Chapter 23

Flexible Budgets and Standard Cost Systems

Review Questions

1. What is a variance?

2. Explain the difference between a favorable and an unfavorable variance.

A variance is favorable if it increases operating income. For example, if actual revenue is greater

3. What is a static budget performance report?

A static budget is a budget prepared for only one level of sales volume. A static budget performance

(static budget variances).

4. How do flexible budgets differ from static budgets?

A flexible budget is a budget prepared for various levels of sales volume within a relevant range. A

5. How is a flexible budget used?

Because a flexible budget is prepared for various levels of sales volume within a relevant range, it

6. What are the two components of the static budget variance? How are they calculated?

The overall static budget variance is the difference between actual operating income, based on the

7. What is a flexible budget performance report?

A flexible budget performance report compares actual results to the expected results in the flexible

8. What is a standard cost system?

A standard cost system is an accounting system that uses standards for product costs—direct

9. Explain the difference between a cost standard and an efficiency standard. Give an example of each.

Each input (direct materials, direct labor, and manufacturing overhead) that goes into making a

product has both a cost standard and an efficiency standard. A cost standard is the expected cost of

10. Give the general formulas for determining cost and efficiency variances.

The cost variance is the difference in costs (actual cost per unit minus standard cost per unit) of an

11. How does the static budget affect cost and efficiency variances?

A static budget is a budget prepared for only one level of sales volume—the number of units

12. List the direct materials variances, and briefly describe each.

The direct materials variances are the direct materials cost variance and the direct materials

efficiency variance.

13. List the direct labor variances, and briefly describe each.

The direct labor variances are the direct labor cost variance and the direct labor efficiency variance.

The direct labor cost variance measures how well the company keeps direct labor cost per hour

14. List the variable overhead variances, and briefly describe each.

The variable overhead variances are the variable overhead cost variance and the variable overhead

efficiency variance.

15. List the fixed overhead variances, and briefly describe each.

The fixed overhead variances are the fixed overhead cost variance and the fixed overhead volume

variance.

16. How is the fixed overhead volume variance different from the other variances?

The fixed overhead volume variance is not a flexible budget variance (whereas the fixed overhead

17. What is management by exception?

Management by exception is when managers concentrate on results that are outside the accepted

18. List the eight product variances and the manager most likely responsible for each.

Variance

Manager Responsible

Direct materials cost variance

Purchasing

Direct materials efficiency variance

Production

Direct labor cost variance

Human Resources

Direct labor efficiency variance

Production

Variable overhead cost variance

Production

Variable overhead efficiency variance

Production

Fixed overhead cost variance

Production

Fixed overhead volume variance

Production

19. Briefly describe how journal entries differ in a standard cost system.

Journal entries differ in a standard cost system in the following ways:

• Raw Materials Inventory: Actual quantity at standard cost.

20. What is a standard cost income statement?

A standard cost income statement highlights the manufacturing variances for management. It doesn’t

