C

CH

HA

AP

PT

TE

ER

R

2

20

0

A

Ac

cc

co

ou

un

nt

ti

in

ng

g

C

Ch

ha

an

ng

ge

es

s

a

an

nd

d

E

Er

rr

ro

or

r

C

Co

or

rr

re

ec

ct

ti

io

on

ns

s

Overview

Chapter 4 provided an overview of accounting changes and error correction. Later, we discussed

changes encountered in connection with specific assets and liabilities as we dealt with those topics in

subsequent chapters.

Now, in this chapter, we revisit accounting changes and error correction with the intent to

Learning Objectives

After studying this chapter, you should be able to:

LO20-1 Differentiate among the three types of accounting changes and distinguish between the

retrospective and prospective approaches to accounting for and reporting accounting

changes.

LO20-2 Describe how changes in accounting principle typically are reported.

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

I. Accounting changes fall into one of three categories. (T20-1)

A. Changes in principle.

B. Changes in estimates.

C. Changes in reporting entity.

20-2 Intermediate Accounting, 8e

A. For each year reported in the comparative statements, we revise those statements to appear as if

the newly adopted accounting method had been applied all along. (T20-4) (T20-5) (T20-6)

B. In addition to reporting revised amounts in the comparative financial statements, we must also

adjust the book balances of affected accounts. This means creating a journal entry to change

IV. EXCEPTIONS NECESSITATING THE PROSPECTIVE APPROACH

A. Sometimes a lack of information makes it impracticable to report a change retrospectively so

the new method is simply applied prospectively. (T20-9)

1. If it’s impracticable to adjust each year reported, the change is applied retrospectively as of

B. Another exception to retrospective application is when an FASB Statement or another

authoritative pronouncement requires prospective application for specific changes in

accounting methods.

C. We account for a change in depreciation method as a change in accounting estimate that is

achieved by a change in accounting principle. Therefore, we account for such a change

prospectively; that is, precisely the way we account for changes in estimates.

V. Changes in estimates are accounted for prospectively.

VIII. When errors are discovered, they should be corrected and accounted for retrospectively.

(T20-14) Illustrations: T20-15, T20-16, T20-17, T20-18

A. A journal entry is made to correct any account balances that are incorrect as a result of

20-4 Intermediate Accounting, 8e

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

ACCOUNTING CHANGES

Type of

Change

Description

Examples

Change in

Change from

➢ adopt a new FASB standard

➢ change methods of inventory

Change in

estimate

Revision of an

estimate because

of new

information or

new experience

➢ change depreciation methods

➢ change estimate of useful life

of depreciable asset

➢ change estimate of residual

value

➢ change estimate of warranty

expense percentage

➢ change estimate of periods

Graphic 20-1 T20-1

20-6 Intermediate Accounting, 8e

CORRECTION OF AN ERROR

Type

Description

Examples

Correction of an

➢ mathematical mistakes

➢ inaccurate physical count

of inventory

T20-2

CHANGE IN ACCOUNTING PRINCIPLE

Although consistency and comparability are desirable,

changing to a new method sometimes is appropriate.

