SOLUTION

Requirement 1

COOKE COMPANY

Budgeted Income Statement

For the Quarter Ended March 31, 2017

P22-41A, cont.

Requirement 2

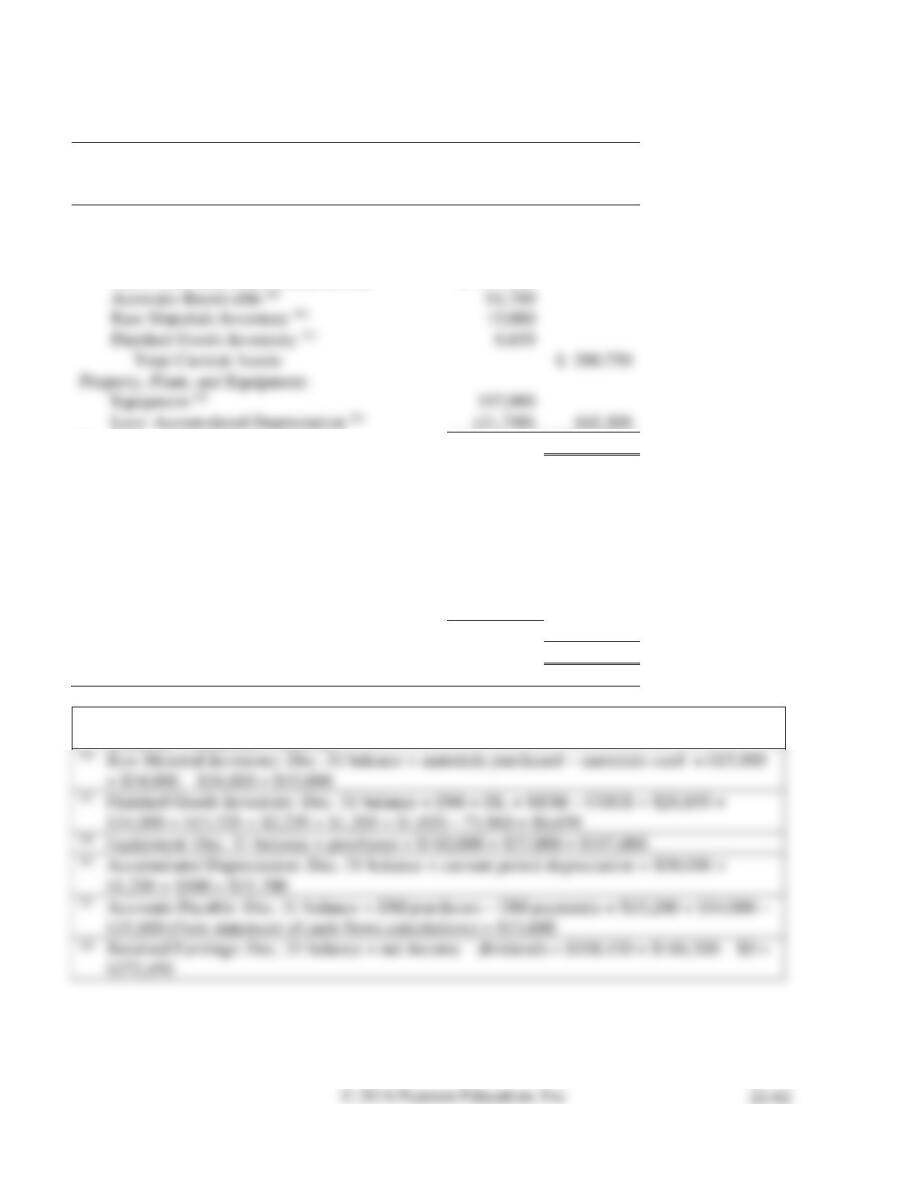

COOKE COMPANY

Budgeted Balance Sheet

March 31, 2017

Assets

Current Assets:

Cash (from statement of cash flows)

$ 117,400

Accounts Receivable (a)

61,700

Raw Materials Inventory (b)

15,000

Finished Goods Inventory (c)

6,650

Total Current Assets

$ 200,750

Property, Plant, and Equipment:

197,000

165,300

Total Assets

$ 366,050

Liabilities

Current Liabilities:

Accounts Payable (f)

$ 13,600

Stockholders’ Equity

Common Stock

$ 80,000

Retained Earnings (g)

272,450

Total Stockholders’ Equity

352,450

Total Liabilities and Stockholders’ Equity

$366,050

(a)

Accounts Receivable: Dec. 31 balance + total sales – customer payments = $15,500 +

$308,500 – $262,300 = $61,700

(b)

(c)

$35,600 (from statement of cash flows calculations) = $13,600

(g)

P22-41A, cont.

