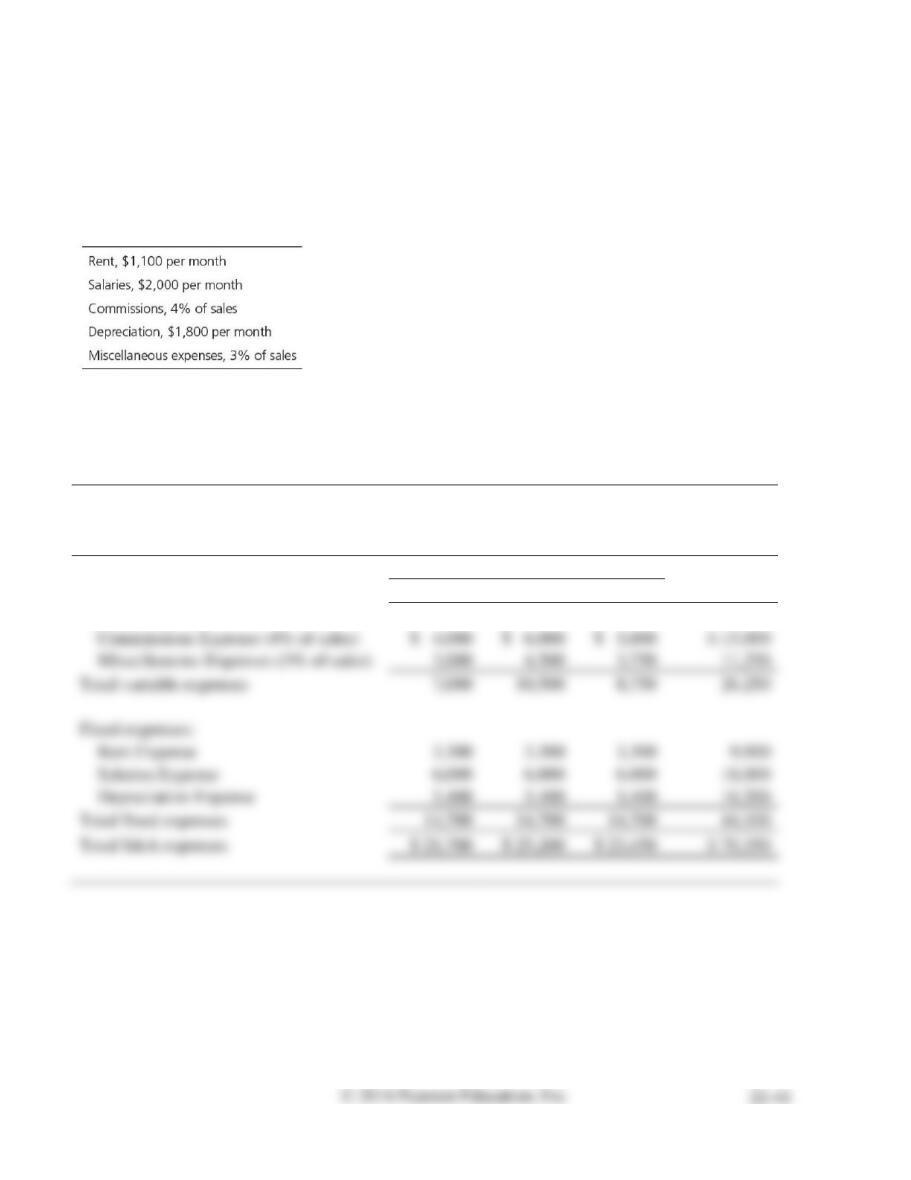

E22A-34 Preparing an operating budget—selling and administrative expense budget

Learning Objective 6

Appendix 22A

Qtr. ended Mar. 31 total S&A exp. $21,700

Consider the sales budget presented in Exercise E22A-33. Stewart’s selling and administrative expenses

include the following:

Prepare a selling and administrative expense budget for each of the three quarters of 2016 and totals for

the nine-month period.

SOLUTION

STEWART, INC.

Selling and Administrative Expense Budget

Nine Months Ended September 30, 2016

Quarter Ended

Nine-Month

Mar. 31

Jun. 30

Sep. 30

Total

Variable expenses:

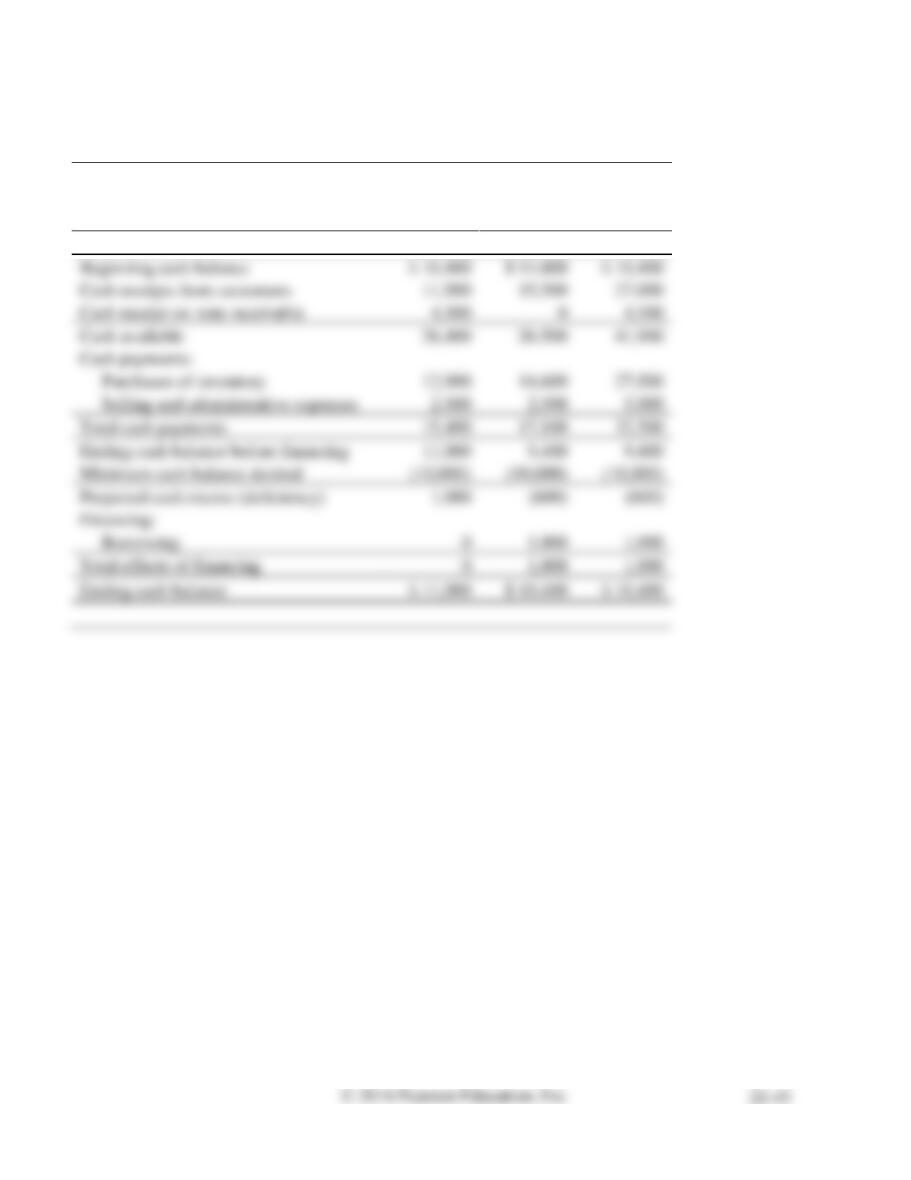

E22A-35 Preparing a financial budget—schedule of cash receipts and schedule of cash payments

Learning Objective 7

Appendix 22A

b. Sep. cash recpts. $119,795

Agua Frio is a distributor of bottled water. For each of the items, compute the amount of cash receipts or

payments Agua Frio will budget for September. The solution to one item may depend on the answer to

an earlier item.

SOLUTION

Part a

cash received

$17,000

$7,000

$3,000

$13,000

Part b

Aug.

Sept.

Budgeted cases to be sold

7,400

9,600

Sales price per case

× $13

× $13

Total sales

$ 96,200

$ 124,800

Aug.:

$96,200 total sales

$ 67,340 credit sales

$ 67,340 credit sales

$ 16,835 collected in Sept.

Sept.:

$124,800 total sales

30%

$ 37,440 cash sales

$87,360 credit sales

¾

$ 65,520 collected in Sept.

Sept.

Aug. credit sales—¼ collected in Sept.

$ 16,835

Sept. cash sales

37,440

Sept. credit sales—¾ collected in Sept.

Total cash receipts from customers

$ 119,795

E22A-35, cont.

Part c

Total sales

(from part b)

×

30%

×

½

=

Commissions and other selling

expenses paid in Sept.

Rent and property taxes – Sept.

Aug. —½ paid in Sept.

Sept. —½ paid in Sept.

Total cash paid for selling and administrative expenses

E22A-36 Preparing a financial budget—cash budget, sensitivity analysis

Learning Objectives 5, 7

Appendix 22A

1. Feb. ending cash bal. $10,400

Linstead Auto Parts, a family-owned auto parts store, began January with $10,400 cash. Management

forecasts that collections from credit customers will be $11,500 in January and $15,500 in February. The

store is scheduled to receive $4,500 cash on a business note receivable in January. Projected cash

payments include inventory purchases ($12,900 in January and $14,600 in February) and selling and

administrative expenses ($2,500 each month).

Linstead Auto Parts’s bank requires a $10,000 minimum balance in the store’s checking account. At

the end of any month when the account balance falls below $10,000, the bank automatically extends

credit to the store in multiples of $1,000. Linstead Auto Parts borrows as little as possible and pays back

loans in quarterly installments of $1,500, plus 3% APR interest on the entire unpaid principal. The first

payment occurs three months after the loan.

Requirements

1. Prepare Linstead Auto Parts’s cash budget for January and February.

2. How much cash will Linstead Auto Parts borrow in February if collections from customers that

month total $14,500 instead of $15,500?

SOLUTION

Requirement 1

LINSTEAD AUTO PARTS

Cash Budget

For the Two Months Ended February 28

January

February

Total

E22A-36, cont.

Requirement 2

Linstead Auto Parts will borrow $2,000 in February if collections from customers that month total

$14,500 instead of $15,500 because the ending cash balance before financing is $1,600 less than the

$10,000 minimum required.

