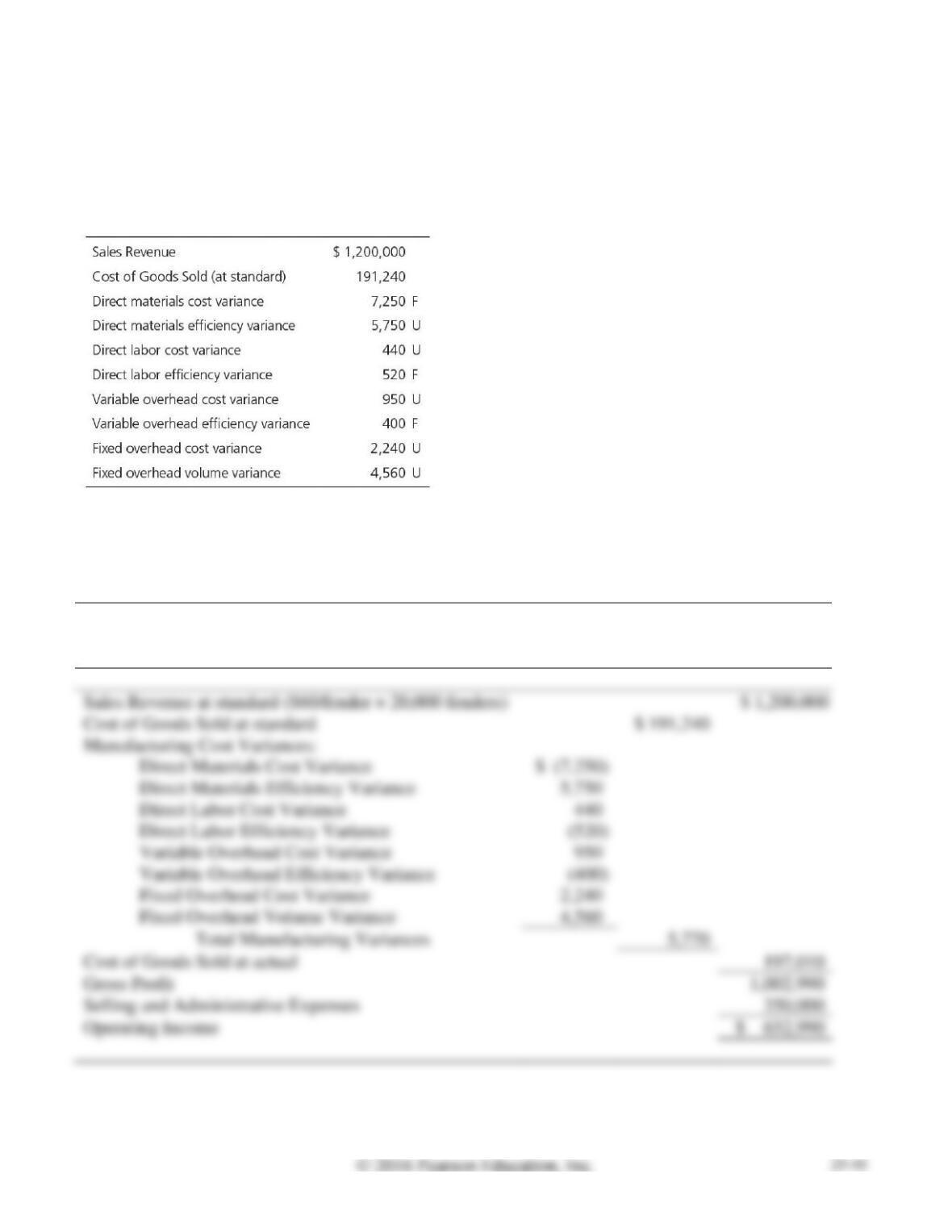

E23-24 Preparing a standard cost income statement

Learning Objective 6

GP $1,002,990

All-Star Fender, which uses a standard cost system, manufactured 20,000 boat fenders during 2016. The

2016 revenue and cost information for All-Star follows:

Assume each fender produced was sold for the standard price of $60, and total selling and administrative

costs were $350,000. Prepare a standard cost income statement for 2016 for All-Star Fender.

SOLUTION

ALL-STAR FENDER

Standard Cost Income Statement

For the Year Ended December 31, 2016

Problems (Group A)

