20–20 Intermediate Accounting, 8e

ERROR AFFECTING PREVIOUS FINANCIAL

STATEMENTS, BUT NOT NET INCOME

Example: Incorrectly recording salaries payable as accounts

payable, recording a loss as an expense, or classifying a cash

To correct incorrect accounts …. ($ in millions)

Note receivable ……………………………………………….. 2

Accounts receivable ……………………………………… 2

RECORDING AN ASSET AS AN EXPENSE

In 2016, internal auditors discovered that Seidman

Distribution, Inc. had debited an expense account for the $7

Analysis:

($ in millions)

Correct Incorrect

(Should Have Been Recorded) (As Recorded)

2014 Equipment 7.0 Expense 7.0

Cash 7.0 Cash 7.0

T20–17

20–22 Intermediate Accounting, 8e

RECORDING AN ASSET AS AN EXPENSE

(Illustration continued)

During the two-year period, depreciation expense was

understated by $2.8 million, but other expenses were

To correct incorrect accounts …. ($ in millions)

Equipment ………………………………………………………. 7.0

Accumulated depreciation …………………………….. 2.8

Retained earnings …………………………………………. 4.2

T20–17 (continued)

INVENTORY MISSTATED

In early 2016, Overseas Wholesale Supply discovered that

$1 million of inventory had been inadvertently excluded

from its 2014 ending inventory count.

Analysis: U = Understated

O = Overstated

2014 2015

Beginning inventory → Beginning inventoryU

If discovered in 2015 (before closing): ($ in millions)

Inventory …………………………………………………………. 1

Retained earnings …………………………………………. 1

20–24 Intermediate Accounting, 8e

S

Su

ug

gg

ge

es

st

ti

io

on

ns

s

f

fo

or

r

C

Cl

la

as

ss

s

A

Ac

ct

ti

iv

vi

it

ti

ie

es

s

1. Critical Thinking Activity

It is alleged that not all accounting choices are made by management in the best interest of fair

and consistent financial reporting.

Suggestion:

Points to note:

Your students should come up with a wide variety of motives. Among them will likely be the

2. Real World Activity

The following February 22, 2013, report in Wallst.com described a change in the way

Abercrombie & Fitch accounts for inventories:

Abercrombie & Fitch Co. (NYSE: ANF) reported fourth-quarter and full-year 2012 earnings

before markets opened this morning.

For the quarter, the specialty retailer posted adjusted diluted earnings per share (EPS) of $2.21 on revenues

of $1.47 billion. In the same period a year ago, the company reported adjusted EPS of $1.12 on revenues of

Suggestion:

Ask students to consult the footnotes to the 2012 financials of Abercrombie & Fitch Co. and

describe the details of the change and to speculate on the motivation for the original method and the

change.

INVENTORIES

During the fourth quarter of Fiscal 2012, the Company elected to change its inventory valuation

method from the lower of cost or market utilizing the retail method to the lower of cost or market under the

weighted average cost method. The Company believes the new method is preferable as it is consistent with

4. CHANGE IN ACCOUNTING PRINCIPLE

The Company elected to change its method of accounting for inventory from the lower of cost or

market utilizing the retail method to the weighted average cost method effective February 2, 2013. In

accordance with generally accepted accounting principles, all periods have been retroactively adjusted to

20–26 Intermediate Accounting, 8e

As a result of the retroactive application of the change in accounting for inventory, the following items

in the Company’s Consolidated Statements of Operations and Comprehensive Income and Consolidated

Statements of Cash Flows have been restated:

