2-1

CHAPTER 2

Financial Statements

and the Annual Report

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Outcomes Exercises Minutes Level

Module 1

1. Describe the objectives of financial reporting.

Module 2

3. Explain the concept and purpose of a classified balance sheet 2 10 Mod

and prepare the statement. 3 10 Easy

Module 3

5. Explain the difference between a single-step and a 6 10 Easy

multiple-step income statement and prepare each type 7 10 Mod

of income statement. 12* 10 Mod

13* 15 Mod

14* 5 Easy

Module 4

9. Read and use the financial statements and other elements 11 20 Diff

in the annual report of a publicly held company.

2-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Outcomes Alternates Minutes Level

Module 1

1. Describe the objectives of financial reporting. 12* 45 Diff

Module 2

3. Explain the concept and purpose of a classified balance sheet 3 50 Mod

and prepare the statement.

Module 3

5. Explain the difference between a single-step and a 6 30 Mod

multiple-step income statement and prepare each type 7 45 Mod

of income statement. 11* 20 Mod

prepare the statement. 12* 45 Diff

Module 4

9. Read and use the financial statements and other elements 9 30 Diff

in the annual report of a publicly held company.

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-3

Estimated

Time in

Learning Outcomes Cases Minutes Level

Module 1

1. Describe the objectives of financial reporting.

Module 2

3. Explain the concept and purpose of a classified balance sheet

and prepare the statement.

Module 3

5. Explain the difference between a single-step and a

multiple-step income statement and prepare each type

of income statement.

Module 4

9. Read and use the financial statements and other elements 4 20 Mod

in the annual report of a publicly held company.

2-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 2 EXERCISE 2-1 CHARACTERISTICS OF USEFUL ACCOUNTING INFORMATION

1. materiality 4. consistency

LO 3 EXERCISE 2-2 THE OPERATING CYCLE

1. For a company that sells a product, the operating cycle begins when the cash is in-

vested in inventory and ends when cash is collected by the company from its cus-

2. The operating cycle for Baxter, the manufacturer of the bikes, would normally be

longer than Two Wheeler’s. This is because a manufacturer incurs various costs to

LO 3 EXERCISE 2-3 CLASSIFICATION OF FINANCIAL STATEMENT ITEMS

1. CA 6. NCA

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-5

LO 4 EXERCISE 2-4 CURRENT RATIO

1. Current Ratio = Current Assets/Current Liabilities

December 31, 2015:

2. Baldwin’s current ratio decreased from 2.0 at the end of 2015 to 1.5 at the end of

2016. In general, the higher the current ratio, the more liquid the company.

3. Cash decreased by 50%, from $6,000 to $3,000, and accounts receivable increased

LO 3 EXERCISE 2-5 CLASSIFICATION OF ASSETS AND LIABILITIES

1. CA 4. NCA 7. CA

LO 5 EXERCISE 2-6 SELLING EXPENSES AND GENERAL AND ADMINISTRATIVE EXPENSES

1. Advertising expense—S

2. Depreciation expense—store furniture and fixtures—S

3. Office rent expense—G&A

2-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 2-7 MISSING INCOME STATEMENT AMOUNTS

Sara’s Amy’s Jane’s

Coffee Shop Deli Bagels

Net sales $35,000 (3) $63,000 $78,000

Cost of goods sold (1) 28,000 45,000 (7) 39,000

Solved as follows (in the order listed):

(1) $35,000 – $7,000 = $28,000

(2) $3,000 + $1,500 = $4,500

LO 6 EXERCISE 2-8 INCOME STATEMENT RATIO

Profit margin:

Net Income/Revenues = $45,000*/$134,800 = 33.4%

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-7

LO 7 EXERCISE 2-9 STATEMENT OF RETAINED EARNINGS

LANDON CORPORATION

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2016

Retained earnings, January 1, 2016……………………………. $130,520*

Net income for 2016 …………………………………………………. 145,480

Dividends declared and paid ……………………………………… (40,000)

