Exercises

E23-15 Preparing a flexible budget

Learning Objective 1

$203,500 Op. Inc. for 55,000 units

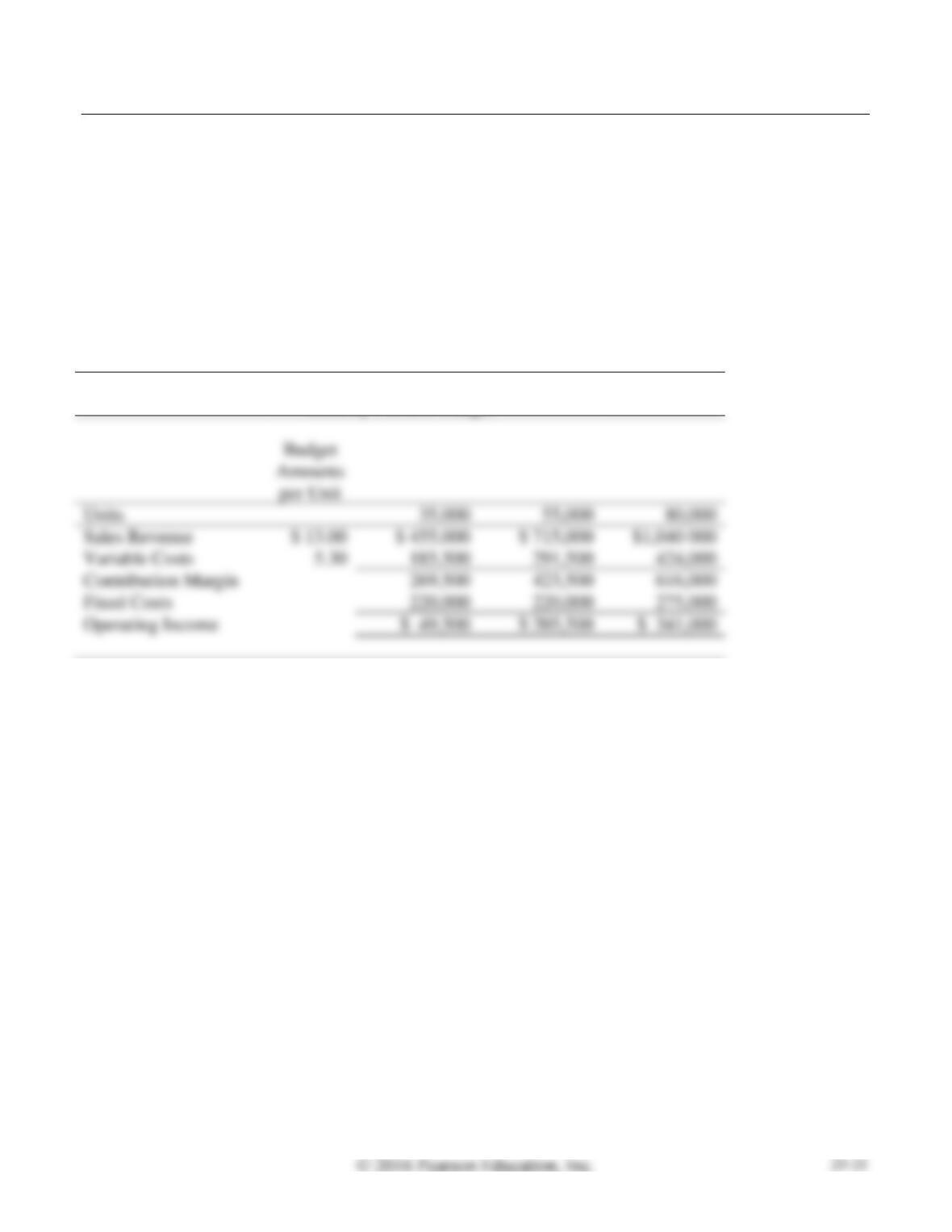

Safe Now sells its main product, ergonomic mouse pads, for $13 each. Its variable cost is $5.30 per pad.