February

Revised

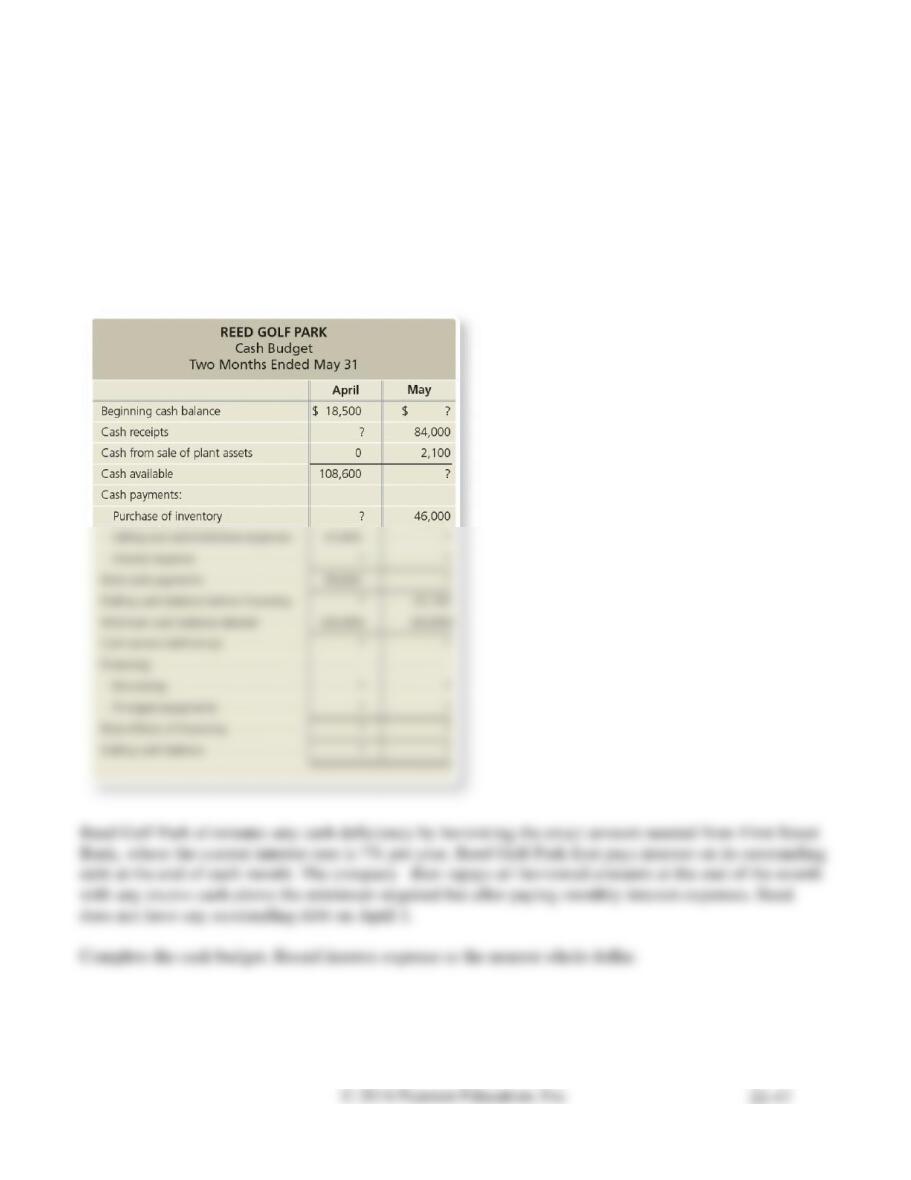

E22A-37 Preparing a financial budget—cash budget

Learning Objective 7

Appendix 22A

May ending cash bal. $20,000

You recently began a job as an accounting intern at Reed Golf Park. Your first task was to help prepare

the cash budget for April and May. Unfortunately, the computer with the budget file crashed, and you

did not have a backup or even a paper copy. You ran a program to salvage bits of data from the budget

file. After entering the following data in the budget, you may have just enough information to

reconstruct the budget.

SOLUTION

REED GOLF PARK

Cash Budget

Two Months Ended May 31

April

May

Beginning cash balance

$18,500

$ 20,000(i)

Cash receipts

90,100(a)

84,000

Cash from sale of plant assets

0

2,100

Cash available

108,600

106,100(j)

Cash payments:

Purchase of inventory

46,000

Selling and administrative expenses

Total cash payments

84,000(l)

Ending cash balance before financing

Minimum cash balance desired

Cash excess (deficiency)

Financing:

Borrowing

11,000(f)

Principal repayments

Total effects of financing

Ending cash balance

(a)

$108,600 − $18,500 = $90,100

(b)

No outstanding debt on April 1; thus, no interest expense and/or principal repayments in

April or May related to financing prior to April.

(c)

$99,600 − $47,600 − $0 = $52,000

(d)

$108,600 − $99,600 = $9,000

(e)

$9,000 − $20,000 = ($11,000)

(f)

Amount borrowed is the cash deficiency calculated in (e)

(g)

$11,000 − $0 = $11,000

(h)

$9,000 + $11000 = $20,000

(i)

The cash balance at the beginning of May is the cash balance at the end of April.

(j)

$20,000 + $84,000 + $2,100 = $106,100

(k)

$11,000 principal borrowed in April × 7% interest rate per year × 1/12 = $64

(l)

$106,100 − $22,100 = $84,000

(m)

$84,000 − $46,000 − $64 = $37,936

(n)

$22,100 − $20,000 = $2,100

(o)

No borrowing needed in May, since the ending cash balance before financing exceeds the

minimum cash balance desired.

(p)

The principal repayment in May is the cash excess over the minimum cash balance desired.

(q)

$0 − $2,100 = $(2,100)

E22A-38 Preparing a financial budget––budgeted balance sheet

Learning Objective 7

Appendix 22A

Cash $7,500

Use the following June actual ending balances and July 31, 2016, budgeted amounts for Ollies to

prepare a budgeted balance sheet for July 31, 2016.

a. June 30 Merchandise Inventory balance, $17,760

b. July purchase of Merchandise Inventory, $4,600, paid in cash

c. July payments of Accounts Payable, $8,700

d. June 30 Accounts Payable balance, $10,500

e. June 30 Furniture and Fixtures balance, $34,300; Accumulated Depreciation balance, $29,820

f. June 30 total stockholders’ equity balance, $28,120

g. July Depreciation Expense, $800

h. Cost of Goods Sold, 60% of sales

i. Other July expenses, including income tax, $5,000, paid in cash

j. June 30 Cash balance, $11,200

k. July budgeted sales, all on account, $12,200

l. June 30 Accounts Receivable balance, $5,180

m. July cash receipts from collections on account, $14,600

Hint: It may be helpful to trace the effects of each transaction on the accounting equation to determine

the ending balance of each account.