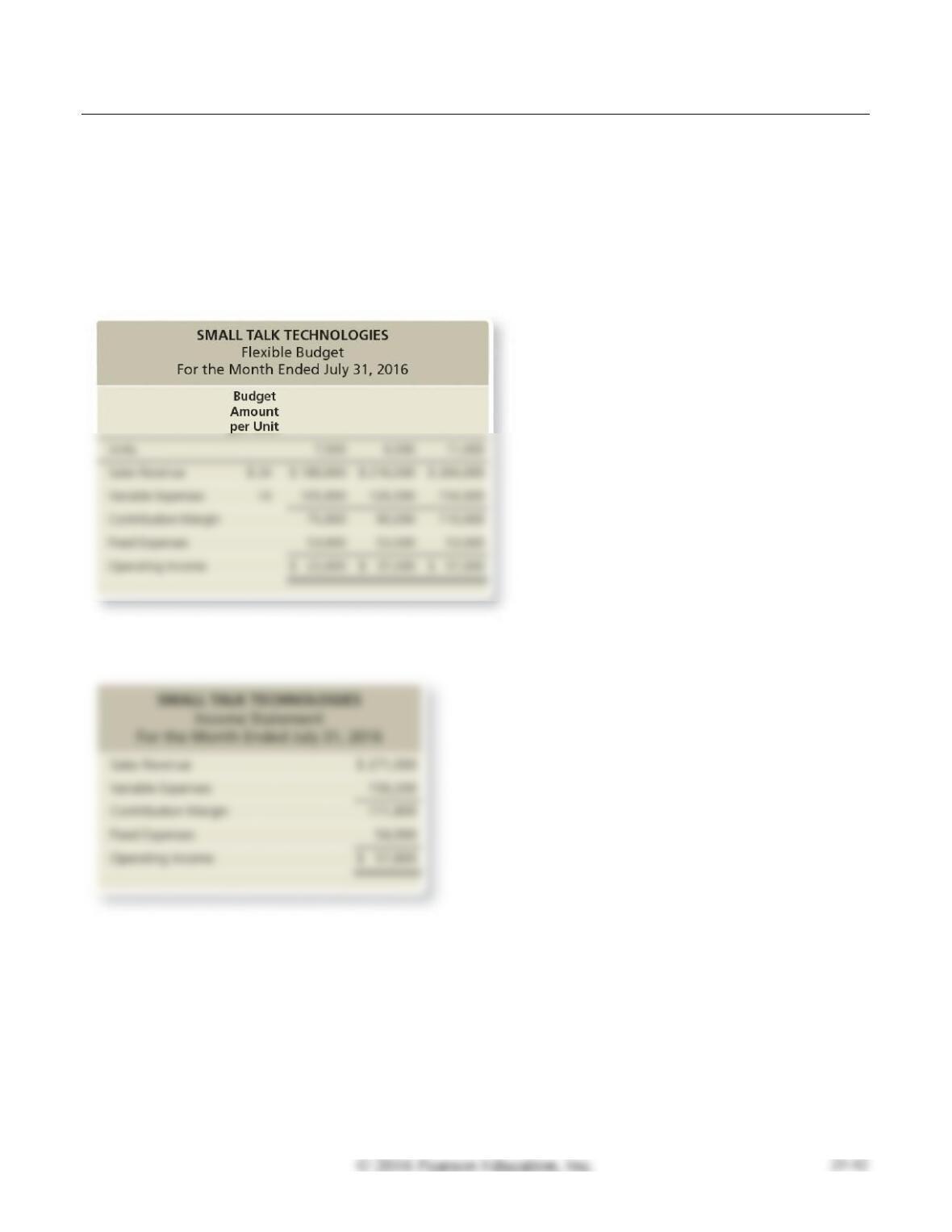

P23-25A Preparing a flexible budget performance report

Learning Objective 1

1. Static Bud. Var. for Op. Inc. $20,800 F

Small Talk Technologies manufactures capacitors for cellular base stations and other communications

applications. The company’s July 2016 flexible budget shows output levels of 7,500, 9,000, and 11,000

units. The static budget was based on expected sales of 9,000 units.

The company sold 11,000 units during July, and its actual operating income was as follows:

Requirements

1. Prepare a flexible budget performance report for July.

2. What was the effect on Small Talk’s operating income of selling 2,000 units more than the static

budget level of sales?

3. What is Small Talk’s static budget variance for operating income?

4. Explain why the flexible budget performance report provides more useful information to Small

Talk’s managers than the simple static budget variance. What insights can Small Talk’s managers

draw from this performance report?

SOLUTION

Requirement 1

SMALL TALK TECHNOLOGIES

Flexible Budget Performance Report

For the Month Ended July 31, 2016

1

2

(1) – (3)

3

4

(3) – (5)

5

Budget

Amounts

per Unit

Actual

Results

Flexible

Budget

Variance

Flexible

Budget

Sales

Volume

Variance

Static

Budget

$ 271,000

28,000

20,000

Requirement 2

Selling 2,000 units more than the static budget level of sales increased Small Talk’s operating income by

Requirement 3

P23-25A, cont.

Requirement 4

The static budget is prepared for only one level of sales volume—the 9,000 units expected to be sold—

and it doesn’t change after it is developed. The $20,800 favorable static budget variance is the difference

between actual operating income ($57,800), based on 11,000 units actually sold, and the expected

operating income ($37,000) in the static budget, based on 9,000 units expected to be sold. The flexible

budget performance report (Requirement 1) provides more useful information than the simple static

budget variance because it separates the $20,800 favorable static budget variance into its components:

the $800 favorable flexible budget variance and the $20,000 favorable sales volume variance.

The overall $800 favorable flexible budget variance is the difference between actual operating income

($57,800) for the 11,000 units actually sold and expected operating income ($57,000) in the flexible

budget for the 11,000 units actually sold. Because the $7,000 favorable flexible budget variance for sales

revenue was $800 greater than the sum of the unfavorable flexible budget variances for variable

expenses ($5,200) and fixed expenses ($1,000), the overall flexible budget variance (for operating

income) was $800 favorable. The individual flexible budget variances arise because actual sales price

per unit, variable expense per unit, and fixed expenses were different from those expected for the 11,000

units actually sold.