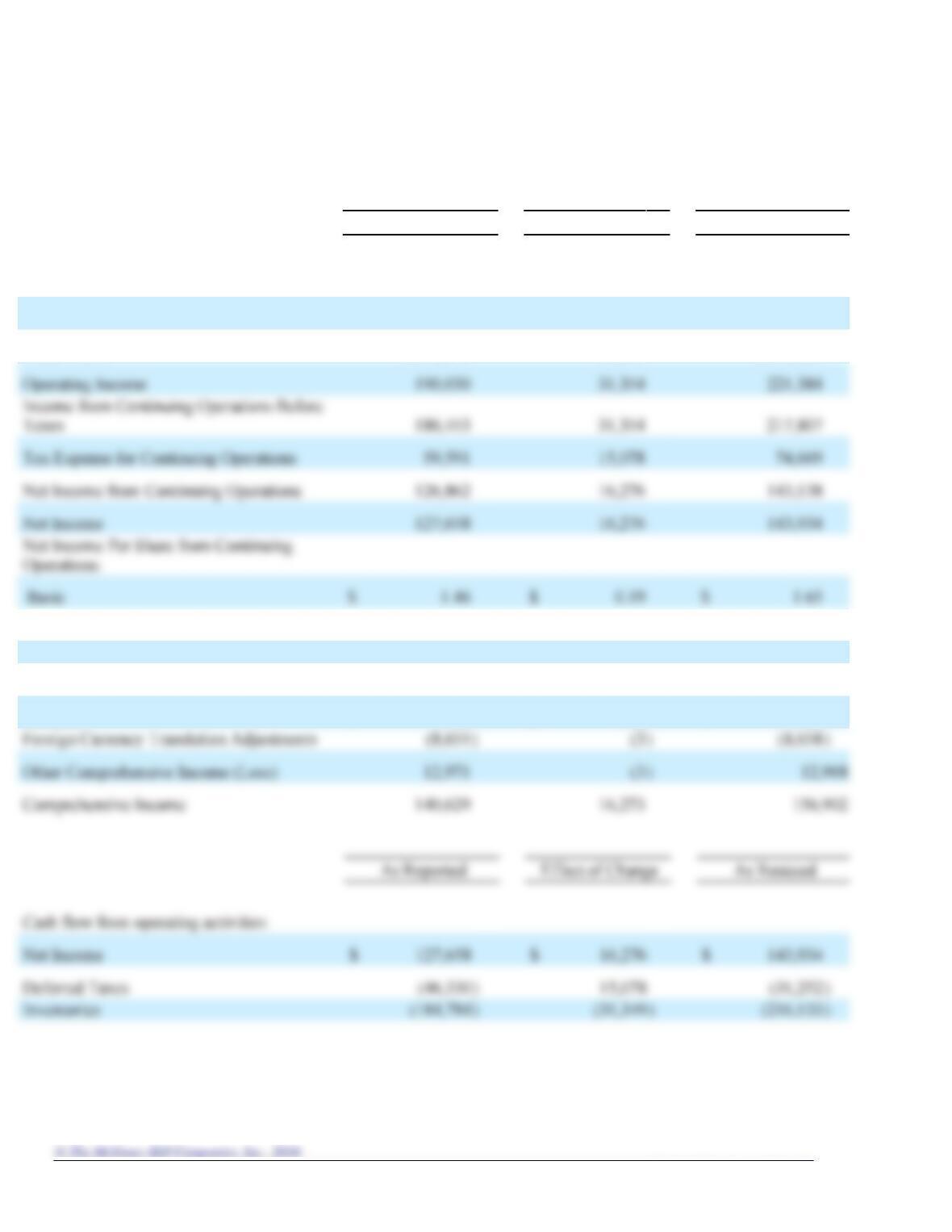

Fiscal Year Ended January 28, 2012 (in thousands, except per share data)

As Reported

Effect of Change

As Restated

Net Sales

$

4,158,058

$

—

$

4,158,058

Cost of Goods Sold

1,639,188

(31,354

)

1,607,834

Gross Profit

2,518,870

31,354

2,550,224

Operating Income

31,354

Tax Expense for Continuing Operations

15,078

Net Income from Continuing Operations

16,276

Net Income

Basic

$

1.46

$

0.19

$

1.65

Diluted

$

1.42

$

0.18

$

1.60

Net Income Per Share:

Basic

$

1.47

$

0.19

$

1.66

Diluted

$

1.43

$

0.18

$

1.61

Foreign Currency Translation Adjustments

Other Comprehensive Income (Loss)

)

Comprehensive Income

16,273

As Reported

Effect of Change

As Restated

Cash flow from operating activities:

Net Income

$

$

$

Deferred Taxes

(46,330

15,078

Inventories

(184,784

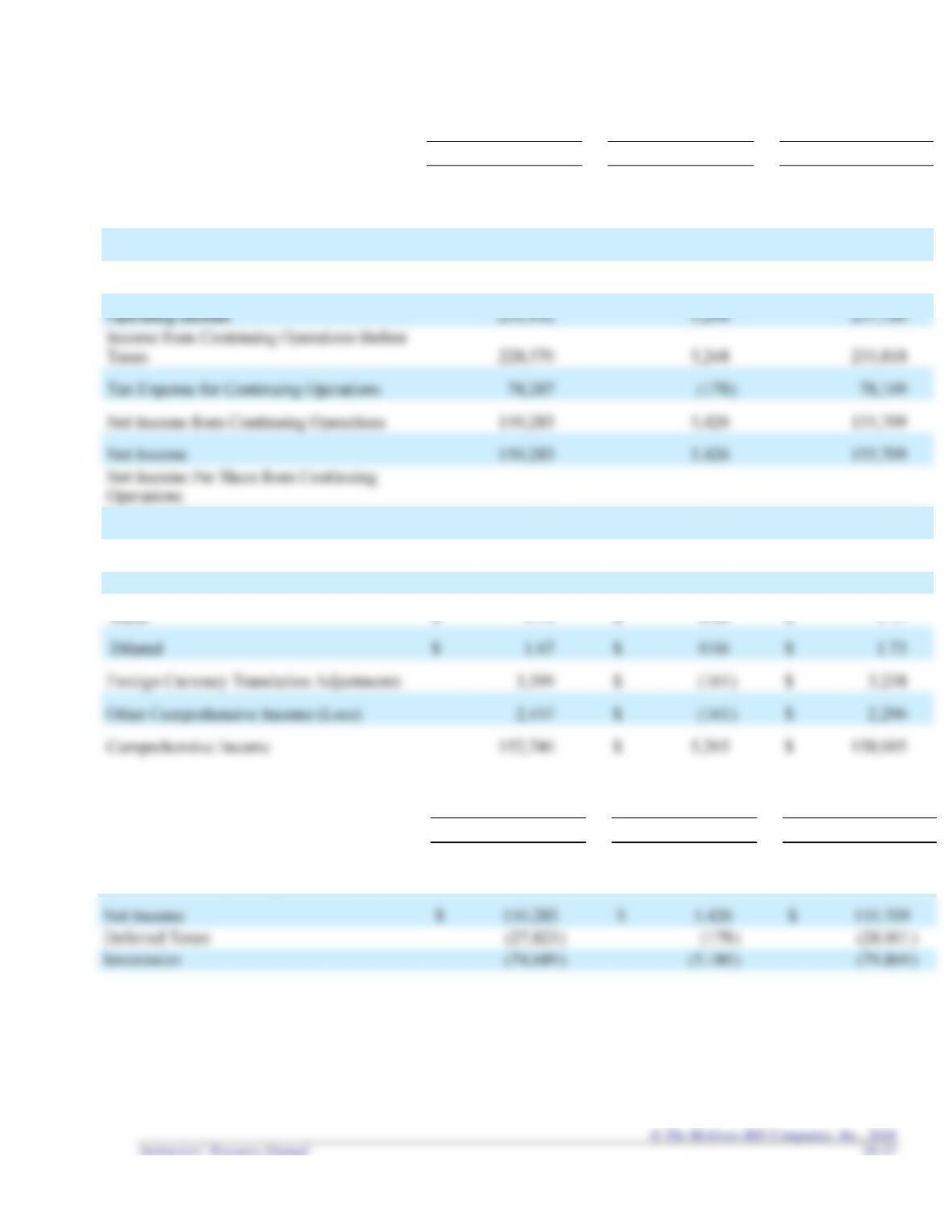

Fiscal Year Ended January 29, 2011 (in thousands, except per share data)

As Reported

Effect of Change

As Restated

Net Sales

$

3,468,777

$

—

$

3,468,777

Cost of Goods Sold

1,256,596

(5,248

)

1,251,348

Gross Profit

2,212,181

5,248

2,217,429

Operating Income

5,248

Tax Expense for Continuing Operations

Net Income from Continuing Operations

5,426

Net Income

5,426

Basic

$

1.71

$

0.06

$

1.77

Diluted

$

1.67

$

0.06

$

1.73

Net Income Per Share:

Basic

$

$

$

Diluted

$

1.67

$

0.06

$

1.73

Foreign Currency Translation Adjustments

$

$

Other Comprehensive Income (Loss)

$

)

$

Comprehensive Income

$

5,265

$

As Reported

Effect of Change

As Restated

Cash flow from operating activities:

Net Income

$

$

$

Deferred Taxes

Inventories

As a result of the retroactive application of the change in accounting for inventories, the following items in

the Company’s Consolidated Balance Sheets have been restated:

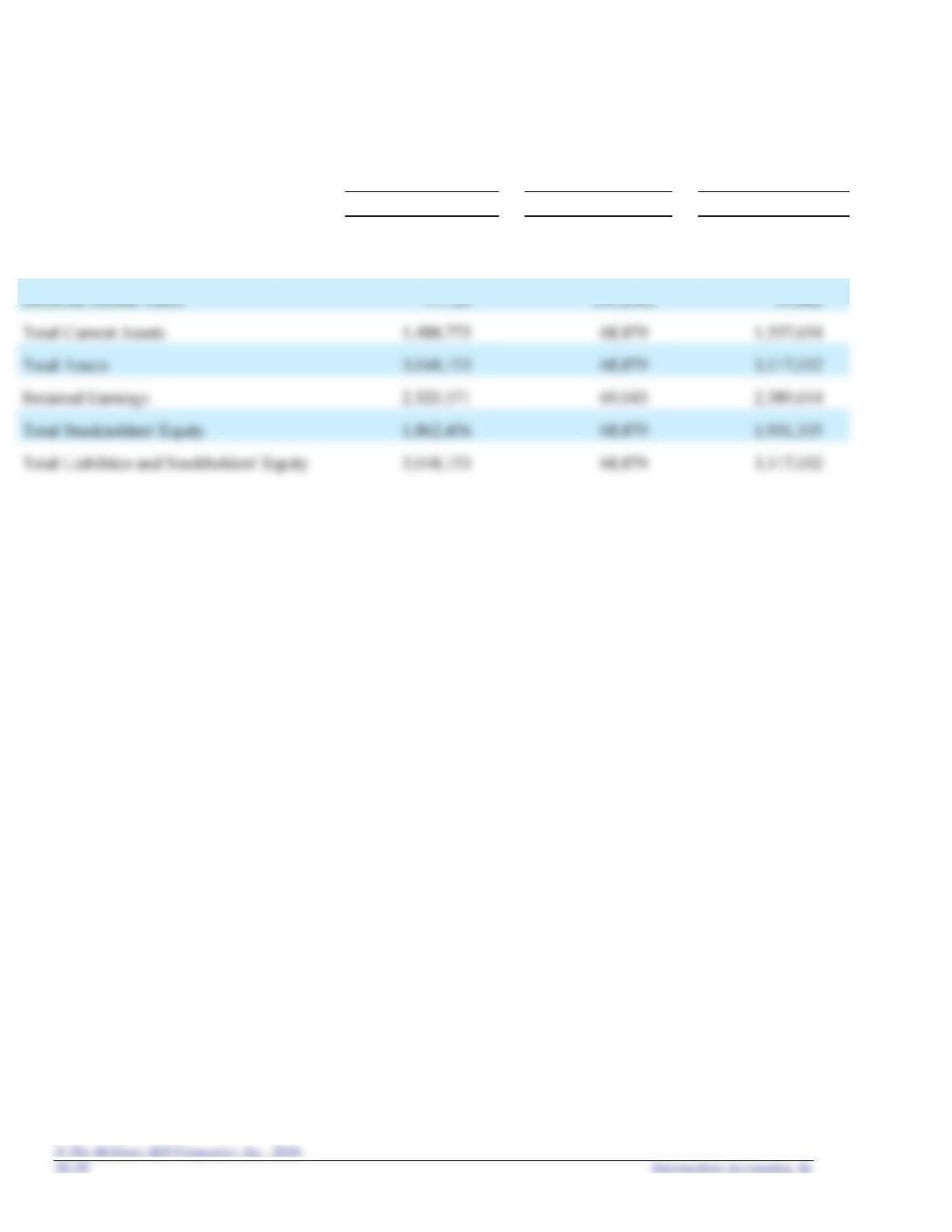

January 28, 2012 (in thousands):

As Reported

Effect of Change

As Restated

Inventories

$

569,818

$

110,117

$

679,935

Deferred Income Taxes

Total Current Assets

Total Assets

Retained Earnings

Total Stockholders’ Equity

Total Liabilities and Stockholders’ Equity

3. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis, and judgment skills.