T20-3

20-8 Intermediate Accounting, 8e

Illustration

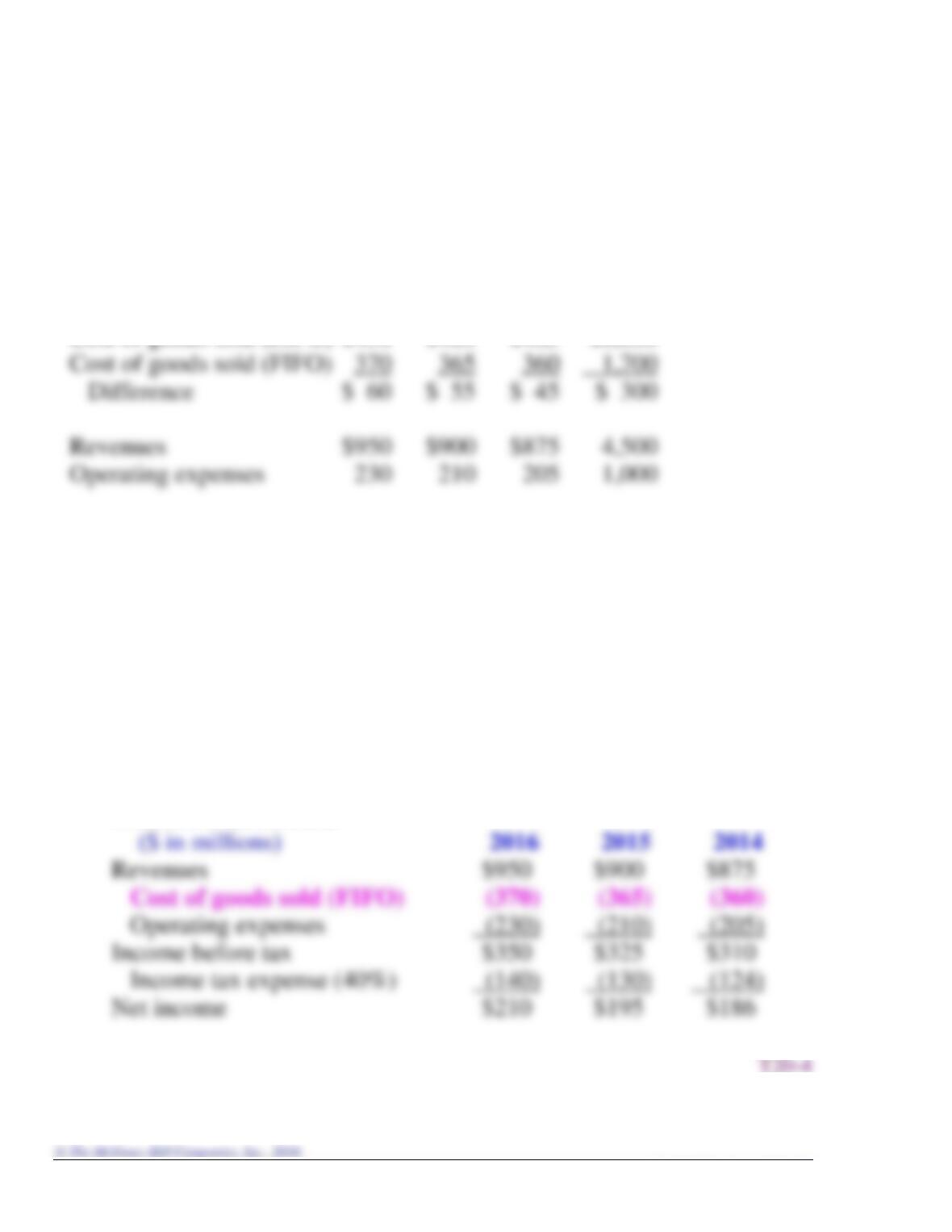

Air Parts Corporation used the LIFO inventory costing method.

At the beginning of 2016, Air Parts decided to change to the

FIFO method. Income components for 2016 and prior years

were as follows ($ in millions):

previous

2016 2015 2014 years

Cost of goods sold (LIFO) $430 $420 $405 $2,000

Air Parts has paid dividends of $40 million each year beginning

in 2006. Its income tax rate is 40%. Retained earnings on

January 1, 2014, was $700 million; inventory was $500 million.

For each year reported in the comparative statements, Air

Parts makes those statements appear as if the newly adopted

accounting method (FIFO) had been applied all along.

Income Statements

Balance Sheets

Inventory. Air Parts will report 2016 inventory by its newly

adopted method, FIFO, and also will revise the amounts it

reported last year for its 2015 and 2014 inventory. Each

year, inventory will be higher than it would have been by

LIFO.