Short Exercises

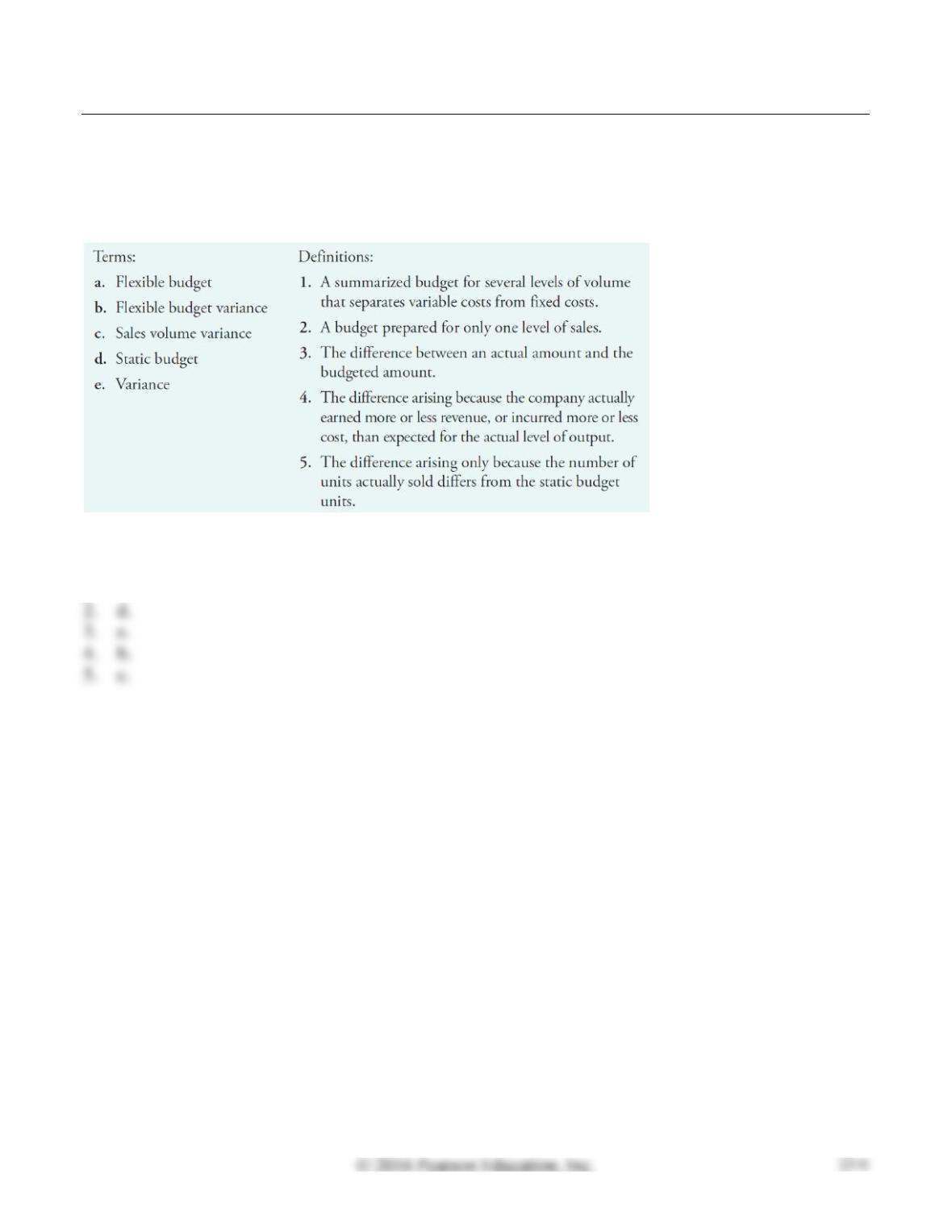

S23-1 Matching terms

Learning Objective 1

Match each term to the correct definition.

SOLUTION

1.

a.

2.

d.

3.

e.

4.

b.

5.

c.

S23-2 Preparing flexible budgets

Learning Objective 1

Major, Inc. manufactures travel locks. The budgeted selling price is $15 per lock, the variable cost is

$10 per lock, and budgeted fixed costs are $12,000 per month. Prepare a flexible budget for output

levels of 3,000 locks and 10,000 locks for the month ended April 30, 2016.

SOLUTION

MAJOR, INC.