• The $7,000 favorable flexible budget variance for sales revenue was favorable because the

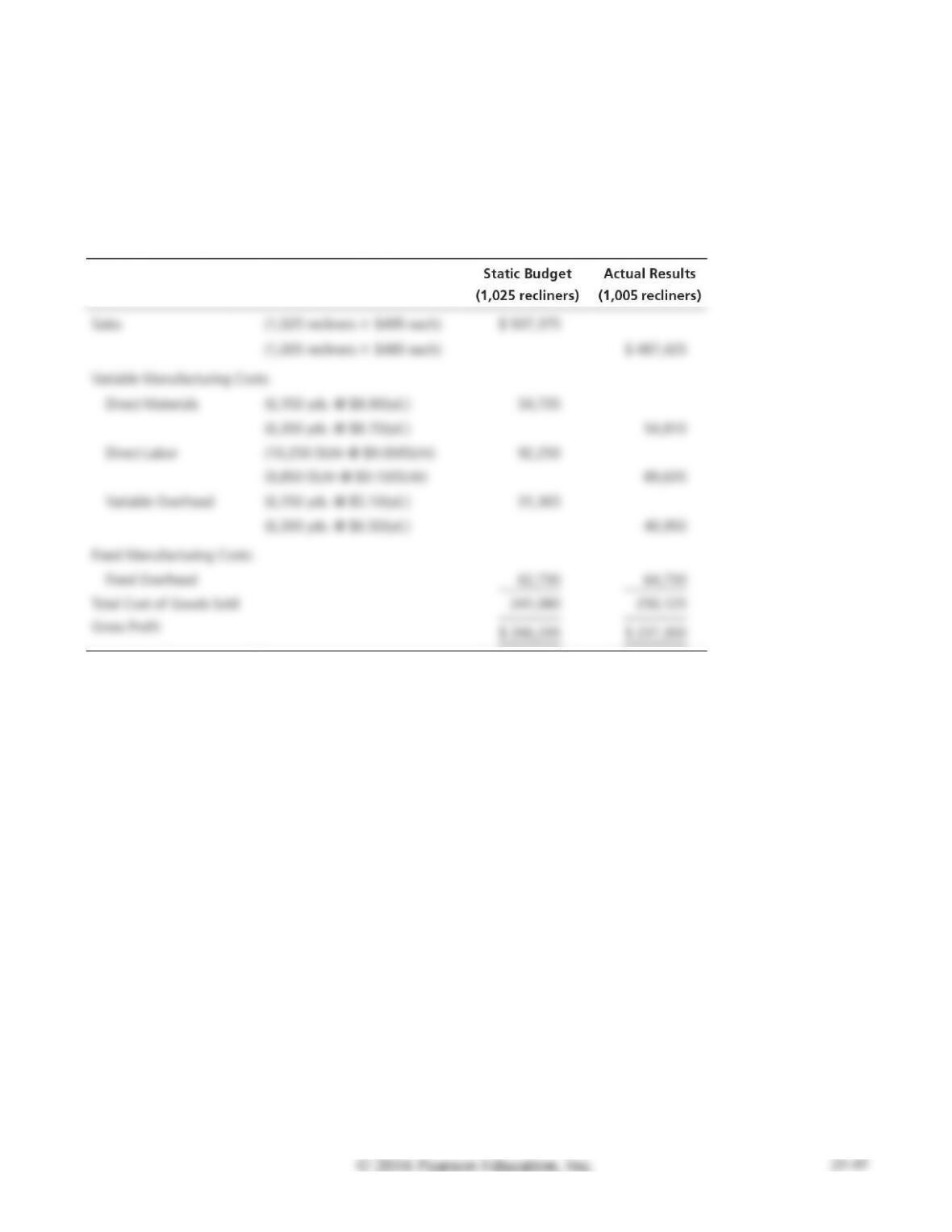

P23-26A Preparing a flexible budget computing standard cost variances

Learning Objectives 1, 3, 4

2. VOH Eff. Var. $1,377 U

Kyler Recliners manufactures leather recliners and uses flexible budgeting and a standard cost system.

Kyler allocates overhead based on yards of direct materials. The company’s performance report includes

the following selected data:

Requirements

1. Prepare a flexible budget based on the actual number of recliners sold.

2. Compute the cost variance and the efficiency variance for direct materials and for direct labor. For

manufacturing overhead, compute the variable overhead cost, variable overhead efficiency, fixed

overhead cost, and fixed overhead volume variances. Round to the nearest dollar.

3. Have Kyler’s managers done a good job or a poor job controlling materials, labor, and overhead

costs? Why?

4. Describe how Kyler’s managers can benefit from the standard cost system.

SOLUTION

Requirement 1

KYLER RECLINERS

Flexible Budget

Actual Units (Recliners)

Sales

Variable Manufacturing Costs:

Direct Materials

Direct Labor

Variable Overhead

Fixed Manufacturing Costs:

Fixed Overhead

Total Cost of Goods Sold

Gross Profit

Budget

Amounts

(a)

$ 54,735

/

1,025 recliners

=

$53.40 per recliner

(b)

$ 92,250

/

1,025 recliners

=

$ 90.00 per recliner

(c)

$ 31,365

/

1,025 recliners

=

$ 30.60 per recliner

(d)

$495.00 per recliner

×

1,005 recliners

=

$ 497,475

(e)

$ 53.40 per recliner

×

1,005 recliners

=

$ 53,667

$ 90.00 per recliner

×

1,005 recliners

=

$ 90,450

(g)

$ 30.60 per recliner

×

1,005 recliners

=

$ 30,753

Requirement 2

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($8.70 per yard – $8.90 per yard)

×

6,300 yards

=

$1,260 F

=

×

$8.90 per yard

=

$2,403 U

=

×

AQ

=

×

=

$985 U

P23-26A, cont.

