CHAPTER 19

Cost-Volume-Profit

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Explain variable, fixed, and

mixed costs and the relevant

range.

1, 2, 3, 4, 5,

6

1, 2

1

1, 2, 3, 4, 5,

6

1A, 6A

4. Compute the break-even

point using three approaches.

12, 13, 14

8, 9

4, 5

8, 9, 10, 11,

12, 13, 14,

16, 17

1A, 2A, 3A,

4A, 5A

5. Determine the sales required

determine margin of safety.

15, 16

10, 11, 12

5

14, 15, 16,

2A, 4A, 5A,

2. Apply the high-low method to

mixed costs.

7, 8

1, 3, 4, 5

2

3, 5,

1A

3. Prepare a CVP income

9, 10, 11, 17

6, 7

3

7, 8, 9, 10, 11,

12, 13, 17

1A, 2A, 4A,

5A, 6A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Determine variable and fixed costs, compute break-even

point, prepare a CVP graph, and determine net income.

Simple

20–30

2A

Prepare a CVP income statement, compute break-even

point, contribution margin ratio, margin of safety ratio,

and sales for target net income.

Moderate

30–40

3A

Compute break-even point under alternative courses

of action.

Simple

20–30

changes in business environment.

5A

Compute contribution margin, fixed costs, break-even

point, sales for target net income, and margin of safety

ratio.

Moderate

20–30

6A

Determine contribution margin ratio, break-even point, and

margin of safety.

20–30

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Explain variable, fixed, and mixed

costs and the relevant range.

E19-4

Q19-1

Q19-2

Q19-3

Q19-4

Q19-5

Q19-6

BE19-1

DI19-1

E19-1

E19-2

E19-4

E19-2

E19-5

E19-6

BE19-2

E19-3

P19–1A

P19–6A

* 4. Compute the break-even point

using three approaches.

Q19–12

Q19–14

Q19–13

BE19-8

BE19-9

DI19-4

DI19-5

E19-8

E19-9

E19–10

E19–11

E19–12

E19–13

E19–14

E19–16

E19–17

E19–16

P19–1A

P19–2A

P19–5A

P19–3A

P19–4A

Q19–15

Q19–16

DI19-5

E19–12

E19–14

E19–15

E19–17

E19–16

P19–2A

P19–5A

BLOOM’ S TAXONOMY TABLE

Q19-7

E19-1

Q19-8

DI19-2

E19-5

E19-6

BE19-3

E19-3

P19–1A

ANSWERS TO QUESTIONS

1. (a) Cost behavior analysis is the study of how specific costs respond to changes in the level of activity

within a company.

(b) Cost behavior analysis is important to management in planning business operations and in deciding

between alternative courses of action.

3. Fixed costs remain the same in total regardless of changes in the activity level. In contrast, fixed

costs per unit vary inversely with activity. As volume increases, fixed costs per unit decline and vice

versa.

5. This is true. Most companies operate within the relevant range. Within this range, it is possible to

establish a linear (straight-line) relationship for both variable and fixed costs. If a relevant range

cannot be established, segregation of costs into fixed and variable becomes extremely difficult.

8. Variable cost per unit is $1.30, or [($165,000 – $100,000) ÷ (90,000 – 40,000)]. At any level of activity,

fixed costs are $48,000 per month [$165,000 – (90,000 X $1.30)].

Questions Chapter 19 (Continued)

12. Disagree. Knowledge of the break–even point is useful to management in deciding whether to introduce

new product lines, change sales prices on established products, and enter new market areas.

13. $26,000 ÷ 25% = $104,000

15. Margin of safety is the difference between actual or expected sales and sales at the break-even

point. 1,250 X $12 = $15,000; $15,000 – $13,200 = $1,800; $1,800 ÷ $15,000 = 12%.

17. PACE COMPANY

CVP Income Statement

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 19-1

BRIEF EXERCISE 19-2

BRIEF EXERCISE 19-3

BRIEF EXERCISE 19-4

BRIEF EXERCISE 19-5

BRIEF EXERCISE 19-6

BRIEF EXERCISE 19-7

RUSSELL INC.