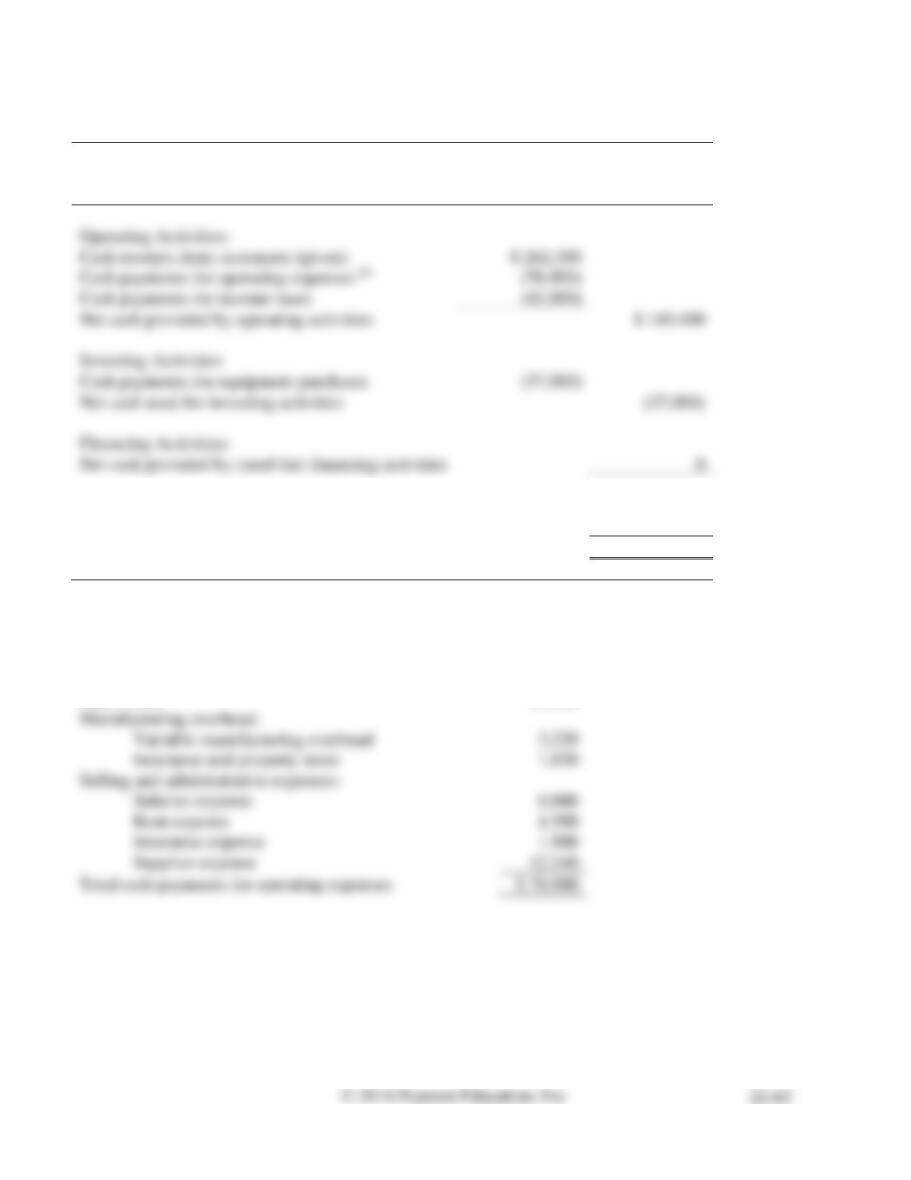

Requirement 3

COOKE COMPANY

Budgeted Statement of Cash Flows

For the Quarter Ended March 31, 2017

Operating Activities:

Cash receipts from customers (given)

Cash payments for income taxes

Net cash provided by operating activities

$ 140,400

Investing Activities:

Cash payments for equipment purchases

Net cash used for investing activities

Financing Activities:

Net cash provided by (used for) financing activities

Net increase in cash

103,400

Cash balance, January 1, 2017

14,000

Cash balance, March 31, 2017

$ 117,400

(h)

Cash payments for operating expenses:

Direct materials payments: Dec. 31 AP balance + 60% of

1st quarter purchases = $15,200 + (60% × $34,000)

$ 35,600

Direct labor

13,320

Manufacturing overhead:

Selling and administrative expenses:

12,340

Total cash payments for operating expenses

$ 76,900

1. 3rd Qtr. DM purchases $7,380

4th Qtr. total cash pmts. (before interest) $32,998

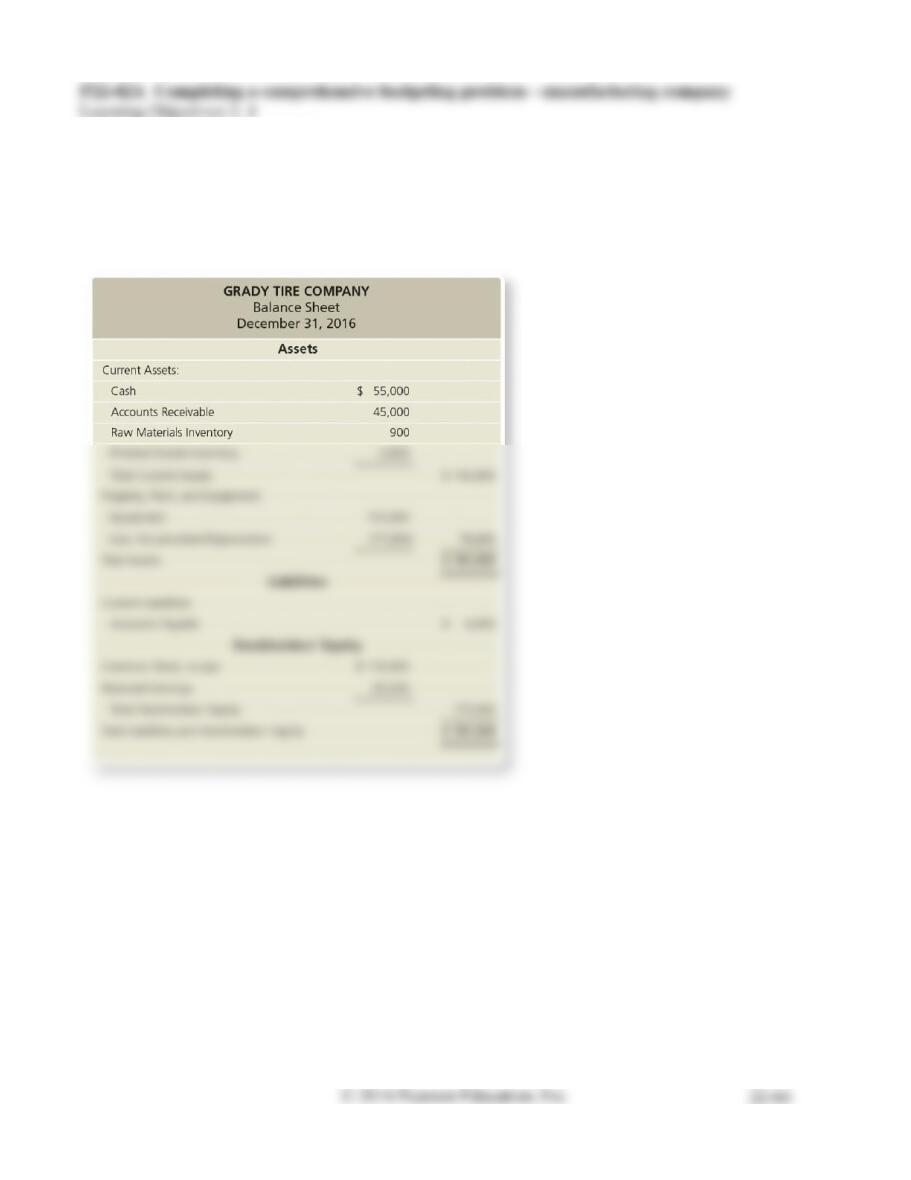

The Grady Tire Company manufactures racing tires for bicycles. Grady sells tires for $60 each. Grady is

planning for the next year by developing a master budget by quarters. Grady’s balance sheet for

December 31, 2016, follows:

d. Direct materials cost is $9 per tire.

e. Desired ending Raw Materials Inventory is 20% of the next quarter’s direct materials needed for

production; desired ending inventory for December 31 is $900; indirect materials are insignificant

and not considered for budgeting purposes.

f. Each tire requires 0.4 hours of direct labor; direct labor costs average $10 per hour.

g. Variable manufacturing overhead is $4 per tire.

h. Fixed manufacturing overhead includes $3,000 per quarter in depreciation and $1,770 per quarter for

other costs, such as utilities, insurance, and property taxes.

i. Fixed selling and administrative expenses include $7,500 per quarter for salaries; $3,000 per quarter

for rent; $1,650 per quarter for insurance; and $2,000 per quarter for depreciation.

n. Direct labor, manufacturing overhead, and selling and administrative costs are paid in the quarter

incurred.

o. Income tax expense is projected at $4,000 per quarter and is paid in the quarter incurred.

p. Grady desires to maintain a minimum cash balance of $50,000 and borrows from the local bank as

needed in increments of $1,000 at the beginning of the quarter; principal repayments are made at the

beginning of the quarter when excess funds are available and in increments of $1,000; interest is 8%

per year and paid at the beginning of the quarter based on the amount outstanding from the previous

quarter.

Requirements

1. Prepare Grady’s operating budget and cash budget for 2017 by quarter. Required schedules and

budgets include: sales budget, production budget, direct materials budget, direct labor budget,

manufacturing overhead budget, cost of goods sold budget, selling and administrative expense

SOLUTION

Requirement 1

GRADY TIRE COMPANY

Sales Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted tires to be sold

700

750

800

850

3,100

Sales price per tire

× $60

× $60

× $60

× $60

× $60

Total sales

$ 42,000

$ 45,000

$ 48,000

$ 51,000

$ 186,000

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted tires to be sold

700

750

800

850

3,100

(20% of next quarter’s sales)

150

160

170

180

180

Total tires needed

850

910

970

1,030

3,280

Less: Tires in beginning inventory

100

150

160

170

100

Budgeted tires to be produced

750

760

810

860

3,180

P22-42A, cont.

Requirement 1, cont.

GRADY TIRE COMPANY

Direct Materials Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted tires to be produced

Direct materials cost per tire

Direct materials needed for production

Plus: Desired direct materials in ending inventory

(20% of next quarter’s needed for production)

Total direct materials needed

Less: Direct materials in beginning inventory

Budgeted purchases of direct materials

GRADY TIRE COMPANY

Direct Labor Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted tires to be produced

750

760

810

860

3,180

Direct labor hours per tire

× 0.4

× 0.4

× 0.4

× 0.4

× 0.4

Direct labor hours needed for production

300

304

324

344

1,272

Direct labor cost per hour

Budgeted direct labor cost

P22-42A, cont.