SOLUTION

OLLIES

Budgeted Balance Sheet

July 31, 2016

Assets

Current Assets:

Cash

$ 7,500

Accounts Receivable

Merchandise Inventory

Total Current Assets

$ 25,320

Property, Plant, and Equipment:

Furniture and Fixtures

Less: Accumulated Depreciation

Total Assets

$ 29,000

Current Liabilities:

Accounts Payable

$ 1,800

E22A-38, cont.

Cash

Accounts

Receivable

Merchandise

Inventory

Furniture

& Fixtures

Accumulated

Depreciation

Accounts

Payable

Stockholders’

Equity

June 30, Balance

$ 11,200

$ 5,180

$ 17,760

$ 34,300

$ (29,820)

$ 10,500

$ 28,120

Payments for

purchase of Inventory

(4,600)

4,600

Payments of

Accounts Payable

(8,700)

(8,700)

Depreciation Expense

Payments of

Other Expenses

(5,000)

Sales on account

12,200

12,200

Cash receipts

14,600

July 31, Balance

$ 7,500

$ 2,780

$ 15,040

$ 34,300

$ (30,620)

$ 1,800

$ 27,200

60%

×

$12,200 sales

=

$7,320 Cost of Goods Sold

Problems (Group A)

P22-39A Preparing an operating budget—sales, production, direct materials, direct labor,

overhead, COGS, and S&A expense budgets

Learning Objective 3

3. POHR $8

4. Adult bats COGS $60,690

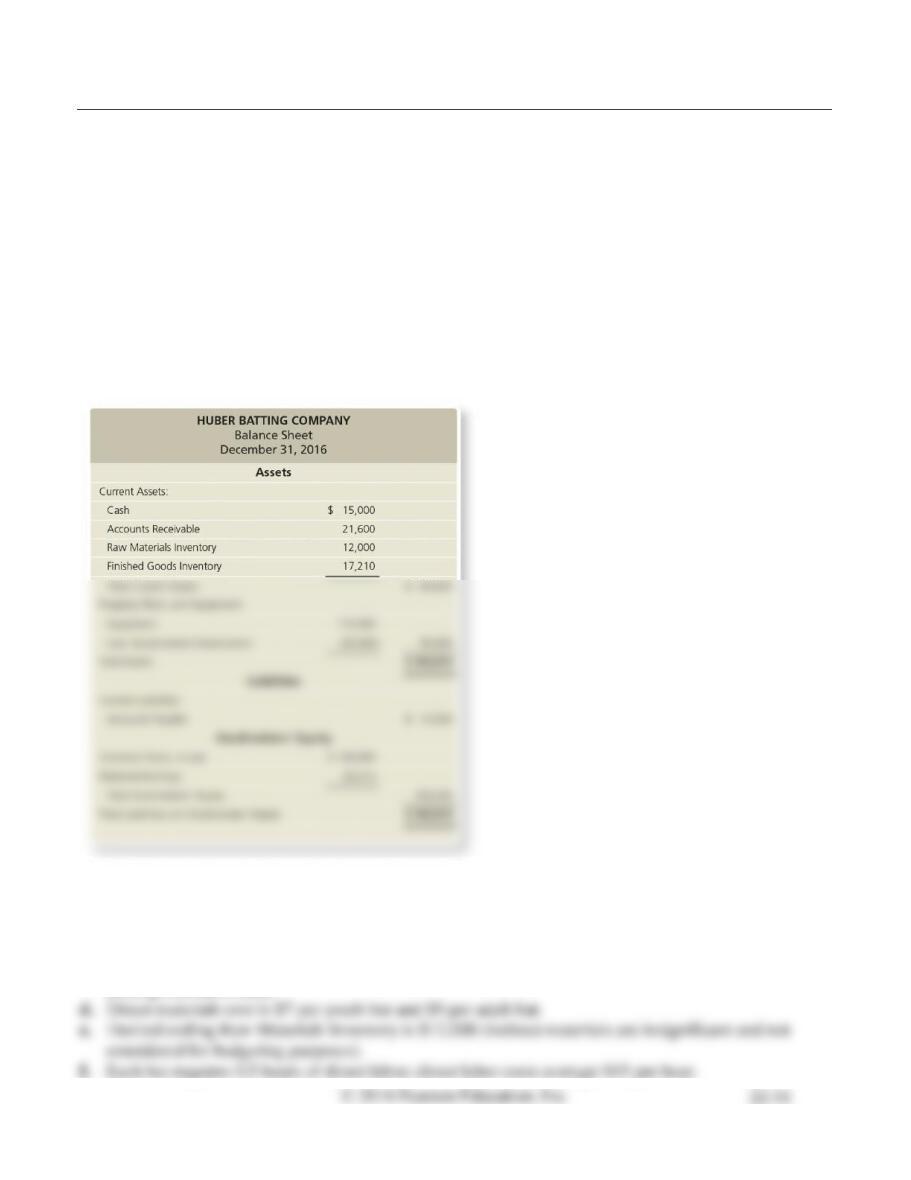

The Huber Batting Company manufactures wood baseball bats. Huber’s two primary products are a

youth bat, designed for children and young teens, and an adult bat, designed for high school and college-

aged players. Huber sells the bats to sporting goods stores, and all sales are on account. The youth bat

sells for $35; the adult bat sells for $65. Huber’s highest sales volume is in the first three months of the

year as retailers prepare for the spring baseball season. Huber’s balance sheet for December 31, 2016,

follows:

Other data for Huber Batting Company for the first quarter of 2017:

a. Budgeted sales are 1,300 youth bats and 3,100 adult bats.

b. Finished Goods Inventory on December 31 consists of 650 youth bats at $17 each and 440 adult bats

at $14 each.

c. Desired ending Finished Goods Inventory is 100 youth bats and 550 adult bats; FIFO inventory

costing method is used.

g. Variable manufacturing overhead is $0.50 per bat.

h. Fixed manufacturing overhead includes $600 per quarter in depreciation and $13,260 per quarter for

other costs, such as insurance and property taxes.

i. Fixed selling and administrative expenses include $14,000 per quarter for salaries; $3,000 per

quarter for rent; $2,000 per quarter for insurance; and $300 per quarter for depreciation.

j. Variable selling and administrative expenses include supplies at 3% of sales.

Requirements

1. Prepare Huber’s sales budget for the first quarter of 2017.

2. Prepare Huber’s production budget for the first quarter of 2017.

3. Prepare Huber’s direct materials budget, direct labor budget, and manufacturing over– head budget

for the first quarter of 2017. Round the predetermined overhead allocation rate to two decimal

places. The overhead allocation base is direct labor hours.

4. Prepare Huber’s cost of goods sold budget for the first quarter of 2017.

5. Prepare Huber’s selling and administrative expense budget for the first quarter of 2017.

SOLUTION

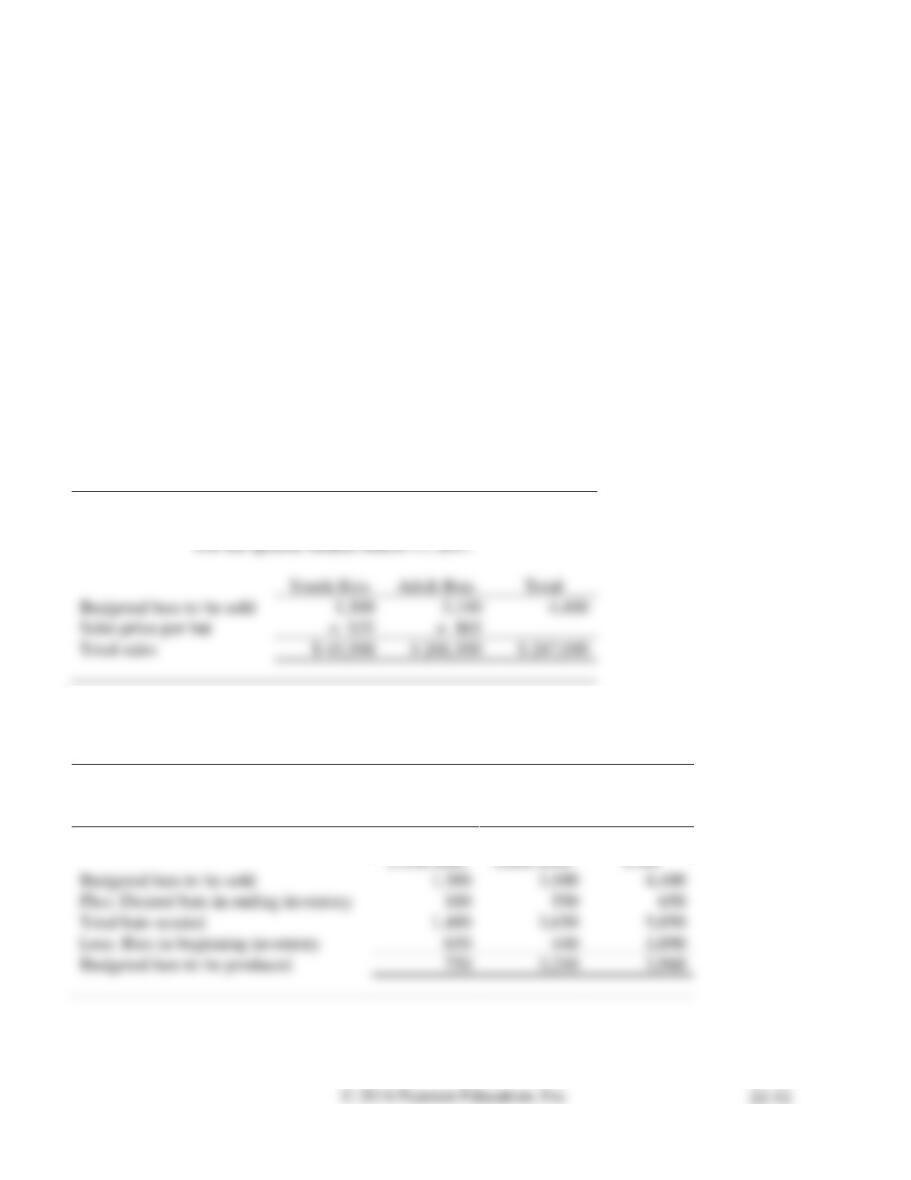

Requirement 1

HUBER BATTING COMPANY

Sales Budget

Budgeted bats to be sold

Sales price per bat

Total sales

Requirement 2

HUBER BATTING COMPANY

Production Budget

For the Quarter Ended March 31, 2017

Budgeted bats to be sold

Plus: Desired bats in ending inventory

Total bats needed

Less: Bats in beginning inventory

Budgeted bats to be produced

P22-39A, cont.

