SOLUTION

Requirement 1

ROOT RECLINERS

Flexible Budget

Budget

Amounts

per Unit

Actual Units (Recliners)

980

Sales

Variable Manufacturing Costs:

Direct Materials

Direct Labor

Variable Overhead

Fixed Manufacturing Costs:

Fixed Overhead

Total Cost of Goods Sold

Gross Profit

(a)

$ 52,200

/

1,000 recliners

=

$ 52.20 per recliner

(b)

$ 90,000

/

1,000 recliners

=

$ 90.00 per recliner

(c)

$ 30,000

/

1,000 recliners

=

$ 30.00 per recliner

(d)

$ 505.00 per recliner

×

980 recliners

=

$ 494,900

(e)

$ 52.20 per recliner

×

980 recliners

=

$ 51,156

$ 90.00 per recliner

×

980 recliners

=

$ 88,200

(g)

$ 30.00 per recliner

×

980 recliners

=

$ 29,400

Requirement 2

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($8.50 per yard – $8.70 per yard)

×

6,143 yards

=

$1,229 F

Direct Materials Efficiency Variance

=

×

=

×

$8.70 per yard

=

$2,288 U

Direct Labor Cost Variance

=

×

AQ

=

($9.10 per DLHr – $9.00 per DLHr)

×

9,600 DLHr

=

$960 U

P23-31B, cont.

Requirement 2, cont.

Direct Labor Efficiency Variance

=

(AQ ̶ SQ)

×

SC

=

(9,600 DLHr – 9,800 DLHr(b))

×

$9.00 per DLHr

=

$1,800 F

=

×

=

×

6,143 yards

=

$8,600 U

=

×

=

$1,315 U

FOH Cost Variance

=

Actual FOH

̶

Budgeted FOH

=

$62,000

̶

$60,000

=

$2,000 U

=

̶

Allocated FOH

=

$60,000

̶

=

$1,200 U

1,000 recliners

=

6 yards per recliner

Thus:

×

980 recliners

=

5,880 yards

10,000 DLHr

1,000 recliners

=

10 DLHr per recliner

Thus:

10 DLHr per recliner

×

980 recliners

=

9,800 DLHr

6,000 yards

=

$10.00 per yard

Thus:

×

5,880 yards

=

$58,800

P23-31B, cont.

Requirement 3

The $1,229 favorable direct materials cost variance indicates that Root’s managers did a good job

keeping actual direct materials cost per yard within standard. The $8.50 actual cost per yard was less

than the $8.70 standard cost per yard.

The $8,600 unfavorable variable overhead cost variance indicates that Root’s managers did not do a

good job keeping actual variable overhead cost per yard within standard. The $6.40 actual cost per yard

was greater than the $5.00 standard cost per yard (the standard variable overhead allocation rate per

yard).

The $2,000 unfavorable fixed overhead cost variance indicates that Root’s managers did not do a good

job keeping actual total fixed cost within budget. The $62,000 actual total fixed overhead cost was

greater than the $60,000 budgeted total fixed overhead cost.

P23-31B, cont.

Requirement 4

Root’s managers can benefit from the standard costing system in the following ways:

• Preparing the master budget.

P23-32B Computing standard cost variances and reporting to management

Learning Objectives 3, 4, 5

1. DM Eff. Var. $300 F

Smart Sets manufactures headphone cases. During September 2016, the company produced 108,000

cases and recorded the following cost data:

Standard Cost Information

Actual Information

Requirements

1. Compute the cost and efficiency variances for direct materials and direct labor.

2. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the

fixed overhead cost and volume variances.

3. Smart Sets’s management used better-quality materials during September. Discuss the trade-off

between the two direct material variances.

SOLUTION

Requirement 1

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($0.20 per part – $0.15 per part)

×

214,000 parts

=

$10,700 U

=

×

=

$300 F

=

×

=

$166 U

=

×

$8.00 per DLHr

=

$4,000 F

×

108,000 cases

=

216,000 parts

0.02 DLHr per case

×

108,000 cases

=

2,160 DLHr

P23-32B, cont.

