Chapter 20

Cost-Volume-Profit Analysis

Review Questions

1. What is a variable cost? Give an example.

Variable costs are costs that increase or decrease in total in direct proportion to increases or

2. What is a fixed cost? Give an example.

Fixed costs are costs that do not change in total over wide ranges of volume. Fixed costs remain

3. What is a mixed cost? Give an example.

Mixed costs are costs that contain both a fixed and variable component. An example of a mixed cost

4. What is the purpose of using the high-low method?

5. Describe the three steps of the high-low method.

The three steps of the high-low method are:

6. What is the relevant range?

7. A chain of convenience stores has one manager per store who is paid a monthly salary. Relative to

Store #36 located in Atlanta, Georgia, is the manager’s salary fixed or variable? Why?

8. A chain of convenience stores has one manager per store who is paid a monthly salary. Relative to

the number of stores, is the manager’s salary fixed or variable? Why?

9. What is contribution margin?

10. What are the three ways contribution margin can be expressed?

The three ways that contribution margin can be expressed are:

11. How does a contribution margin income statement differ from a traditional income statement?

12. What is cost-volume-profit analysis?

13. What are the CVP assumptions?

The CVP assumptions are:

14. What is target profit?

15. What are the three approaches to calculating the sales required to achieve the target profit? Give the

formula for each one.

The three approaches to calculating the sales required to achieve target profit are:

a. The equation approach. The equation is:

16. Of the three approaches to calculate sales required to achieve target profit, which one(s) calculate the

required sales in units and which one(s) calculate the required sales in dollars?

17. What is the breakeven point?

18. Why is the calculation to determine the breakeven point considered a variation of the target profit

calculation?

The calculation to determine breakeven point is considered a variation of the target profit calculation

because the equations and methodology are the same as calculating target profit equal to zero.

19. On the CVP graph, where is the breakeven point shown? Why?

20. What is sensitivity analysis? How do managers use this tool?

Sensitivity analysis is a “what if” technique that estimates profit or loss results if selling price, costs,

21. What effect does an increase in sales price have on contribution margin? An increase in fixed costs?

An increase in variable costs?

22. What is the margin of safety? What are the three ways it can be expressed?

The margin of safety is the excess of expected sales over breakeven sales. The margin of safety can

be expressed in units, in dollars, or as a ratio.

23. What is a company’s cost structure? How can cost structure affect a company’s profits?

The cost structure of a company is the proportion of fixed costs to variable costs. The relationship

24. What is operating leverage? What does it mean if a company has a degree of operating leverage of

3?

Operating leverage predicts the effects that fixed costs have on changes in operating income when

25. How can CVP analysis be used by companies with multiple products?

CVP analysis can be used by companies with multiple products by using the same CVP formulas,

Short Exercises

S20-1 Identifying variable, fixed, and mixed costs

Learning Objective 1

Philadelphia Acoustics builds innovative speakers for music and home theater systems. Identify each

cost as variable (V), fixed (F), or mixed (M), relative to number of speakers produced and sold.

1. Units of production depreciation on routers used to cut wood enclosures.

2. Wood for speaker enclosures.

3. Patents on crossover relays.

4. Total compensation to salesperson who receives a salary plus a commission based on meeting sales

goals.

5. Crossover relays.

6. Straight-line depreciation on manufacturing plant.

7. Grill cloth.

8. Cell phone costs of salesperson.

9. Glue.

10. Quality inspector’s salary.

SOLUTION

1.

Units of production depreciation on routers used to cut wood enclosures.

V

2.

Wood for speaker enclosures.

V

3.

Patents on crossover relays.

6.

Straight-line depreciation on manufacturing plant.

7.

Grill cloth.

V

9.

Glue.

V

S20-2 Identifying variable, fixed, and mixed costs

Learning Objective 1

Holly’s Day Care has been in operation for several years. Identify each cost as variable (V), fixed (F), or

mixed (M), relative to number of students enrolled.

1. Building rent.

2. Toys.

3. Compensation of the office manager, who receives a salary plus a bonus based on number of

students enrolled.

4. Afternoon snacks.

5. Lawn service contract at $200 per month.

6. Holly’s salary.

7. Wages of afterschool employees.

8. Drawing paper for student artwork.

9. Straight-line depreciation on furniture and playground equipment.

10. Fee paid to security company for monthly service.

SOLUTION

1.

Building rent.

F

2.

Toys.

