

401 402 403 404 405

Physical units method $0.50 $0.50 $0.50 $0.50 $0.50

Question 3

Costing Method

Relative

Physical Unit Sales Value

Gross Margin $(600) Method A: $(30)

Method B: $456

A problem arises under RSV costing when there

is product switching (402s sold as 401s). Now, there is a

choice:

2. In order to achieve the desired result (gross margin of

$456), it is necessary to consider all 6,000 of the

items shipped to be 401s. This means violating the

costing rule. Use a 401 cost, not a 402 cost, for the

402s shipped as 401s.

year anyway, the issue really is one of manufacturing

scheduling! Is it time to produce another batch, or not?

What level of inventory triggers the production decision?

Since we average one new batch every 2 1/2 weeks

The toy company may be forcing Unitron to

change its long-term view on joint products and by–

products. The “seconds” are already large to be

about this time with “Speak and Spell.”

At the even lower selling price of $.15 per unit,

the Toy Company’s 48,000 “seconds” will generate

$7,200 incremental revenue and gross profit. Based on

RSV, 401s generate only $7,480 gross profit annually.

Even the high-tech 404s and 405s combined generate only

Assume 83,000 units sold

at $.15/unit, sales value = $12,450 (35,000+48,000)

Total joint products sales

revenue=$246,000+12,450 = $258,450

If I sell them now for $.15, will I lose an

opportunity to sell them later for enough more than $.15

to make up for the time value of the foregone cash

inflow?

Annual output is 100,000 units and inventory on

hand is 65,000. This is thirteen batches, or thirty-two+

Question 5

There is no simple answer to the “proper”

allocation method. The impact may be purely behavioral.

4,500 units of 401 (greater than a batch’s yield) we will

not likely have a sufficient quantity on hand and will ship

some 402 units.

If Unitron’s strategy is to push high-end items,

with the low end as just fillers, and if the high-end items

are harder to sell, then average costing better matches the

Behavioral Implications?

The Average Cost System shows low-end items (401) as

hard. Planned-for substitutions are also equally profitable

so they are encouraged. The sales view is always sell

downward one level if necessary. It is up to production

scheduling to replenish the inventory at the right time.

Which set of likely behavioral consequences is

preferable for Unitron?

34-4

Question 6

At the simplest level, selling an additional

100,000 404’s involves producing thirty-four additional

batches (3,000 404s per batch)—a highly unlikely

Obviously, the more extra batches we are

required to produce for this order, the less attractive it

looks. The fewer extra batches, the better it looks. We

can use the matrix tableau from Question 1 to

40,000 unit demand for 403s now being met with 404s.

Twelve more batches yields the 60,000 extra 404s and

405s, and 54,000 more 403s as well. This is more than

enough 403s to replace the 40,000 404s that would now

batches still costs us almost $80,000 extra ($6,400 x 12 =

$76,800). But can we get the production requirement

down even further?

18 Months (30 Batches) Extra Output*

Sales DOD Needs Prod. Shortfall Per Eight more Units

(All Amounts in Thousands) Batch Batches Excess

34-5

The allowed profit margin on defense work

varies between 8% and 10%. Assuming a $.75

discounted price with a 10% allowed margin, we can

estimate what the cost report to the government would

have to look like:

Total revenue of $75,000 and allowable profit of

$7,500 means total cost cannot exceed $67,500:

Assuming a 9% charge for all nonmanufacturing

costs was “reasonable,” this “cost plus” bid proposal

would probably survive the government audit review.

Since Unitron spends far more than 9% of sales on total

nonmanufacturing costs, it would be easy to justify the

9% allocation as reasonable.

A Closer Look

As Exhibit B to this note shows, it is possible to

meet the extra demand with only five extra batches if we

extend the horizon over a 2 ¼-year time frame. This

means extra production cost of only $32,000 (on a

variable cost basis) and $50,000 (at full cost). At a

$75,000 bid, with the DOD cost report as shown above,

this is $25,000 extra profit (full-cost basis) with no excess

Question 6 is very rich, as this commentary

reveals. We like to spend at least fifteen minutes of class

time here to demonstrate the following:

1. Careful analysis can make the problem look much

different (need for thirty-four extra batches versus

only five extra).

