CHAPTER 21

Incremental Analysis

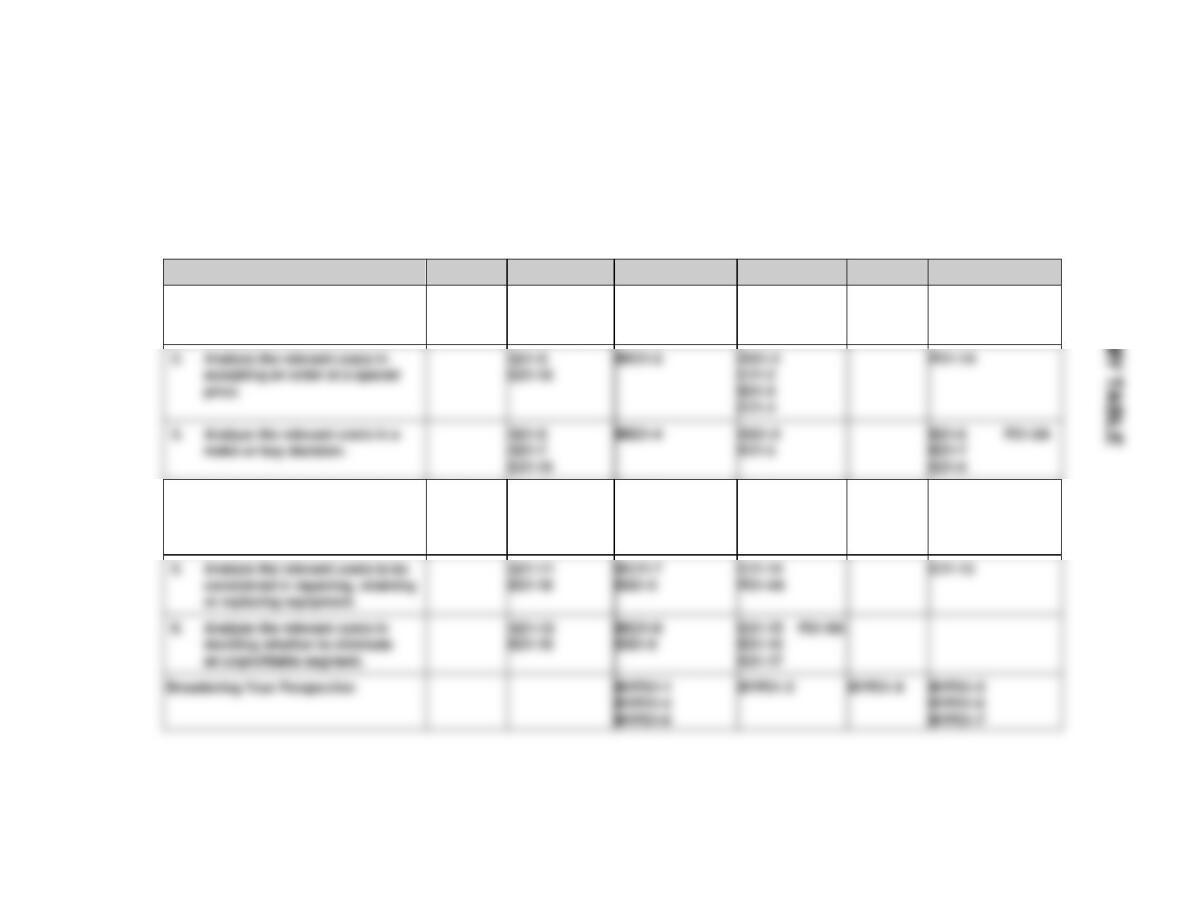

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe management’s

decision-making process and

incremental analysis.

1, 2, 3, 4

1, 2

1

1, 18

4. Analyze the relevant costs in

determining whether to sell or

process materials further.

8, 9, 10

5, 6

4

9, 10, 11,

12, 18

3A

retaining or replacing

6. Analyze the relevant costs in

deciding whether to eliminate

an unprofitable segment.