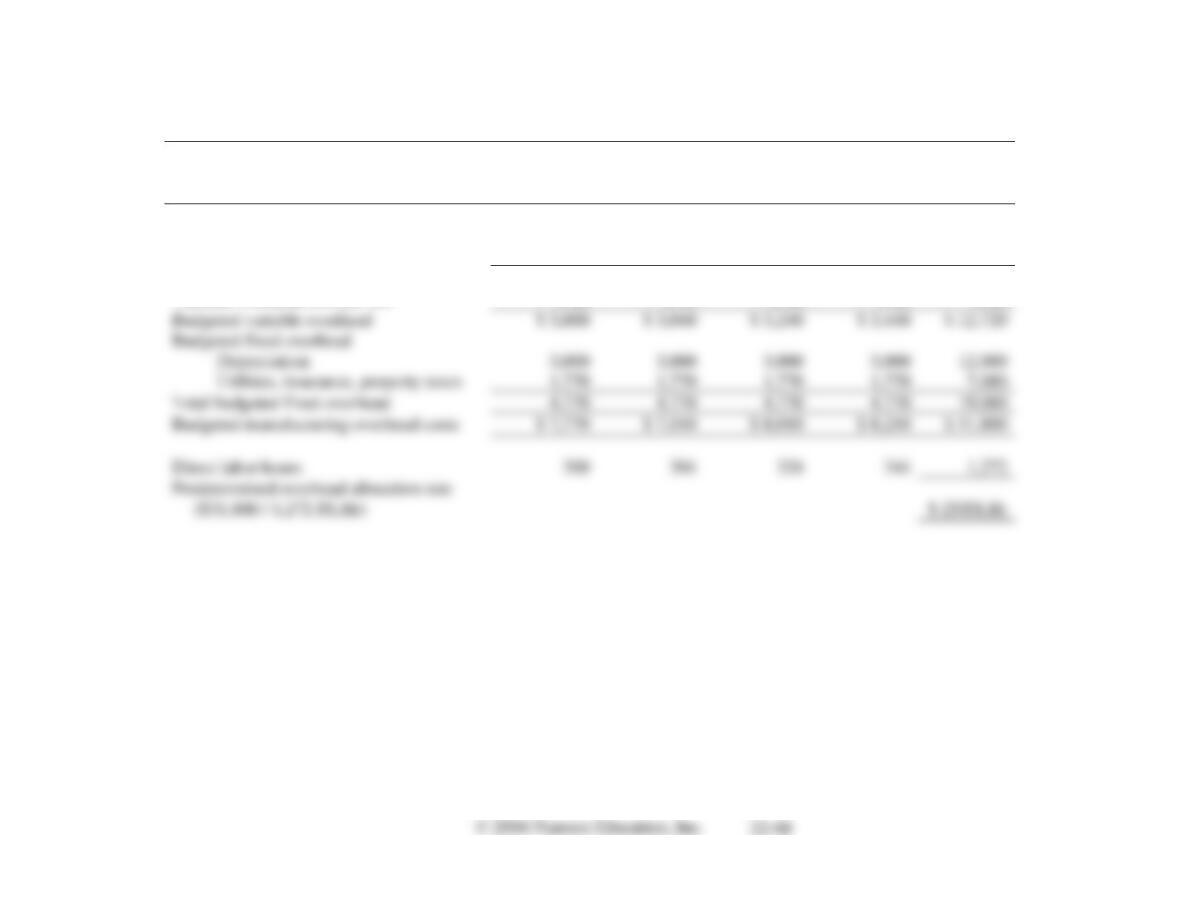

Requirement 1, cont.

GRADY TIRE COMPANY

Manufacturing Overhead Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted tires to be produced

750

760

810

860

3,180

Variable overhead cost per tire

× $4

× $4

× $4

× $4

× $4

Budgeted variable overhead

$ 12,720

Budgeted fixed overhead

Depreciation

Utilities, insurance, property taxes

7,080

Total budgeted fixed overhead

Budgeted manufacturing overhead costs

$ 31,800

Direct labor hours

300

304

324

344

1,272

Predetermined overhead allocation rate

($31,800 / 1,272 DLHr)

P22-42A, cont.

Requirement 1, cont.

Calculations for Cost of Goods Sold Budget:

Year ended December 31, 2017:

Direct materials cost per tire

$ 9.00

Direct labor cost per tire (0.4 DLHr/tire × $10/DLHr)

4.00

Manufacturing overhead cost per tire (0.4 DLHr/tire × $25/DLHr)

10.00

Total projected manufacturing cost per tire

$ 23.00

Beginning inventory, 100 tires at $26 each

Tires produced and sold in 2017 at $23 each

Total budgeted cost of goods sold

P22-42A, cont.

Requirement 1, cont.

GRADY TIRE COMPANY

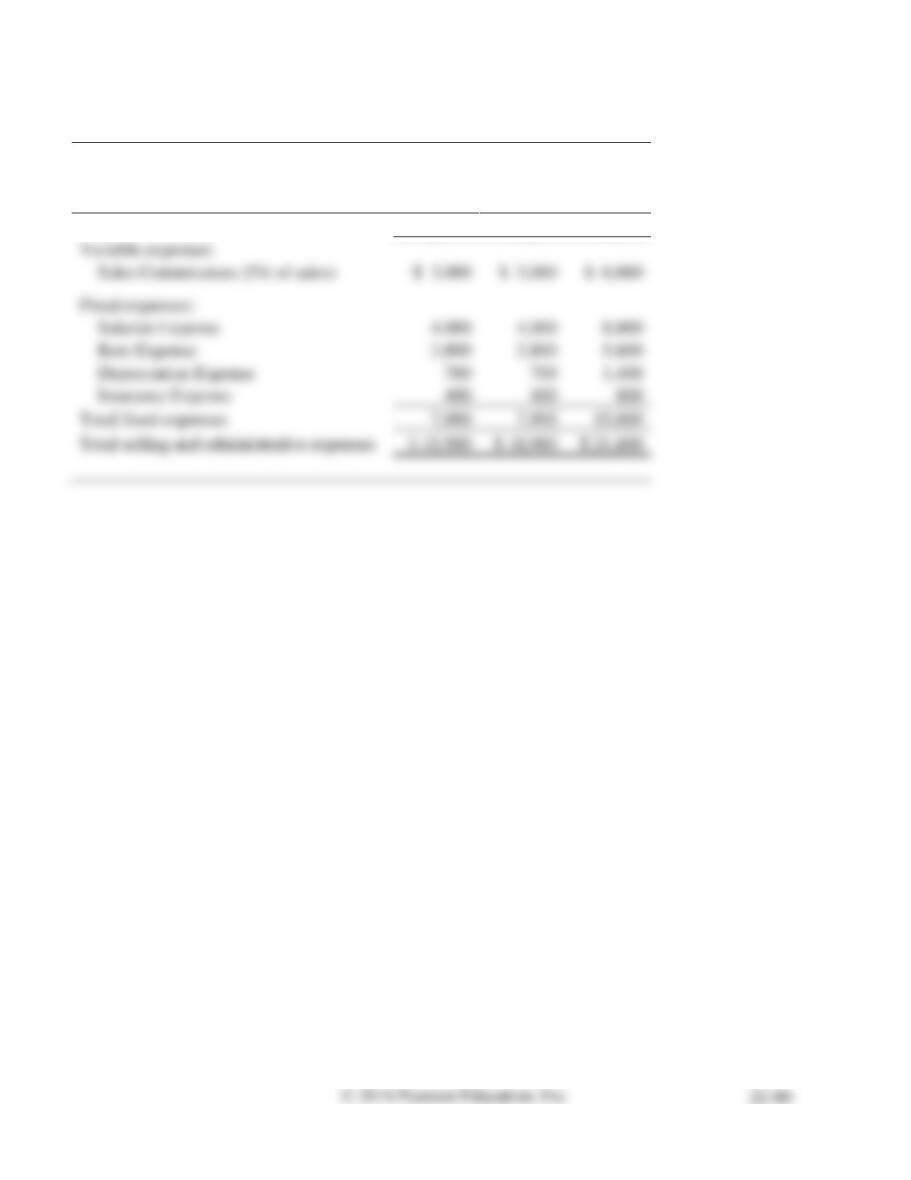

Selling and Administrative Expense Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Salaries Expense

Rent Expense

Insurance Expense

Depreciation Expense

Supplies Expense (2% of sales)

Total budgeted selling and administrative expense

P22-42A, cont.