Retained earnings, December 31, 2016 ………………………. $236,000

LO 8 EXERCISE 2-10 COMPONENTS OF THE STATEMENT OF CASH FLOWS

1. Paid for supplies—O

2. Collected cash from customers—O

2-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 9 EXERCISE 2-11 BASIC ELEMENTS OF FINANCIAL REPORTS

1. Management discussion and analysis—The information in this section of the an-

nual report is prepared by management and is management’s opportunity to explain

various items that appear in the financial statements. Increases and decreases in

various items are highlighted and reasons for these changes are given. The informa-

tion in this section is not subject to any outside review or support. Users must rely on

the integrity of management that the information contained in the report is reliable.

2. Product/markets of company—Management provides information in the annual

report about the company’s products and markets. The detail provided by manage-

3. Financial statements—These are the responsibility of management and are nor-

mally prepared by the controller. They include the income statement, balance sheet,

statement of changes in stockholders’ equity, and statement of cash flows. The in-

formation provided in the financial statements is subject to verification as part of the

external audit.

4. Notes to financial statements—These are also the responsibility of management,

and they include detailed explanations about the various items appearing in the

5. Independent accountants’ report—As the name implies, this report is prepared by

the independent auditors. It includes information about the scope of the audit (the

statements included in the audit), the auditing standards followed in conducting the