34-6

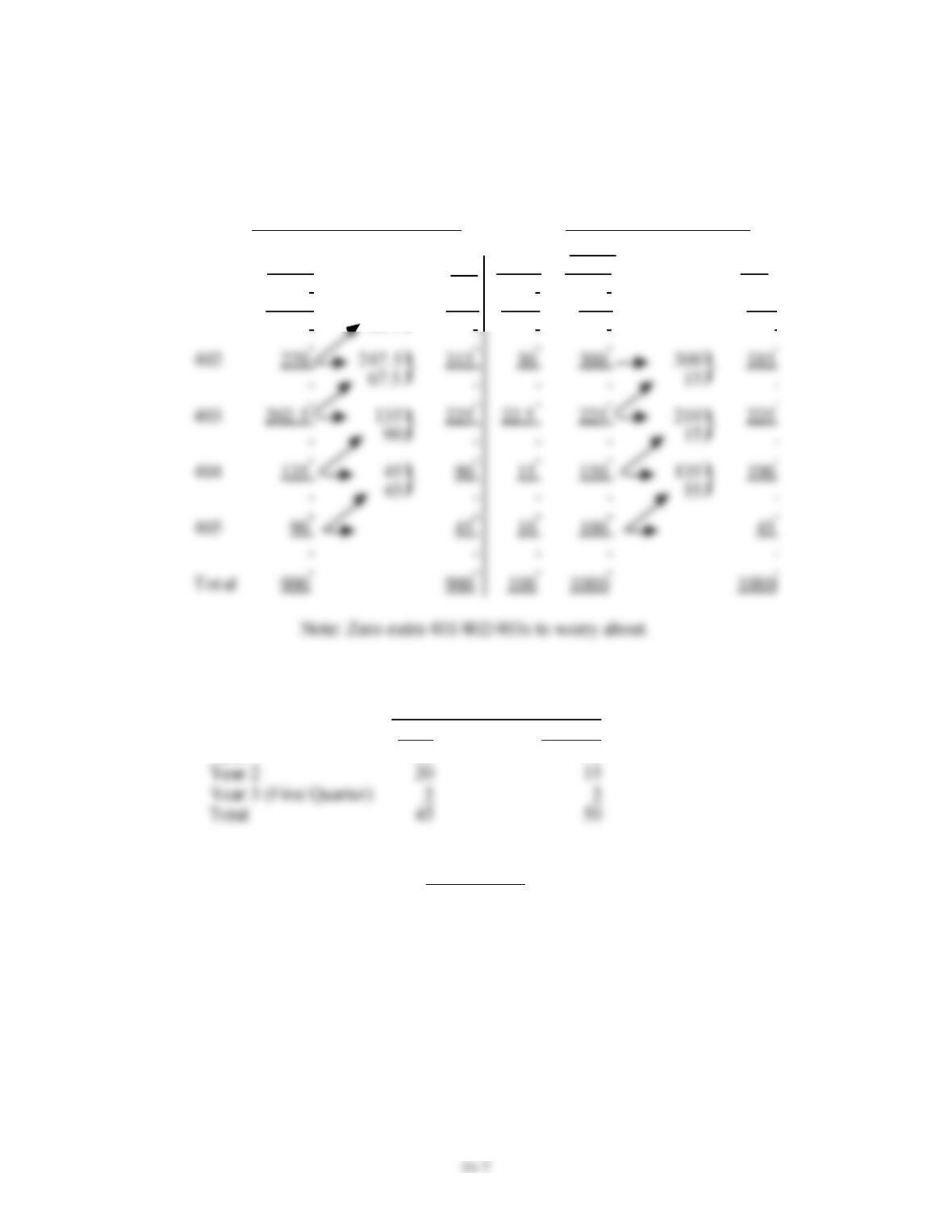

Exhibit A

Produced As/Sold As Matrix

Sold As

401 402 403 404 405 Total

401 90,000 90,000

Work from the highest value products backward to the lowest value products.

• Note that sales demand and estimated production quantities do not match for individual products.

Exhibit B

(Thousands of Units)

Now-2 1/4 Years

(forty-five Batches) Make five Extra Batches

401

Prod.

202.5

202.5

22.5

225

Ext ra

22.5

Tot al

Prod.

225

225

}

Sell Sell

Batches

Now Revised

Year 1 20 30

Strategic Fit?