Requirement 1, cont.

Schedule of Cash Receipts from Customers

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Total sales

$ 42,000

$ 45,000

$ 48,000

$ 51,000

$ 186,000

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Cash Receipts from Customers:

Accounts Receivable balance, December 31, 2016

$ 45,000

8,820

$ 20,580

9,450

$ 22,050

$ 23,520

Total cash receipts from customers

$ 66,420

$ 43,530

$ 46,530

$ 49,530

$ 206,010

Accounts Receivable balance, December 31, 2017:

P22-42A, cont.

Requirement 1, cont.

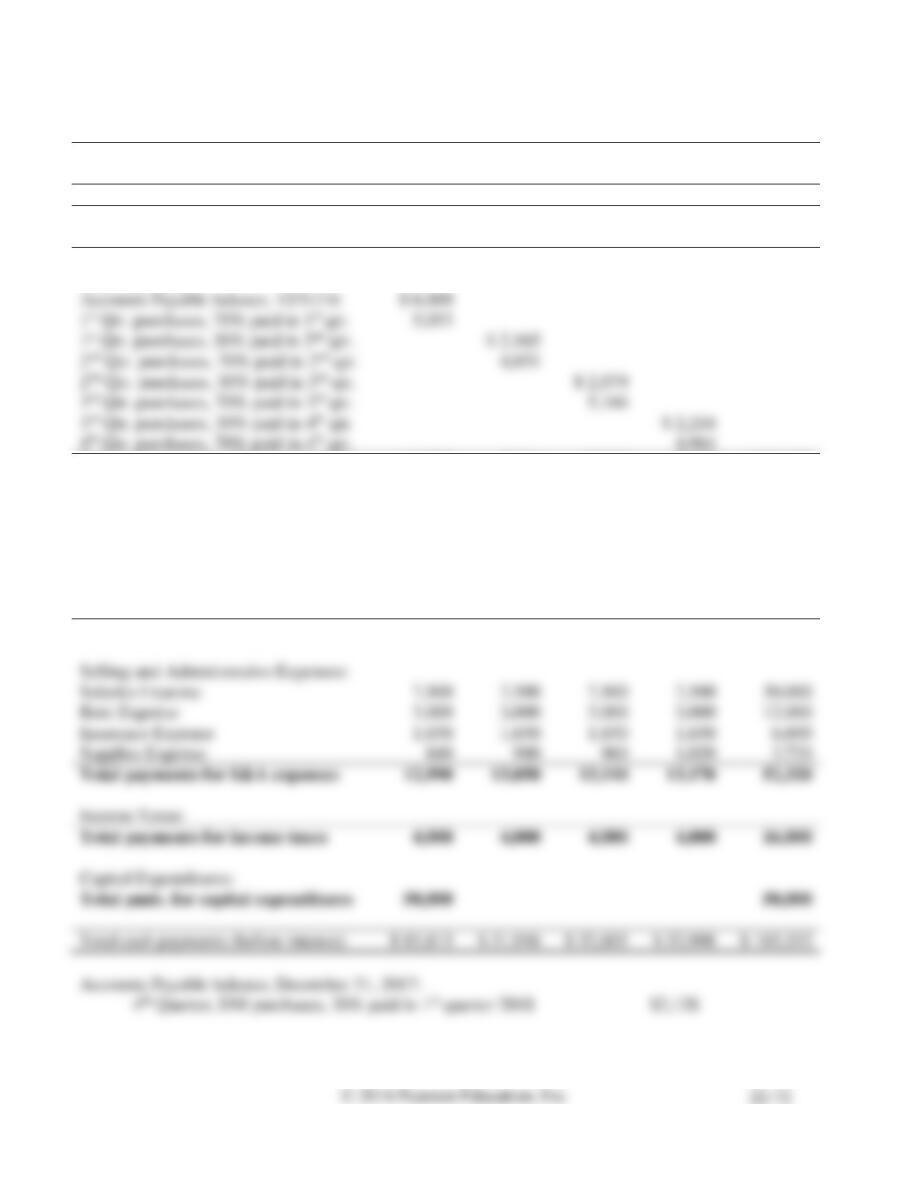

Schedule of Cash Payments

1st Qtr.

2nd Qtr.

3rd Qtr.

4th Qtr.

Total

Total direct materials purchases

$ 7,218

$ 6,930

$ 7,380

$ 7,092

$ 28,620

1st Qtr.

2nd Qtr.

3rd Qtr.

4th Qtr.

Total

Cash Payments

Direct Materials:

Accounts Payable balance, 12/31/16

$ 6,000

5,053

$ 2,165

4,851

$ 2,079

5,166

$ 2,214

4,964

Total payments for direct materials

11,053

7,016

7,245

7,178

$ 32,492

Direct Labor:

Total payments for direct labor

3,000

3,040

3,240

3,440

12,720

Manufacturing Overhead:

Variable manufacturing overhead

3,000

3,040

3,240

3,440

12,720

Utilities, insurance, property taxes

1,770

1,770

1,770

1,770

7,080

Total payments for mfg. overhead

4,770

4,810

5,010

5,210

19,800

Selling and Administrative Expenses:

Salaries Expense

7,500

7,500

7,500

7,500

30,000

Rent Expense

3,000

3,000

3,000

3,000

12,000

Insurance Expense

1,650

1,650

1,650

1,650

6,600

Supplies Expense

1,020

3,720

Total payments for S&A expenses

12,990

13,050

13,110

13,170

52,320

Income Taxes:

Total payments for income taxes

4,000

4,000

4,000

4,000

16,000

Capital Expenditures:

Total pmts. for capital expenditures

50,000

50,000

Total cash payments (before interest)

Accounts Payable balance, December 31, 2017:

$2,128

P22-42A, cont.