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-9

MULTI-CONCEPT EXERCISES

LO 3,5,7 EXERCISE 2-12 FINANCIAL STATEMENT CLASSIFICATION

BS = Balance sheet; IS = Income statement; RE = Retained earnings statement

1. Accounts payable—BS 11. Land held for future expansion—BS

5. Bonds payable—BS 15. Patent amortization expense—IS

6. Buildings—BS 16. Prepaid insurance—BS

7. Cash—BS 17. Retained earnings—BS and RE

LO 5,6 EXERCISE 2-13 SINGLE- AND MULTIPLE-STEP INCOME STATEMENT

1. Sales—B 7. Net income—B

2. Cost of goods sold—B 8. Supplies on hand—N

2-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

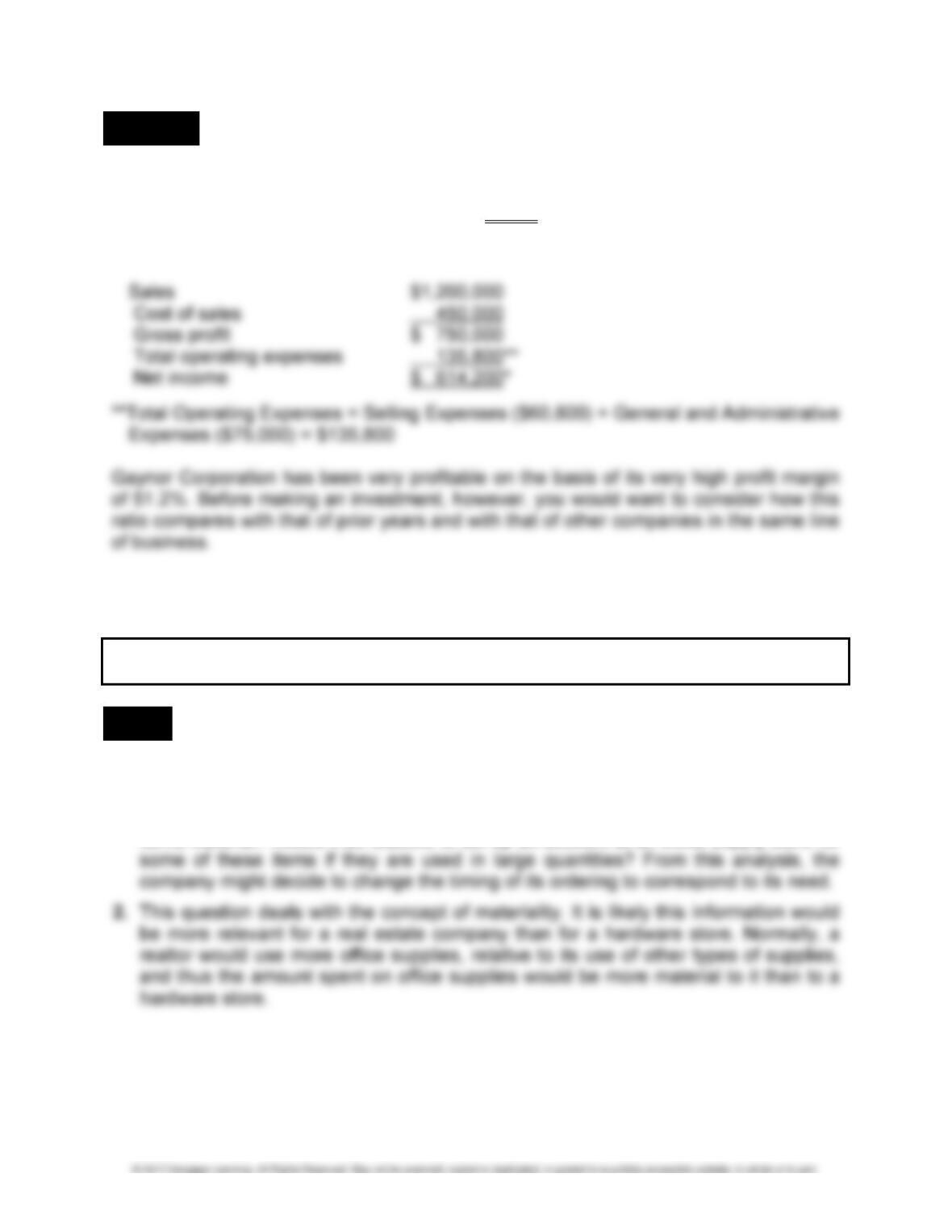

LO 5,6 EXERCISE 2-14 MULTIPLE-STEP INCOME STATEMENT

Profit margin:

Net Income/Sales = $614,200*/$1,200,000 = 51.2%

*$1,200,000 – $450,000 – $60,800 – $75,000 = $614,200*

PROBLEMS

LO 2 PROBLEM 2-1 MATERIALITY

1. Among the questions that might be answered by the analysis that was performed

are these: Is the usage of any of the items cyclical? Is there a relationship between

the usage of any two or more of the items? Is the amount being spent on these

items material? Would it be feasible to set up an account at an office supply store for

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-11

LO 2 PROBLEM 2-2 COSTS AND EXPENSES

1. Display fixtures in a retail store—Only a portion of the cost would appear in the

period of acquisition; the fixtures should be depreciated over their useful lives.

5. Cost of a franchise—This is a cost that should benefit several future periods, and

only a portion should be expensed in the current period; the cost of the franchise

should be treated as an intangible asset and amortized over the periods during

which benefits are expected.

6. Office supplies—The portion of the supplies used should be recognized as an

expense in the current period; the unused portion should be reported as a current

asset.

2-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3 PROBLEM 2-3 CLASSIFIED BALANCE SHEET

1. Classified balance sheet:

RUTH CORPORATION

BALANCE SHEET

DECEMBER 31, 2016

Assets

Current assets:

Cash …………………………………………………………………. $ 13,230

Accounts receivable ……………………………………………. 23,450

Inventory ……………………………………………………………. 45,730

Prepaid rent ……………………………………………………….. 1,500

Office supplies ……………………………………………………. 2,340

Liabilities

Current liabilities:

Accounts payable ……………………………………………….. $ 18,255

Income taxes payable ………………………………………….. 6,200

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-13

PROBLEM 2-3 (Concluded)