Flexible Budget

For the Month Ended April 30, 2016

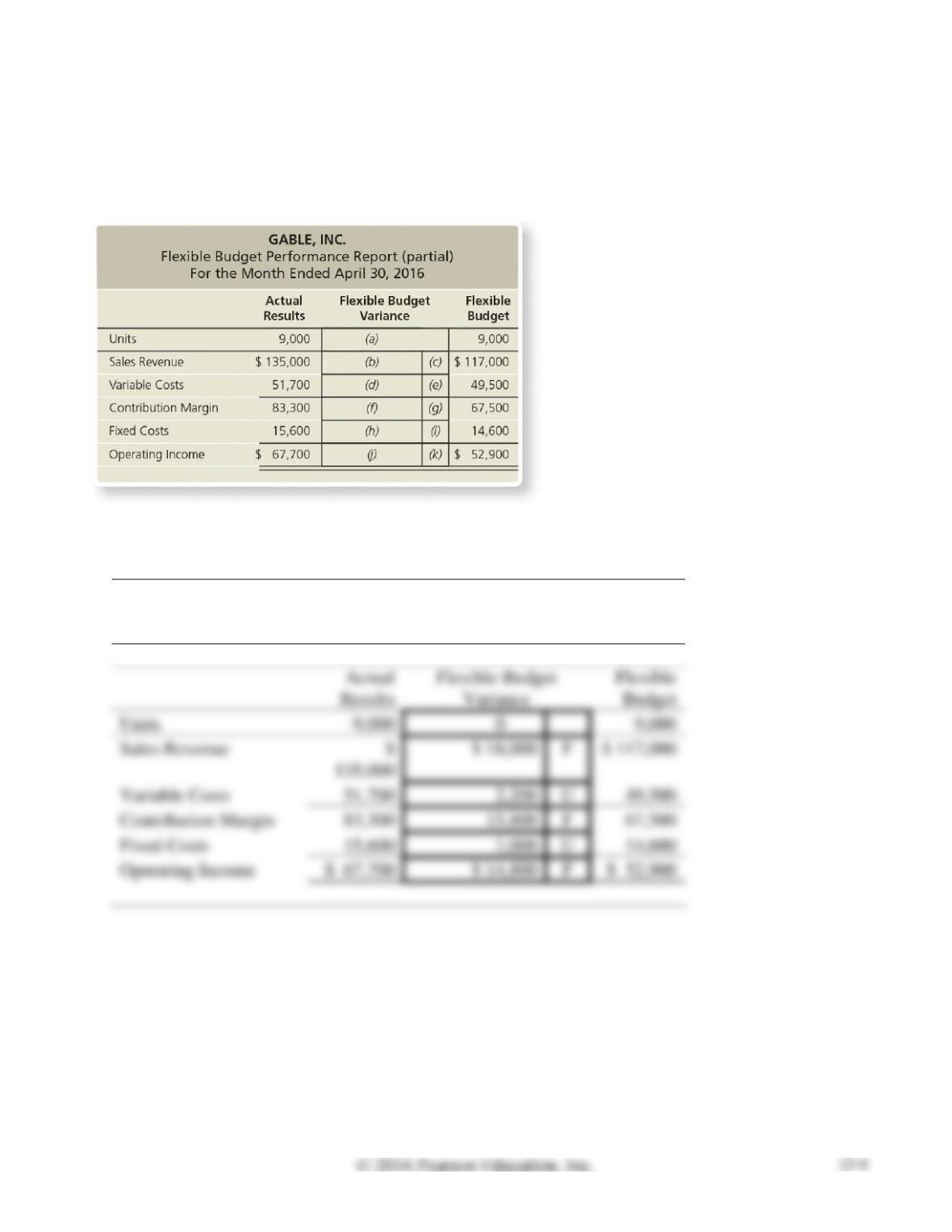

S23-3 Calculating flexible budget variances

Learning Objective 1

Complete the flexible budget variance analysis by filling in the blanks in the partial flexible budget

performance report for 9,000 travel locks for Gable, Inc.

SOLUTION

GABLE, INC.

Flexible Budget Performance Report (partial)

For the Month Ended April 30, 2016

S23-4 Matching terms

Learning Objective 2

Match each term to the correct definition.

SOLUTION

1.

b.

2.

3.

4.

d.

S23-5 Identifying the benefits of standard costs

Learning Objective 2

Setting standards for a product may involve many employees of the company. Identify some of the

employees who may be involved in setting the standard costs, and describe what their role might be in

setting those standards.

SOLUTION

The purchasing manager provides information about purchase costs, discounts, delivery requirements,

and credit policies (for direct materials cost standards).

S23-6 Calculating materials variances

Learning Objective 3

Goldman, Inc. is a manufacturer of lead crystal glasses. The standard direct materials quantity is 0.7

pound per glass at a cost of $0.30 per pound. The actual result for one month’s production of 6,900

glasses was 1.3 pounds per glass, at a cost of $0.40 per pound. Calculate the direct materials cost

variance and the direct materials efficiency variance.