V

based on number of students enrolled.

4.

Afternoon snacks.

V

6.

F

7.

Wages of afterschool employees.

V

9.

Straight-line depreciation on furniture and playground equipment.

F

S20-3 Using the high-low method

Learning Objective 1

Mel owns a machine shop. In reviewing the shop’s utility bills for the past 12 months, he found that the

highest bill of $2,600 occurred in August when the machines worked 1,400 machine hours. The lowest

utility bill of $2,300 occurred in December when the machines worked 900 machine hours.

Requirements

1. Calculate the variable rate per machine hour and the total fixed utility cost.

2. Show the equation for determining the total utility cost for the machine shop.

3. If Mel anticipates using 1,000 machine hours in January, predict the shop’s total utility bill using the

equation from Requirement 2.

SOLUTION

Requirement 1

Variable cost per unit

=

Change in total cost

/

Change in volume of activity

=

(Highest volume – Lowest volume)

=

=

=

Total fixed cost

=

Total mixed cost

=

Total mixed cost

=

=

=

Requirement 2

Total utility cost

=

(Variable cost per unit × Number of units)

+

Total fixed cost

=

($0.60 per MHr × Number of machine hours)

+

$1,760

Total utility cost

=

(Variable cost per unit × Number of units)

+

Total fixed cost

=

+

$1,760

=

+

$1,760

=

S20-4 Calculating contribution margin

Learning Objective 2

Garson Company sells a product for $90 per unit. Variable costs are $60 per unit, and fixed costs are

$800 per month. The company expects to sell 540 units in September. Calculate the contribution margin

per unit, in total, and as a ratio.

SOLUTION

Unit contribution margin

=

Net sales revenue per unit

–

Variable costs per unit

=

$90 per unit

–

$60 per unit

=

$30 per unit

Total contribution margin

=

=

=

=

Contribution margin ratio

=

Contribution margin

Net sales revenue

=

=

Contribution margin ratio

=

Contribution margin

Net sales revenue

=

=

S20-5 Preparing a contribution margin income statement

Learning Objective 2

Gabrick Company sells a product for $30 per unit. Variable costs are $20 per unit, and fixed costs are

$2,500 per month. The company expects to sell 560 units in September. Prepare an income statement for

September using the contribution margin format.

SOLUTION

S20-6 Calculating required sales in units, contribution margin given

Learning Objective 3

Malden, Inc. sells a product with a contribution margin of $60 per unit. Fixed costs are $10,500 per

month. How many units must Malden sell to earn an operating income of $15,000?

SOLUTION

S20-7 Calculating required sales in units, contribution margin ratio given

Learning Objective 3

Summer Company sells a product with a contribution margin ratio of 60%. Fixed costs are $650 per

month. What amount of sales (in dollars) must Summer Company have to earn an operating income of

$7,000? If each unit sells for $30, how many units must be sold to achieve the desired operating income?