Stockholders’ Equity

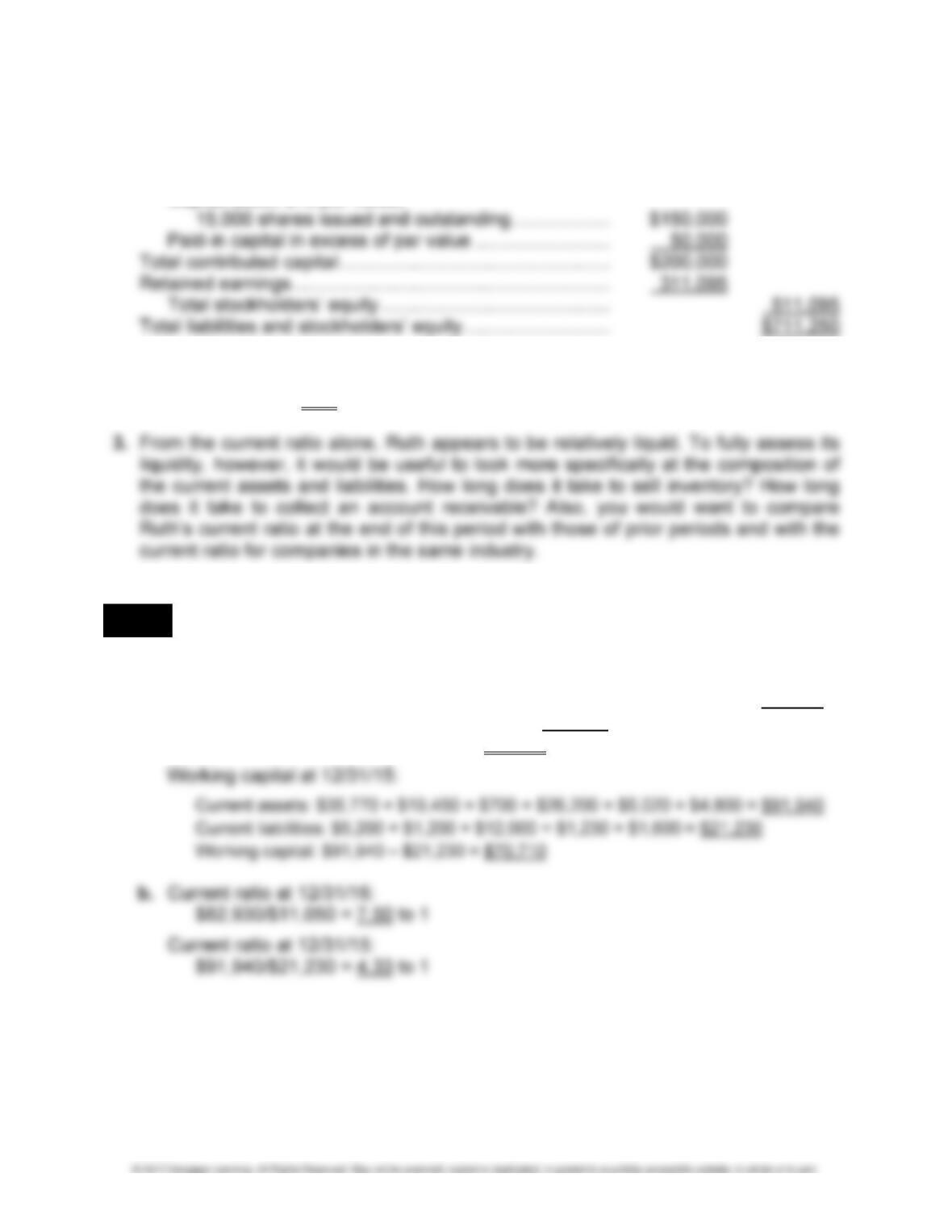

Contributed capital:

Capital stock, $10 par value,

2. Current Ratio = Current Assets/Current Liabilities

$86,250/$40,155 = 2.15 to 1

LO 4 PROBLEM 2-4 FINANCIAL STATEMENT RATIOS

1. a. Working capital at 12/31/16:

Current assets: $27,830 + $20,200 + $450 + $24,600 + $6,250 + $3,600 = $82,930

Current liabilities: $8,400 + $1,450 + $1,200 = $11,050

Working capital: $82,930 – $11,050 = $71,880

2-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 2-4 (Concluded)