SOLUTION

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($0.40 per pound – $0.30 per pound)

×

=

$897 U

=

(AQ ̶ SQ)

×

=

×

=

$1,242 U

×

6,900 glasses

=

8,970 actual pounds

0.7 pound per glass

×

6,900 glasses

=

4,830 standard pounds

S23-7 Calculating labor variances

Learning Objective 3

Goldman, Inc. manufactures lead crystal glasses. The standard direct labor time is 0.5 hours per glass, at

a cost of $17 per hour. The actual results for one month’s production of 6,900 glasses were 0.2 hours per

glass, at a cost of $11 per hour. Calculate the direct labor cost variance and the direct labor efficiency

variance.

SOLUTION

Direct Labor Cost Variance

=

(AC ̶ SC)

×

AQ

=

($11 per DLHr – $17 per DLHr)

×

1,380 DLHr(a)

=

$8,280 F

=

×

=

×

=

$35,190 F

×

6,900 glasses

=

1,380 actual DLHr

Note: Short Exercises S23-6 and S23-7 must be completed before attempting Short Exercise S23-8.

S23-8 Interpreting material and labor variances

Learning Objective 3

Refer to your results from Short Exercises S23-6 and S23-7.

Requirements

1. For each variance, who in Goldman’s organization is most likely responsible?

2. Interpret the direct materials and direct labor variances for Goldman’s management.

SOLUTION

Requirement 1

Variance

Manager Responsible

Requirement 2

The $897 unfavorable direct materials cost variance calculated in S23-6 indicates that the actual direct

materials cost per pound was not kept within standard. The $0.40 actual cost per pound was greater than

the $0.30 standard cost per pound.

S23-9 Computing standard overhead allocation rates

Learning Objective 4

The following information relates to Smithson, Inc.’s overhead costs for the month:

Smithson allocates manufacturing overhead to production based on standard direct labor hours.

Compute the standard variable overhead allocation rate and the standard fixed overhead allocation rate.

SOLUTION

Standard VOH

allocation rate

=

Budgeted VOH

Budgeted allocation base

=

Budgeted allocation base

=

Note: Short Exercise S23-9 must be completed before attempting Short Exercise S23-10.

S23-10 Computing overhead variances

Learning Objective 4

Refer to the Smithson, Inc. data in Short Exercise S23-9. Last month, Smithson re- ported the following

actual results: actual variable overhead, $10,400; actual fixed overhead, $2,750; actual production of

5,000 units at 0.30 direct labor hours per unit. The standard direct labor time is 0.25 direct labor hours

per unit (1,200 static direct labor hours / 4,800 static units).

Requirements

1. Compute the overhead variances for the month: variable overhead cost variance, variable overhead

efficiency variance, fixed overhead cost variance, and fixed overhead volume variance.

2. Explain why the variances are favorable or unfavorable.

SOLUTION

Requirement 1

VOH Cost Variance

=

Actual VOH

−

(SC × AQ)

=

$10,400

−

($7.00 per DLHr(a) × 1,500 DLHr(b))

=

$100 F

=

×

=

$1,750 U

=

$850 F

=

$150 F

Calculated in S23-9

5,000 units produced × 0.3 direct labor hours per unit = 1,500 DLHr

5,000 units produced × 0.25 direct labor hours per unit = 1,250 DLHr

S23-10 (continued)

Requirement 2

The $100 favorable variable overhead cost variance indicates that actual variable overhead cost per

direct labor hour was kept within standard. The $6.93(a) actual cost per direct labor hour was less than

the $7.00 standard cost per direct labor hour (the standard variable overhead allocation rate per direct

labor hour).

