Problem 20-7 (concluded)

Equipment:

$80,000 – 4,000

Depreciation per ton = = $.19 per ton

400,000 tons

Requirement 2

Mineral mine:

Cost $ 2,200,000

Structures:

Cost $ 150,000

Less accumulated depreciation:

Equipment:

Cost $ 80,000

20–62 Intermediate Accounting, 8/e

Problem 20-8

a. This is a change in estimate.

No entry is needed to record the change

2016 adjusting entry:

If the effect is material, a disclosure note should describe the effect of a change in

b. This is a change in estimate.

No entry is needed to record the change

Calculation of annual depreciation after the estimate change:

$1,000,000 Cost

$25,000 Old depreciation ($1,000,000 ÷ 40 years)

A disclosure note should describe the effect of a change in estimate on income

from continuing operations, net income, and related per share amounts for the current

period.

Problem 20-8 (continued)

c. This is a change in accounting principle that usually is reported prospectively.

No entry is needed to record the change.

When a company changes to the LIFO inventory method from another inventory

method, accounting records usually are insufficient to determine the cumulative

d. This is a change in accounting estimate resulting from a change in accounting

principle.

No entry is needed to record the change

Problem 20-8 (concluded)

A change in depreciation method is considered a change in accounting estimate

resulting from a change in accounting principle. Accordingly, the Hoffman Group

reports the change prospectively; previous financial statements are not revised.

Instead, the company simply employs the straight-line method from now on. The

undepreciated cost remaining at the time of the change is depreciated straight line over

the remaining useful life.

($ in 000s)

Asset’s cost $330

Accumulated depreciation to date (calculated below) (162)

Calculation of SYD depreciation:

e. This is a change in estimate.

To revise the liability on the basis of the new estimate:

Loss—litigation ………………………………………………………… 150,000

f. This is a change in accounting principle accounted for prospectively.

Because the change will be effective only for assets placed in service after the

Problem 20-9

P R 1. By acquiring additional stock, Wagner increased its investment in

Wise, Inc., from a 12% interest to 25% and changed its method of

accounting for the investment to the equity method.

E P 6. Due to an unexpected relocation, Wagner determined that its office

building previously depreciated using a 45-year life should be

depreciated using an 18-year life.

E P 7. Wagner offers a three-year warranty on the farming equipment it

sells. Manufacturing efficiencies caused Wagner to reduce its

expectation of warranty costs from 2% of sales to 1% of sales.

20–66 Intermediate Accounting, 8/e

Problem 20-10

Requirement 1

Analysis: U = Understated

O = Overstated

2014 2015

Beginning inventory → Beginning inventory U-6,000

Plus: Net purchases Plus: Net purchases U-3,000

Requirement 2

Retained earnings ……………………………… 12,000

Requirement 3

The financial statements that were incorrect as a result of both errors (effect of

one error in 2014 and effect of three errors in 2015) would be retrospectively restated

Problem 20-11

Requirement 1

Analysis:

Correct Incorrect

(Should Have Been Recorded) (As Recorded)

[1] $1,900,000 x 25% (2 times the straight-line rate of 12.5%)

[2] $2,000,000 x 25%

[3] ($1,900,000 – 475,000) x 25%

[4] ($2,000,000 – 500,000 ) x 25%

To correct incorrect accounts

Retained earnings …………………………………………. 56,250

Problem 20–11 (concluded)

Requirement 2

This is a change in accounting estimate resulting from a change in accounting

principle.

No entry is needed to record the change

A change in depreciation method is considered a change in accounting estimate

resulting from a change in accounting principle. Accordingly, the Collins Corporation

Asset’s cost (after correction) $1,900,000

Accumulated depreciation to date ($475,000 + 356,250) (831,250)

Problem 20-12

a. This is a correction of an error.

To correct the error:

Prepaid insurance ($35,000 ÷ 5 yrs x 3 yrs: 2016–2018) ………. 21,000

The financial statements that were incorrect as a result of the error would be

retrospectively restated to report the prepaid insurance acquired and reflect the correct

operations, net income, and earnings per share.

b. This is a change in estimate.