Requirement 2

VOH Cost Variance

=

Actual VOH

−

(SC × AQ)

=

$14,000

−

($9 per DLHr × 1,660 DLHr)

=

$940 F

=

×

=

$4,500 F

=

$ 5,360 F

=

$ 3,200 F

×

2,160 DLHr

=

$34,560

Requirement 3

There may be trade-offs between the direct materials cost variance and the direct materials efficiency

variance. Decisions made by the purchasing manager may affect the direct materials efficiency variance

for the production manager. Perhaps Smart Sets used better quality direct materials, indicated by the fact

P23-33B Computing and journalizing standard cost variances

Learning Objectives 3, 4, 5, 6

3. VOH Cost Var. $2,985 F

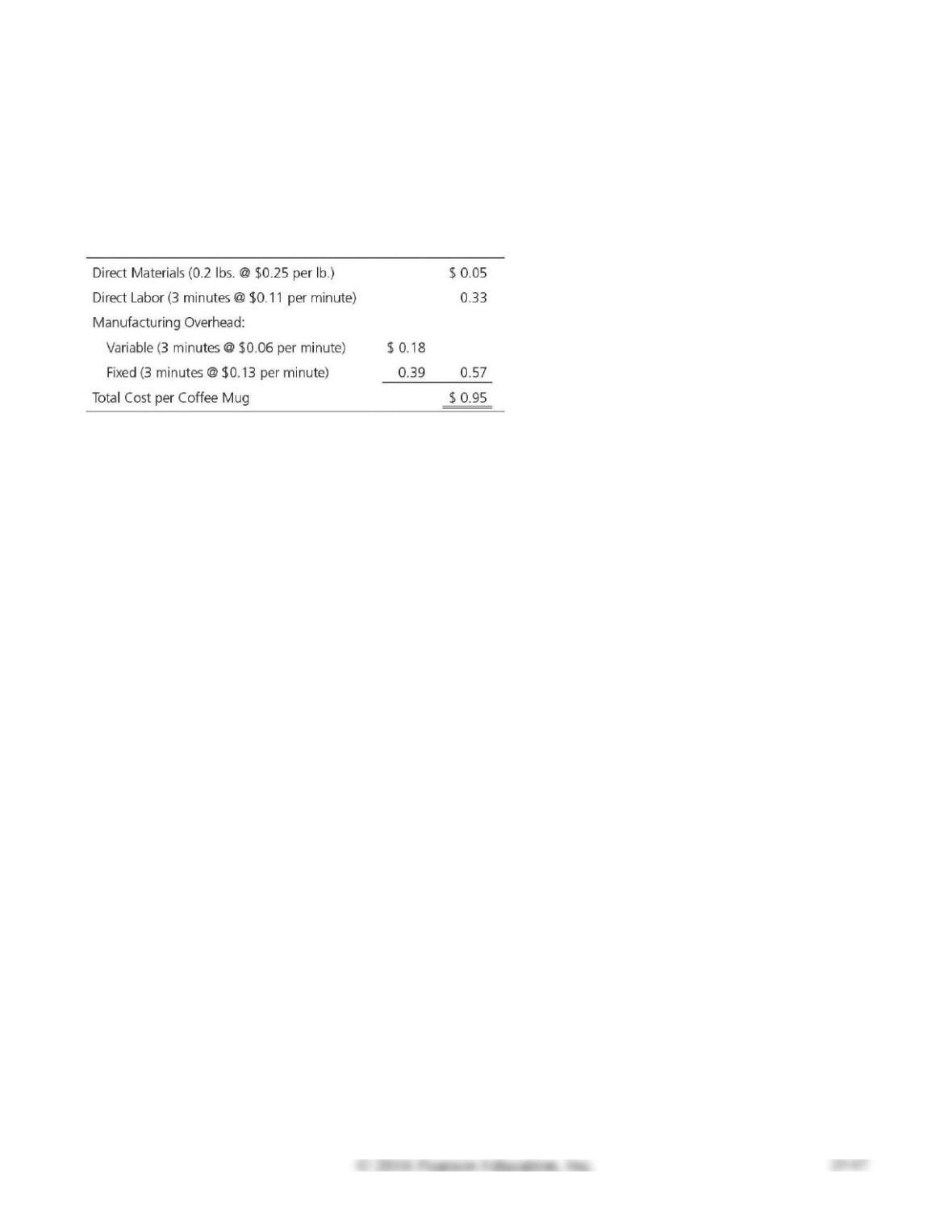

Smith manufactures coffee mugs that it sells to other companies for customizing with their own logos.