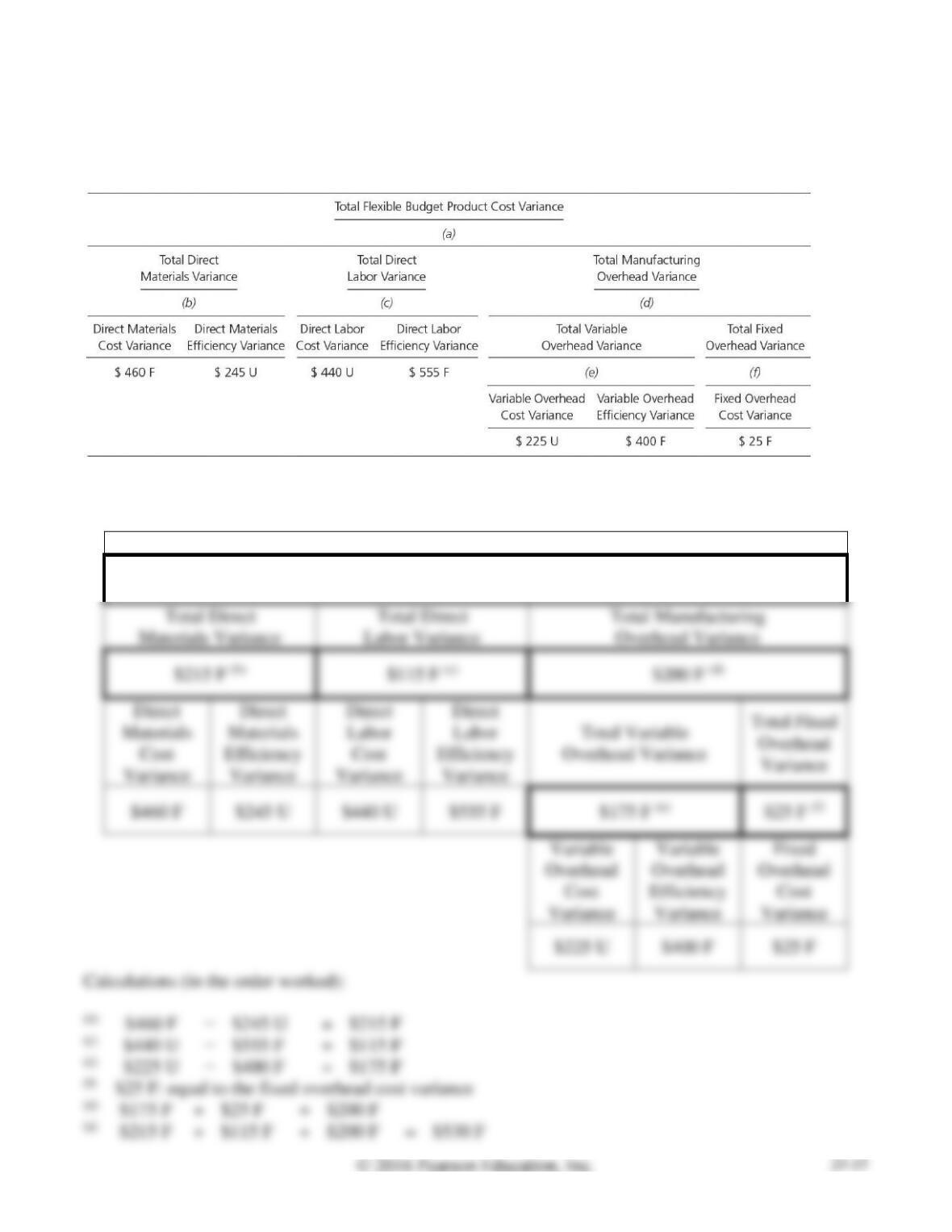

S23-11 Understanding variance relationships

Learning Objective 5

Complete the table below for the missing variances.

SOLUTION

Total Flexible Budget Product Cost Variance

$530 F (a)