SOLUTION

Required sales in dollars

=

Fixed costs + Target profit

Contribution margin ratio

Required sales in dollars

Required sales in units

=

Contribution margin per unit

=

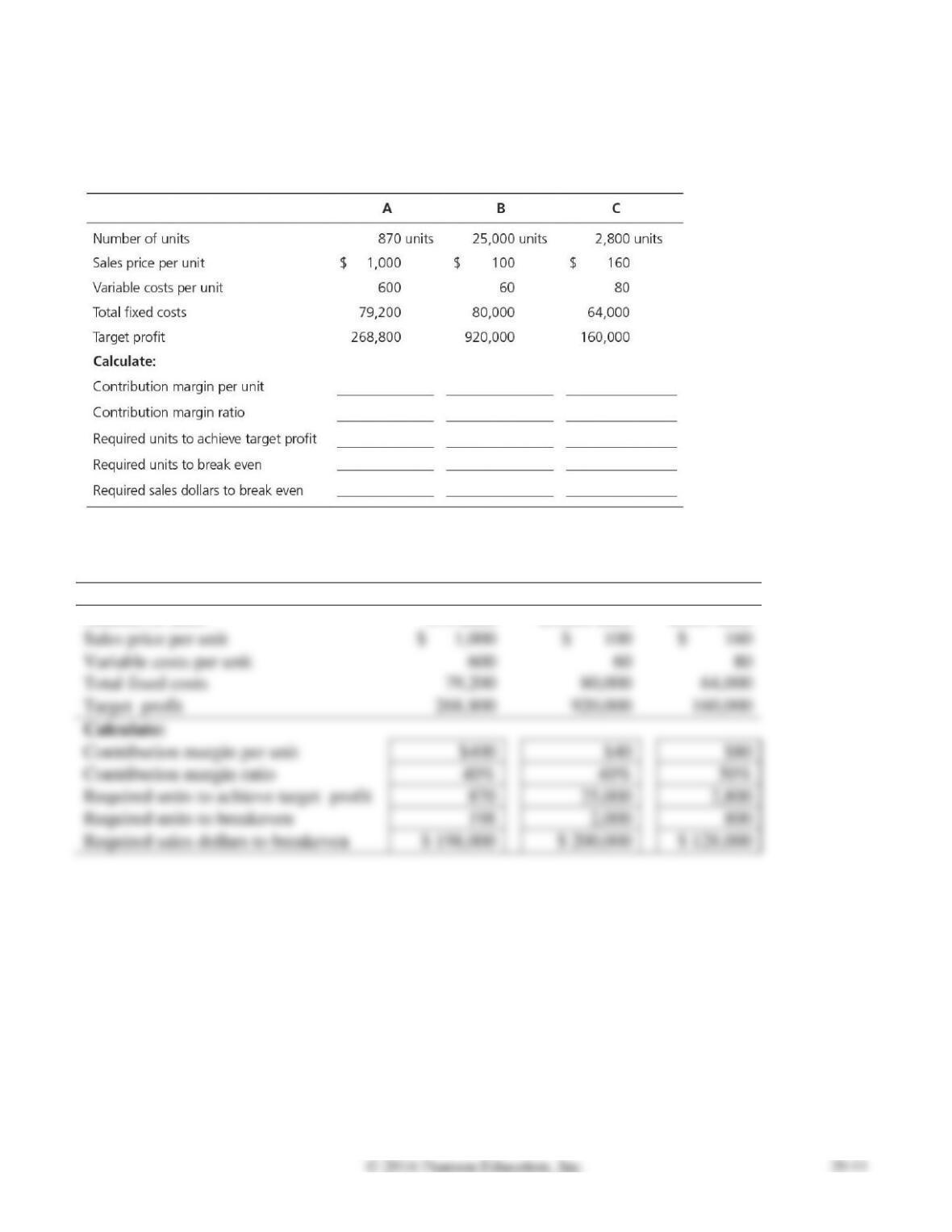

S20-8 Computing contribution margin, units to achieve target profit, and breakeven point

Learning Objectives 2, 3

Compute the missing amounts for the following table.

SOLUTION

A

B

C

Number of units

870 units

25,000 units

2,800 units

Required units to achieve target profit

Use the following information to complete Short Exercises S20-9 through S20-14.

Playtime Park competes with Water World by providing a variety of rides. Playtime Park sells tickets at

$60 per person as a one-day entrance fee. Variable costs are $24 per person, and fixed costs are

$226,800 per month.

S20-9 Computing contribution margin per unit, breakeven point in sales units

Learning Objectives 2, 3

Compute the contribution margin per unit and the number of tickets Playtime Park must sell to break

even. Perform a numerical proof to show that your answer is correct.

SOLUTION

Unit contribution margin

=

Net sales revenue per unit

–

Variable costs per unit

=

$60 per ticket

–

$24 per ticket

=

$36 per ticket

Contribution margin per unit

–

–

Fixed costs

=

Target profit

–

–

=

–

–

=

breakeven point.

S20-10 Computing contribution margin ratio, breakeven point in sales dollars

Learning Objectives 2, 3

Compute Playtime Park’s contribution margin ratio. Carry your computation to two decimal places. Use

the contribution margin ratio approach to determine the sales revenue Playtime Park needs to break

even.

SOLUTION

Utilizing the contribution margin per unit calculated in S20-9:

Contribution margin ratio

S20-11 Applying sensitivity analysis of changing sales price and variable cost

Learning Objective 4

Using the Playtime Park information presented, do the following tasks.

Requirements

1. Suppose Playtime Park cuts its ticket price from $60 to $54 to increase the number of tickets sold.

Compute the new breakeven point in tickets and in sales dollars.

2. Ignore the information in Requirement 1. Instead, assume that Playtime Park in- creases the variable

cost from $24 to $30 per ticket. Compute the new breakeven point in tickets and in sales dollars.