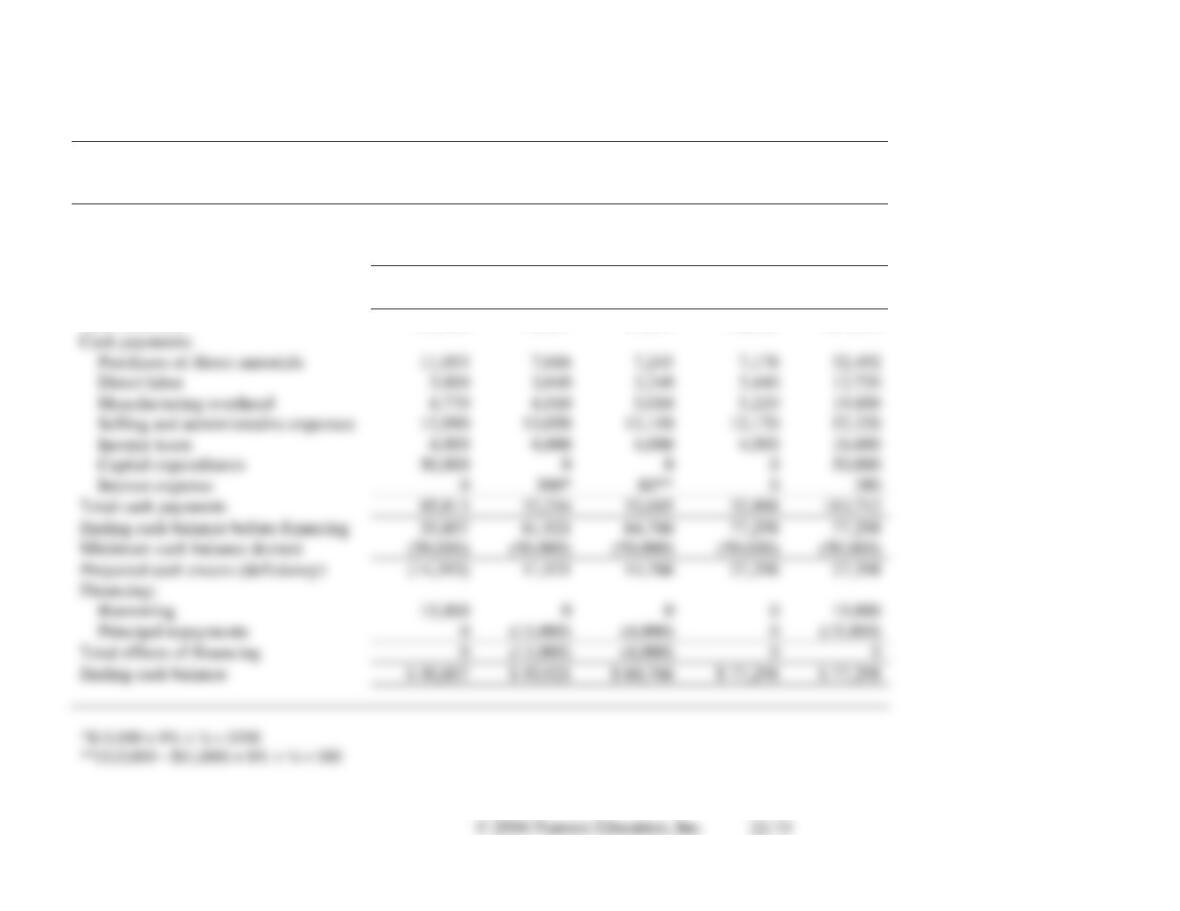

Requirement 1, cont.

GRADY TIRE COMPANY

Cash Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Beginning cash balance

$ 55,000

$ 50,607

$ 50,921

$ 60,766

$ 55,000

Cash receipts

66,420

43,530

46,530

49,530

206,010

Cash available

121,420

94,137

97,451

110,296

261,010

Cash payments:

Purchases of direct materials

11,053

32,492

Direct labor

12,720

Manufacturing overhead

19,800

Selling and administrative expenses

12,990

13,050

13,110

13,170

52,320

Income taxes

16,000

Capital expenditures

50,000

0

0

50,000

Interest expense

Total cash payments

85,813

32,216

32,685

32,998

183,712

Ending cash balance before financing

35,607

61,921

64,766

77,298

77,298

Minimum cash balance desired

(50,000)

(50,000)

Projected cash excess (deficiency)

(14,393)

11,921

14,766

27,298

27,298

Financing:

Borrowing

15,000

0

0

15,000

Principal repayments

Total effects of financing

Ending cash balance

$ 50,607

$ 50,921

$ 60,766

$ 77,298

$ 77,298

P22-42A, cont.

Requirement 2

GRADY TIRE COMPANY

Budgeted Income Statement

For the Year Ended December 31, 2017

Sales Revenue

$ 186,000

Cost of Goods Sold

Gross Profit

Selling and Administrative Expenses

Operating Income

Interest Expense

380

Income before Income Taxes

Income Tax Expense

Net Income

$ 37,700

GRADY TIRE COMPANY

Budgeted Balance Sheet

December 31, 2017

Assets

Current Assets:

Cash

$ 77,298

Accounts Receivable

24,990

Raw Materials Inventory

Finished Goods Inventory (180 tires at $23 each)

Total Current Assets

Property, Plant, and Equipment:

Equipment ($155,000 + $50,000)

Less: Accumulated Depreciation ($77,000 + $12,000 + $8,000)

108,000

Total Assets

Liabilities

Current Liabilities:

Accounts Payable

$ 2,128

Stockholders’ Equity

Common Stock

Retained Earnings ($65,500 + $37,700 – $0)

Total Stockholders’ Equity

213,200

Total Liabilities and Stockholders’ Equity

P22-42A, cont.

