Problem 2–9 (continued)

Insurance expense Utility expense

___________________________ ___________________________

Bal. 0 Bal. 30,000

Adjusting 1,500

2–82 Intermediate Accounting, 8/e

Problem 2–9 (continued)

Requirement 3

Account Title

Debits

Credits

Cash

8,000

Accounts receivable

9,000

Prepaid insurance

1,500

Land

200,000

Buildings

50,000

Accumulated depreciation—buildings

21,000

Office equipment

100,000

Accounts payable

35,050

Salaries and wages payable

Deferred rent revenue

1,200

Common stock

200,000

Retained earnings

56,450

Sales revenue

90,000

Interest revenue

3,000

Rent revenue

6,300

Salaries and wages expense

38,500

11,000

Insurance expense

1,500

Utility expense

30,000

Maintenance expense

15,000

464,500

464,500

Problem 2–9 (continued)

Requirement 4

December 31, 2016

Sales revenue ………………………………………………………… 90,000

Interest revenue …………………………………………………….. 3,000

Problem 2–9 (concluded)

Requirement 5

Account Title

Debits

Credits

Cash

8,000

Accounts receivable

9,000

Prepaid insurance

1,500

Land

200,000

Buildings

50,000

Office equipment

100,000

Accounts payable

Salaries and wages payable

Common stock

Retained earnings

Problem 2–10

Computations:

Sales revenue

Sales revenue during 2016 = $320,000 + 22,000 = $342,000

Cost of goods sold

Accounts payable

Inventory

1/1 Balance 0

Purchases 250,000

? Cost of goods sold

12/31 Balance 50,000

Cost of goods sold during 2016 = $250,000 – 50,000 = $200,000

Rent expense and prepaid rent

2–86 Intermediate Accounting, 8/e

Problem 2–10 (continued)

McGUIRE CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ……………………………………………

$342,000

Cost of goods sold …………………………………….

200,000

Gross profit ………………………………………………

142,000

Other expense:

Problem 2–10 (concluded)

McGUIRE CORPORATION

Balance Sheet

At December 31, 2016

Assets

Current assets:

Cash ……………………………………………………

$ 56,000

(1)

Accounts receivable ……………………………..

Prepaid rent …………………………………………

2,000

Inventory …………………………………………….

Office equipment ……………………………………

Less: Accumulated depreciation …………….

$157,000

Liabilities and Shareholders’ Equity

Current liabilities:

Accounts payable …………………………………

$ 30,000

Salaries and wages payable ……………………

5,000

Common stock …………………………………….

Retained earnings …………………………………

$157,000

2–88 Intermediate Accounting, 8/e

Problem 2–11

Requirement 1

a. Sales revenue

Accounts receivable

11/30 Balance 10,000

b. Cost of goods sold

Accounts payable

12,000 11/30 Balance

Cash paid 60,000

Inventory

11/30 Balance 7,000

Purchases 63,000

Problem 2–11 (concluded)

c. Insurance expense

Prepaid insurance

d. Salaries and wages expense

Salaries and wages payable

5,000 11/30 Balance

Cash payments 10,000

Requirement 2

Accounts receivable ……………………………………………….. 73,000

Sales revenue …………………………………………………….. 73,000

Problem 2–12

Requirement 1

Computations:

Sales revenue:

Cash collected from customers $675,000

Add: Increase in accounts receivable 30,000

Sales revenue $705,000

Cost of goods sold:

Cash paid for merchandise $390,000

Add: Increase in accounts payable 12,000

Purchases during2016 402,000

Add: Decrease in inventory 18,000

Cost of goods sold $420,000

Problem 2–12 (continued)

Interest expense:

Amount accrued at the end of 2016

($100,000 x .06 x 2/12) $1,000 (d)

Rent expense:

Depreciation expense: Increase in accumulated depreciation $10,000

Zambrano Wholesale Corporation

Income statement

For the Year Ended December 31, 2016

Sales revenue $705,000

Cost of goods sold 420,000

2–92 Intermediate Accounting, 8/e

Problem 2–12 (concluded)

Requirement 2

a. Prepaid insurance $ 2,000

Problem 2–13

Account Title

Unadjusted Trial Balance

Adjusting Entries

Adjusted Trial Balance

Income Statement

Balance Sheet

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash

23,300

23,300

23,300

Accounts receivable

32,500

32,500

32,500

Supplies

0

(4) 500

500

500

Prepaid rent

0

(5) 1,000

Inventory

65,000

65,000

65,000

Office equipment

75,000

75,000

75,000

Accumulated depreciation-

Accounts payable

26,100

26,100

26,100

Note payable

30,000

30,000

30,000

Interest payable

0

(3) 1,000

Common stock

80,000

80,000

80,000

Retained earnings

16,050

16,050

16,050

Sales revenue

Cost of goods sold

95,000

95,000

95,000

Interest expense

0

(3) 1,000

Rent expense

14,000

(5) 1,000

13,000

13,000

Supplies expense

(4) 500

Utility expense

Depreciation expense

0

13,375

13,375

Problem 2–13 (continued)

EXCALIBUR CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ………………………………………..

$180,000

Cost of goods sold …………………………………

95,000

Gross profit …………………………………………..

85,000

Operating expenses:

63,725

Operating income ………………………………….

Other expense:

Net income …………………………………………..

