Exercise 2–9

1. Interest receivable ($90,000 x 8% x 3/12) ………………….. 1,800

Interest revenue …………………………………………….. 1,800

2. Rent expense ($6,000 x 2/3) …………………………………… 4,000

Exercise 2–10

1. $7,200 represents nine months of interest on a $120,000 note, or 75% of

annual interest.

2. $60,000 ÷ 12 months = $5,000 per month in rent

$35,000 ÷ $5,000 = 7 months expired. The rent was paid on June 1, seven

months ago.

3. $500 represents two months (November and December) in accrued interest, or

2–22 Intermediate Accounting, 8/e

Exercise 2–11

1. Insurance expense ($6,000 x 3/12) …………………………... 1,500

Prepaid insurance …………………………………………… 1,500

2. Interest expense ($80,000 x 8% 3/12) ………………………. 1,600

Exercise 2–12

Requirement 1

BLUEBOY CHEESE CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ………………………………………..

$800,000

Cost of goods sold …………………………………

480,000

Gross profit …………………………………………..

320,000

$120,000

215,000

Other expense:

Net income ……………………………………………

$101,000

Exercise 2–12 (continued)

BLUEBOY CHEESE CORPORATION

Balance Sheet

At December 31, 2016

Assets

Current assets:

Cash ………………………………………………….

$ 21,000

Accounts receivable …………………………….

300,000

Inventory …………………………………………….

Prepaid rent ………………………………………..

Property and equipment:

Office equipment ………………………………..

Less: Accumulated depreciation ……………

$731,000

Liabilities and Shareholders’ Equity

Current liabilities:

Accounts payable ………………………………..

$ 60,000

Salaries payable ………………………………….

8,000

Common stock ……………………………………

Retained earnings ……………………………….

$731,000

Exercise 2–12 (concluded)

