Exercises

E22-21 Budgeting benefits

Learning Objective 1

This year Op. Inc. $1,880,000

David Rodriguez owns a chain of travel goods stores, Rodriguez Travel Goods. Last year, his sales staff

sold 25,000 suitcases at an average sales price of $150. Variable expenses were 60% of sales revenue,

and the total fixed expense was $120,000. This year, the chain sold more expensive product lines. Sales

were 20,000 suitcases at an average price of $250. The variable expense percentage and the total fixed

expenses were the same both years. Rodriguez evaluates the chain manager by comparing this year’s

operating income with last year’s operating income.

Prepare a performance report for this year, similar to Exhibit 22-2, which compares this year’s results

with last year’s results. How would you improve Rodriguez’s performance evaluation system to better

analyze this year’s results?

SOLUTION

RODRIGUEZ TRAVEL GOODS

Income Statement Performance Report

E22-22 Describing master budget components

Learning Objective 2

Sarah Edwards, division manager for Pillows Plus, is speaking to the controller, Diana Rothman, about

the budgeting process. Sarah states, “I’m not an accountant, so can you explain the three main parts of

the master budget to me and tell me their purpose?” Answer Sarah’s question.

SOLUTION

A master budget is the set of budgeted financial statements and supporting schedules for the entire

The master budget models the company’s planned activities, and managers pay special attention to

ensure that the results of the budgeted income statement, the budgeted balance sheet, and the budgeted

statement of cash flows support key strategies. Creating a budget facilitates coordination and

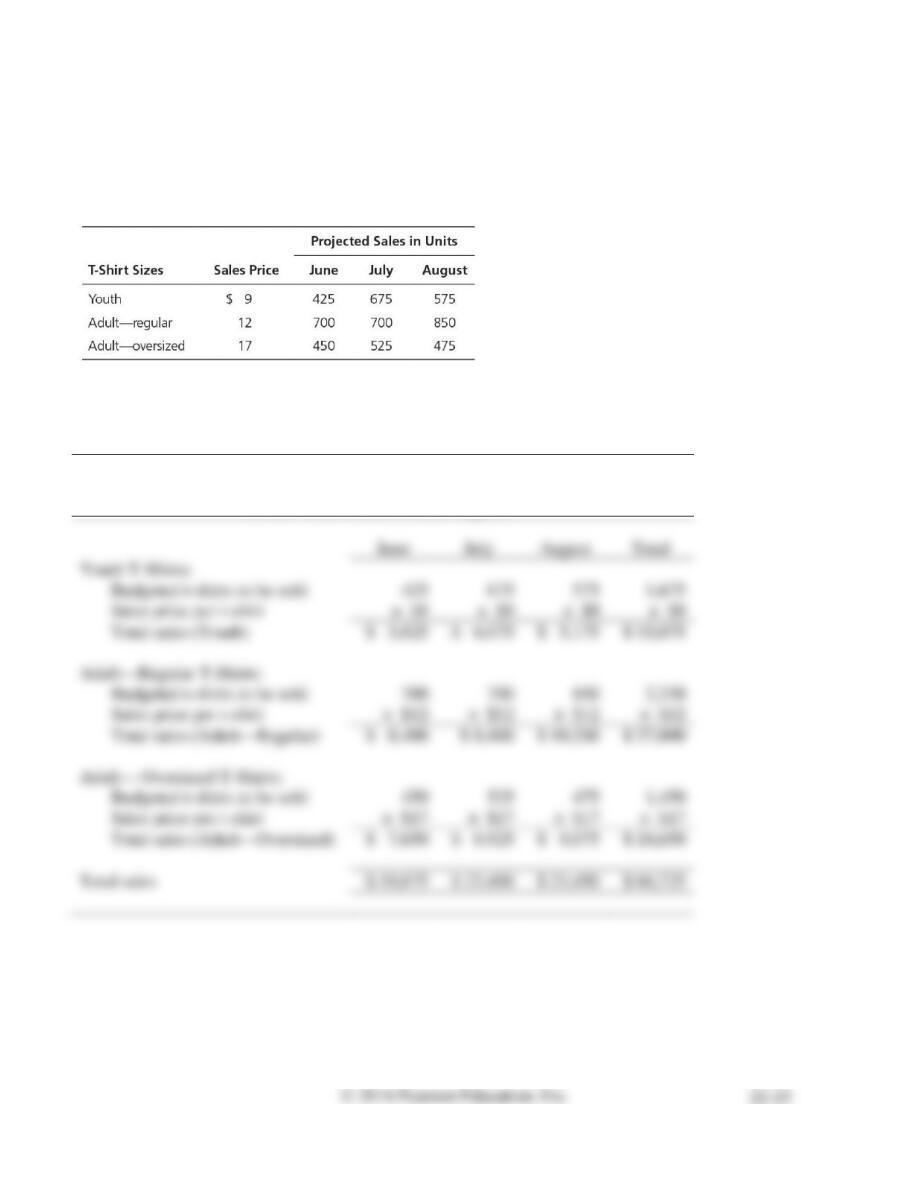

E22-23 Preparing an operating budget—sales budget

Learning Objective 3

Jul. total sales $23,400

Sinclair Company manufactures T-shirts printed with tourist destination logos. The following table

shows sales prices and projected sales volume for the summer months:

Prepare a sales budget for Sinclair Company for the three months.