Fixed costs are $220,000 per month for volumes up to 65,000 pads. Above 65,000 pads, monthly fixed

costs are $275,000. Prepare a monthly flexible budget for the product, showing sales revenue, variable

costs, fixed costs, and operating income for volume levels of 35,000, 55,000, and 80,000 pads.

SOLUTION

SAFE NOW

Monthly Flexible Budget

E23-16 Preparing a flexible budget performance report

Learning Objective 1

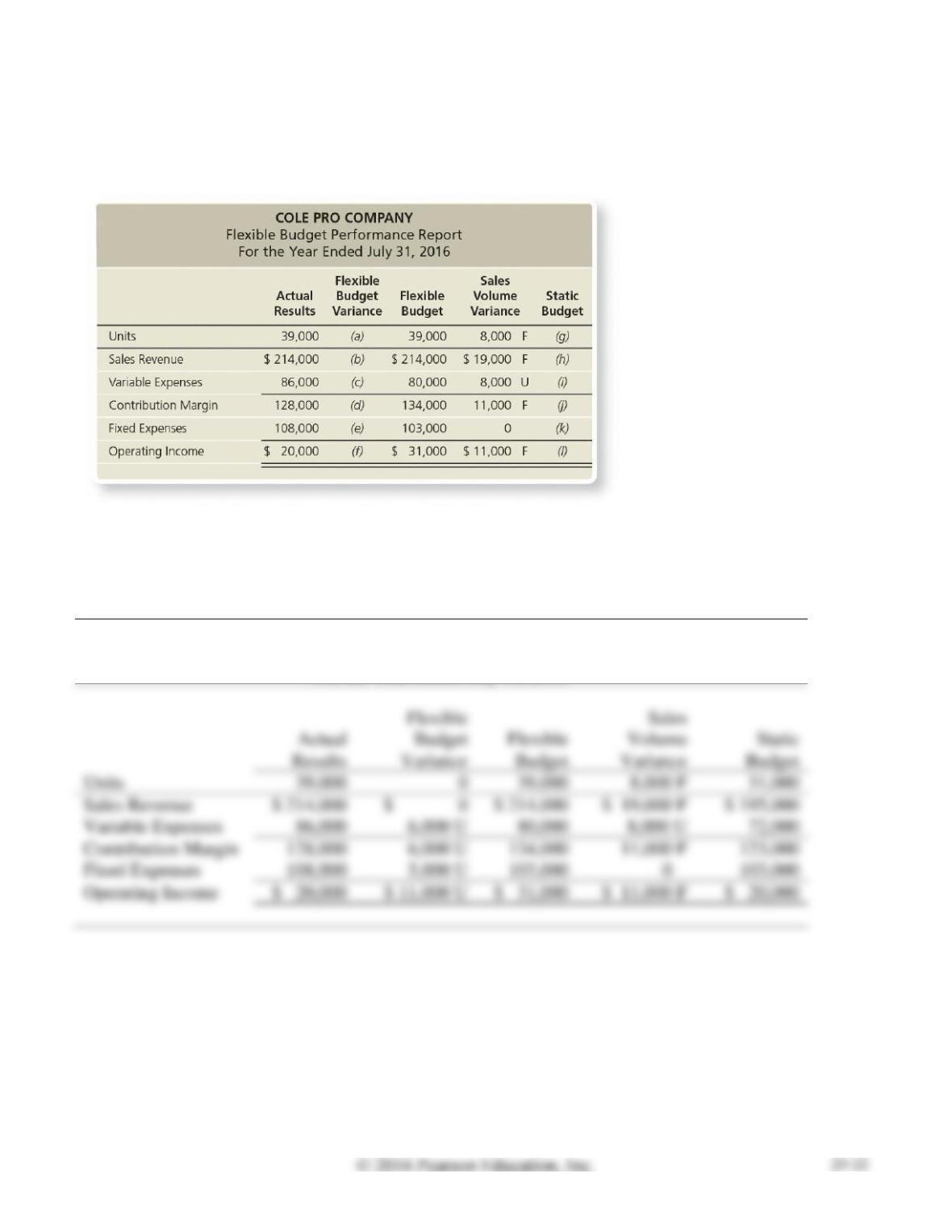

Cole Pro Company managers received the following incomplete performance report:

Complete the performance report. Identify the employee group that may deserve praise and the group

that may be subject to criticism. Give your reasoning.