Requirement 2, cont

Direct Labor Efficiency Variance

=

(AQ ̶ SQ)

×

SC

=

(9,850 DLHr – 10,050 DLHr(b))

×

$9.00 per DLHr

=

$1,800 F

=

×

=

×

6,300 yards

=

$8,820 U

=

×

=

$1,377 U

FOH Cost Variance

=

Actual FOH

̶

Budgeted FOH

=

$64,730

̶

$62,730

=

$2,000 U

=

̶

Allocated FOH

=

$62,730

̶

=

$1,224 U

1,025 recliners

=

6 yards per recliner

Thus:

×

1,005 recliners

=

6,030 yards

1,025 recliners

=

10 DLHr per recliner

Thus:

10 DLHr per recliner

×

1,005 recliners

=

10,050 DLHr

6,150 yards

=

$10.20 per yard

Thus:

×

6,030 yards

=

$61,506

P23-26A, cont.

Requirement 3

The $1,260 favorable direct materials cost variance indicates that Kyler’s managers did a good job

keeping actual direct materials cost per yard within standard. The $8.70 actual cost per yard was less

than the $8.90 standard cost per yard.

The $1,800 favorable direct labor efficiency variance indicates that Kyler’s managers did a good job

keeping actual usage of direct labor hours within standard. The 9,850 total direct labor hours actually

used was less than the 10,050 total direct labor hours allowed to manufacture 1,005 recliners.

The $8,820 unfavorable variable overhead cost variance indicates that Kyler’s managers did not do a

good job keeping actual variable overhead cost per yard within standard. The $6.50 actual cost per yard

was greater than the $5.10 standard cost per yard (the standard variable overhead allocation rate per

yard).

P23-26A, cont.

Requirement 4

Kyler’s managers can benefit from the standard costing system in the following ways:

• Preparing the master budget.