Requirement 3

HUBER BATTING COMPANY

Direct Materials Budget

For the Quarter Ended March 31, 2017

Youth Bats

Adult Bats

Total

Budgeted bats to be produced (from Req. 2)

Direct materials cost per bat

Direct materials needed for production

Plus: Desired direct materials in ending inventory

Total direct materials needed

Less: Direct materials in beginning inventory

Budgeted purchases of direct materials

HUBER BATTING COMPANY

Direct Labor Budget

For the Quarter Ended March 31, 2017

Youth Bats

Adult Bats

Total

Budgeted bats to be produced (from Req. 2)

Direct labor hours per bat

Direct labor cost per hour

Budgeted direct labor cost

P22-39A, cont.

Requirement 3, cont.

HUBER BATTING COMPANY

Manufacturing Overhead Budget

For the Quarter Ended March 31, 2017

Youth Bats

Adult Bats

Total

Budgeted bats to be produced (from Req. 2)

Variable overhead cost per bat

× $0.50

× $0.50

Budgeted variable overhead

Budgeted fixed overhead

Depreciation

Insurance and property taxes

Total budgeted fixed overhead

Budgeted manufacturing overhead costs

Direct labor hours (from DL Budget)

$15,840 / 1,980 DLHr

P22-39A, cont.

Requirement 4

Calculations for Cost of Goods Sold Budget:

Bats in

beginning inventory

×

Cost per bat

=

Cost of bats in

beginning inventory

Youth Bats:

650 bats

×

$17 per bat

=

$ 11,050

Adult Bats:

440 bats

×

$14 per bat

=

$ 6,160

=

Youth Bats:

=

Adult Bats:

=

Manufacturing cost per bat

Direct materials cost per bat

Direct labor cost per bat (0.5 DLHr/bat × $15/DLHr)

Manufacturing overhead cost per bat (0.5 DLHr/bat × $8/DLHr)

Total projected manufacturing cost per bat

Bats produced

and sold in

1st quarter of 2017

×

Manufacturing

cost per bat

=

Cost of bats

produced and sold

in 1st quarter of 2017

Youth Bats:

650 bats

×

$18.50 per bat

=

$12,025

Adult Bats:

2,660 bats

×

$20.50 per bat

=

$54,530

Beginning inventory

Total budgeted cost of goods sold

P22-39A, cont.

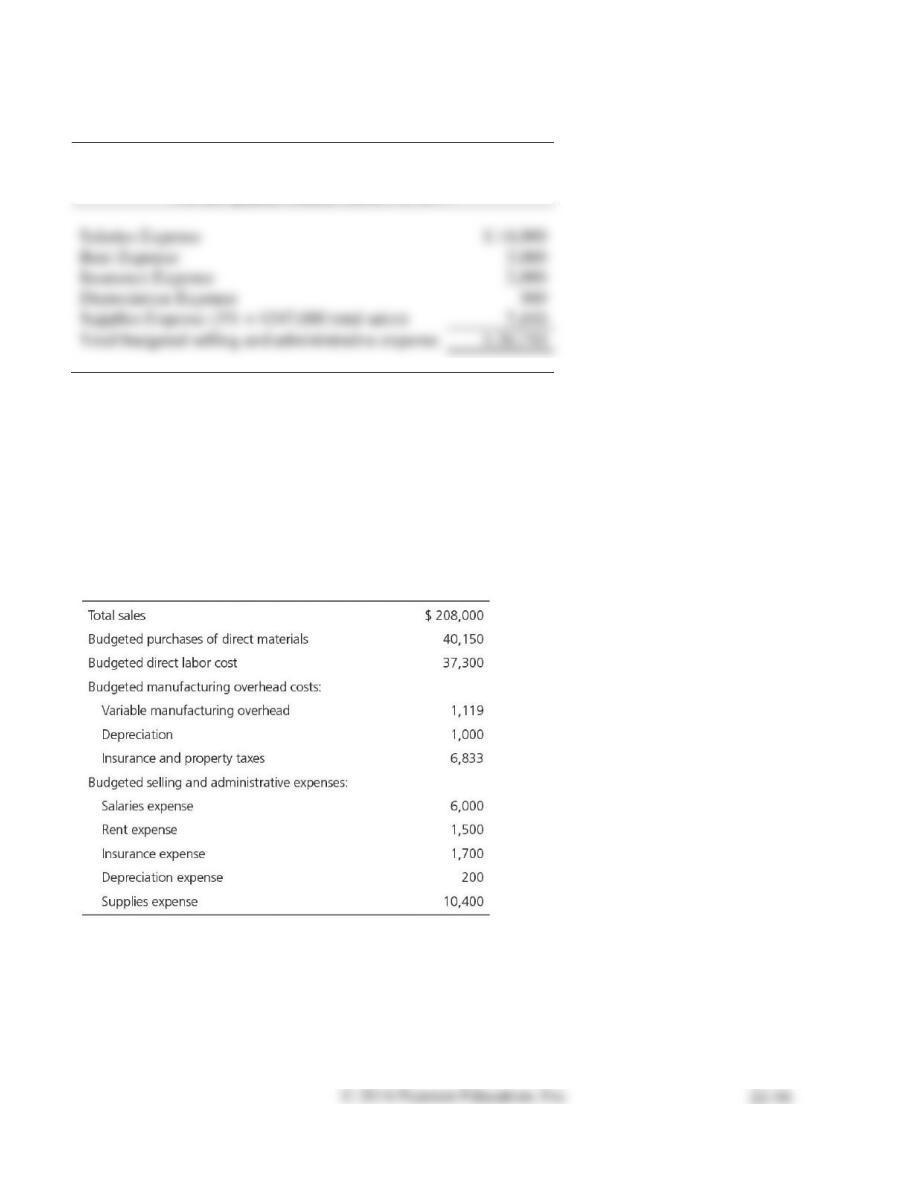

Requirement 5

HUBER BATTING COMPANY

Selling and Administrative Expense Budget

For the Quarter Ended March 31, 2017

Salaries Expense

Rent Expense

Insurance Expense

Depreciation Expense

Supplies Expense (3% × $247,000 total sales)