SOLUTION

COLE PRO COMPANY

Flexible Budget Performance Report

For the Year Ended July 31, 2016

E23-16, cont.

Based on the overall favorable sales volume variance, marketing and sales personnel deserve praise. The

number of units actually sold was greater than the number of units expected to be sold. The overall

$11,000 favorable sales volume variance is the difference between expected operating income ($31,000)

in the flexible budget for the 39,000 units actually sold and expected operating income ($20,000) in the

static budget based on 31,000 units expected to be sold. The overall favorable sales volume variance and

the individual volume variances for sales revenue ($19,000 favorable), variable expenses ($8,000

unfavorable), and contribution margin ($11,000 favorable) arise only because the company sold 39,000

units rather than the 31,000 units expected in the static budget.

Although the overall variable expenses flexible budget variance is $6,000 unfavorable, this is the net

result of variable production flexible budget variances and variable selling and administrative flexible

budget variances. Further, a variable production flexible budget variance is the net result of the total

direct materials variance, total direct labor variance, and total variable manufacturing overhead variance.

Digging even deeper:

• The total direct material variance is the net result of the direct materials cost variance

(purchasing manager) and direct materials efficiency variance (production manager).

• The total direct labor variance is the net result of the direct labor cost variance (human resources

manager) and direct labor efficiency variance (production manager).

• The total variable manufacturing overhead variance (production manager) is the net result of the

variable overhead cost variance and variable overhead efficiency variance.

E23-17 Preparing a flexible budget performance report

Learning Objective 1

Flex. Bud. Var. for Op. Inc. $46,620 F

Top managers of Stenback Industries predicted 2016 sales of 14,900 units of its product at a unit price of

$7.00. Actual sales for the year were 14,300 units at $10.50 each. Variable costs were budgeted at $2.20

per unit, and actual variable costs were $2.30 per unit. Actual fixed costs of $45,000 exceeded budgeted

fixed costs by $2,000.

Prepare Stenback’s flexible budget performance report. What variance contributed most to the year’s

favorable results? What caused this variance?

SOLUTION

STENBACK INDUSTRIES

Flexible Budget Performance Report

For the Year Ended December 31, 2016

1

2

(1) – (3)

3

4

(3) – (5)

5

Budget

Amounts

per Unit

Actual

Results

Flexible

Budget

Variance

Flexible

Budget

Sales

Volume

Variance

Static

Budget

Units

14,300

14,300

14,900

Sales Revenue

$ 50,050

F

U

Variable Costs

U

F

Contribution Margin

117,260

48,620

F

U

Fixed Costs

45,000

U

Operating Income

$ 72,260

$ 46,620

F

$ 25,640

$ 2,880

U

Flexible Budget Variance Sales Volume Variance

(a)

$ 10.50 per unit

×

14,300 units

=

$ 150,150

(b)

$ 2.30 per unit

×

14,300 units

=

$ 32,890

(c)

$ 7.00 per unit

×

14,300 units

=

$

100,100

(d)

$ 2.20 per unit

×

14,300 units

=

$ 31,460

(e)

$45,000

=

$ 43,000

$ 7.00 per unit

×

14,900 units

=

$ 104,300

(g)

$ 2.20 per unit

×

14,900 units

=

$ 32,780

E23-18 Defining the benefits of setting cost standards and calculating materials and labor

variances

Learning Objectives 2, 3

2. DM Eff. Var. $100 F

Bargain, Inc. produced 1,000 units of the company’s product in 2016. The standard quantity of direct

materials was three yards of cloth per unit at a standard cost of $1.00 per yard. The accounting records

showed that 2,900 yards of cloth were used and the company paid $1.05 per yard. Standard time was

two direct labor hours per unit at a standard rate of $9.75 per direct labor hour. Employees worked 1,800

hours and were paid $9.25 per hour.