Requirement 2, cont.

GRADY TIRE COMPANY

Budgeted Statement of Cash Flows

For the Year Ended December 31, 2017

Operating Activities:

Cash receipts from customers

$ 206,010

Cash payments for operating expenses*

(117,332)

Cash payments for interest expense

Cash payments for income taxes

Net cash provided by operating activities

Investing Activities:

Cash payments for equipment purchases

Net cash used for investing activities

Financing Activities:

Proceeds from issuance of notes payable

Payment of notes payable

Net cash provided by (used for) financing activities

Net increase in cash

Cash balance, January 1, 2017

Cash balance, December 31, 2017

P22-43A Using sensitivity analysis

Learning Objective 5

1. Option 2 Feb. NI $1,750

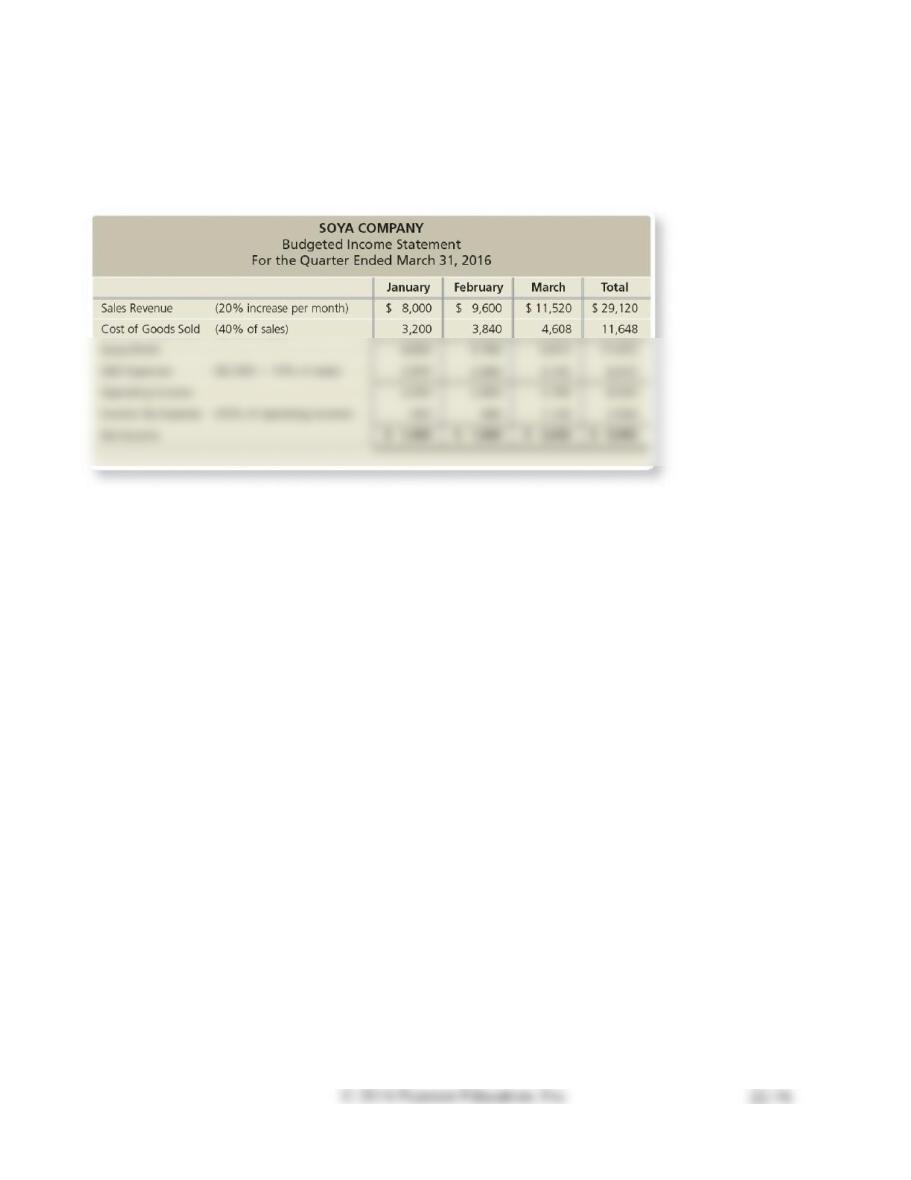

Soya Company prepared the following budgeted income statement for the first quarter of 2016:

Soya Company is considering two options. Option 1 is to increase advertising by $1,200 per month.

Option 2 is to use better-quality materials in the manufacturing process. The better materials will

increase the cost of goods sold to 45% but will provide a better product at the same sales price. The

marketing manager projects either option will result in sales increases of 25% per month rather than

20%.

Requirements

1. Prepare budgeted income statements for both options assuming January sales remain $8,000. Round

all calculations to the nearest dollar.

2. Which option should Soya choose? Explain your reasoning.

SOLUTION

Requirement 1

Option 1:

SOYA COMPANY

Budgeted Income Statement

For the Quarter Ended March 31, 2016

January

February

March

Total

Sales Revenue (25% increase per month)

$ 8,000

$ 10,000

$ 12,500

$ 30,500

Cost of Goods Sold (40% of sales)

12,200

Gross Profit

18,300

S&A Expenses ($2,000 + $1,200 advertising + 10% of sales)

12,650

Operating Income

Income Tax Expense (30% of operating income)

Net Income

Option 2:

SOYA COMPANY

Budgeted Income Statement

For the Quarter Ended March 31, 2016

January

February

March

Total

Sales Revenue (25% increase per month)

$ 8,000

$ 10,000

$ 12,500

$ 30,500

Cost of Goods Sold (45% of sales)

Gross Profit

S&A Expenses ($2,000 + 10% of sales)

Operating Income

Income Tax Expense (30% of operating income)

Net Income

$ 1,750

$ 5,407

P22-43A, cont.