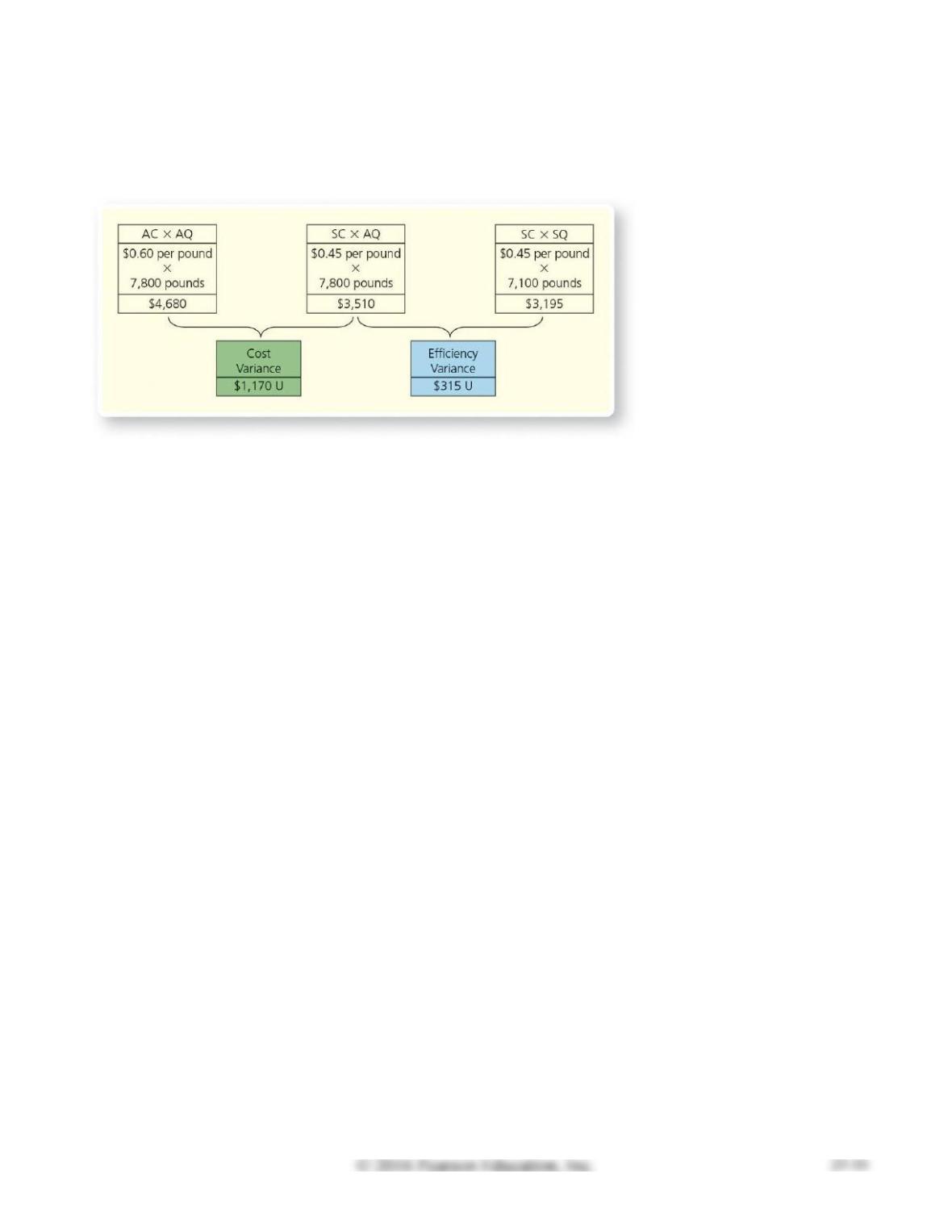

S23-12 Journalizing materials entries

Learning Objective 6

The following direct materials variance analysis was performed for Jackson.

Requirements

1. Record Jackson’s direct materials journal entries. Assume purchases were made on account.

2. Explain what management will do with this variance information.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Raw Materials Inventory

3,510

Direct Materials Cost Variance

1,170

4,680

3,195

Direct Materials Efficiency Variance

3,510

Requirement 2

It is not enough for Jackson’s management to know that a variance occurred. They must know why it

occurred. Each of the direct materials variances will be investigated and information will be obtained

from the managers responsible for each. (The purchasing manager is responsible for the direct materials

cost variance, and the production manager is responsible for the direct materials efficiency variance).

S23-13 Journalizing labor entries

Learning Objective 6

The following direct labor variance analysis was performed for Logan.