Requirements

1. What are the benefits of setting cost standards?

2. Calculate the direct materials cost variance and the direct materials efficiency variance as well as the

direct labor cost and efficiency variances.

SOLUTION

Requirement 1

Benefits of setting cost standards (using a standard costing system) include the following:

Requirement 2

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($1.05 per yard – $1.00 per yard)

×

2,900 yards

=

$145 U

Direct Materials Efficiency Variance

=

×

=

×

=

$100 F

=

×

=

$900 F

=

×

$9.75 per DLHr

=

$1,950 F

×

1,000 units

=

3,000 standard yards

×

1,000 units

=

2,000 standard DLHr

E23-19 Calculating materials and labor variances

Learning Objective 3

DL Eff. Var. $1,540 F

Pro Fender, which uses a standard cost system, manufactured 20,000 boat fenders during 2016, using

146,000 square feet of extruded vinyl purchased at $1.05 per square foot. Production required 410 direct

labor hours that cost $15.00 per hour. The direct materials standard was seven square feet of vinyl per

fender, at a standard cost of $1.10 per square foot. The labor standard was 0.026 direct labor hour per

fender, at a standard cost of $14.00 per hour.

Compute the cost and efficiency variances for direct materials and direct labor. Does the pattern of

variances suggest Pro Fender’s managers have been making trade-offs? Explain.

SOLUTION

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($1.05 per sq. foot – $1.10 per sq. foot)

×

146,000

sq. feet

=

$7,300 F

=

×

=

×

=

$6,600 U

(AC ̶ SC)

=

×

=

$410 U

=

×

=

$1,540 F

×

20,000 fenders

=

520 standard DLHr

E23-19 (continued)

There may be trade-offs between the direct materials cost variance and the direct materials efficiency

variance. Decisions made by the purchasing manager may affect the direct materials efficiency variance

for the production manager. Pro Fender’s purchasing manager may have purchased lower quality (less

expensive) direct materials, leading to the $7,300 favorable direct materials cost variance (the $1.05