Smith prepares flexible budgets and uses a standard cost system to control manufacturing costs. The

standard unit cost of a coffee mug is based on static budget volume of 59,900 coffee mugs per month:

Actual cost and production information for July 2016 follows:

a. Actual production and sales were 62,600 coffee mugs.

b. Actual direct materials usage was 10,000 lbs. at an actual cost of $0.17 per lb.

c. Actual direct labor usage of 199,000 minutes at a cost of $27,860.

d. Actual overhead cost was $8,955 variable and $31,945 fixed.

e. Selling and administrative costs were $95,000.

Requirements

1. Compute the cost and efficiency variances for direct materials and direct labor.

2. Journalize the purchase and usage of direct materials and the assignment of direct labor, including

the related variances.

3. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the

fixed overhead cost and volume variances.

4. Journalize the actual manufacturing overhead and the allocated manufacturing overhead. Journalize

the movement of all production from Work-in-Process Inventory. Journalize the adjusting of the

Manufacturing Overhead account.

5. Smith intentionally hired more highly skilled workers during July. How did this decision affect the

cost variances? Overall, was the decision wise?

SOLUTION

Requirement 1

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($0.17 per lb. – $0.25 per lb.)

×

10,000 lbs.

=

$800 F

=

×

$0.25 per lb.

=

$630 F

=

×

=

$5,970 U

=

×

=

$1,232 U

×

62,600 mugs

=

12,520 lbs.

$27,860 total cost

199,000 minutes

=

$0.14 cost per minute

3 minutes per mug

×

62,600 mugs

=

187,800 minutes

P23-33B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Raw Materials Inventory ($0.25/lb. × 10,000 lbs.)

2,500

Direct Materials Cost Variance (from Req. 1)

800

Accounts Payable ($0.17/lb. × 10,000 lbs.)

1,700

Purchased direct materials.

3,130

Direct Materials Efficiency Variance (from Req. 1)

630

Raw Materials Inventory ($0.25/lb. × 10,000 lbs.)

2,500

Used direct materials.

Direct Labor Cost Variance (from Req.1 )

5,970

Direct Labor Efficiency Variance (from Req. 1)

1,232

Wages Payable ($0.14/min × 199,000 min.)

Direct labor costs incurred.

Requirement 3

VOH Cost Variance

=

Actual VOH

−

(SC × AQ)

=

$8,955

−

($0.06 per min. × 199,000 min.)

=

$2,985 F

=

×

=

$672 U

=

$ 8,584 U

=

$ 1,053 F

×

=

$23,361

×

×

=

$24,414

P23-33B, cont.

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Manufacturing Overhead ($8,955 + $31,945)

40,900

Various Accounts

40,900

Manufacturing overhead costs incurred.

35,682

Manufacturing Overhead

35,682

Manufacturing overhead costs allocated.

Finished Goods Inventory ($3,130 + $20,658 + $35,682)

59,470

59,470

Completed goods transferred.

Variable Overhead Efficiency Variance (from Req. 3)

Fixed Overhead Cost Variance (from Req. 3)

To adjust Manufacturing Overhead.

Requirement 5

Because Smith hired more skilled workers, the $0.14 actual direct labor cost per minute was greater than

the $0.11 direct labor standard cost per minute. Therefore, the direct labor cost variance was $5,970

unfavorable for the 62,600 mugs actually produced. Hiring more skilled direct labor workers could be

Note: Problem P23-33B must be completed before attempting Problem P23-34B.

P23-34B Preparing a standard cost income statement

Learning Objective 6

COGS at actual $70,460

Review your results from Problem P23-33B. Smith’s actual and standard sales price per mug is $5.

Prepare the standard cost income statement for July 2016.