Requirement 2

December 31, 2016

Sales revenue ………………………………………………………... 800,000

Income summary ……………………………………………….. 800,000

Income summary …………………………………………………… 699,000

2–26 Intermediate Accounting, 8/e

Exercise 2–13

December 31, 2016

Sales revenue …………………………………………………………. 750,000

Interest revenue ……………………………………………………… 3,000

Income summary ………………………………………………… 753,000

Exercise 2–14

December 31, 2016

Sales revenue ………………………………………………………... 492,000

Interest revenue ……………………………………………………… 6,000

Gain on sale of investments ……………………………………. 8,000

Income summary ……………………………………………….. 506,000

Exercise 2–15

Requirement 1

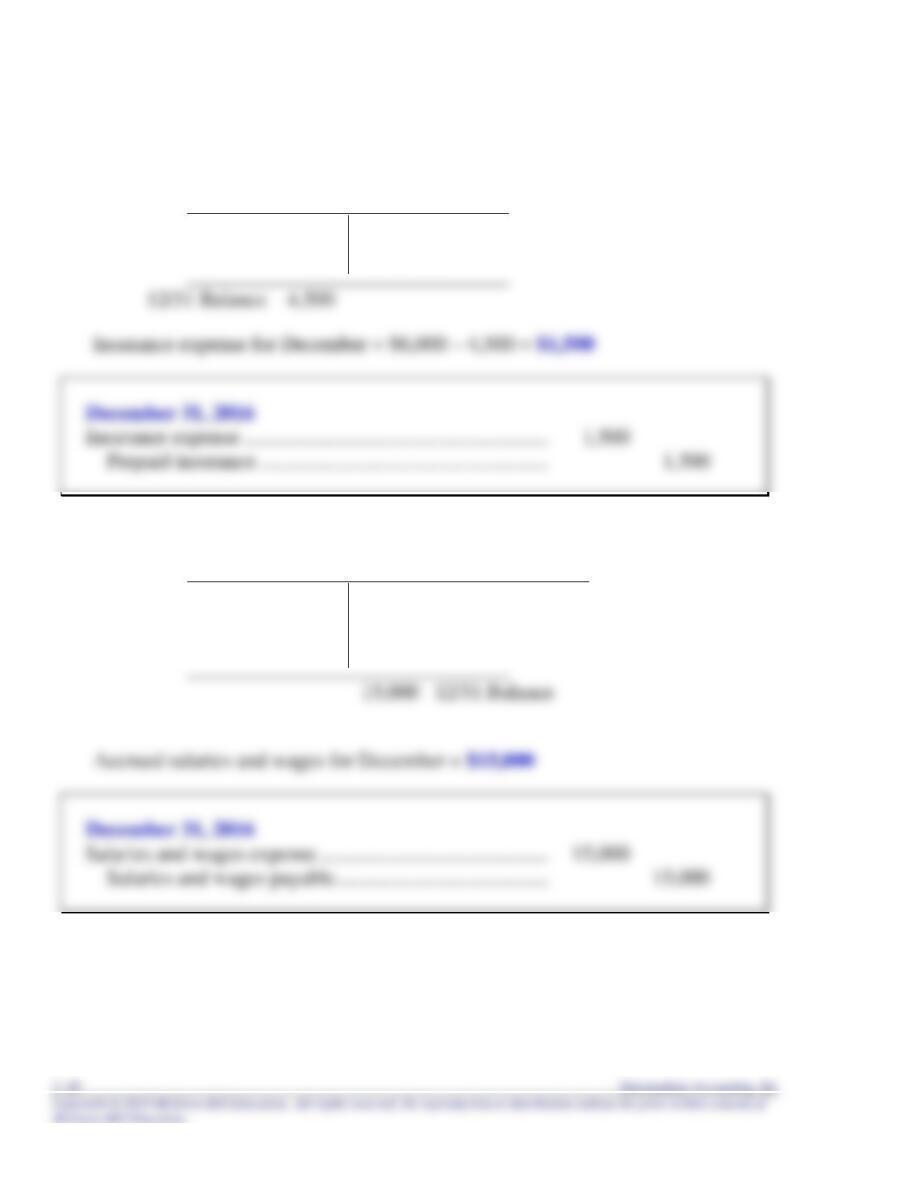

Supplies

11/30 Balance 1,500

Exercise 2–15 (continued)

Requirement 2

Prepaid insurance

11/30 Balance 6,000

Expense ?

Requirement 3

Salaries and wages payable

10,000 11/30 Balance

Salaries and wages paid 10,000 ? Accrued salaries and wages

Exercise 2–15 (concluded)

Requirement 4

Deferred rent revenue

2,000 11/30 Balance

Recognized for Dec. 1,000

2–30 Intermediate Accounting, 8/e

Exercise 2–16

Requirement 1

2016

Debit

Credit

Feb. 1

Cash …………………………………………….

12,000

Note payable ……………………………..

12,000

Prepaid insurance …………………………..

3,600

Cash ………………………………………….

3,600

Supplies ……………………………………….

2,800

Accounts payable ………………………..

2,800

Note receivable ……………………………..

6,000

Cash ………………………………………….

6,000

Requirement 2

2016

Debit

Credit

Dec. 31

Interest expense ($12,000 x 10% x 11/12)

1,100

Interest payable …………………………..

1,100

Dec. 31

Insurance expense ($3,600 x 9/24) ………

1,350

Prepaid insurance ……………………….

1,350

Dec. 31

Supplies expense ($2,800 – 1,250) ……….

1,550

1,550

Dec. 31

Interest receivable ………………………….

Exercise 2–17

Unadjusted net income $30,000

Adjustments:

Exercise 2–18

Stanley and Jones Lawn Service Company

Income Statement

For the Year Ended December 31, 2016

Sales revenue (1) …………………………………….

$315,000

Operating expenses:

$180,000

Operating income ………………………………….

Other expense:

Net income …………………………………………..

(1) $320,000 cash collected less $5,000 decrease in accounts receivable.

(2) $25,000 cash paid for the purchase of supplies less $500 increase in supplies.

Exercise 2–18 (concluded)

(3) $6,000 cash paid for insurance less $2,000 ending balance in prepaid insurance.

(4) $20,000 cash paid for miscellaneous expenses plus increase in accrued liabilities.

Exercise 2–19

Cash basis income ($545,000 – 412,000) $133,000

Add:

Exercise 2–20

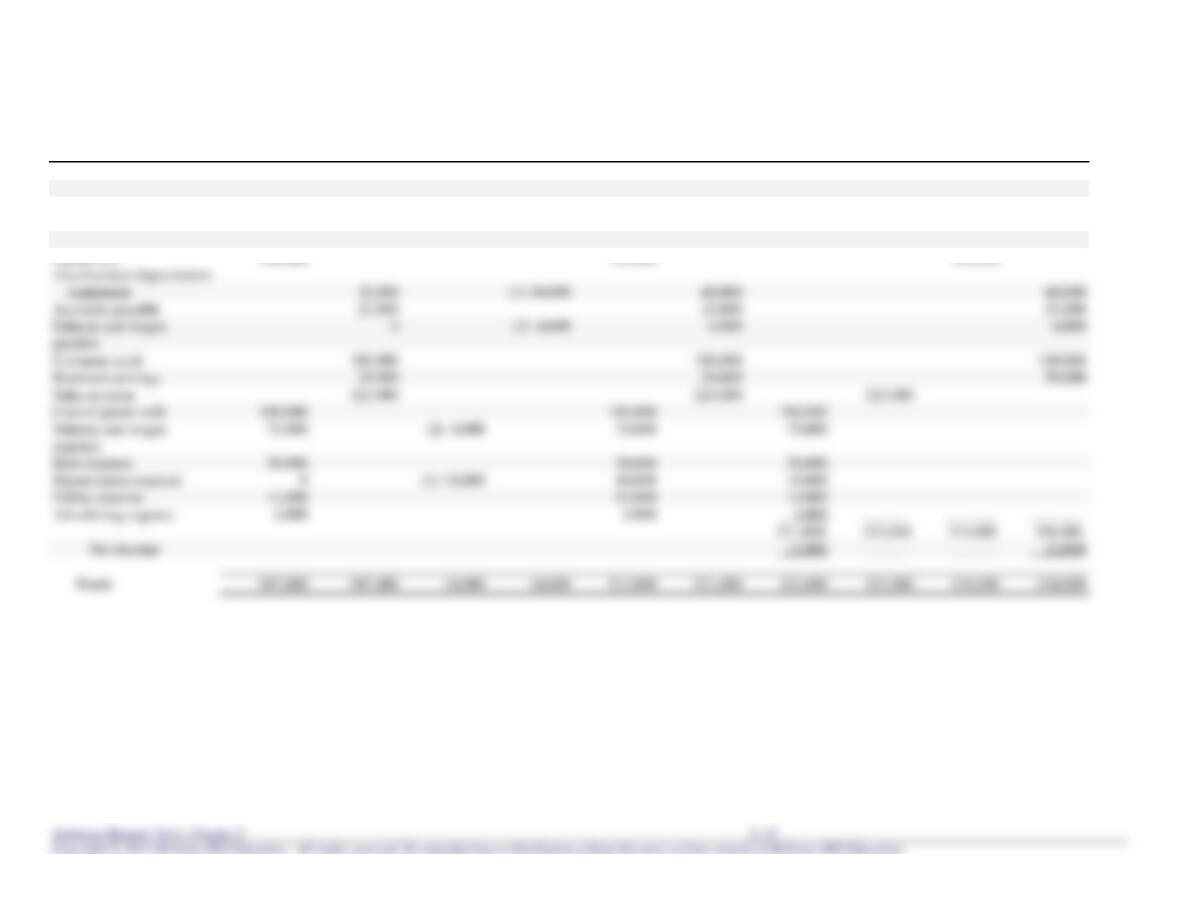

Requirement 1

Account Title

Unadjusted Trial Balance

Adjusting Entries

Adjusted Trial Balance

Income Statement

Balance Sheet

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash

20,000

20,000

20,000

Accounts receivable

35,000

35,000

35,000

Prepaid rent

5,000

5,000

5,000

Inventory

50,000

50,000

50,000

Equipment

30,000

40,000

40,000

Accounts payable

25,000

25,000

25,000

payable

Common stock

Retained earnings

29,000

29,000

Sales revenue

Cost of goods sold

Rent expense

30,000

30,000

30,000

Depreciation expense

10,000

10,000

Utility expense

12,000

12,000

12,000

Advertising expense

4,000

4,000

14,000

14,000

2–36 Intermediate Accounting, 8/e

Exercise 2–20 (continued)

Requirement 2

WOLKSTEIN DRUG COMPANY

Income Statement

For the Year Ended December 31, 2016

Sales revenue ………………………………………..

$323,000

Cost of goods sold …………………………………

180,000

Gross profit …………………………………………..

Operating expenses:

Net income …………………………………………..

Exercise 2–20 (concluded)

WOLKSTEIN DRUG COMPANY

Balance Sheet

At December 31, 2016

Assets

Current assets:

Cash …………………………………………………….

$ 20,000

Accounts receivable ………………………………

Inventory …………………………..…………………

Prepaid rent ………………………………………….

Property and equipment:

Equipment ……………………………………………

Less: Accumulated depreciation

$170,000

Liabilities and Shareholders’ Equity

Current liabilities:

Accounts payable ………………………………….

$ 25,000

Salaries and wages payable …………………….

Common stock ……………………………………..

Retained earnings ………………………………….

$170,000

*Beginning balance of $29,000 plus net income of $12,000.