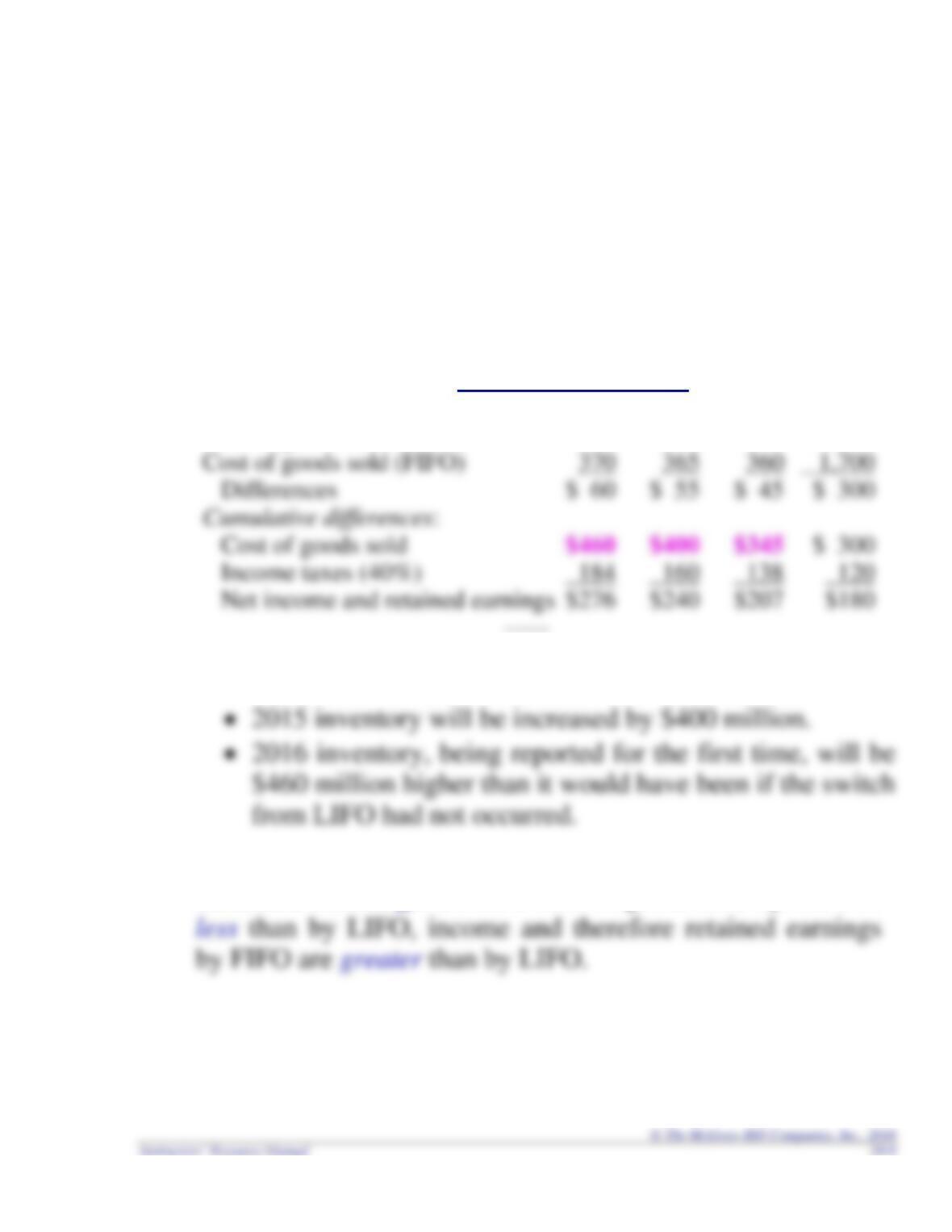

Years ending Dec. 31: previous

($ in millions) 2016 2015 2014 years

Cost of goods sold (LIFO) $430 $420 $405 $2,000

• 2014 inventory will be $345 million higher than it was

reported in last year’s statements.

Retained Earnings. Because cost of goods sold by FIFO is

T20-5

20–10 Intermediate Accounting, 8e

Statements of Shareholders’ Equity

If adjustment due to a change in accounting principle (and it

The January 1, 2014, retained earnings balance reported in

the comparative statements of shareholders’ equity below

($ in millions)

Common

Stock

Additional

Paid-in

Capital

Retained

Earnings

Total

SE

Jan. 1, 2014

$ 880

Net income (revised to FIFO)

186

Dividends

(40)

Dec. 31, 2014

Net income (revised to FIFO)

195

Dividends

(40)

Dec. 31, 2015

Dividends

(40)

Dec. 31, 2016

T20-6

Adjust Accounts for the Change

The journal entry updates inventory, retained earnings, and the

income tax liability for revisions resulting from differences in the

LIFO and FIFO methods prior to the switch, pre-2016.

Cumulative Cumulative

Difference Difference

($ in millions) 2015 2014 pre-2014 pre-2016

Journal entry to record the change in principle.

January 1, 2016

($ in millions)

Inventory (additional inventory if FIFO had been used) 400

T20-7

20–12 Intermediate Accounting, 8e

DISCLOSURE NOTE

In the first set of financial statements after the change, a

disclosure note is needed to provide justification that the

new method is clearly preferable.

EXCEPTIONS NECESSITATING THE PROSPECTIVE APPROACH

1. WHEN RETROSPECTIVE APPLICATION IS IMPRACTICABLE

Sometimes a lack of information makes it impracticable to report a

change retrospectively so the new method is simply applied

2. WHEN MANDATED BY AUTHORITATIVE PRONOUNCEMENTS

Another exception to retrospective application is when a new

3. CHANGING DEPRECIATION, AMORTIZATION, DEPLETION

METHODS

We account for a change in depreciation method as a change in

T20-9

CHANGE IN ACCOUNTING ESTIMATE

20–14 Intermediate Accounting, 8e

Changes in estimates are accounted for prospectively.

When a company revises a previous estimate, prior

Illustration

CHANGE IN ACCOUNTING ESTIMATE

Universal Semiconductors estimates warranty expense as 2%

of credit sales. After a review during 2016, Universal

determined that 3% of credit sales is a more realistic

estimate of its payment experience. Credit sales in 2016 are

$300 million. The effective income tax rate is 40%.

($ in millions)

Warranty expense (3% x $300 million) 9

Warranty liability 9

20–16 Intermediate Accounting, 8e

CHANGE IN REPORTING ENTITY

A reporting entity can be a single company, or it can be a

group of companies that reports a single set of financial

statements. A change in reporting entity occurs as a result

of:

(1) Presenting consolidated financial statements in place of

Reported by restating all previous periods’ financial

statements as if the new reporting entity existed in those

periods.

APPROACHES TO REPORTING ACCOUNTING

CHANGES AND ERROR CORRECTIONS

Current

Previous Years Year Later Years

______________________________________________________________

T20–13

20–18 Intermediate Accounting, 8e

ERROR CORRECTION

Steps to Correct an Error:

A journal entry is made to correct any account balances

that are incorrect as a result of the error.

If retained earnings is one of the accounts incorrect as a

result of the error, the correction is reported as a “prior

T20–14

ERROR DISCOVERED IN THE SAME REPORTING

PERIOD THAT IT OCCURRED

If an accounting error is made and discovered in the same

accounting period, the original erroneous entry should

To reverse erroneous entry($ in millions)

Cash ………………………………………………………………. 3

Maintenance expense ……………………………………. 3