SOLUTION

SINCLAIR COMPANY

Sales Budget

For the Three Months Ended August 31

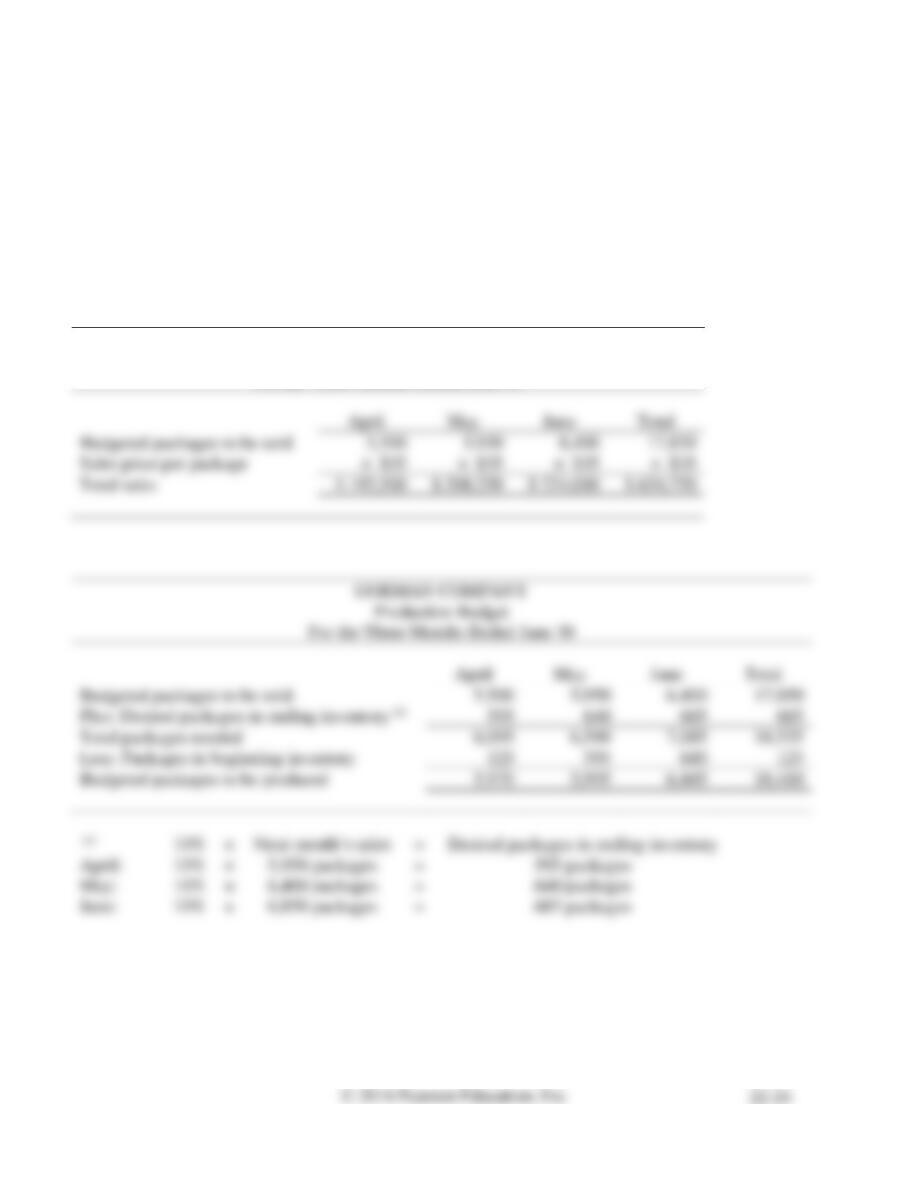

E22-24 Preparing an operating budget—sales and production budgets

Learning Objective 3

May pkg. produced 5,995

Gorman Company manufactures drinking glasses. One unit is a package of eight glasses, which sells for

$35. Gorman projects sales for April will be 5,500 packages, with sales increasing by 450 packages per

month for May, June, and July. On April 1, Gorman has 125 packages on hand but desires to maintain

an ending inventory of 10% of the next month’s sales. Prepare a sales budget and a production budget

for Gorman for April, May, and June.

SOLUTION

GORMAN COMPANY

Sales Budget

For the Three Months Ended June 30

E22-25 Preparing an operating budget—direct materials, direct labor, and manufacturing

overhead budgets

Learning Objective 3

2nd Qtr. OH $587.50

Trevor, Inc. manufactures model airplane kits and projects production at 500, 570, 300, and 450 kits for

the next four quarters. Direct materials are $10 per kit. Indirect materials are considered insignificant

and are not included in the budgeting process. Beginning Raw Materials Inventory is $200, and the

company desires to end each quarter with 30% of the materials needed for the next quarter’s production.

Trevor desires a balance of $200 in Raw Materials Inventory at the end of the fourth quarter. Each kit

requires 0.75 hours of direct labor at an average cost of $25 per hour. Manufacturing overhead is

allocated using direct labor hours as the allocation base. Variable overhead is $0.75 per kit, and fixed

overhead is $160 per quarter. Prepare Trevor’s direct materials budget, direct labor budget, and

manufacturing overhead budget for the year. Round the direct labor hours needed for production,

budgeted overhead costs, and predetermined overhead allocation rate to two decimal places. Round

other amounts to the nearest whole number.

SOLUTION

TREVOR, INC.

Direct Materials Budget

For the Year Ended December 31

E22-25, cont.

TREVOR, INC.