Exercise 2–21

Requirement 1

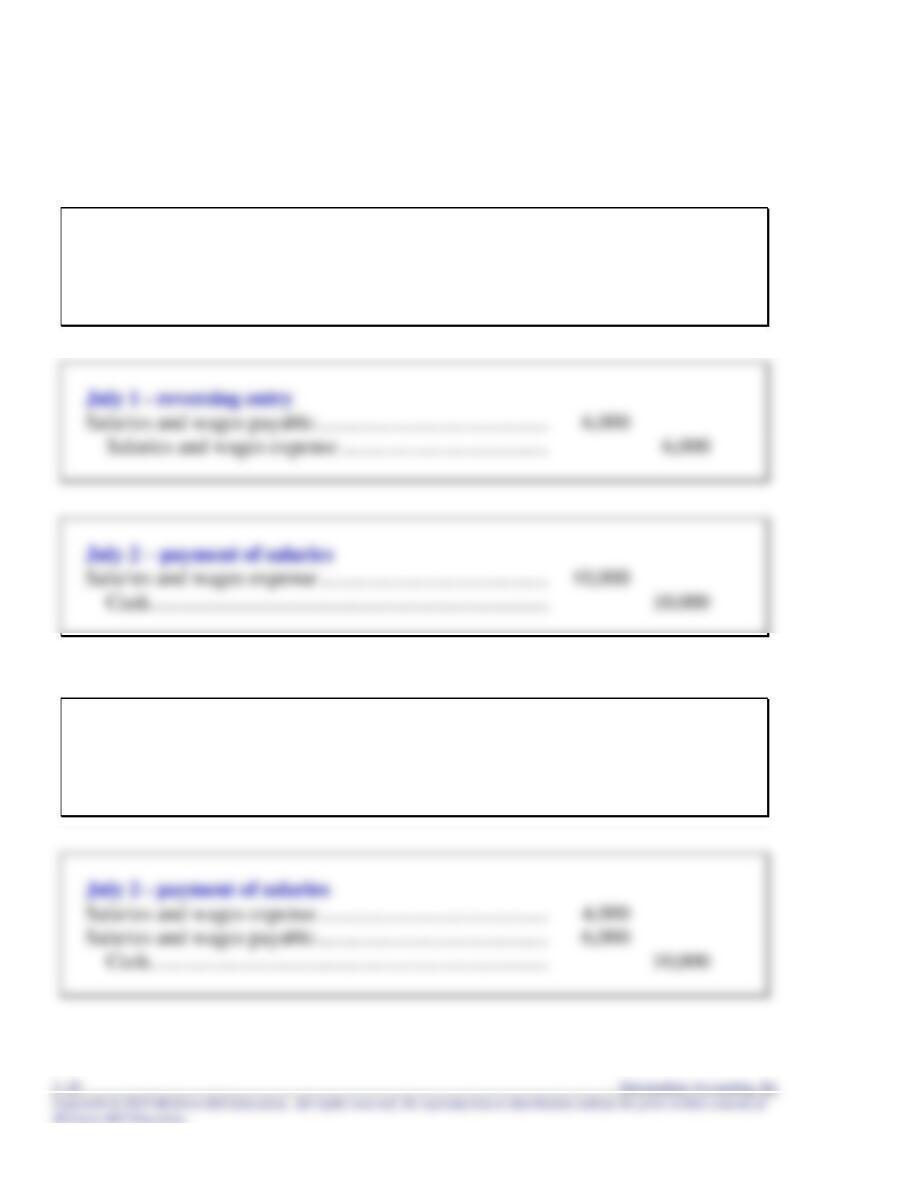

June 30 – adjusting entry

Salaries and wages expense ($10,000 x 3/5) ………………….. 6,000

Salaries and wages payable ………………………………….. 6,000

Requirement 2

June 30 – adjusting entry

Salaries and wages expense …………………………………….. 6,000

Salaries and wages payable ………………………………….. 6,000

Exercise 2–22

Requirement 1

The accountant would reverse adjusting entry 1, the accrual of interest receivable, and

Requirement 2

1. Interest receivable ($90,000 x 8% x 3/12) …………………. 1,800

Requirement 3

1. Interest revenue ……………………………………………….. 1,800

Exercise 2–23

Requirement 1

The transactions affected would be the prepayment of rent, transaction 2, and the

purchase of supplies in transaction 6.

Requirement 2

2. Original transaction on November 1:

Adjusting entry on December 31:

Supplies ……………………………………………………….….. 3,250

Supplies expense …………………………………………… 3,250

Requirement 3

2. Rent expense ……………………………………………………. 2,000