Requirements

1. Record Logan’s direct labor journal entry (use Wages Payable).

2. Explain what management will do with this variance information.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Work-in-Process Inventory

20,800

Direct Labor Efficiency Variance

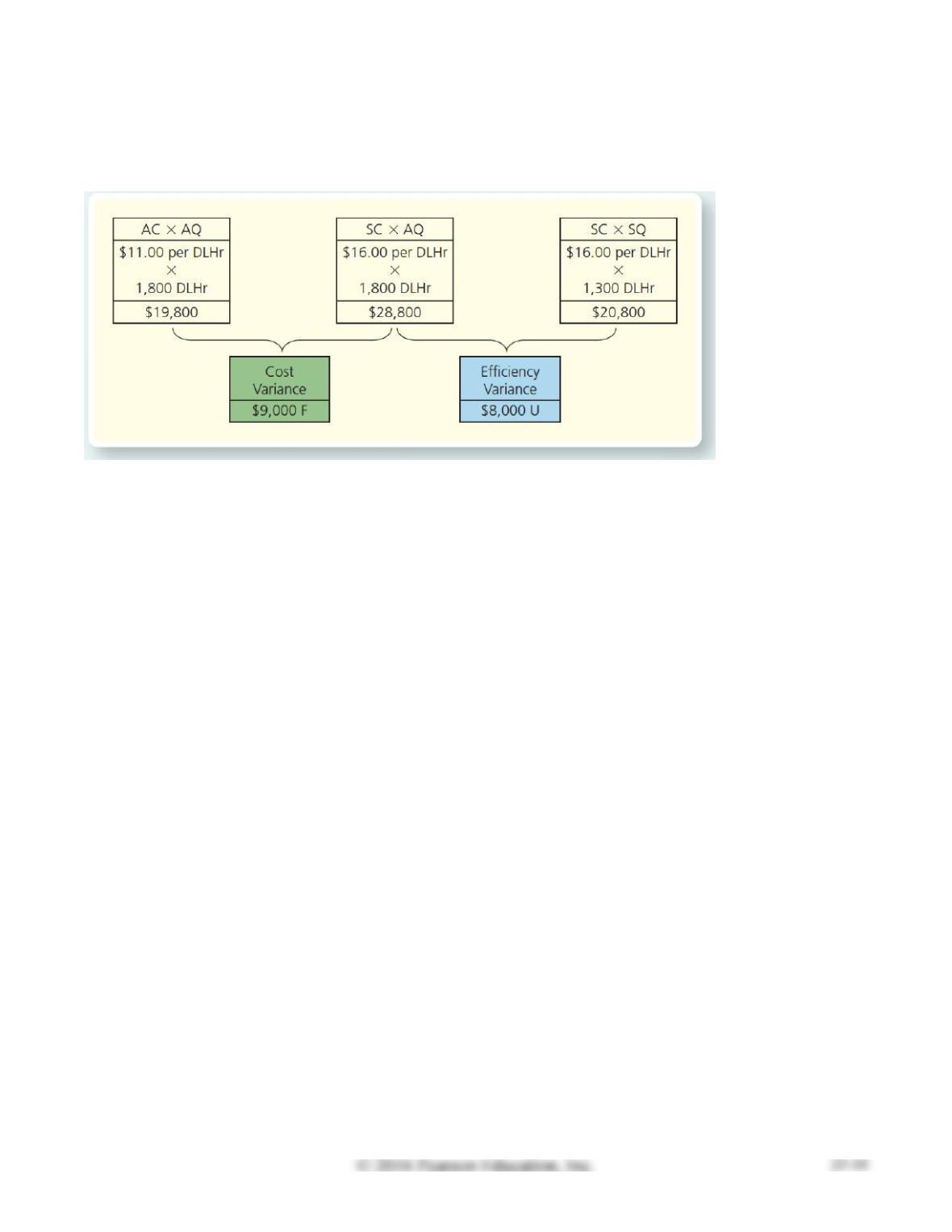

Direct Labor Cost Variance

Wages Payable

19,800

Requirement 2

It is not enough for Logan’s management to know that a variance occurred. They must know why it

occurred. Each of the direct labor variances will be investigated and information will be obtained from

the managers responsible for each (the human resources manager is responsible for the direct labor cost

variance and the production manager is responsible for the direct labor efficiency variance).