Requirement 2

If one of the two options is chosen, it would be Option 2 because net income for the quarter is expected

to be $1,452 higher than it is in Option 1 ($5,407 for Option 2 − $3,955 for Option 1).

P22A-44A Preparing an operating budget—sales budget; inventory, purchases and COGS

budget; and S&A expense budget

Learning Objective 6

Appendix 22A

2. May purchases $30,750

3. Apr. total S&A exp. $10,900

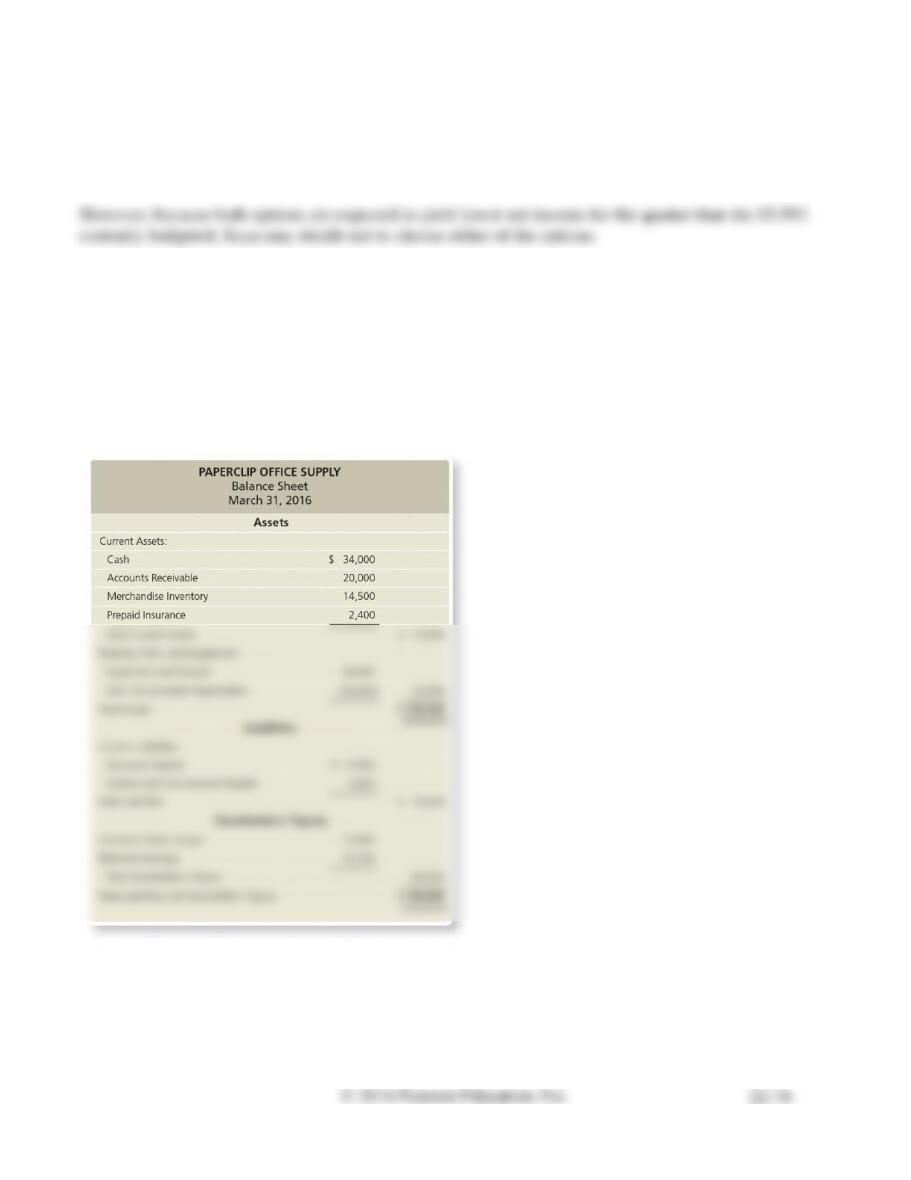

Paperclip Office Supply’s March 31, 2016, balance sheet follows:

The budget committee of Paperclip Office Supply has assembled the following data:

a. Sales in April are expected to be $60,000. Paperclip forecasts that monthly sales will increase 2%

over April sales in May. June’s sales will increase by 4% over April sales. July sales will increase

20% over April sales. Cash receipts are 80% in the month of the sale and 20% in the month

following the sale.

b. Paperclip maintains inventory of $7,000 plus 25% of the cost of goods sold budgeted for the

following month. Cost of goods sold equal 50% of sales revenue. Purchases are paid 30% in the

month of the purchase and 70% in the month following the purchase.

Requirements

1. Prepare Paperclip’s sales budget for April and May 2016. Round all amounts to the nearest dollar.

2. Prepare Paperclip’s inventory, purchases, and cost of goods sold budget for April and May.

3. Prepare Paperclip’s selling and administrative expense budget for April and May.

SOLUTION

Requirement 1

PAPERCLIP OFFICE SUPPLY

Sales Budget

Total budgeted sales

Requirement 2

PAPERCLIP OFFICE SUPPLY

Inventory, Purchases, and Cost of Goods Sold Budget

For the Two Months Ended May 31, 2016

Cost of goods sold (50% of sales)

Total merchandise inventory required

Less: Beginning merchandise inventory

Budgeted purchases

*May desired ending inventory:

+

P22A-44A, cont.

Requirement 3

PAPERCLIP OFFICE SUPPLY

Selling and Administrative Expense Budget

For the Two Months Ended May 31, 2016

April

May

Total