Problem 2–13 (continued)

EXCALIBUR CORPORATION

Statement of Shareholders’ Equity

For the Year Ended December 31, 2016

Total

Common Retained Shareholders’

Stock Earnings Equity

Balance at January 1, 2016 $80,000 $22,050 $102,050

2–96 Intermediate Accounting, 8/e

Problem 2–13 (continued)

EXCALIBUR CORPORATION

Balance Sheet

At December 31, 2016

Assets

Current assets:

Cash ……………………………………………………..

$ 23,300

Accounts receivable ………………………………..

Supplies ………………………………………………..

Prepaid rent …………………………………………….

1,000

Inventory …………………………..…………………..

Office equipment ………………………………………

Less: Accumulated depreciation ……………….

$177,925

Liabilities and Shareholders’ Equity

Current liabilities:

Accounts payable ……………………………………

$ 26,100

Salaries and wages payable ……………………..

4,500

Common stock ……………………………………….

Retained earnings …………………………………..

$177,925

Problem 2–13 (concluded)

December 31,2016

Sales revenue ………………………………………………………… 180,000

Income summary ……………………………………………….. 180,000

Income summary …………………………………………………… 159,725

2–98 Intermediate Accounting, 8/e

Judgment Case 2–1

Requirement 1

Cash basis accounting produces a measure of performance called net operating

Requirement 2

In most cases, the accrual accounting model provides a better measure of

Requirement 3

Judgment Case 2–2

Requirement 1

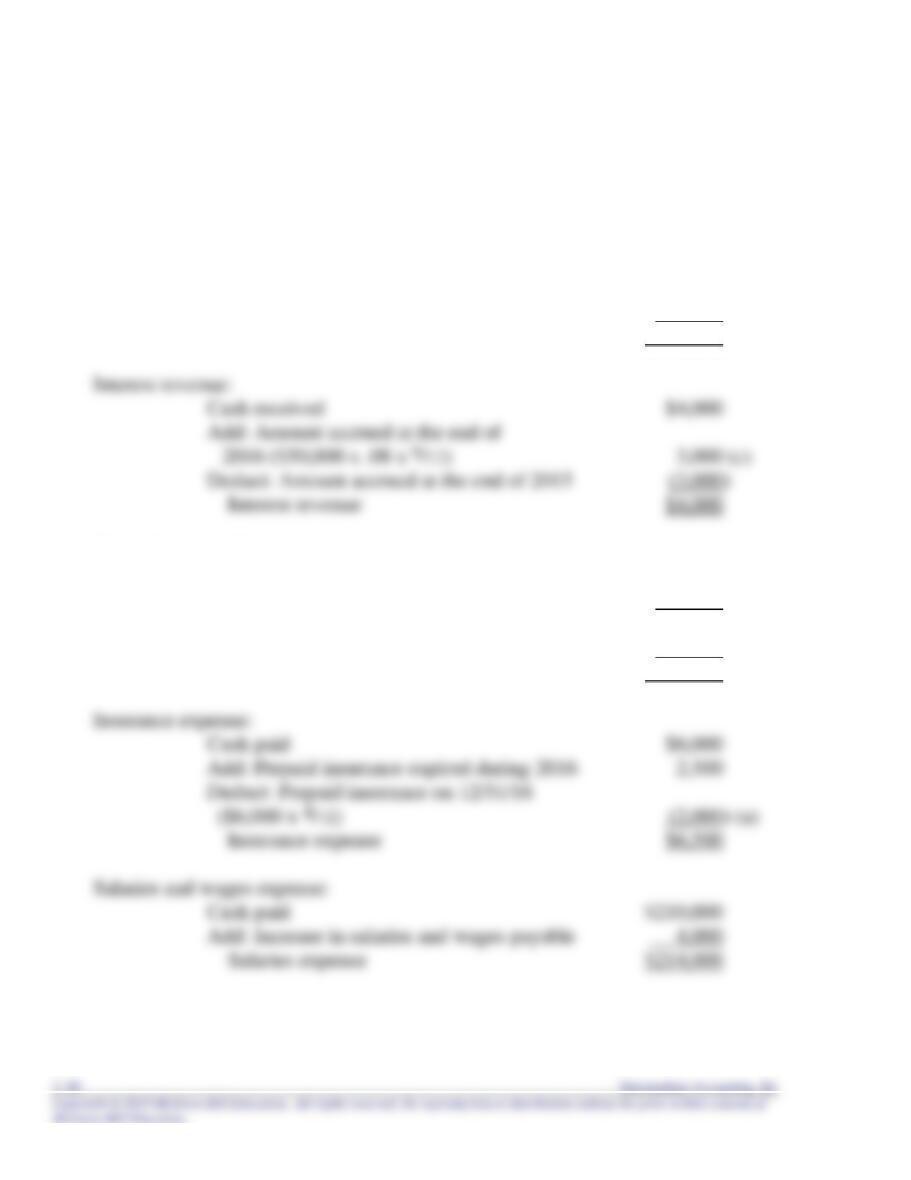

Cash basis net income $26,000

Add: 1. Unexpired (prepaid insurance) $12,000 x 8/12 8,000

Requirement 2

Assets would be higher by $12,500 ($8,000 + 1,500 + 3,000) and liabilities

CASES

Communication Case 2–3

Requirement 1

Prepayments occur when the cash flow precedes either expense or revenue

recognition. Accruals occur when the cash flow comes after either expense or revenue

recognition.

Requirement 2

The appropriate adjusting entry for a prepaid expense is a debit to expense and a

cause liabilities to be overstated and shareholders’ equity to be understated.

Requirement 3

The required adjusting entry for accrued liabilities is a debit to expense and a

credit to a liability. For accrued receivables, the appropriate adjusting entry is a debit