Communication Skills. Ethics Case 20-3, Research Case 20-7, and Problem 20-10 are suitable

for student presentation(s). In addition to Communication Case 20-5, Research Case 20-7 can

Research Skills. In their professional lives, our graduates will be required to locate and extract

relevant information from available resource material to determine the correct accounting

As a research activity, have students search the internet for examples of reported accounting

changes. You might let them use their own creativity in deciding where to look for examples

or you might suggest:

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

students to gather, assemble, organize, process, or interpret date to provide options for making

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

20–30 Intermediate Accounting, 8e

4. Ethical Dilemmas

A. The chapter contains two ethical dilemmas. The first is:

ETHICAL DILEMMA

The net income of Union Carbide increased in in a single year by over $200 million, due

almost entirely to three changes in accounting principle: (a) the depreciation method was changed,

You may wish to discuss this in class. If so, discussion should include these elements.

Step 1 – The Facts:

The increase in net income of Union Carbide was due almost entirely to: (1) a change in

Step 2 – The Ethical Issue and the Stakeholders:

The ethical issue or dilemma is whether Union Carbide made the changes for the purpose of

Step 3 – Values:

Values include competence, integrity, objectivity, loyalty to the company, responsibility for

following accounting principles, and responsibility to users of financial statements.

Step 4 – Alternatives:

1. Continue the use of previous accounting methods regarding depreciation, interest

Step 5 – Evaluation of Alternatives in Terms of Values:

1. Alternative 1 would have caused significantly lower reported earnings, perhaps reflecting

Step 6 – Consequences:

Alternative 1.

Would have caused significantly lower reported earnings, with possible negative impact

Alternative 2.

Would have caused significantly higher reported earnings, perhaps misleading investors,

Step 7 – Decision:

Student(s) must decide their course of action.

B. The chapter contains two ethical dilemmas. The second is:

ETHICAL DILEMMA

As a second-year accountant for McCormack Chemical Company, you were excited to be

named Assistant Manager of the Agricultural Chemicals Division. After two weeks in your new

position, you were supervising the year-end inventory count when the Senior Manager mentioned

Discussion should include these elements.

Step 1 – Facts:

As a newly promoted Assistant Manager of the Agricultural Chemicals Division of McCormack

Chemical Company, you observe that two carloads of herbicides, deemed to be unsaleable, are

omitted from the ending inventory count. The Senior Manager states that the inventory should be

Step 2 – The Ethical Issue and the Stakeholders:

The ethical issue or dilemma is whether your obligations to obey your superior and support

Step 3 – Values:

Values include competence, honesty, integrity, objectivity, loyalty to employees, loyalty to the

company, and responsibility to users of financial statements.

Step 4 – Alternatives:

1. Follow the suggestion of the Senior Manager to defer the inventory write off until next

Step 5 – Evaluation of Alternatives in Terms of Values:

1. Alternative 1 illustrates loyalty to the employer and fellow employees.

Step 6 – Consequences:

Alternative 1

Positive consequences: You would keep your job and please the Senior Manager. Fellow

employees would keep their jobs and be able to support their families.

Alternative 2

Positive consequences: Users of financial statements would receive more reliable and

Alternative 3

Positive consequences: You maintain your integrity. Users may receive more reliable and

relevant information regarding assets and net income if upper management levels or the audit

Alternative 4

Positive consequences: You maintain your integrity and avoid conflict with management and

Step 7 – Decision:

Student(s) must decide their course of action.

20–34 Intermediate Accounting, 8e

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

t

Learning Est. time

Questions Objective(s) Topic (min.)