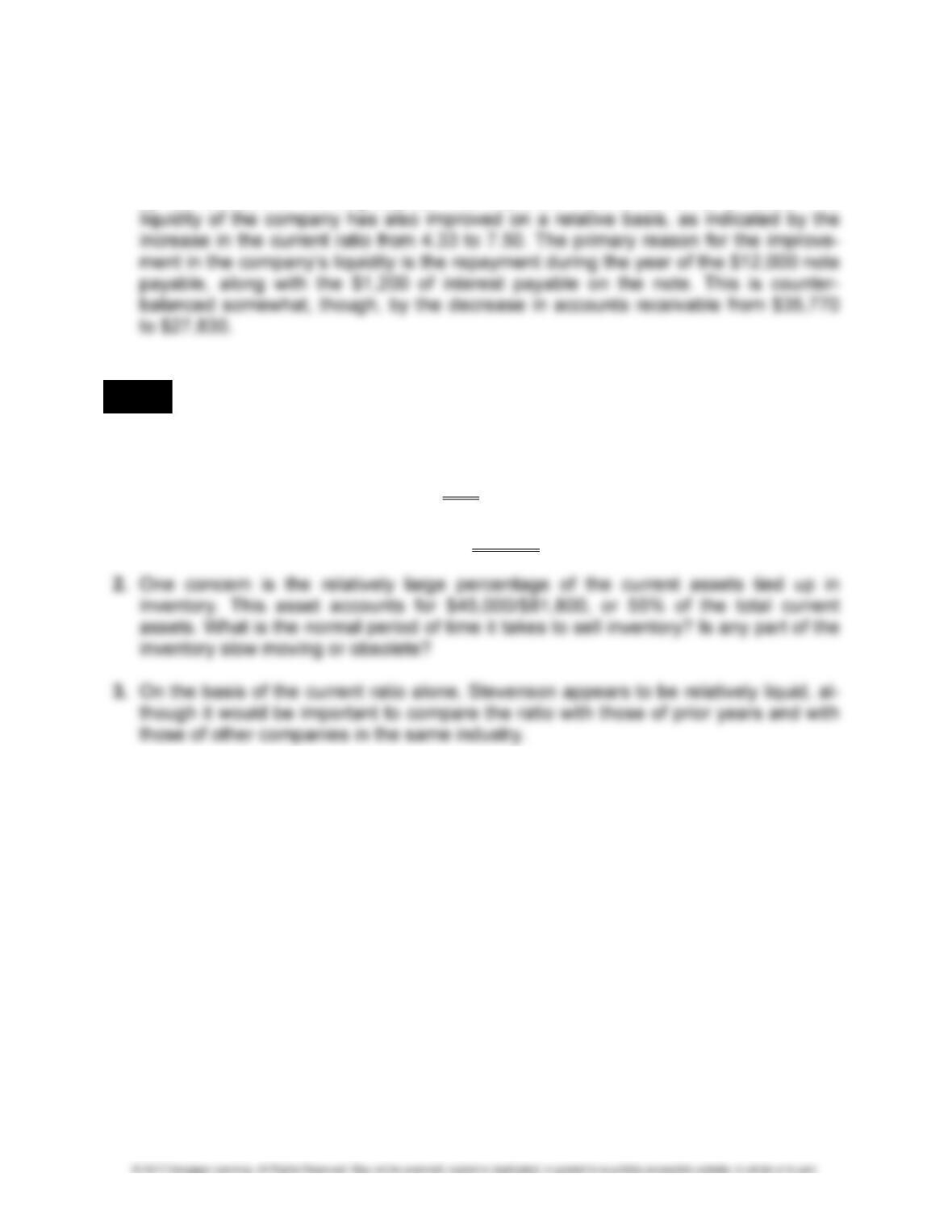

2. Both the absolute liquidity position of the company and the relative liquidity position

of the company have improved during 2016. First, the absolute position, as indicated

by the amount of working capital, has improved from $70,710 to $71,880. The

LO 4 PROBLEM 2-5 WORKING CAPITAL AND CURRENT RATIO

1. Current Ratio = Current Assets/Current Liabilities

= ($23,000 + $13,000 + $45,000 + $800)/($54,900 + $1,200)