12

8

6

15, 16, 17,

5A

2. Analyze the relevant costs in

accepting an order at a

5

3

2

2, 3, 4, 18

1A

4

3

5, 6, 7, 8, 18

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Use incremental analysis for special order and identify

nonfinancial factors in the decision.

Simple

20–30

consider opportunity cost, and identify nonfinancial

Determine if product should be sold or processed further.

5A

Prepare incremental analysis concerning elimination of

divisions.

30–40

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End-of–Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Describe management’s decision–

making process and incremental

analysis.

Q21-1

Q21-2

Q21-3

Q21-4

E21-1

E21–18

BE21-1

BE21-2

DI21-1

*4. Analyze the relevant costs in

determining whether to sell or

process materials further.

Q21-8

Q21-9

Q21–10

E21–18

BE21-5

BE21-6

DI21-4

E21-9

E21–10

E21–11

P21–3A

E21–12

considered in repairing, retaining

or replacing equipment.

BE21-7

DI21-5

E21–14

P21–4A

deciding whether to eliminate

BE21-8

DI21-6

E21–15

E21–16

P21–5A

*2. Analyze the relevant costs in

price.

Q21-5

BE21-3

E21-2

E21-3

E21-4

P21–1A

Q21-7

E21–18

BE21-4

DI21-3

E21-5

E21-7

E21-8

ANSWERS TO QUESTIONS

1. The following steps are frequently involved in management’s decision-making process:

2. My roommate is incorrect. Accounting contributes to the decision-making process at Steps 2 and 4.

Prior to the decision, accounting provides relevant revenue and cost data for each course of action.

Following the decision, internal reports are prepared to show the actual impact of the decision.

6. The manufacturing costs that are relevant in the make-or-buy decision are those that will change

if the parts are purchased.

7. Opportunity cost may be defined as the potential benefit that may be obtained by following an

alternative course of action. Opportunity cost is relevant in a make-or-buy decision when the

facilities used to make the part can be used to generate additional income.

10. Joint costs are irrelevant to a sell-or–process-further decision because they are sunk costs and

will not change whether the decision is to sell the existing product or process it further. Therefore,

joint costs are ignored in this decision.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 21-1

BRIEF EXERCISE 21-2

BRIEF EXERCISE 21-3

BRIEF EXERCISE 21-4

BRIEF EXERCISE 21-5

BRIEF EXERCISE 21-6

BRIEF EXERCISE 21-7

BRIEF EXERCISE 21-8

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 21-1

DO IT! 21-3

(a)

$177,000

$211,000

$ 36,000

DO IT! 21-4

DO IT! 21-5

DO IT! 21-6

SOLUTIONS TO EXERCISES

EXERCISE 21-1

EXERCISE 21-2

EXERCISE 21-3

EXERCISE 21-4

EXERCISE 21-5

EXERCISE 21-6

(a) 1.

Buy

EXERCISE 21-6 (Continued)

EXERCISE 21–7

EXERCISE 21-7 (Continued)

EXERCISE 21-8

EXERCISE 21-8 (Continued)

EXERCISE 21-9

EXERCISE 21-9 (Continued)

EXERCISE 21–10

EXERCISE 21–11

EXERCISE 21-12

EXERCISE 21–13

EXERCISE 21–14

EXERCISE 21–15

EXERCISE 21–16

EXERCISE 21–17

Calculation of contribution margin per unit:

EXERCISE 21-17 (Continued)

Company profit with Products C and E:

EXERCISE 21–18

SOLUTIONS TO PROBLEMS

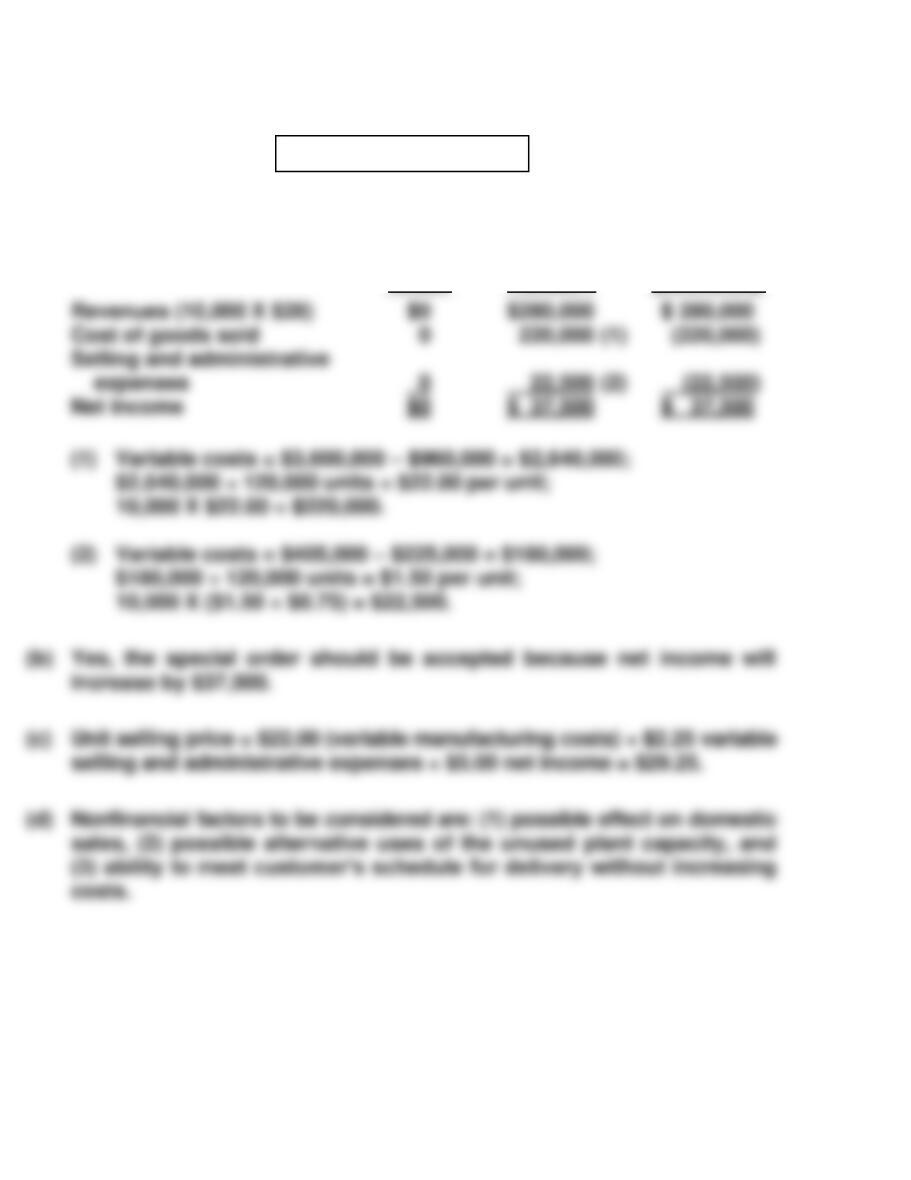

PROBLEM 21–1A

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

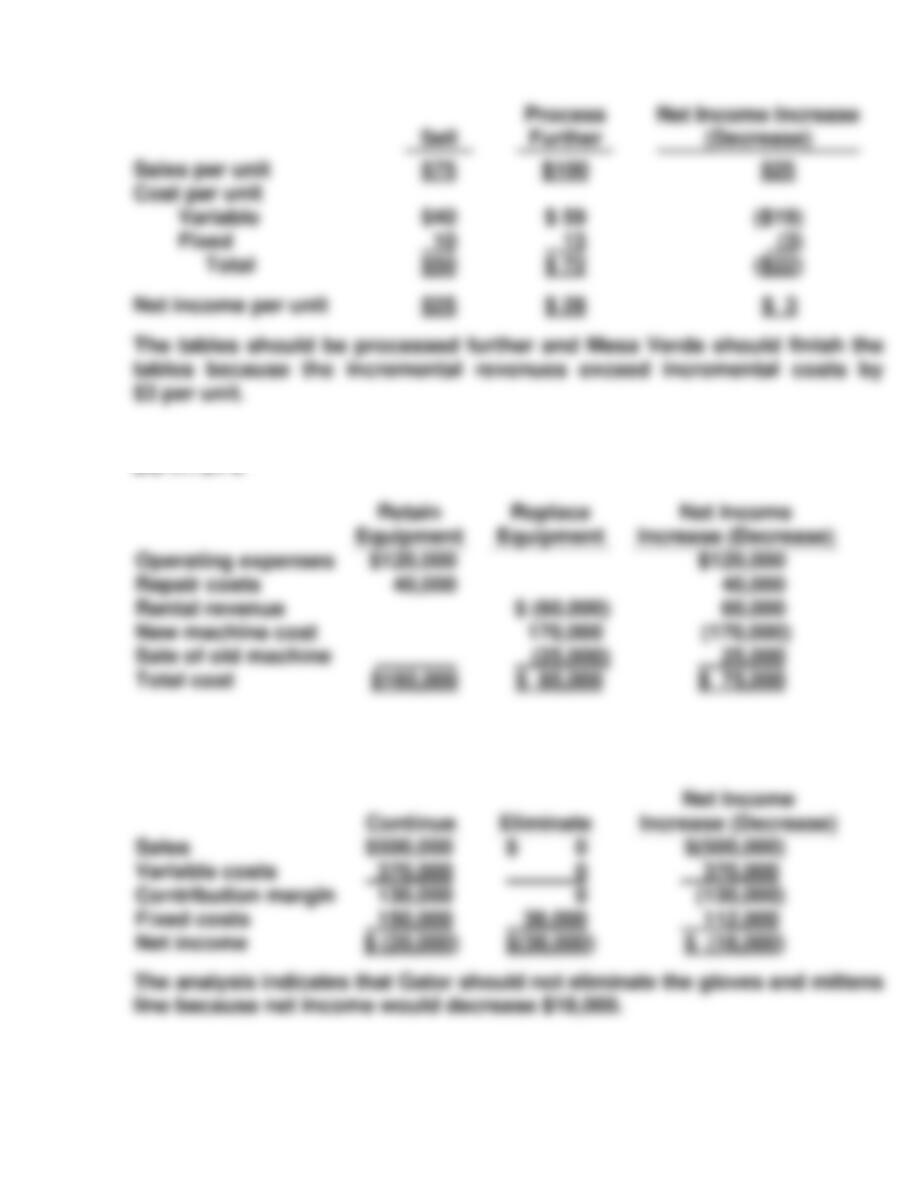

PROBLEM 21–2A

(a)

Net Income

Increase

Net Income

Increase

PROBLEM 21–3A

(a) (1)

Table Cleaner Not Processed Further

Costs:

Total costs

Gross profit

Total revenue

Costs:

Gross profit

PROBLEM 21-3A (Continued)