20-1

1

Classify accounting changes

5

20-2

1

Three accounting approaches to reporting

accounting changes

5

20-3

2

Change in accounting principle

5

20-4

2

Change in accounting principle

5

20-5

2

Change in accounting principle

5

20-6

3

Change in accounting principle – exception

5

20-8

4

Change in estimate

5

Distinguish between a change in principle and a

5

change in estimate

20-10

5

Change in reporting entity

5

20-11

5

Change in reporting entity

5

20-12

6

Correcting an error

5

20-13

6

Correcting an error

5

20-14

6

Correcting an error

5

20-15

6

Correcting an error

5

20-16

6

Correcting an error

5

20-17

IFRS; Correcting an error

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

20-1

2

Change in inventory methods

5

20-2

2

Change in inventory methods

5

20-3

3

Change in inventory methods

5

20-4

3

Change in depreciation methods

5

20-5

3

Change in depreciation methods

5

20-6

4

Book royalties

5

20-7

4

Warranty expense

5

20-8

4

Change in estimate; useful life of patent

5

20-9

6

Error correction

5

20-10

6

Error correction

5

20-11

6

Error correction

5

20-12

6

Error correction

5

Learning Est. time

Exercises Objective(s) Topic (min.)

20-1

2

Change in inventory methods

15

20-2

2

Change in inventory methods

10

20-3

2

Change from the treasury stock method to

retired stock

10

20-4

2

Change to equity method

15

20-6

2

FASB codification research

15

25

20-9

3

Change in inventory methods; incomplete

information

10

20-11

3

Change in principle; change in depreciation

methods

10

20-12

4

Book royalties

15

20-13

4

Loss contingency

10

20-14

4

Warranty expense

15

20-15

4

Deferred taxes; change in tax rates

10

20-16

4

Accounting change

10

20-17

4

Change in estimate; equipment

20

20-18

Classifying accounting changes

15

20-19

6

Error correction; inventory error

20

6

Error corrections; investment

15

6

Error in amortization schedule

20

20-22

6

Error correction; accrued interest on bonds

15

20-23

6

Error correction; three errors

25

20-24

6

Inventory errors

15

20-25

Classifying accounting changes and errors

15

20–36 Intermediate Accounting, 8e

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

3

Change in depreciation method

3

CPA-2

4

Retrospective restatement

3

CPA-3

4

Change in estimate

3

CPA-4

5

Change in reporting entity

3

CPA-5

6

Error

3

CPA-6

6

Error

3

CPA-7

7

IFRS

3

CPA-8

7

IFRS

3

CPA-9

7

IFRS

3

7

IFRS

3

7

IFRS

3

7

IFRS

3

7

IFRS

3

7

IFRS

3

7

IFRS

3

4

Change in estimate

3

6

Error

3

6

Error

3

Learning Est. time

Problems Objective(s) Topic (min.)

20-1

2

Change in inventory costing methods;

comparative income statements

25

20-2

2

Change in principle; change in method of

accounting for inventories

40

20-3

Change in inventory costing methods;

comparative income statements

25

Change in inventory methods

30

Depletion; change in estimate

40

Accounting changes; six situations

60

Accounting changes; ten situations

25

Inventory error

35

Error; a change in depreciation methods

30

Accounting changes and error correction;

20-12

1, 2, 3, 4, 6

eight situations; tax effects ignored

80

20-13

1, 2, 3, 4, 6

Accounting changes and error correction;

eight situations; tax effects considered

90

20-14

1, 3, 4, 6

Correction of errors; six errors

30

Integrating problem; errors; deferred taxes;

contingency; change in tax rates

Integrating problem; error; depreciation;

Errors; change in estimate; change in

principle; restatement of previous financial

35

Learning Est. time

Cases Objective(s) Topic (min.)

Integrating Case 20-1

2

Change to dollar-value LIFO

25

Communication Case 20-2

2

Change in inventory costing methods

45

Ethics Case 20-3

1 ,2, 3

Softening the blow

20

Analysis Case 20-4

2, 3

Change in inventory costing methods

35

Communication Case 20-5

4

Change in loss contingency; write a memo

30

Analysis Case 20-6

4

Two wrongs make a right?

20

Analysis Case 20-9

Various changes

20

Judgment Case 20-10

1, 2, 3, 4, 5

Accounting changes; independent situations

40

Judgment Case 20-11

6

Inventory errors

20

Ethics Case 20-12

6

Inventory errors

30