Total budgeted selling and administrative expense

P22-40A Preparing a financial budget—schedule of cash receipts, schedule of cash payments, cash

budget

Learning Objective 4

1. Total cash pmts. $187,127

2. Ending Cash bal. $25,573

Humble Company has provided the following budget information for the first quarter of 2016:

Additional data related to the first quarter of 2016 for Humble Company:

a. Capital expenditures include $37,000 for new manufacturing equipment to be purchased and paid in

the first quarter.

b. Cash receipts are 75% of sales in the quarter of the sale and 25% in the quarter following the sale.

c. Direct materials purchases are paid 50% in the quarter purchased and 50% in the next quarter.

d. Direct labor, manufacturing overhead, and selling and administrative costs are paid in the quarter

incurred.

e. Income tax expense for the first quarter is projected at $50,000 and is paid in the quarter incurred.

f. Humble Company expects to have adequate cash funds and does not anticipate borrowing in the first

quarter.

g. The December 31, 2015, balance in Cash is $40,000, in Accounts Receivable is $16,700, and in

Accounts Payable is $15,200.

Requirements

1. Prepare Humble Company’s schedule of cash receipts from customers and schedule of cash

payments for the first quarter of 2016.

2. Prepare Humble Company’s cash budget for the first quarter of 2016.

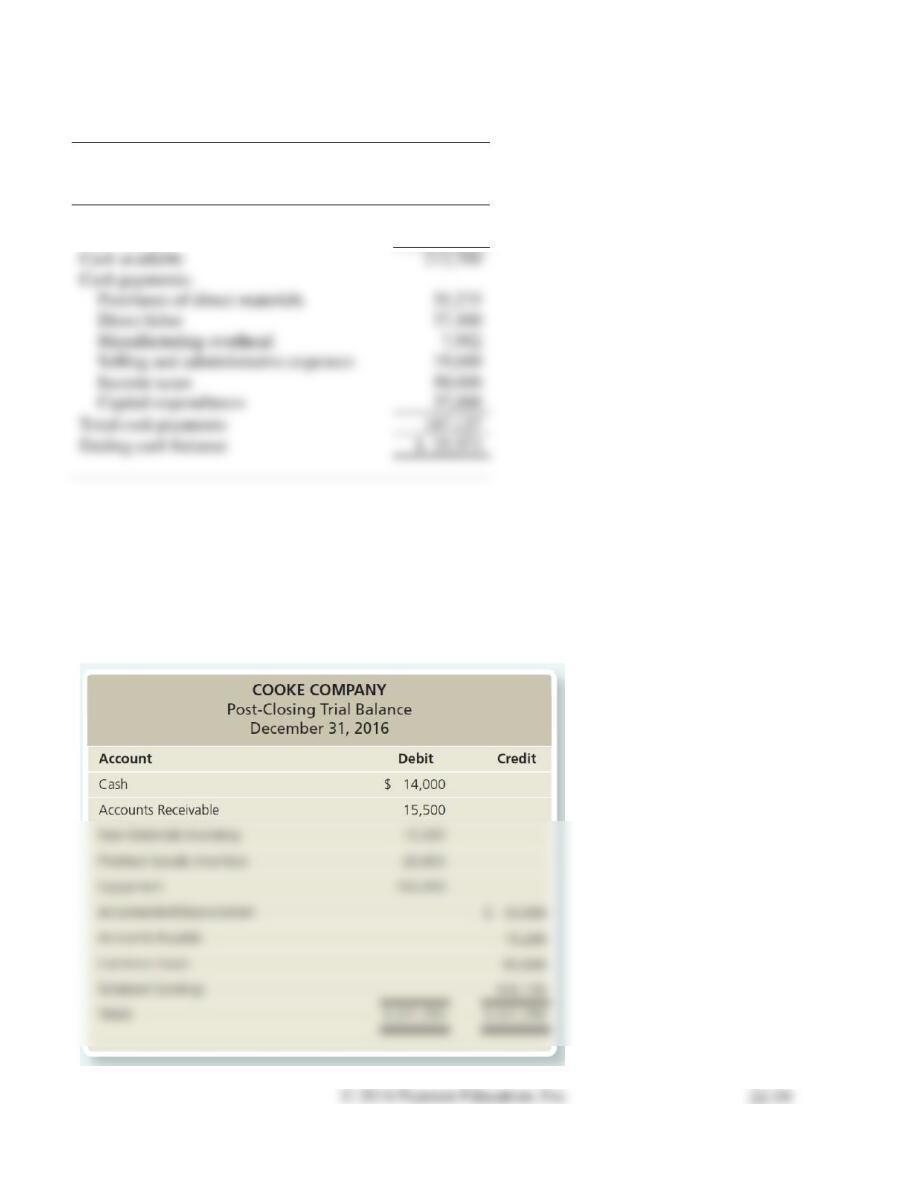

SOLUTION

Requirement 1

Schedule of Cash Receipts from Customers

1st Qtr. 2016

Total sales

Cash Receipts from Customers:

Accounts Receivable balance, December 31, 2015

Total cash receipts from customers

Accounts Receivable balance, March 31, 2016:

$52,000

P22-40A, cont.

Requirement 1, cont.

Schedule of Cash Payments

1st Qtr. 2016

Total direct materials purchases

$ 40,150

1st Qtr. 2016

Cash Payments

Direct Materials:

Accounts Payable balance, December 31, 2015

$ 15,200

1st Quarter—Direct materials purchases (50% paid in 1st Qtr.)