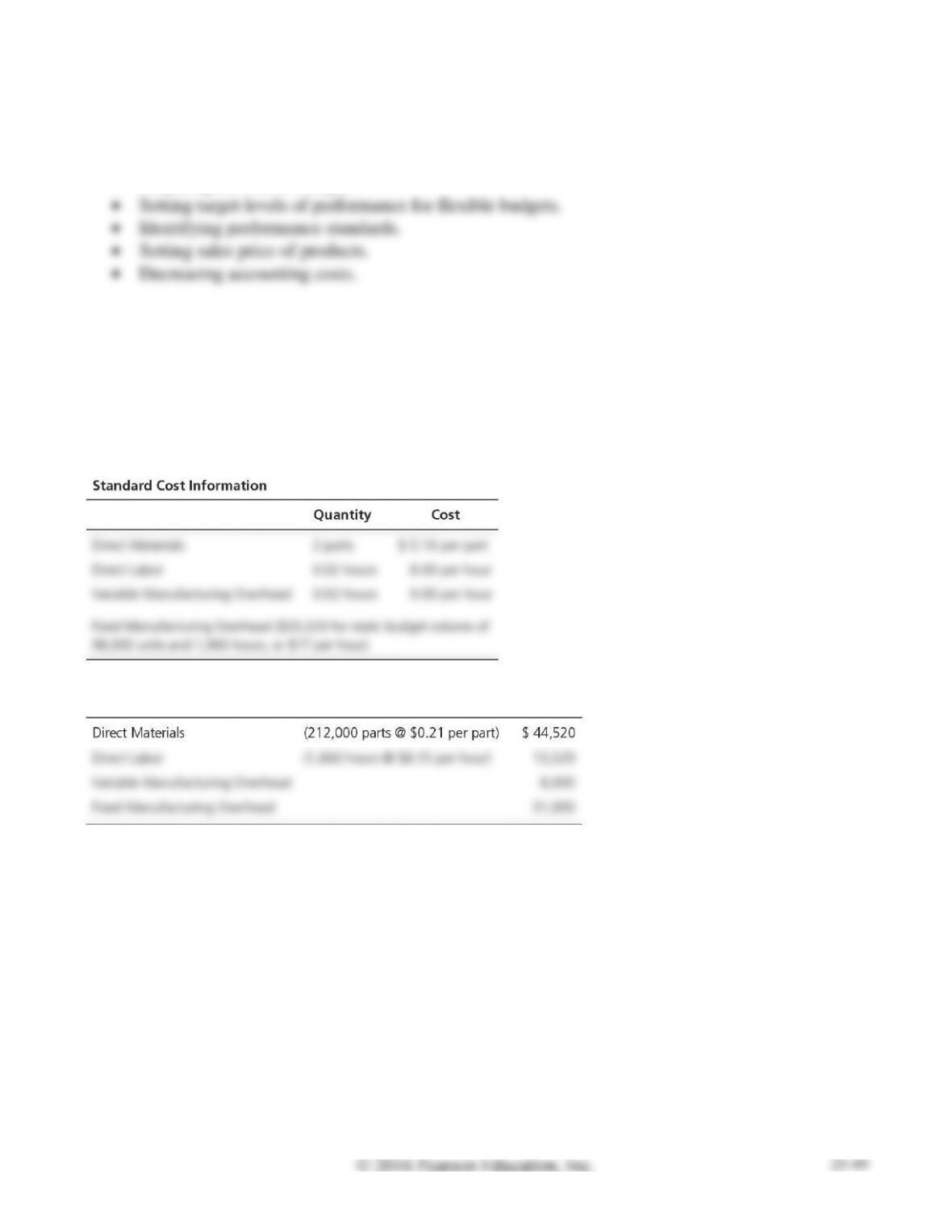

P23-27A Computing standard cost variances and reporting to management

Learning Objectives 3, 4, 5

1. DM Eff. Var. $640 F

Smart Hearing manufactures headphone cases. During September 2016, the company produced and sold

108,000 cases and recorded the following cost data:

Actual Cost Information

Requirements

1. Compute the cost and efficiency variances for direct materials and direct labor.

2. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the

fixed overhead cost and volume variances.

3. Smart Hearing’s management used better quality materials during September. Discuss the trade-off

between the two direct material variances.

SOLUTION

Requirement 1

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($0.21 per part – $0.16 per part)

×

212,000 parts

=

$10,600 U

=

×

=

$640 F

=

×

=

$249 U

=

×

=

$4,000 F

×

108,000 cases

=

216,000 parts

×

108,000 cases

=

2,160 DLHr

P23-27A, cont.

Requirement 2

VOH Cost Variance

=

Actual VOH

−

(SC × AQ)

=

$8,000

−

($9 per DLHr × 1,660 DLHr)

=

$6,940 F

=

×

$9 per DLHr

=

$4,500 F

=

$2,320 F

=

$3,400 F

×

2,160 DLHr

=

$36,720

Requirement 3

There may be trade-offs between the direct materials cost variance and the direct materials efficiency

variance. Decisions made by the purchasing manager may affect the direct materials efficiency variance

for the production manager. Perhaps Smart Hearing used better quality direct materials, indicated by the

fact that the $0.21 actual direct materials cost per part was greater than the $0.16 direct materials

P23-28A Computing and journalizing standard cost variances

Learning Objectives 3, 4, 5, 6

3. VOH Cost Var. $1,980 F

Juda manufactures coffee mugs that it sells to other companies for customizing with their own logos.

Juda prepares flexible budgets and uses a standard cost system to control manufacturing costs. The

standard unit cost of a coffee mug is based on static budget volume of 59,800 coffee mugs per month:

Actual cost and production information for July 2016 follows:

a. There were no beginning or ending inventory balances. All expenditures were on account.

Requirements

1. Compute the cost and efficiency variances for direct materials and direct labor.

2. Journalize the purchase and usage of direct materials and the assignment of direct labor, including

the related variances.

3. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the

fixed overhead cost and volume variances.

4. Journalize the actual manufacturing overhead and the allocated manufacturing overhead. Journalize

the movement of all production costs from Work-in-Process Inventory. Journalize the adjusting of

the Manufacturing Overhead account.

5. Juda intentionally hired more highly skilled workers during July. How did this decision affect the

cost variances? Overall, was the decision wise?

SOLUTION

Requirement 1

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($0.17 per lb. – $0.25 per lb.)

×

10,000 lbs.

=

$800 F

=

×

$0.25 per lb.

=

$625 F

=

×

=

$3,960 U

=

×

=

$1,365 U

×

62,500 mugs

=

12,500 lbs.

$29,700 total cost

198,000 minutes

=

$0.15 cost per minute

3 minutes per mug

×

62,500 mugs

=

187,500 minutes

P23-28A, cont.