SOLUTION

SMITH

Standard Cost Income Statement

For the Month Ended July 31, 2016

Continuing Problem

P23-35 Calculating materials and labor variances and preparing journal entries

This continues the Daniels Consulting situation from Problem P22-57 of Chapter 22. Assume Daniels

has created a standard cost card for each job. Standard direct materials per job include 10 software

packages at a cost of $900 per package. Standard direct labor costs per job include 105 hours at $100 per

hour. Daniels plans on completing 12 jobs during March 2018.

Actual direct materials costs for March included 90 software packages at a total cost of $81,450. Actual

direct labor costs included 110 hours per job at an average rate of $107 per hour. Daniels completed all

12 jobs in March.

Requirements

1. Calculate direct materials cost and efficiency variances.

2. Calculate direct labor cost and efficiency variances.

3. Prepare journal entries to record the use of both materials and labor for March for the company.

SOLUTION

Requirement 1

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($905 per package(a) – $900 per package)

×

90 packages

=

$450 U

=

×

=

×

=

$27,000 F

$81,450 total DM cost

/

90 packages

=

$905 DM cost per package

10 packages per job

×

12 jobs

=

120 packages

Requirement 2

Direct Labor Cost Variance

=

(AC ̶ SC)

×

AQ

=

($107 per DLHr – $100 per DLHr)

×

1,320 DLHr(a)

=

$9,240 U

Direct Labor Efficiency Variance

=

×

=

×

=

$6,000 U

P23-36, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Work-in-Process Inventory ($900/pkg. × 120 pkgs.)

108,000

Direct Materials Efficiency Variance (from Req. 1)

27,000

Raw Materials Inventory ($900/pkg. × 90 pkgs.)

81,000

Used direct materials.

Work-in-Process Inventory ($100/DLHr × 1,260 DLHr)

126,000

Direct Labor Cost Variance (from Req. 2)

Direct Labor Efficiency Variance (from Req. 2)

Wages Payable ($107/DLHr × 110 DLHr/job × 12 jobs)

141,240

Direct labor costs incurred.

Decision Case 23-1

Suppose you manage the local Scoopy’s ice cream parlor. In addition to selling ice cream cones, you

make large batches of a few flavors of milk shakes to sell throughout the day. Your parlor is chosen to

test the company’s “Made-for-You” system. This new system enables patrons to customize their milk

shakes by choosing different flavors.

Customers like the new system and your staff appears to be adapting, but you wonder whether this

new made-to-order system is as efficient as the old system in which you just made a few large batches.

Efficiency is a special concern because your performance is evaluated in part on the restaurant’s

efficient use of materials and labor. Your superiors consider efficiency variances greater than 5% to be

unacceptable.

You decide to look at your sales for a typical day. You find that the parlor used 390 pounds of ice

cream and 72 hours of direct labor to produce and sell 2,000 shakes. The standard quantity allowed for a

shake is 0.2 pound of ice cream and 0.03 hour of direct labor. The standard costs are $1.50 per pound for

ice cream and $8 per hour for labor.

Requirements

1. Compute the efficiency variances for direct labor and direct materials.

2. Provide likely explanations for the variances. Do you have reason to be concerned about your

performance evaluation? Explain.

3. Write a memo to Scoopy’s national office explaining your concern and suggesting a remedy.

SOLUTION

Requirement 1

Direct Labor Efficiency Variance

=

(AQ ̶ SQ)

×

SC

=

(72 DLHr – 60 DLHr(a))

×

$8 per DLHr

=

$96 U

=

×

=

(390 pounds – 400 pounds(b))

×

=

$15 F

0.03 DLHr per shake

×

2,000 shakes

=

60 DLHr

×

2,000 shakes

=

400 pounds

Requirement 2

The $15 favorable direct materials efficiency variance indicates that actual usage of direct materials (ice

cream) was kept within standard. The 390 pounds of ice cream actually used was less than the 400

pounds allowed to produce 2,000 shakes. Although favorable, the variance is relatively small—only

2.5% under the $600 total direct materials standard allowed to produce 2,000 shakes(a).

×

$1.50 per pound

=

$600

Thus:

$600

=

2.5%

60 DLHr

×

$8 per DLHr

=

$480

Thus:

$480

=

20%

Decision Case 23-1, cont.

Requirement 3

DATE:

TO: Scoopy’s National Office

FROM:

SUBJECT: “Made-for-You” System

The “Made-for-You” system test has yielded some benefits. Customers enjoy being able to customize

their shakes, employees appear to be adapting, and the direct materials efficiency variance is favorable.