SOLUTION

Requirement 1

Unit contribution margin

=

Net sales revenue per unit

–

Variable costs per unit

=

$54 per ticket

–

$24 per ticket

=

$30 per ticket

Required sales in dollars

=

7,560 tickets × $54 per ticket

=

$408,240

Requirement 2

Unit contribution margin

=

Net sales revenue per unit

–

Variable costs per unit

=

$60 per tablet

–

$30 per tablet

=

$30 per tablet

Contribution margin ratio

=

Contribution margin

Net sales revenue

=

=

Fixed costs + Target profit

Contribution margin ratio

$226,800 + $0

Contribution margin per unit

S20-12 Applying sensitivity analysis of changing fixed costs

Learning Objective 4

Refer to the original information (ignoring the changes considered in Short Exercise S20-11). Suppose

Playtime Park reduces fixed costs from $226,800 per month to $208,800 per month. Compute the new

breakeven point in tickets and in sales dollars.

SOLUTION

Unit contribution margin

=

Net sales revenue per unit

–

Variable costs per unit

=

$60 per ticket

–

$24 per ticket

=

$36 per ticket

Contribution margin per unit

Required sales in dollars

Required sales in units

Sales price per unit

=

×

=

S20-13 Computing margin of safety

Learning Objective 5

Refer to the original information (ignoring the changes considered in Short Exercises S20-11 and S20-

12). If Playtime Park expects to sell 7,000 tickets, compute the margin of safety in tickets and in sales

dollars.

SOLUTION

Utilizing the breakeven sales in units from S20-9:

Expected sales

–

Breakeven sales

=

Margin of safety in units

–

=

Margin of safety in units

Sales price per unit

=

=

S20-14 Computing degree of operating leverage

Learning Objective 5

Refer to the original information (ignoring the changes considered in Short Exercises S20-11 and S20-

12). If Playtime Park expects to sell 7,000 tickets, compute the degree of operating leverage. Estimate

the operating income if sales increase by 15%.

SOLUTION

Net sales revenue

–

Variable costs

–

Fixed costs

=

Target profit

(7,000 tickets × $60/ticket)

–

(7,000 tickets × $24/ticket)