= $81,800/$56,100 = 1.46 to 1

Working Capital = Current Assets – Current Liabilities

= $81,800 – $56,100 = $25,700

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-15

LO 5 PROBLEM 2-6 SINGLE-STEP INCOME STATEMENT

1. Single-step income statement:

SHAW CORPORATION

INCOME STATEMENT

FOR THE CURRENT YEAR

Revenues:

Sales ………………………………………………………………… $48,300

Interest ……………………………………………………………… 1,340

Rent ………………………………………………………………….. 6,700

Total revenues ………………………………………………………… $56,340

2. A single-step income statement does not lend itself as readily to analysis as does a

multiple-step statement. The lack of any grouping of the various expenses makes

2-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 2-7 MULTIPLE-STEP INCOME STATEMENT AND PROFIT MARGIN

1. Multiple-step income statement:

SHAW CORPORATION

INCOME STATEMENT

FOR THE CURRENT YEAR

Sales ……………………………………………………………………… $48,300

Cost of goods sold …………………………………………………… 29,200

Gross profit …………………………………………………………….. $ 19,100

Operating expenses:

Selling expenses:

Advertising …………………………………. $ 1,500

Total operating expenses ………………………………………….. 22,515

Loss from operations ……………………………………………….. $ (3,415)

Other revenues and expenses:

Interest expense …………………………………………………. $ 1,400

Interest revenue ………………………………………………….. 1,340

Rent revenue ……………………………………………………… 6,700

2. The main advantages of the multiple-step income statement are the groupings of

various items and the provision of important subtotals such as income from opera-

tions.