Direct Labor Budget

For the Year Ended December 31

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Budgeted kits to be produced

500

570

300

450

1,820

Direct labor hours per kit

× 0.75

× 0.75

× 0.75

× 0.75

× 0.75

Direct labor hours needed for production

Direct labor cost per hour

Budgeted direct labor cost

Fourth

Budgeted kits to be produced

Variable overhead cost per kit

× $0.75

× $0.75

× $0.75

× $0.75

Budgeted variable overhead

Budgeted fixed overhead

640.00

Direct labor hours (from DL budget)

Predetermined overhead allocation rate

$2,005.00 / 1,365.00 DLHr

Note: Exercise E22-25 must be completed before attempting Exercise E22-26.

E22-26 Preparing an operating budget—cost of goods sold budget

Learning Objective 3

3rd Qtr. COGS $20,895

Refer to the budgets prepared in Exercise E22-25. Determine the cost per kit to manufacture the model

airplane kits. Trevor projects sales of 400, 100, 700, and 500 kits for the next four quarters. Prepare a

cost of goods sold budget for the year. Trevor has no kits in beginning inventory. Round amounts to two

decimal places.

SOLUTION

Direct materials cost per kit

$ 10.00

Direct labor cost per kit (0.75 DLHr per kit × $25 per DLHr)

Manufacturing overhead cost per kit (0.75 DLHr per kit × $1.47 per DLHr*)

Total projected manufacturing cost per kit

Kits produced and sold

Cost per kit

Total budgeted cost of goods sold

$ 2,985

E22-27 Preparing a financial budget—schedule of cash receipts, sensitivity analysis

Learning Objectives 4, 5

1. Feb. total cash receipts $11,960

Armand Company projects the following sales for the first three months of the year: $10,600 in January;

$12,300 in February; and $12,900 in March. The company expects 60% of the sales to be cash and the

remainder on account. Sales on account are collected 50% in the month of the sale and 50% in the

following month. The Accounts Receivable account has a zero balance on January 1. Round to the

nearest dollar.

Requirements

1. Prepare a schedule of cash receipts for Armand for January, February, and March. What is the

balance in Accounts Receivable on March 31?

2. Prepare a revised schedule of cash receipts if receipts from sales on account are 60% in the month of

the sale, 30% in the month following the sale, and 10% in the second month following the sale.

What is the balance in Accounts Receivable on March 31?

SOLUTION

Requirement 1

Schedule of Cash Receipts from Customers

Total sales

Cash Receipts from Customers:

Accounts Receivable balance, January 1

Total cash receipts from customers

Accounts Receivable balance, March 31:

March – Credit sales, 50% collected in April

$ 2,580

E22-27, cont.

Requirement 2

Revised Schedule of Cash Receipts from Customers

January

February

March

Total

Total sales

$ 10,600

$ 12,300

$ 12,900

$ 35,800

January

February

March

Total

Cash Receipts from Customers:

Accounts Receivable balance, January 1

$ 0

$ 1,272

Total cash receipts from customers

$ 11,604

$ 12,736

$ 33,244

Accounts Receivable balance, March 31:

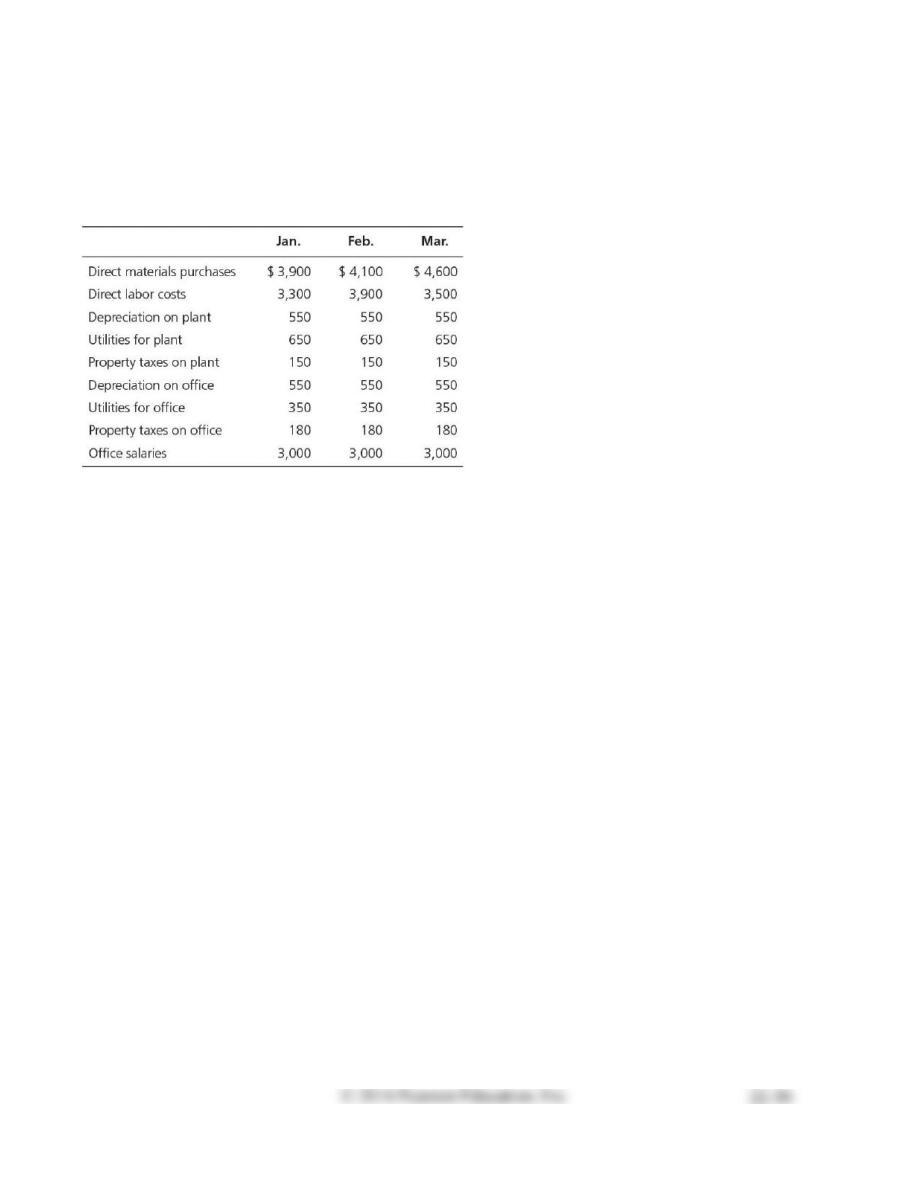

E22-28 Preparing a financial budget—schedule of cash payments

Learning Objective 4

Mar. total cash pmts. $11,600

Armand Company has the following projected costs for manufacturing and selling and administrative

expenses:

All costs are paid in month incurred except: direct materials, which are paid in the month following the

purchase; utilities, which are paid in the month after incurred; and property taxes, which are prepaid for

the year on January 2. The Accounts Payable and Utilities Payable accounts have a zero balance on

January 1. Prepare a schedule of cash payments for Armand for January, February, and March.

Determine the balances in Prepaid Property Taxes, Accounts Payable, and Utilities Payable as of March

31.

SOLUTION

Schedule of Cash Payments

January

February

March

Total

Cash Payments

Direct Materials:

Accounts Payable balance, January 1

January—Direct materials purchases paid in Feb.

February—Direct materials purchases paid in Mar.

Total payments for direct materials

3,900

4,100

Direct Labor:

January—Direct labor paid in January

3,300

February—Direct labor paid in February

3,900

Total payments for direct labor

3,900

3,500

10,700

Manufacturing Overhead:

January—Utilities for plant paid in February

650

February—Utilities for plant paid in March

650

Year—Property taxes on plant prepaid on

Jan. 2, $150/month × 12 months

1,800

Total payments for manufacturing overhead

1,800

650

650

3,100

Selling and Administrative Expenses:

January—Utilities for office paid in February

350

February—Utilities for office paid in March

350

Year—Property taxes on office prepaid on

Jan. 2 ($180/month × 12 months)

2,160

January—Office salaries paid in January

3,000

February—Office salaries paid in February

3,000

March—Office salaries paid in March

3,000

Total payments for S&A expenses

5,160

3,350

3,350

11,860

Total cash payments

March 31 liability balances:

Prepaid Property Taxes – $2,970

Accounts Payable – $4,600

Utilities Payable – $1,000

Note: Exercises E22-27 and E22-28 must be completed before attempting Exercise E22-29.