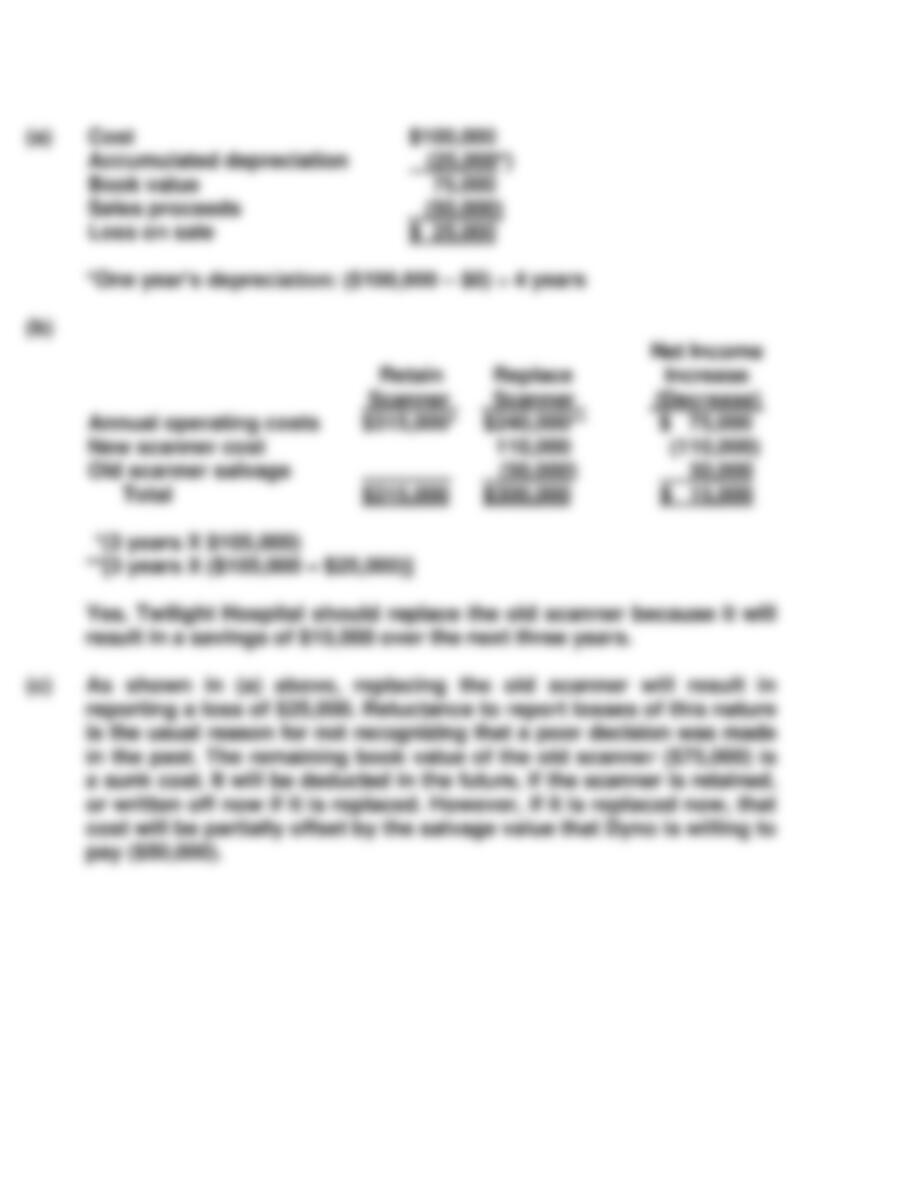

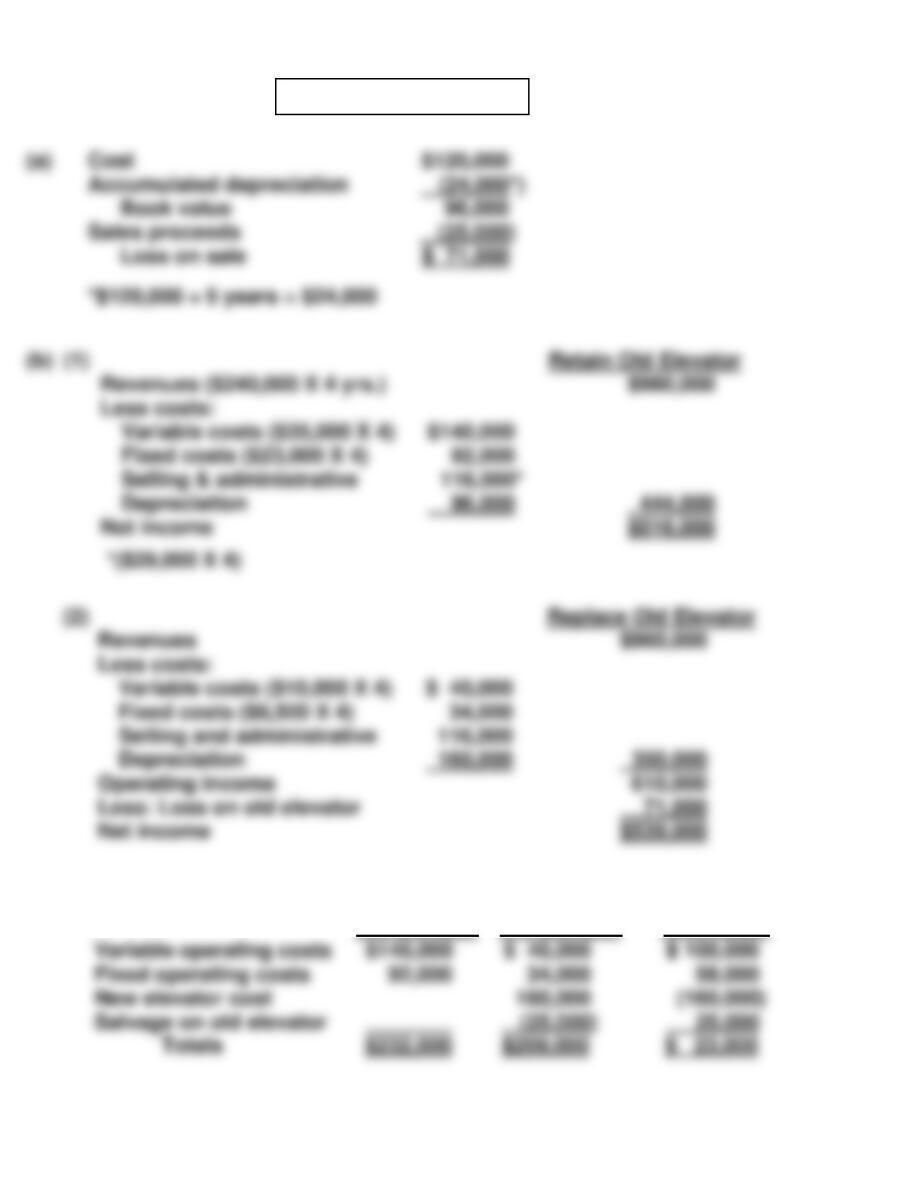

PROBLEM 21–4A

(c)

Retain

Old Elevator

Replace

Old Elevator

Net Income

Increase

(Decrease)

92,000

PROBLEM 21-4A (Continued)

(d) MEMO

TO: Ron Richter

FROM: Student

SUBJECT: Relevant Data for Decision to Replace Old Elevator

PROBLEM 21–5A

(a)

Division I

Division II

(b)

(1)

Division I

Continue

Eliminate

Net Income

Increase

(Decrease)

(2)

Division II

Continue

Eliminate

Net Income

Increase

(Decrease)

PROBLEM 21-5A (Continued)

(c) BRISLIN COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

CD21 CURRENT DESIGNS

Situation #1

(a) Current Designs should accept the special order based on the following

calculations:

CD21 (Continued)

Situation #2

(a) Current designs should not replace the Rotomold oven based on the

following calculations:

CD21 (Continued)

Situation #3

(a) Current Designs should make the seats based on the following calcu-

lations:

BYP 21-1 DECISION-MAKING ACROSS THE ORGANIZATION

Retain

Old Machine

Purchase

New Machine

Net Income

Increase

(Decrease)

BYP 21-2 MANAGERIAL ANALYSIS

(a)

Make

Buy—

Trans-

Tech

Buy—

Omega

Total Manufacturing Cost

BYP 21–2 (Continued)

BYP 21-3 REAL-WORLD FOCUS

BYP 21-4 REAL-WORLD FOCUS

(a) The types of outsourcing services that the company provides assis-

tance on are:

BYP 21-5 COMMUNICATION ACTIVITY

To: Preston Thiese—Plant Manager

From: Hank Jewel—Production Manager

BYP 21-6 ETHICS CASE

BYP 21-7 ALL ABOUT YOU

BYP 21-8 CONSIDERING YOUR COSTS AND BENEFITS