No entry is needed to record the change

2016 adjusting entry:

Calculation of annual depreciation after the estimate change:

$600,000 Cost

$12,500 Old depreciation ([$600,000 – 100,000] ÷ 40 years)

20–70 Intermediate Accounting, 8/e

Problem 20-12 (continued)

A disclosure note should describe the effect of a change in estimate on income

from continuing operations, net income, and related per share amounts for the current

period.

c. This is a correction of an error.

To correct the error:

The financial statements that were incorrect as a result of the error would be

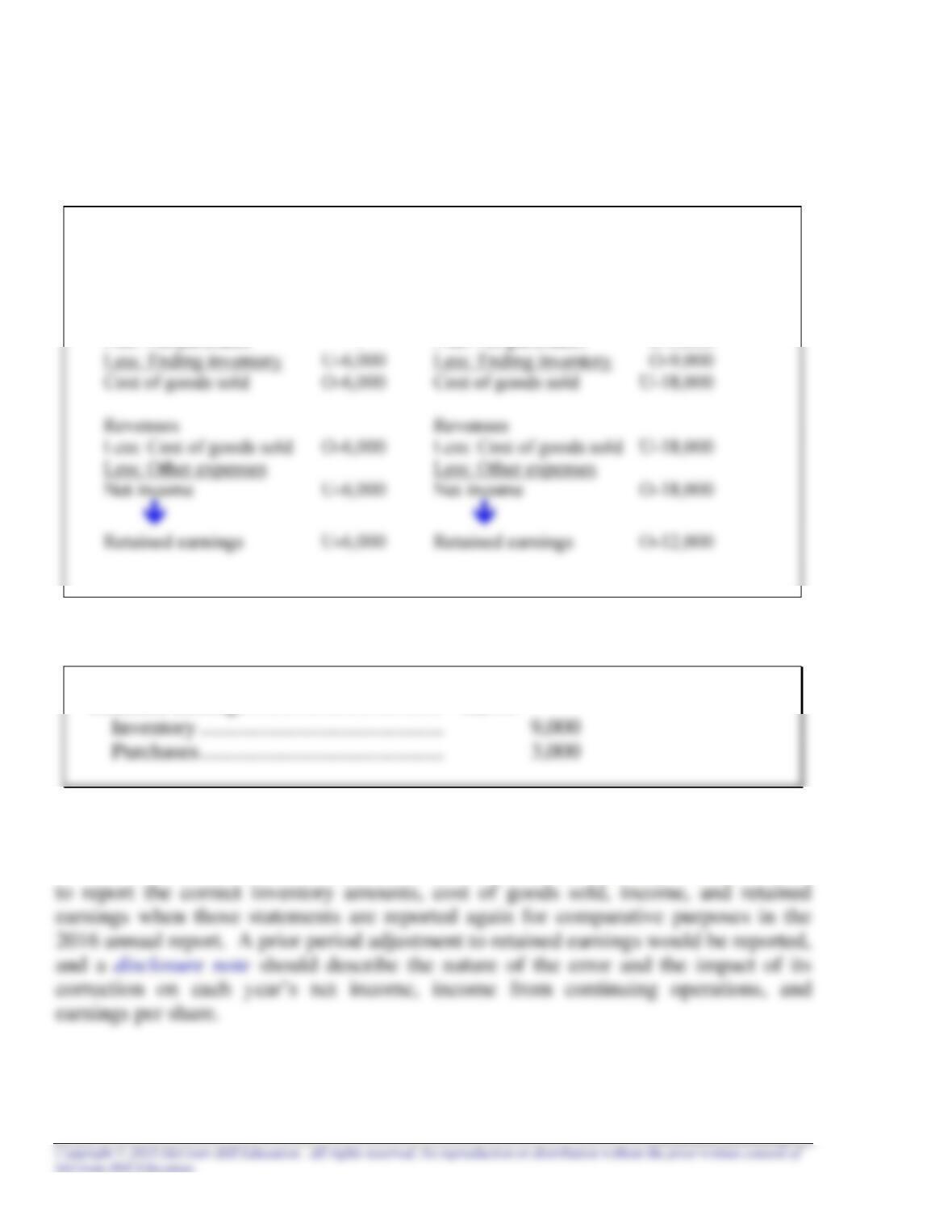

retrospectively restated to report the correct inventory amounts, cost of goods sold,

d. This is a change in accounting principle and is reported retrospectively.