20,075

Total payments for direct materials

35,275

Direct Labor:

Total payments for direct labor

37,300

Manufacturing Overhead:

Variable manufacturing overhead

1,119

Insurance and property taxes

6,833

Total payments for manufacturing overhead

7,952

Selling and Administrative Expenses:

Salaries Expense

6,000

Rent Expense

1,500

Insurance Expense

1,700

Supplies Expense

10,400

Total payments for selling and administrative expenses

19,600

Income Taxes:

Total payments for income taxes

50,000

Capital Expenditures:

Total payments for capital expenditures

37,000

Total cash payments

Accounts Payable balance, March 31, 2016:

$20,075

P22-40A, cont.

Requirement 2

HUMBLE COMPANY

Cash Budget

For the Quarter Ended March 31, 2016

Beginning cash balance

$ 40,000

Cash receipts

172,700

Cash available

212,700

Cash payments:

Purchases of direct materials

Direct labor

Manufacturing overhead

Selling and administrative expenses

Income taxes

Capital expenditures

Total cash payments

187,127

Ending cash balance

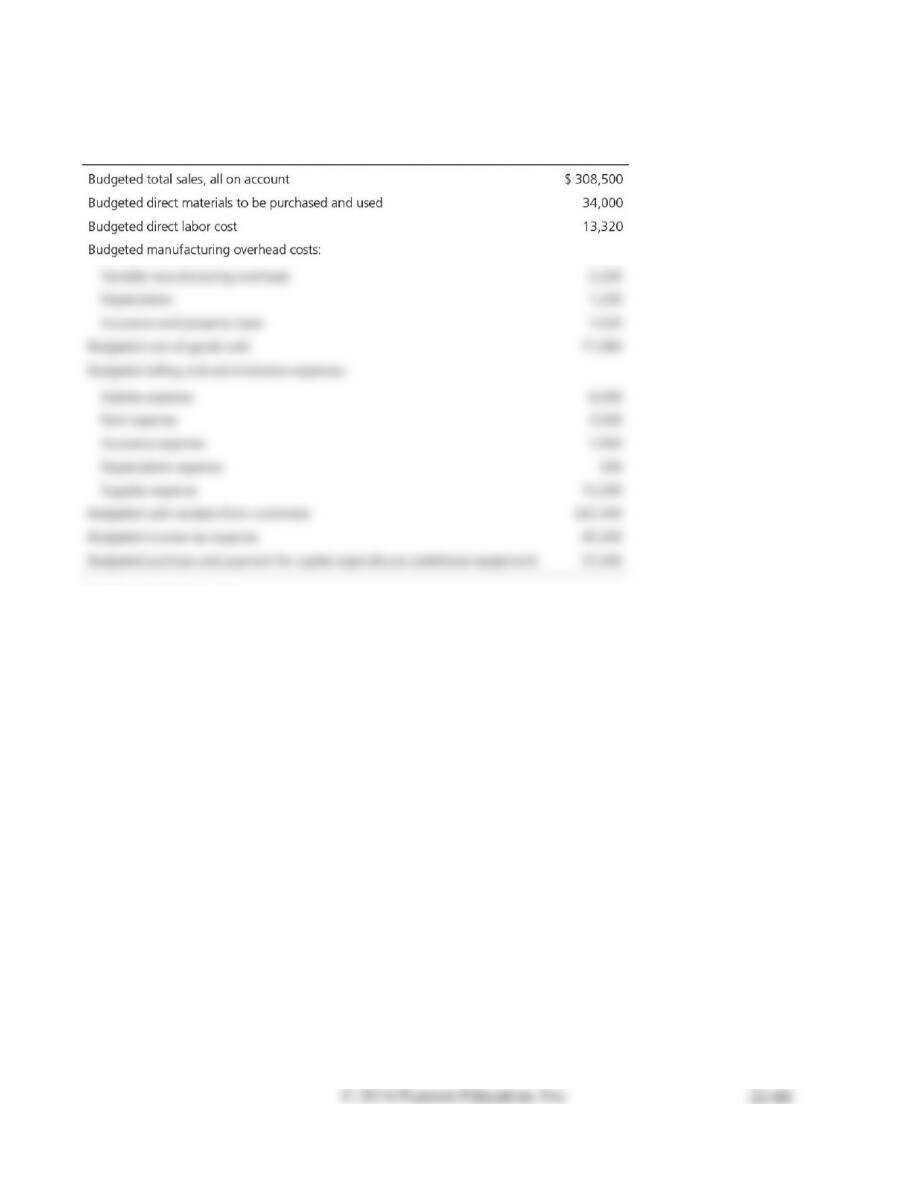

P22-41A Preparing a financial budget—budgeted income statement, balance sheet, and statement

of cash flows

Learning Objective 4

1. NI $166,300

2. FG inventory $6,650

Cooke Company has the following post-closing trial balance on December 31, 2016:

The company’s accounting department has gathered the following budgeting information for the first

quarter of 2017:

Additional information:

a. Direct materials purchases are paid 60% in the quarter purchased and 40% in the next quarter.

b. Direct labor, manufacturing overhead, selling and administrative costs, and income tax expense are

paid in the quarter incurred.

Requirements

1. Prepare Cooke Company’s budgeted income statement for the first quarter of 2017.

2. Prepare Cooke Company’s budgeted balance sheet as of March 31, 2017. Hint: Use the budgeted

statement of cash flows prepared in Requirement 3 to determine the Cash balance.

3. Prepare Cooke Company’s budgeted statement of cash flows for the first quarter of 2017.