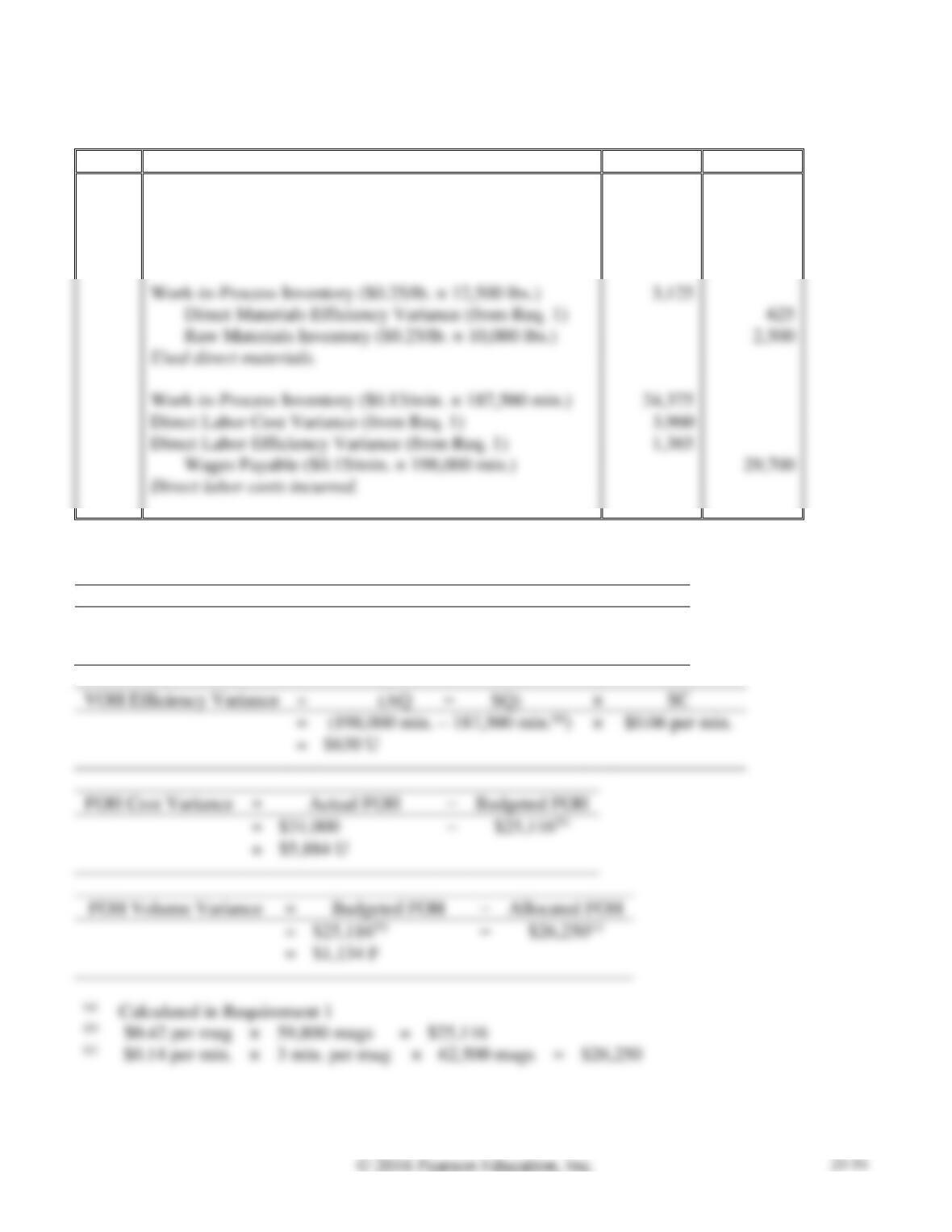

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Raw Materials Inventory ($0.25/lb. × 10,000 lbs.)

2,500

Direct Materials Cost Variance (from Req. 1)

800

Accounts Payable ($0.17/lb. × 10,000 lbs.)

1,700

Purchased direct materials.

3,125

Direct Materials Efficiency Variance (from Req. 1)

625

Raw Materials Inventory ($0.25/lb. × 10,000 lbs.)

2,500

Used direct materials.

Direct Labor Cost Variance (from Req. 1)

3,960

Direct Labor Efficiency Variance (from Req. 1)

1,365

Wages Payable ($0.15/min. × 198,000 min.)

Direct labor costs incurred.

Requirement 3

VOH Cost Variance

=

Actual VOH

−

(SC × AQ)

=

$9,900

−

($0.06 per min. × 198,000 min.)

=

$1,980 F

=

×

=

$630 U

=

$5,884 U

=

$1,134 F

×

59,800 mugs

=

$25,116

×

3 min. per mug

×

62,500 mugs

=

$26,250

P23-28A, cont.

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Manufacturing Overhead ($9,900 VOH + $31,000 FOH)

40,900

Various Accounts

40,900

Manufacturing overhead costs incurred.

37,500

Manufacturing Overhead

37,500

Manufacturing overhead costs allocated.

Finished Goods Inventory ($3,125 + $24,375 + $37,500)

65,000

65,000

Completed goods transferred.

Variable Overhead Efficiency Variance (from Req. 3)

Fixed Overhead Cost Variance (from Req. 3)

To adjust Manufacturing Overhead.

Requirement 5

Because Juda hired more skilled workers, the $0.15 actual direct labor cost per minute was greater than

the $0.13 direct labor standard cost per minute. Therefore, the direct labor cost variance was $3,960

unfavorable for the 62,500 mugs actually produced. Hiring more skilled direct labor workers could be

Note: Problem P23-28A must be completed before attempting Problem P23-29A.

P23-29A Preparing a standard cost income statement

Learning Objective 6

COGS at actual $72,300

Review your results from Problem P23-28A. Juda’s standard and actual sales price per mug is $3.

Prepare the standard cost income statement for July 2016.

SOLUTION

JUDA

Standard Cost Income Statement

For the Month Ended July 31, 2016

Sales Revenue at standard ($3/mug × 62,500 mugs)

$ 187,500

Cost of Goods Sold at standard (from P23-28A)

$ 65,000

Manufacturing Cost Variances (from P23-28A):

$ (800)

Cost of Goods Sold at actual

Gross Profit

Selling and Administrative Expenses

Operating Income / (Loss)

$ (4,800)

Problems (Group B)