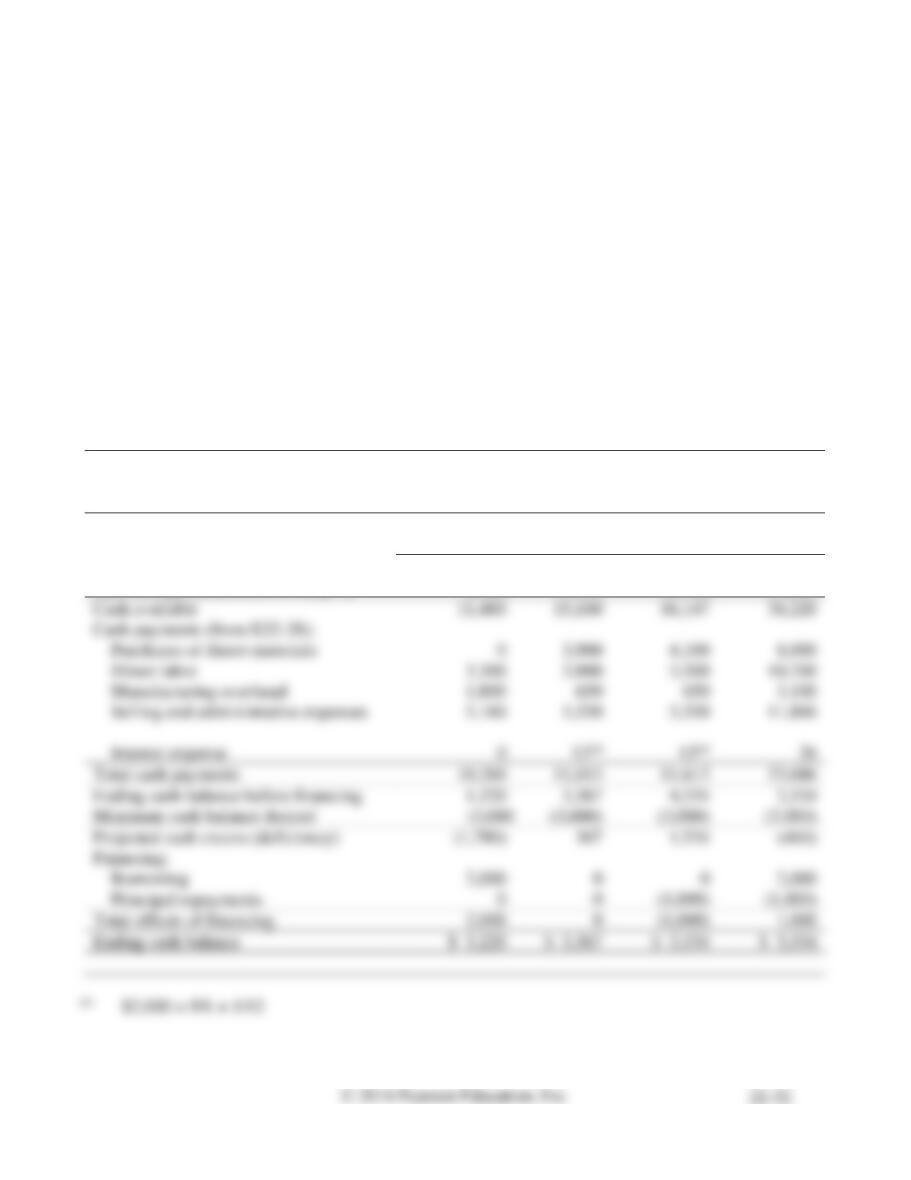

E22-29 Preparing the financial budget—cash budget

Learning Objective 4

Feb. ending cash bal. $3,367

Use the original schedule of cash receipts completed in Exercise E22-27, Requirement 1, and the

schedule of cash payments completed in Exercise E22-28 to complete a cash budget for Armand

Company.

Additional information: Armand’s beginning cash balance is $3,000, and Armand desires to maintain a

minimum ending cash balance of $3,000. Armand borrows cash as needed at the beginning of each

month in increments of $1,000 and repays the amounts borrowed in increments of $1,000 at the

beginning of months when excess cash is available. The interest rate on amounts borrowed is 8% per

year. Interest is paid at the beginning of the month on the outstanding balance from the previous month.

SOLUTION

ARMAND COMPANY

Cash Budget

For the Three Months Ended March 31

January

February

March

Total

Beginning cash balance

$ 3,000

$ 3,220

$ 3,367

$ 3,000

Cash receipts (from E22-27, Req. 1)

8,480

11,960

12,780

33,220

Cash available

11,480

15,180

16,147

36,220

Cash payments (from E22-28):

Purchases of direct materials

Direct labor

3,300

10,700

Manufacturing overhead

1,800

650

Selling and administrative expenses

5,160

11,860

Interest expense

Total cash payments

10,260

11,813

11,613

33,686

Ending cash balance before financing

1,220

Minimum cash balance desired

Projected cash excess (deficiency)

(1,780)

367

Financing:

Borrowing

2,000

0

0

Principal repayments

Total effects of financing

2,000

Ending cash balance

$ 3,367

$ 3,534

$ 3,534

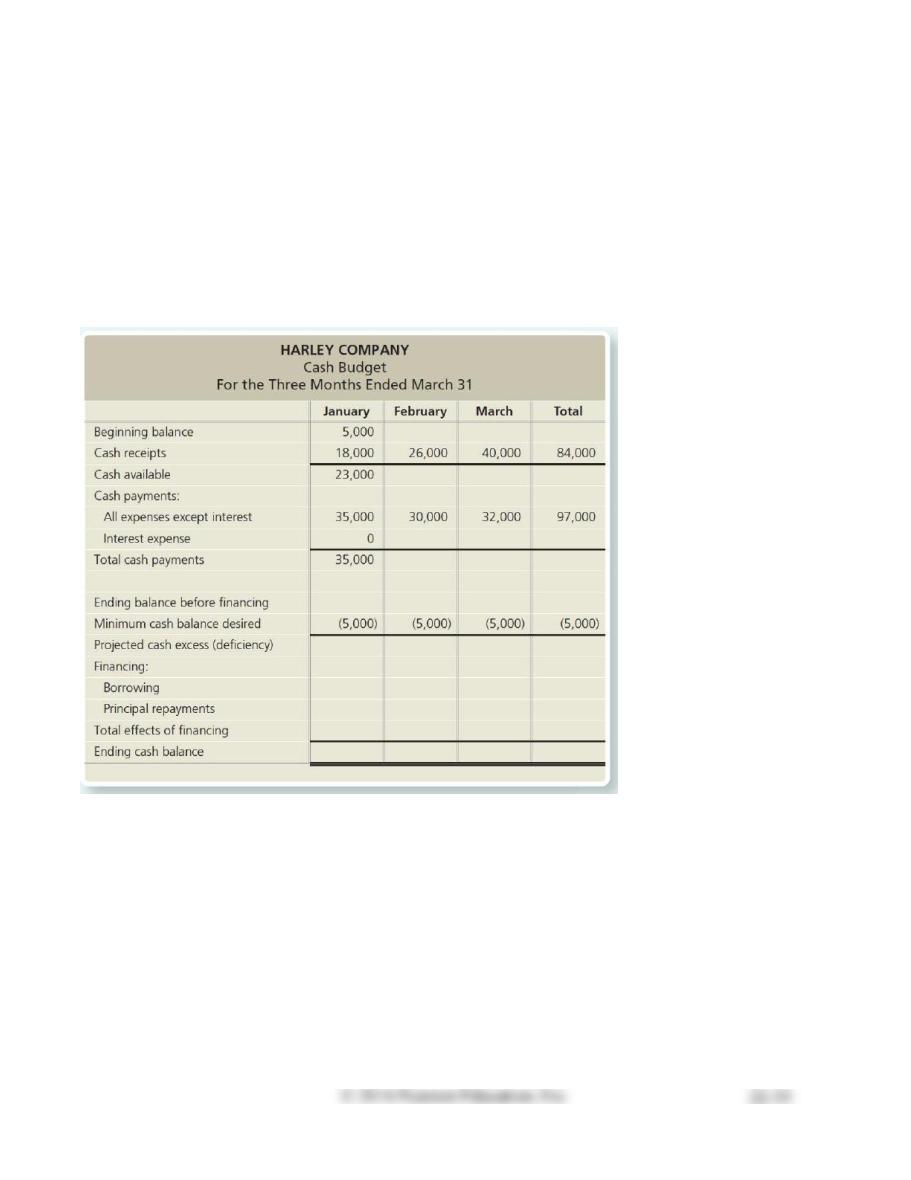

E22-30 Preparing the financial budget—cash budget

Learning Objective 4

Mar. interest expense $212

Harley Company requires a minimum cash balance of $5,000. When the company expects a cash

deficiency, it borrows the exact amount required on the first of the month. Expected excess cash is used

to repay any amounts owed. Interest owed from the previous month’s principal balance is paid on the

first of the month at 12% per year. The company has already completed the budgeting process for the

first quarter for cash receipts and cash payments for all expenses except interest. Harley does not have

any outstanding debt on January 1. Complete the cash budget for the first quarter for Harley Company.

Round interest expense to the nearest whole dollar.

SOLUTION

HARLEY COMPANY

Cash Budget

For the Three Months Ended March 31

January

February

March

Total

Beginning balance

$ 5,000

$ 5,000

$ 5,000

$ 5,000

Cash receipts

18,000

26,000

40,000

84,000

Cash available

23,000

31,000

45,000

89,000

Cash payments:

All expenses except interest

35,000

30,000

32,000

97,000

Interest expense

Total cash payments

35,000

30,170

32,212

97,382

Ending balance before financing

12,788

Minimum cash balance desired

Projected cash excess (deficiency)

Financing:

Borrowing

17,000

21,170

Principal repayments

Total effects of financing

17,000

13,382

Ending cash balance

$ 5,000

$ 5,000

$ 5,000

$ 5,000

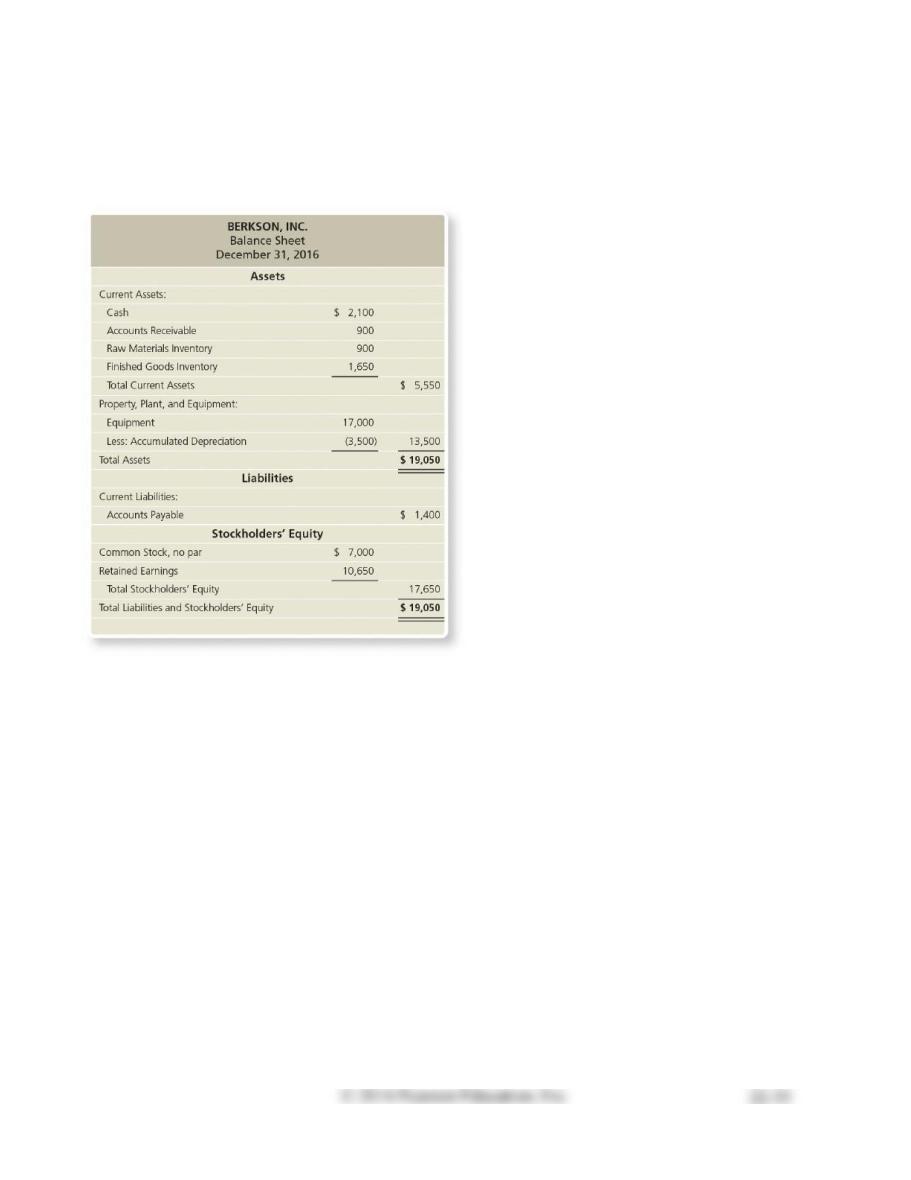

E22-31 Preparing the financial budget—budgeted balance sheet

Learning Objective 4

FG inventory $500

Berkson, Inc. has the following balance sheet at December 31, 2016:

Berkson projects the following transactions for 2017:

Sales on account, $21,000

Cash receipts from customers from sales on account, $15,800

Purchase of raw materials on account, $2,000

Payments on account, $2,000

Total cost of completed products, $15,150, which includes the following:

Raw materials used, $2,000

Direct labor costs incurred and paid, $5,800

Manufacturing overhead costs incurred and paid, $6,500

Depreciation on manufacturing equipment, $850

Cost of goods sold, $16,300

Selling and administrative costs incurred and paid, $1,000

Purchase of equipment, paid in 2017, $1,900

Prepare a budgeted balance sheet for Berkson, Inc. for December 31, 2017.

Hint: It may be helpful to trace the effects of each transaction on the accounting equation to determine

the ending balance of each account.

SOLUTION

BERKSON, INC.

Budgeted Balance Sheet

December 31, 2017

E22-31, cont.

Cash

Accounts

Receivable

Raw

Materials

Inventory

Finished

Goods

Inventory

Equipment

Accumulated

Depreciation

Accounts

Payable

Common

Stock

Retained

Earnings

Dec. 31, 2016

$ 2,100

$ 900

$ 900

$ 1,650

$ 17,000

$ (3,500)

$ 1,400

$ 7,000

$ 10,650

Sales on account

21,000

21,000

from customers

15,800

2,000

Payments

on account

(2,000)

(2,000)

Raw materials

used

2,000

Direct labor

(5,800)

5,800

Mfg. overhead

(6,500)

6,500

850

COGS

S&A

(1,000)

(1,000)

Purchase of

equipment

(1,900)

Dec. 31, 2017

$ 700

$ 6,100

$ 900

$ 500

$ 18,900

$ (4,350)

$ 1,400

$ 7,000

$ 14,350

Cash receipts

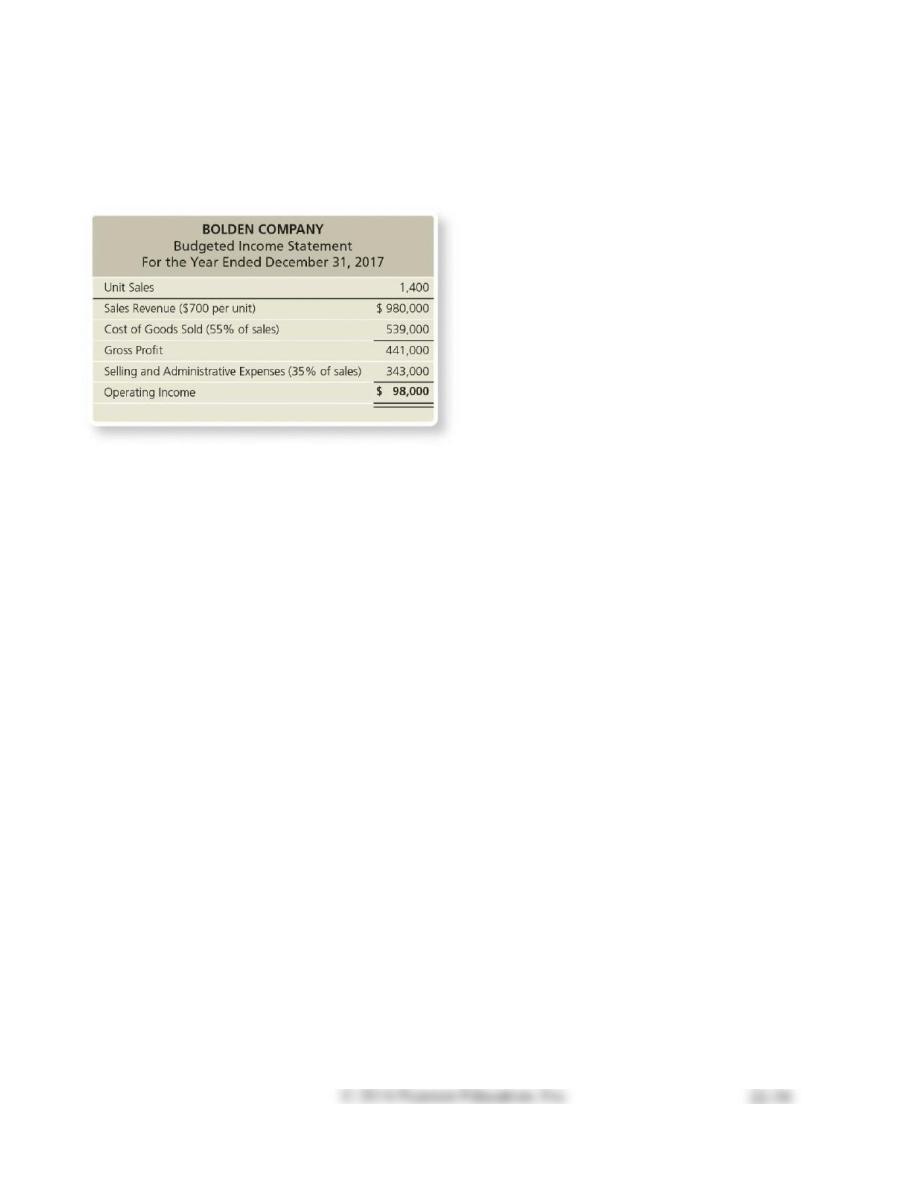

E22-32 Using sensitivity analysis

Learning Objective 5

1. Op. Inc. at 1,600 units $112,000

Bolden Company prepared the following budgeted income statement for 2017:

Requirements

1. Prepare a budgeted income statement with columns for 1,300 units, 1,400 units, and 1,600 units sold.

2. How might managers use this type of budgeted income statement?

3. How might spreadsheet software such as Excel assist in this type of analysis?

SOLUTION

Requirement 1

BOLDEN COMPANY

Budgeted Income Statement

For the Year Ended December 31, 2017

Unit Sales

1,300

1,400

1,600

Sales Revenue ($700 × units sold)

Cost of Goods Sold (55% of sales)

Gross Profit

S&A Expenses (35% of sales)

Operating Income

Requirement 2

The budgeted income statement prepared in Requirement 1 is a flexible budget prepared for various

Requirement 3

Technology, such as Excel spreadsheet software, makes it more cost-effective for managers to conduct

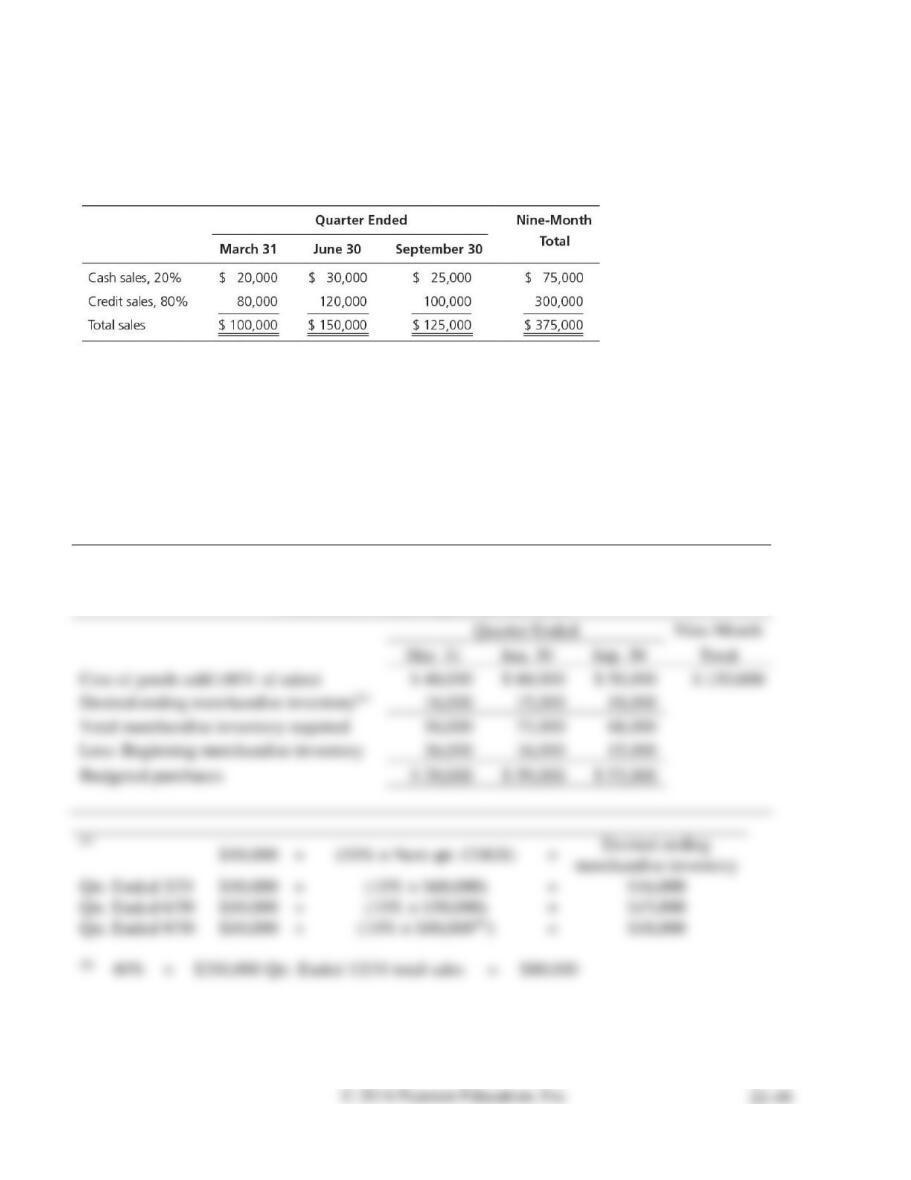

E22A-33 Preparing an operating budget—inventory, purchases, and cost of goods sold budget

Learning Objective 6

Appendix 22A

Stewart, Inc. sells tire rims. Its sales budget for the nine months ended September 30, 2016, follows:

In the past, cost of goods sold has been 40% of total sales. The director of marketing and the financial

vice president agree that each quarter’s ending inventory should not be below $10,000 plus 10% of cost

of goods sold for the following quarter. The marketing director expects sales of $200,000 during the

fourth quarter. The January 1 inventory was $36,000. Prepare an inventory, purchases, and cost of goods

sold budget for each of the first three quarters of the year. Compute cost of goods sold for the entire

nine-month period.

SOLUTION

STEWART, INC.

Inventory, Purchases, and Cost of Goods Sold Budget

Nine Months Ended September 30, 2016