S23-14 Preparing a standard cost income statement

Learning Objective 6

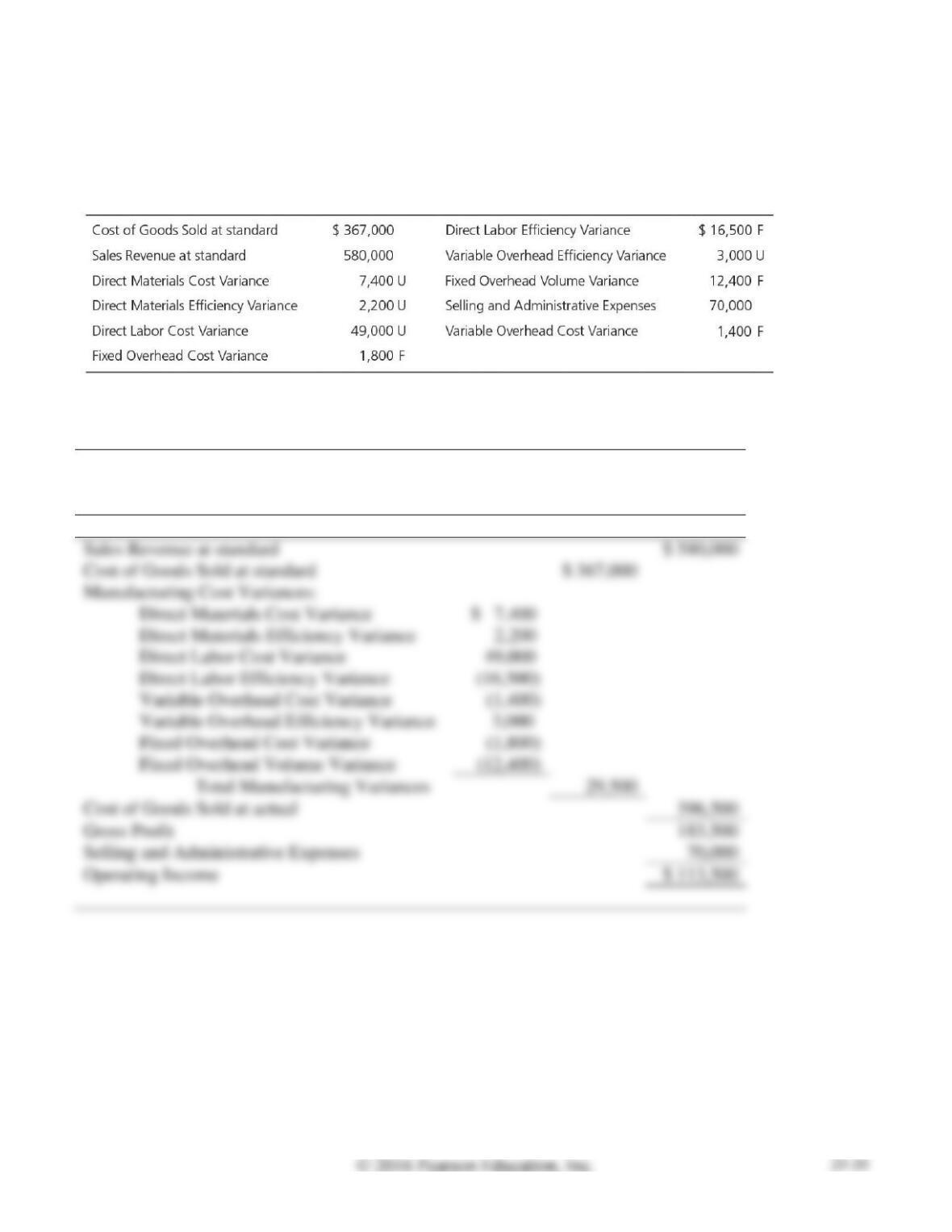

Use the following information to prepare a standard cost income statement for Watson

Company for 2016.

SOLUTION

WATSON COMPANY

Standard Cost Income Statement

For the Year Ended December 31, 2016

Sales Revenue at standard

Cost of Goods Sold at standard

Cost of Goods Sold at actual

Gross Profit

Selling and Administrative Expenses

Operating Income