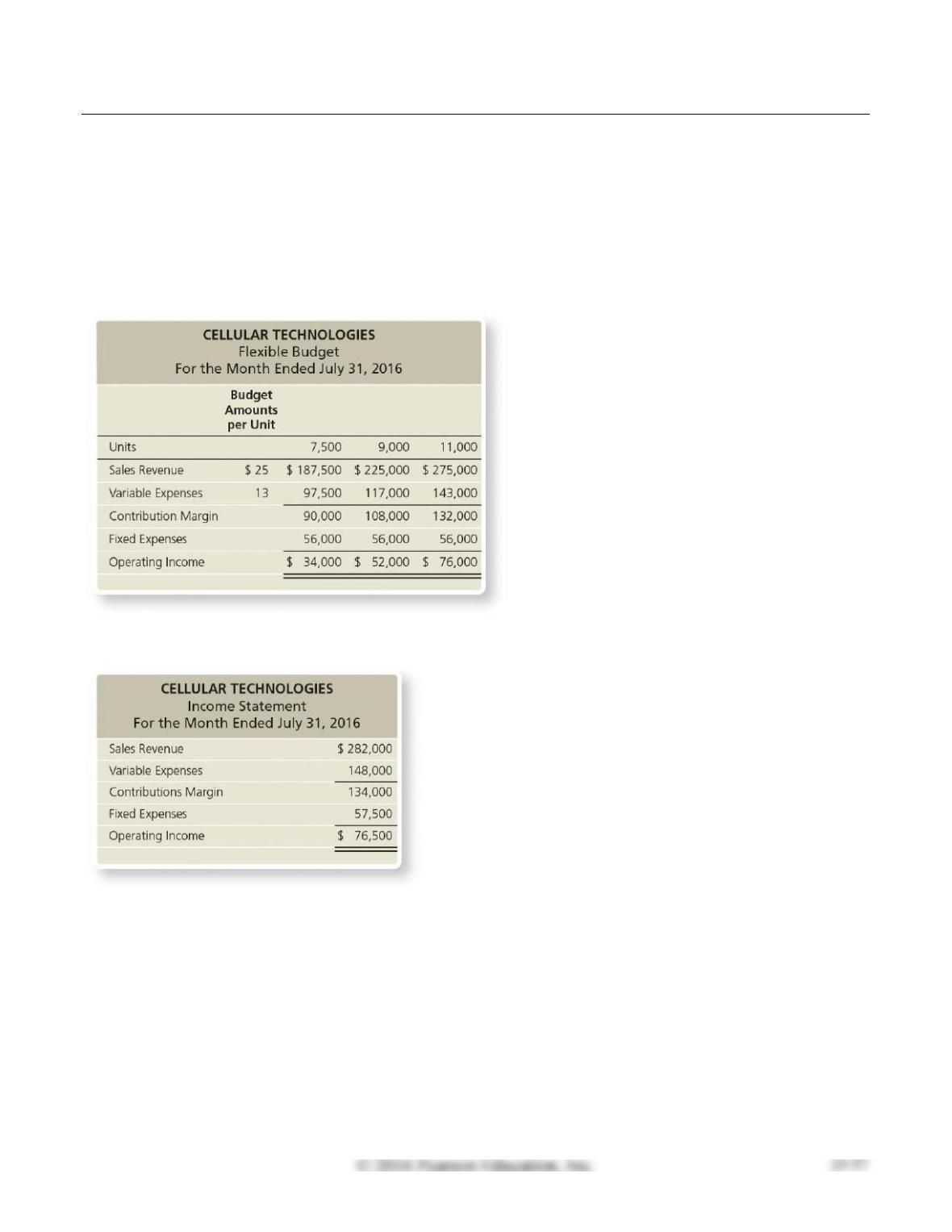

P23-30B Preparing a flexible budget performance report

Learning Objective 1

1. Static Bud. Var. for Op. Inc. $24,500 F

Cellular Technologies manufactures capacitors for cellular base stations and other communication

applications. The company’s July 2016 flexible budget shows output levels of 7,500, 9,000, and 11,000

units. The static budget was based on expected sales of 9,000 units.

The company sold 11,000 units during July, and its actual operating income was as follows:

Requirements

1. Prepare a flexible budget performance report for July 2016.

2. What was the effect on Cellular’s operating income of selling 2,000 units more than the static budget

level of sales?

3. What is Cellular’s static budget variance for operating income?

4. Explain why the flexible budget performance report provides more useful information to Cellular’s

managers than the simple static budget variance. What insights can Cellular’s managers draw from

this performance report?

SOLUTION

Requirement 1

CELLULAR TECHNOLOGIES

Flexible Budget Performance Report

For the Month Ended July 31, 2016

1

2

(1) – (3)

3

4

(3) – (5)

5

Budget

Amounts

per Unit

Actual

Results

Flexible

Budget

Variance

Flexible

Budget

Sales

Volume

Variance

Static

Budget

$ 282,000

$ 275,000

26,000

24,000

Requirement 2

Selling 2,000 units more than the static budget level of sales increased Cellular’s operating income by

$24,000 (which is the $24,000 favorable sales volume variance calculated in Requirement 1).

Requirement 3

P23-30B, cont.