E23-20 Computing overhead variances

Learning Objective 4

1. FOH Vol. Var. $1,720 U

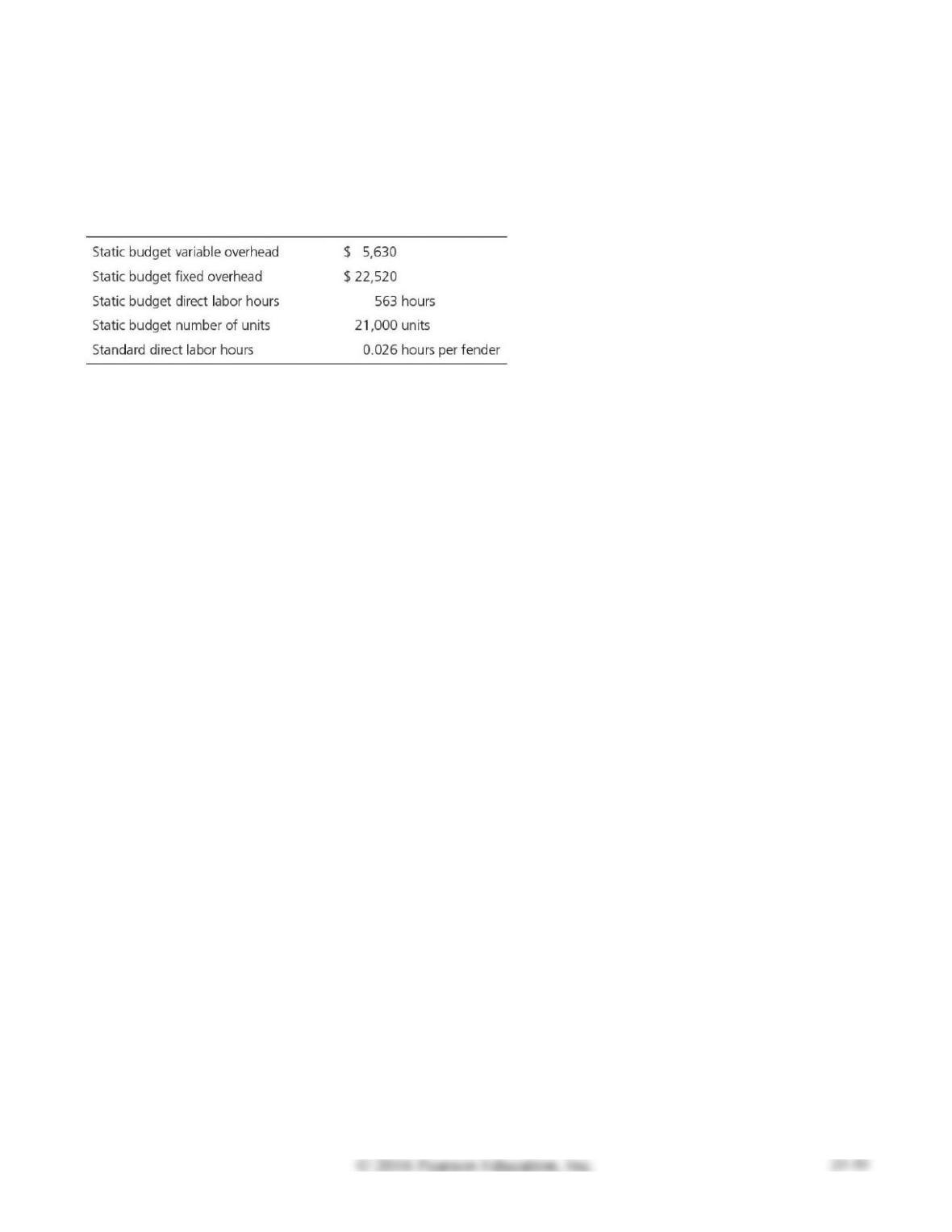

Grand Fender is a competitor of Pro Fender from Exercise E23-19. Grand Fender also uses a standard

cost system and provides the following information:

Grand Fender allocates manufacturing overhead to production based on standard direct labor hours.

Grand Fender reported the following actual results for 2016: actual number of fenders produced, 20,000;

actual variable overhead, $5,200; actual fixed overhead, $24,000; actual direct labor hours, 480.

Requirements

1. Compute the overhead variances for the year: variable overhead cost variance, variable overhead

efficiency variance, fixed overhead cost variance, and fixed overhead volume variance.

2. Explain why the variances are favorable or unfavorable.

SOLUTION

Requirement 1

Standard VOH

allocation rate

=

Budgeted VOH

Budgeted allocation base

allocation rate

Budgeted allocation base

=

$10 per DLHr

E23-20, cont.

Requirement 1, cont.

FOH Cost Variance

=

Actual FOH

̶

Budgeted FOH

=

$24,000

̶

$22,520

=

$1,480 U

=

Budgeted FOH

̶

Allocated FOH

=

$22,520

̶

=

$1,720 U

×

520 DLHr

=

$20,800

Requirement 2

The $400 unfavorable variable overhead cost variance indicates that actual variable overhead cost per

direct labor hour was not kept within standard. The $10.83(c) actual cost per direct labor hour was greater

than the $10.00 standard cost per direct labor hour (the standard variable overhead allocation rate per

direct labor hour).

$5,200

480 DLHr

=

$10.83 rounded

E23-21 Calculating overhead variances

Learning Objective 4

1. VOH Cost Var. $450 U

Good Deal, Inc. is a competitor of Bargain, Inc. from Exercise E23-18. Good Deal also uses a standard

cost system and provides the following information:

Good Deal allocates manufacturing overhead to production based on standard direct labor hours. Good

Deal reported the following actual results for 2016: actual number of units produced, 1,000; actual

variable overhead, $2,400; actual fixed overhead, $2,900; actual direct labor hours, 1,300.