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-17

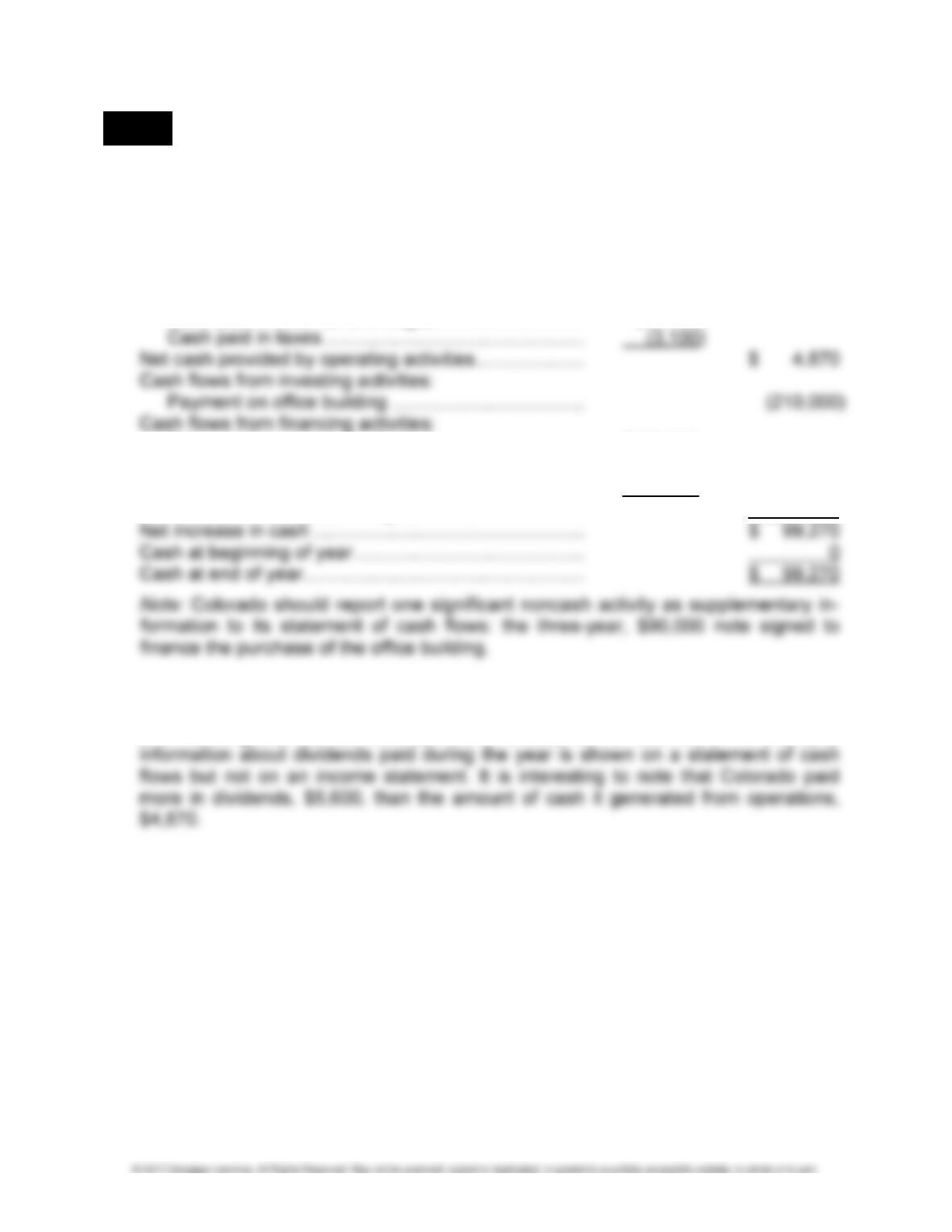

LO 8 PROBLEM 2-8 STATEMENT OF CASH FLOWS

1. COLORADO CORPORATION

STATEMENT OF CASH FLOWS

FOR THE FIRST YEAR

Cash flows from operating activities:

Cash collected from customers ………………………… $ 93,970

Cash paid for inventory ……………………………………. (65,600)

Cash paid in salaries and wages ………………………. (20,400)

Proceeds from issuance of stock ………………………. $250,000

Proceeds from long-term note ………………………….. 60,000

Dividends declared and paid ……………………………. (5,600)

Net cash provided by financing activities ………………… 304,400

2. First, the statement of cash flows reports on operations on a cash basis, as opposed

to the income statement which is prepared on an accrual basis. Second, investing

and financing activities are also reported on a statement of cash flows. For example,

2-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 9 PROBLEM 2-9 BASIC ELEMENTS OF FINANCIAL REPORTS

Letter from the President to Stockholders of Grammar Inc.:

On the surface, 2016 does not appear to have been a successful year for Grammar Inc.

One specific event, however, caused the net loss we experienced for the year. Operat-

MULTI-CONCEPT PROBLEMS

LO 2,4 PROBLEM 2-10 MAKING BUSINESS DECISIONS: LOANING MONEY TO THE

COCA-COLA COMPANY

.

Part A. Ratio Decision Model

1. Formulate the Question:

Is The Coca-Cola Company liquid enough to pay its obligations as they come due?

Current Assets: $8,958 + $9,052 + $3,665 + $4,466 + $3,100 + $3,066 + $679 =

$32,986

Current Liabilities: $9,234 + $19,130 + $3,552 + $400 + $58 = $32,374

Current Ratio = $32,986 = 1.02 to 1

$32,374

CHAPTER 2 • FINANCIAL STATEMENTS AND THE ANNUAL REPORT 2-19

PROBLEM 2-10 (Continued)

4. Compare the Ratio with Other Ratios:

Current Ratio

The Coca-Cola Company PepsiCo

December 31, 2014 December 31, 2013 December 27, 2014 December 28, 2013

1.02 to 1 1.13 to 1 1.14 to 1 1.24 to 1

Calculations:

The Coca-Cola Company at December 31, 2013:

5. Interpret the Ratios:

The Coca-Cola Company’s current ratio is slightly lower at the end of 2014 com-

pared to the end of 2013, 1.02 compared to 1.13. Similarly, PepsiCo’s current ratio

decreased slightly from one year to the next, 1.14 compared to 1.24. On the basis of

the current ratios alone, the two companies are similar in terms of liquidity at the end

of 2014.