Requirement 4

The static budget is prepared for only one level of sales volume—the 9,000 units expected to be sold—

and it doesn’t change after it is developed. The $24,500 favorable static budget variance is the difference

The primary reason for the favorable operating income results is that the 11,000 units actually sold was

more than the 9,000 units expected to be sold in the static budget. The overall $24,000 favorable sales

The overall $500 favorable flexible budget variance is the difference between actual operating income

($76,500) for the 11,000 units actually sold and expected operating income ($76,000) in the flexible

budget for the 11,000 units actually sold. Because the $7,000 favorable flexible budget variance for sales

revenue was $500 greater than the sum of the unfavorable flexible budget variances for variable

expenses ($5,000) and fixed expenses ($1,500), the overall flexible budget variance (for operating

income) was $500 favorable. The individual flexible budget variances arise because actual sales price

per unit, variable expense per unit, and fixed expenses were different from those expected for the 11,000

units actually sold.

• The $7,000 favorable flexible budget variance for sales revenue was favorable because the

$25.64 ($282,000 / 11,000 units, rounded) actual sales price per unit was higher than the $25 per

unit budgeted.

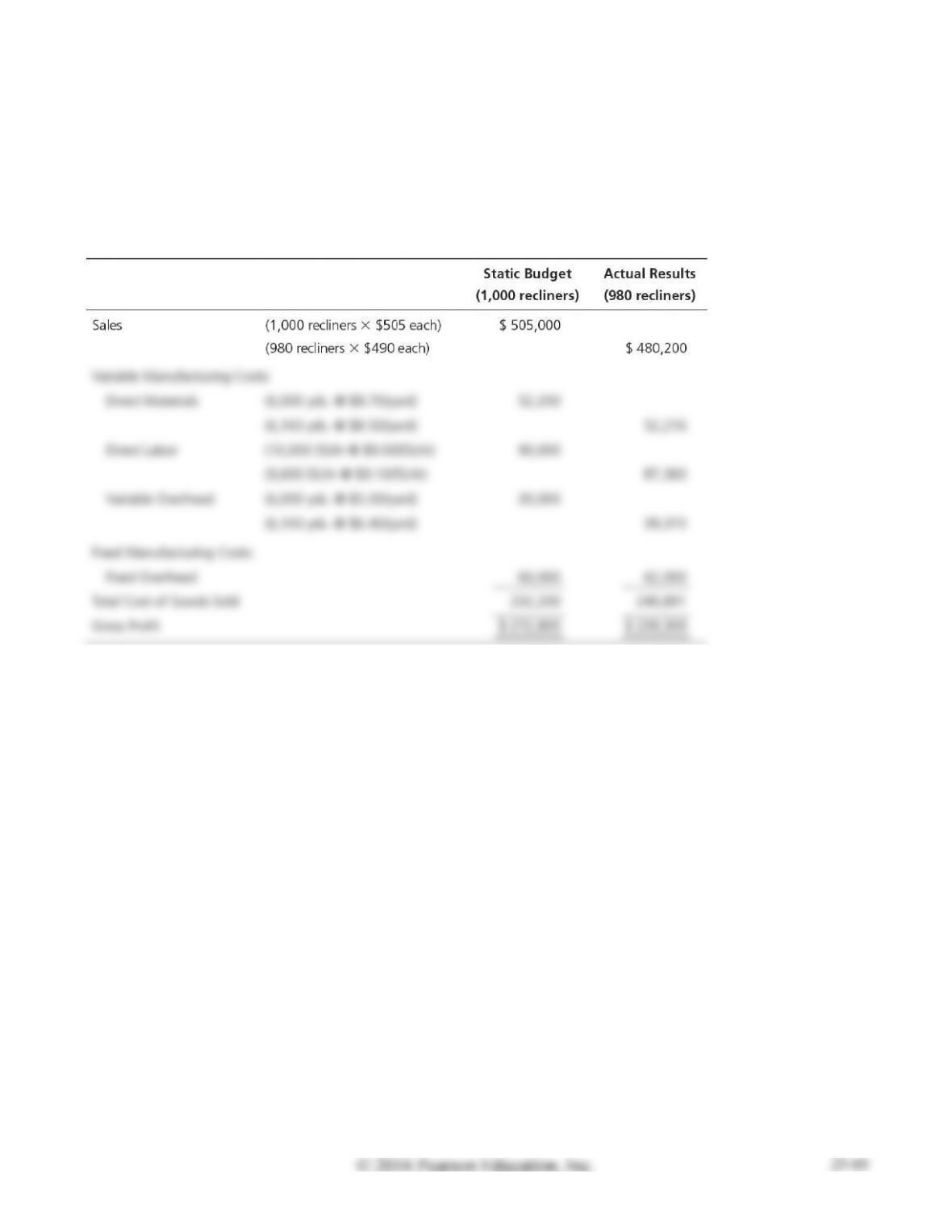

P23-31B Preparing a flexible budget and computing standard cost variances

Learning Objectives 1, 3, 4

2. VOH Eff. Var. $1,315 U

Root Recliners manufactures leather recliners and uses flexible budgeting and a standard cost system.

Root allocates overhead based on yards of direct materials. The company’s performance report includes

the following selected data:

Requirements

1. Prepare a flexible budget based on the actual number of recliners sold.

2. Compute the cost variance and the efficiency variance for direct materials and for direct labor. For

manufacturing overhead, compute the variable overhead cost, variable overhead efficiency, fixed

overhead cost, and fixed overhead volume variances. Round to the nearest dollar.

3. Have Root’s managers done a good job or a poor job controlling materials, labor, and overhead

costs? Why?

4. Describe how Root’s managers can benefit from the standard cost system.