However, employees are relatively less efficient under the new system. The unfavorable direct labor

efficiency variance is 20% over the current direct labor standard allowed for actual shakes produced.

Fraud Case 23–1

Drew Castello, general manager of Sunflower Manufacturing, was frustrated. He wanted the budgeted

results, and his staff was not getting them to him fast enough. Drew decided to pay a visit to the

accounting office, where Jeff Hollingsworth was supposed to be working on the reports. Jeff had

recently been hired to update the accounting system and speed up the reporting process.

After looking at the time records, Jeff pointed out that it was unusual that every employee in the

production area recorded exactly eight hours each day in direct labor. Did they not take breaks? Was no

one ever five minutes late getting back from lunch? What about clean-up time between jobs or at the end

of the day?

Drew began to observe the production laborers and noticed several disturbing items. One employee

was routinely late for work, but his time card always showed him clocked in on time. Another employee

took 10- to 15-minute breaks every hour, averaging about 1½ hours each day, but still reported eight

hours of direct labor each day. Yet another employee often took an extra 30 minutes for lunch, but his

time card showed him clocked in on time. No one in the production area ever reported any “down time”

when they were not working on a specific job, even though they all took breaks and completed other

tasks such as doing clean-up and attending department meetings.

Requirements

1. How might the observed behaviors cause an unfavorable direct labor efficiency variance?

2. How might an employee’s time card show the employee on the job and working when the employee

was not present?

3. Why would the employees’ activities be considered fraudulent?

SOLUTION

Requirement 1

The direct labor efficiency variance measures actual labor usage compared to standard labor usage. If

Requirement 2

An employee’s time card might show the employee on the job and working when not present if the

Requirement 3

The employees’ activities would be considered fraudulent because they are reporting that they worked

Team Project 23-1

Lynx Corp. manufactures windows and doors. Lynx has been using a standard cost system that bases

cost and efficiency standards on Lynx’s historical long–run average performance. Suppose Lynx’s

controller has engaged your team of management consultants to advise him or her whether Lynx should

use some basis other than historical performance for setting standards.

Requirements

1. List the types of variances you recommend that Lynx compute (for example, direct materials cost

variance for glass). For each variance, what specific standards would Lynx need to develop? In

addition to cost standards, do you recommend that Lynx develop any nonfinancial standards?

2. There are many approaches to setting standards other than simply using long-run average historical

costs and quantities.

a. List three alternative approaches that Lynx could use to set standards, and explain how Lynx

could implement each alternative.

b. Evaluate each alternative method of setting standards, including the pros and cons of each

method.

c. Write a memo to Lynx’s controller detailing your recommendations. First, should Lynx retain its

historical data-based standard cost approach? If not, which of the alternative approaches should it

adopt?

SOLUTION

Requirement 1

Lynx should compute cost variances and efficiency variances for each type of direct material (for

Requirement 2

Part a

Three alternative approaches that Lynx could use to set standards include the following:

(1) Engineering analysis/time-and-motion studies.

This approach reveals the minimum amount of direct materials, direct labor, and manufacturing

Team Project 23-1, cont.

Requirement 2, cont.

Part b

(1) Engineering analysis/time-and-motion studies.

This approach usually allows for unavoidable waste and spoilage, but it could result in tight, or difficult-

Team Project 23-1, cont.

Requirement 2, cont.

Part c

MEMO

DATE:

TO: Controller, Lynx Corporation

FROM: _______________, Management Consultants

SUBJECT: Standard Costs

However, we suggest that Lynx examine trade publications for relevant benchmark data, and explore the

possibilities of partnering with other manufacturers to obtain external benchmark data. If benchmark

data are too costly or impossible to obtain, then we recommend conducting time-and-motion studies in

order to set tight, but achievable, standards. In future years, these standards could form the baseline for

continuous improvement adjustments that would give employees incentives to increase efficiency.

Communication Activity 23-1

In 75 words or fewer, explain what a cost variance is and describe its potential causes.

SOLUTION

A cost variance measures how well a company keeps unit costs of production inputs within standards.