To record the change:

Problem 20-12 (continued)

Most changes in accounting principle are accounted for retrospectively. Prior

years’ financial statements are recast to reflect the use of the new accounting method.

The company should increase retained earnings to the balance it would have been if

the FIFO method had been used previously; that is, by the cumulative income

e. This is a correction of an error.

To correct the error:

The 2015 financial statements that were incorrect as a result of the error would be

retrospectively restated to report the correct compensation expense, net income, and

Problem 20-12 (concluded)

f. This is a change in estimate resulting from a change in accounting principle and is

accounted for prospectively.

No entry is needed to record the change

2016 adjusting entry:

Depreciation expense (calculated below) ……………………………. 57,600

Accumulated depreciation ……………………………………. 57,600

A change in depreciation method is considered a change in accounting estimate

Undepreciated cost, Jan. 1, 2016 (given) $460,800

Estimated residual value (0)

g. This is a change in estimate.

No entry is needed to record the change

Problem 20-13

a. This is a correction of an error.

To correct the error:

Prepaid insurance ($35,000 ÷ 5 yrs x 3 yrs: 2016–2018) ………. 21,000

Income tax payable ($21,000 x 40%) ………………………….. 8,400

The financial statements that were incorrect as a result of the error would be

retrospectively restated to report the prepaid insurance acquired and reflect the correct

b. This is a change in estimate.

No entry is needed to record the change

2016 adjusting entry:

Calculation of annual depreciation after the change:

$600,000 Cost

$12,500 Old depreciation ([$600,000 – 100,000] ÷ 40 years)

20–74 Intermediate Accounting, 8/e

Problem 20-13 (continued)

A disclosure note should describe the effect of a change in estimate on income

from continuing operations, net income, and related per share amounts for the current

period.

c. This is a correction of an error.

To correct the error:

The financial statements that were incorrect as a result of the error would be

retrospectively restated to report the correct inventory amounts, cost of goods sold,

d. This is a change in accounting principle and is reported retrospectively.

To record the change:

Most changes in accounting principle are accounted for retrospectively. Prior

years’ financial statements are recast to reflect the use of the new accounting method.

The company should increase retained earnings to the balance it would have been if

amounts affected for all periods reported.

Problem 20-13 (continued)

Companies are required to repay the taxes saved by using LIFO in prior years

within six years. As a result, this liability has both current (payable within one year)

and noncurrent (payable after one year) aspects, but is not a deferred tax liability.

e. This is a correction of an error.

To correct the error:

Retained earnings (net effect) …………………………..…………………. 9,300

The 2015 financial statements that were incorrect as a result of the error would be

retrospectively restated to report the correct compensation expense, net income, and

Problem 20-13 (concluded)

f. This is a change in estimate resulting from a change in accounting principle and is

accounted for prospectively.

No entry is needed to record the change

A change in depreciation method is considered a change in accounting estimate

g. This is a change in estimate.

No entry is needed to record the change.

Problem 20-14

Requirement 1

a. ($ in millions)

Inventory (understatement of 2016 beginning inventory) ……………. 10

Retained earnings (understatement of 2015 income) ……………… 10

Note: The 2014 error requires no adjustment because it has self-corrected by 2016.

Patent …………………………………………………………………….. 3

d.

No entry to record the change

2016 adjusting entry:

Calculation of annual depreciation after the change:

$30 Cost

(18) Previous depreciation (calculated below*)

Problem 20-14 (concluded)

Requirement 2

Shareholders’ Net

Assets Liabilities Equity Income Expenses

2014 $740 $330 $410 $210 $150

2014 inventory (12) (12) (12) 12

2015 $820 $400 $420 $230 $175

2014 inventory 12 (12)

Problem 20-15

1a. To correct the error:

Equipment (cost) ………………………………………………………….. 45,000

b. To reverse erroneous entry:

Cash …………………………..…………………………………………….. 17,000

Office supplies ……………………………………………………….. 17,000

To record correct entry:

d. To correct the error:

Retained earnings ([$12 x 2,000 shares] – $2,000) ………………… 22,000

20–80 Intermediate Accounting, 8/e

Problem 20-15 (concluded)

e. To correct the error:

Retained earnings (overstatement of 2015 income) ………………….. 104,000

Interest expense (overstatement of 2016 interest) ………………. 104,000