Requirements

1. Compute the variable overhead cost and efficiency variances and fixed overhead cost and volume

variances.

2. Explain why the variances are favorable or unfavorable.

SOLUTION

Requirement 1

Standard VOH

allocation rate

=

Budgeted VOH

Budgeted allocation base

allocation rate

Budgeted allocation base

=

$1.50 per DLHr

E23-21, cont.

Requirement 1, cont.

FOH Cost Variance

=

Actual FOH

̶

Budgeted FOH

=

$2,900

̶

$1,600

=

$1,300 U

=

̶

Allocated FOH

=

$1,600

̶

=

$2,400 F

×

2,000 DLHr

=

$4,000

Requirement 2

The $450 unfavorable variable overhead cost variance indicates that actual variable overhead cost per

direct labor hour was not kept within standard. The $1.85(a) actual cost per direct labor hour was greater

than the $1.50 standard cost per direct labor hour (the standard variable overhead allocation rate per

direct labor hour).

$2,400

1,300 DLHr

=

$1.85 rounded

E23-22 Preparing a standard cost income statement

Learning Objective 6

GP $244,300

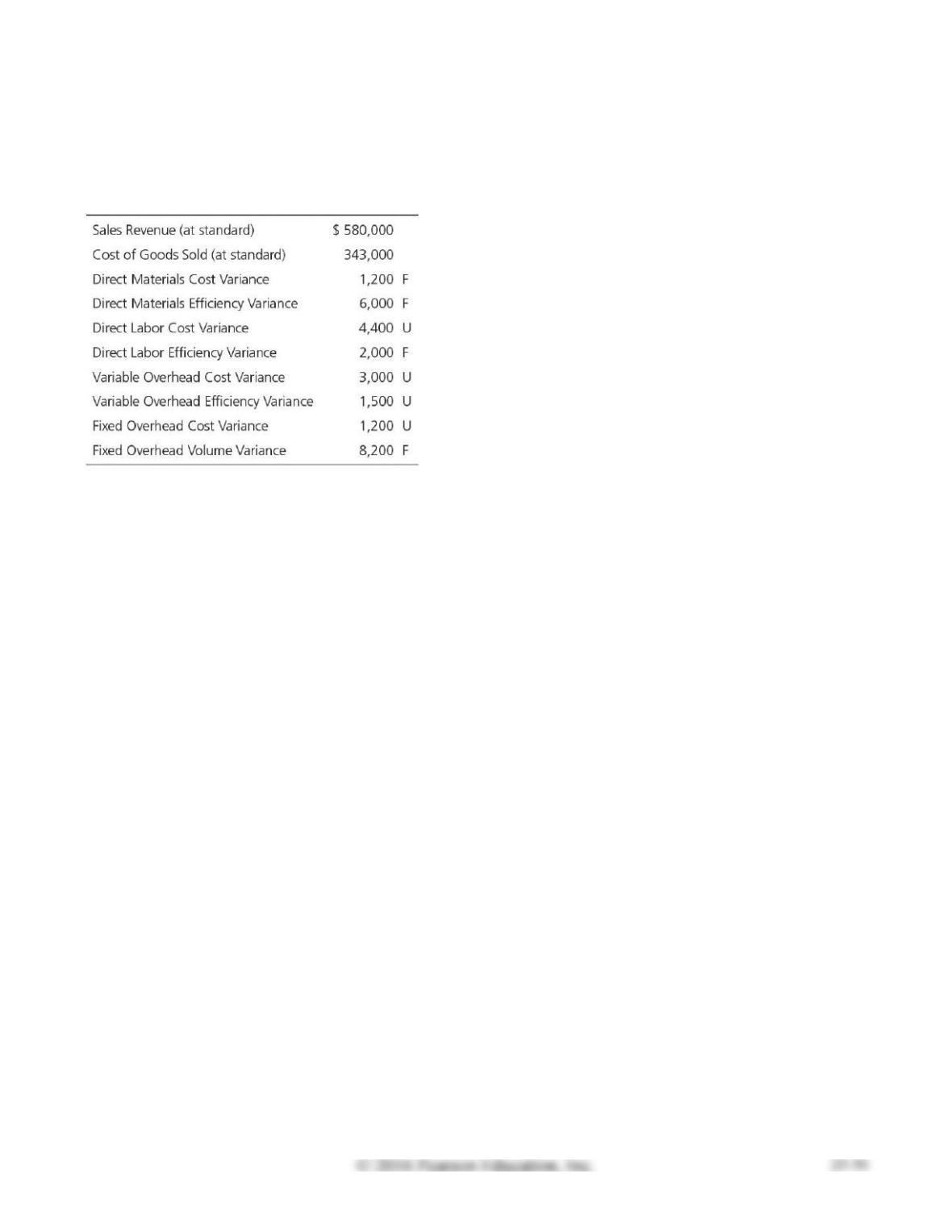

The May 2016 revenue and cost information for Austin Outfitters, Inc. follows:

Prepare a standard cost income statement for management through gross profit. Report all standard cost

variances for management’s use. Has management done a good or poor job of controlling costs?

Explain.

SOLUTION

AUSTIN OUTFITTERS, INC.

Standard Cost Income Statement

For the Month Ended May 31, 2016

Sales Revenue at standard

$ 580,000

Cost of Goods Sold at standard

$ 343,000

Manufacturing Cost Variances:

Cost of Goods Sold at actual

Gross Profit

$ 244,300

The $1,200 favorable direct materials cost variance indicates that management did a good job keeping

actual direct materials cost per unit within standard. The actual cost per unit was less than the standard

cost per unit.

The $6,000 favorable direct materials efficiency variance indicates that management did a good job

keeping actual usage of direct materials within standard. The total quantity of direct materials actually