–

$226,800

=

$420,000

–

$168,000

–

$226,800

=

$25,200

$25,200

$25,200

Operating leverage

15%

Operating income

+

Increase in operating income

+

$37,800

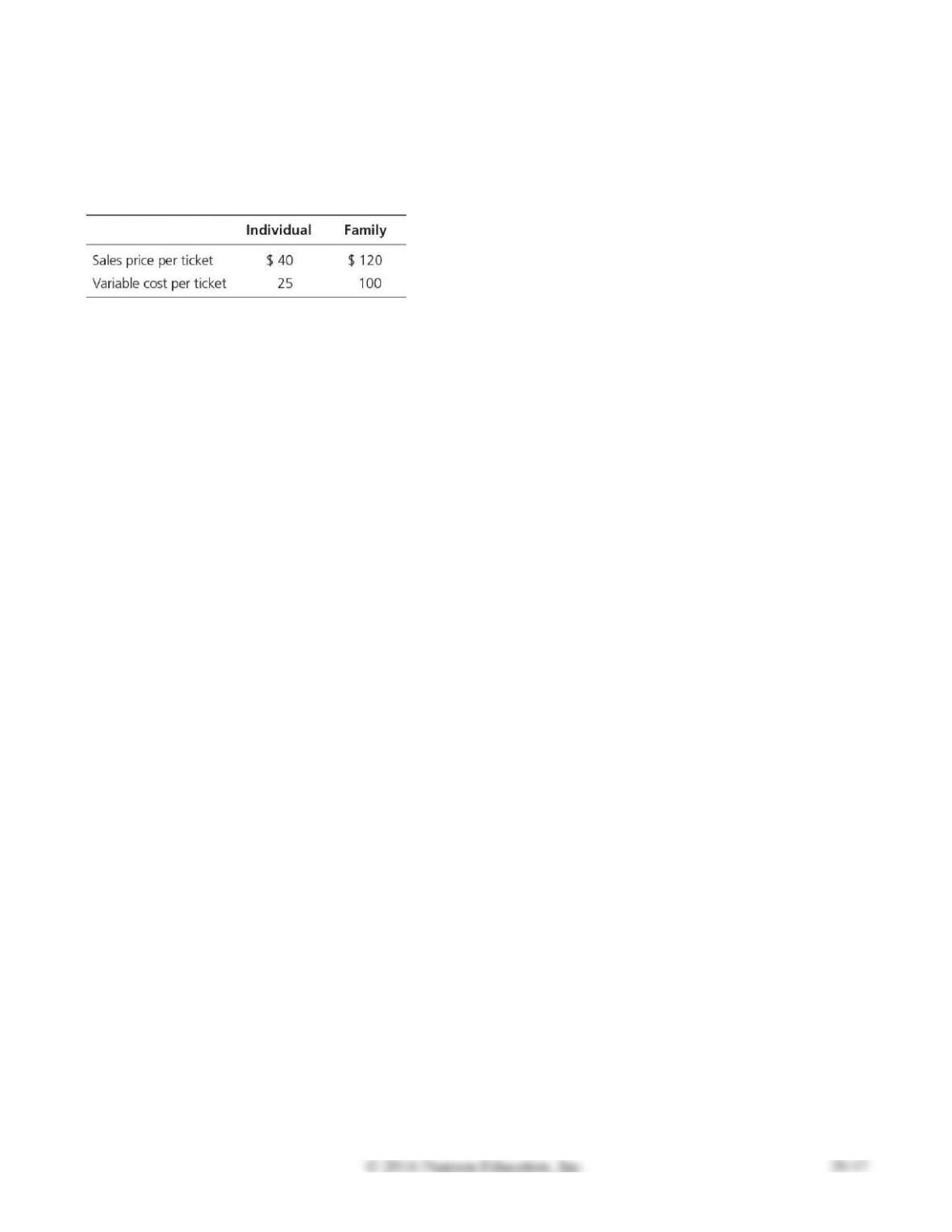

Use the following information to complete Short Exercises S20-15 and S20-16.

SoakNFun Swim Park sells individual and family tickets. With a ticket, each person receives a meal,

three beverages, and unlimited use of the swimming pools. SoakNFun has the following ticket prices

and variable costs for 2016:

SoakNFun expects to sell one individual ticket for every four family tickets. SoakNFun’s total fixed

costs are $76,000.

S20-15 Calculating breakeven point for two products

Learning Objective 5

Using the SoakNFun Swim Park information presented, do the following tasks.

Requirements

1. Compute the weighted-average contribution margin per ticket.

2. Calculate the total number of tickets SoakNFun must sell to break even.

3. Calculate the number of individual tickets and the number of family tickets the company must sell to

break even.

SOLUTION

Requirement 1

Individual

Family

Total

Sales price per unit

Variable cost per unit

Contribution margin per unit

Sales mix in units

Contribution margin

Weighted-average contribution margin per unit

($95 / 5 units)

Requirement 2

Required sales in units

=

Fixed costs + Target profit

Contribution margin per unit

=

4,000 tickets

Required sales of family tickets

=

4,000 tickets × 4/5

=

S20-16 Calculating breakeven point for two products

Learning Objective 5

For 2017, SoakNFun expects a sales mix of four individual tickets for every one family ticket.

Requirements

1. Compute the new weighted-average contribution margin per ticket.

2. Calculate the total number of tickets SoakNFun must sell to break even.

3. Calculate the number of individual tickets and the number of family tickets the company must sell to

break even.

SOLUTION

Requirement 1

Individual

Family

Total

Sales price per unit

$ 40

$ 120

Variable cost per unit

Contribution margin per unit

Sales mix in units

Contribution margin

$ 60

Weighted-average contribution margin per unit

($80 / 5 units)

Requirement 2

Required sales in units

=

Fixed costs + Target profit

Contribution margin per unit

=

4,750 tickets

Required sales of family tickets

=

4,750 tickets × 1/5

=

950 tickets

Exercises

E20-17 Using terminology

Learning Objectives 1, 2, 3, 4, 5

Match the following terms with the correct definitions:

SOLUTION

1.

Costs that do not change in total over wide ranges of volume.

g.

Fixed costs

2.

Technique that estimates profit or loss results when conditions

change.

i.

Sensitivity

analysis

3.

The sales level at which operating income is zero.

Breakeven point

4.

Drop in sales a company can absorb without incurring an

operating loss.

d.

Margin of safety

5.

Combination of products that make up total sales.

Sales mix

6.

Net sales revenue minus variable costs.

b.

Contribution

margin

7.

Describes how a cost changes as volume changes.

Cost behavior

8.

Costs that change in total in direct proportion to changes in

volume.

h.

Variable costs