used was less than the total allowed to manufacture the actual total number of units.

E23-22, cont.

The $1,500 unfavorable variable overhead efficiency variance indicates that management did not do a

good job keeping actual usage of the allocation base for variable overhead within standard. The total

quantity of the allocation base actually used was greater than the total allowed to manufacture the actual

total number of units.

E23-23 Preparing journal entries

Learning Objective 6

MOH Adj. $1,500 DR

Hayesville Company uses a standard cost system and reports the following information for 2016:

Hayesville Company reported the following variances:

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Raw Materials Inventory ($1.05/yard × 2,700 yards)

2,835

Direct Materials Cost Variance

135

Accounts Payable ($1.10/yard × 2,700 yards)

2,970

Purchased direct materials.

Work-in-Process Inventory ($1.05/yard × 3,000 yards)

3,150

Direct Materials Efficiency Variance

315

Raw Materials Inventory ($1.05/yard × 2,700 yards)

2,835

Used direct materials.

Work-in-Process Inventory ($10.25/DLHr × 2,000 DLHr)

20,500

Direct Labor Cost Variance

650

Direct Labor Efficiency Variance

7,175

Wages Payable ($9.75/DLHr × 1,300 DLHr)

12,675

Direct labor costs incurred.

Manufacturing Overhead ($4,000 VOH + $2,500 FOH)

6,500

Various Accounts

6,500

Manufacturing overhead costs incurred.

Work-in-Process Inventory ($4/DLHr × 2,000 DLHr)

8,000

Manufacturing Overhead

8,000

Manufacturing overhead costs allocated.

Finished Goods Inventory ($3,150 + $20,500 + $8,000)

31,650

31,650

Completed goods transferred.

Cost of Goods Sold

31,650

Finished Goods Inventory

31,650

Cost of sales at standard cost.

Manufacturing Overhead

1,500

Variable Overhead Cost Variance

1,400

Fixed Overhead Cost Variance

200

Variable Overhead Efficiency Variance

1,400

Fixed Overhead Volume Variance

1,700

To adjust Manufacturing Overhead.