CVP Income Statement

For the Quarter Ended March 31, 2017

BRIEF EXERCISE 19-8

BRIEF EXERCISE 19-9

BRIEF EXERCISE 19–10

Required sales in dollars = ($195,000 + $75,000) ÷ .30 = $900,000

BRIEF EXERCISE 19–11

BRIEF EXERCISE 19–12

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 19-1

DO IT! 19-2

DO IT! 19-3

Cedar Grove Industries

CVP Income Statement

For the Month Ended May 31, 2017

DO IT! 19-5

SOLUTIONS TO EXERCISES

EXERCISE 19-1

EXERCISE 19-2

EXERCISE 19-3

(a) Maintenance Costs:

EXERCISE 19-3 (Continued)

EXERCISE 19-4

EXERCISE 19-5

(a) Maintenance Costs:

EXERCISE 19-6

EXERCISE 19-7

MEMO

EXERCISE 19-8

EXERCISE 19-9

EXERCISE 19–10

EXERCISE 19–11

EXERCISE 19–12

EXERCISE 19-12 (Continued)

EXERCISE 19–13

(a) and (b) BILLINGS COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

(d) BILLINGS COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

EXERCISE 19–14

EXERCISE 19–15

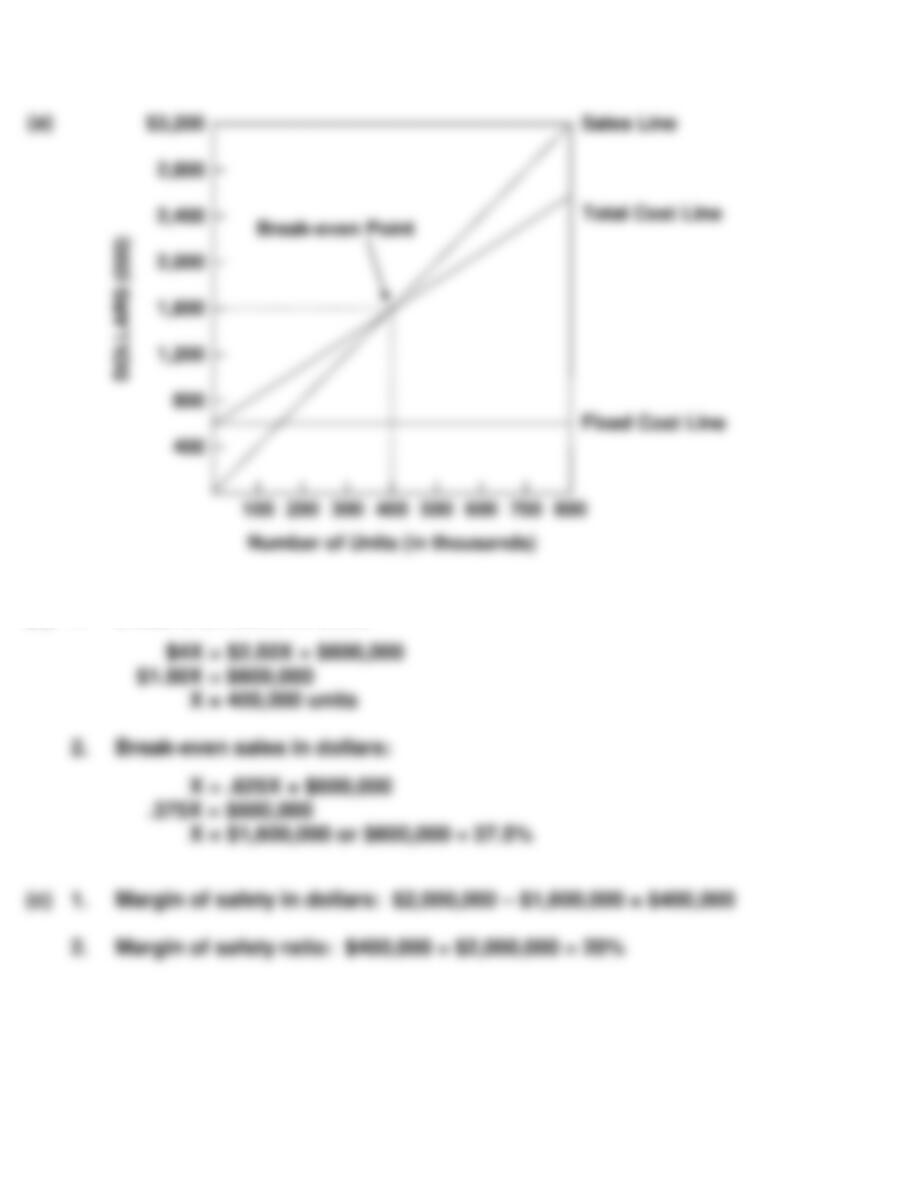

EXERCISE 19–16

(b) 1. Break-even sales in units:

EXERCISE 19–17

SOLUTIONS TO PROBLEMS

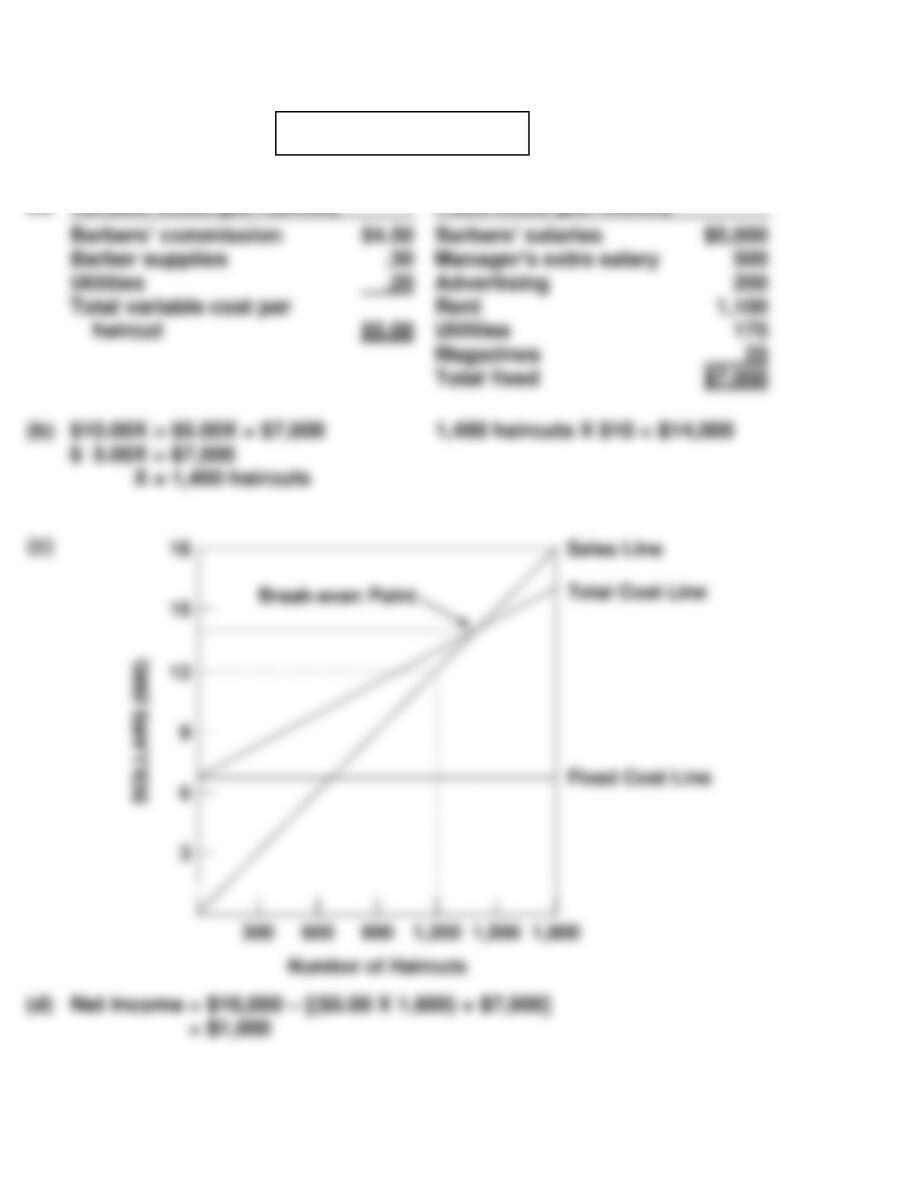

PROBLEM 19–1A

(a)

Variable costs (per haircut)

Fixed costs (per month)

Total fixed $7,000

PROBLEM 19–2A

(a) JORGE COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2017

PROBLEM 19–3A

PROBLEM 19–4A

(c) BARGAIN SHOE STORE

CVP Income Statement

PROBLEM 19–5A

(2)

Fixed Costs

Total fixed costs

(a)

(1)

Contribution margin

Contribution margin

PROBLEM 19-5A (Continued)

PROBLEM 19–6A

CD19 CURRENT DESIGNS

(a)

(1) Capital-Intensive

(2) Labor-Intensive

Total fixed costs $3,026,000

Total fixed costs $2,052,000

Contribution margin $16.00

Contribution margin $12.00

Total fixed costs (1) $3,026,000

Total fixed costs (1) $2,052,000

Contribution margin per unit (2) $16.00

Contribution margin per unit (2) $12.00

Break-even in units (1) ÷ (2) 189,125

Break-even in units (1) ÷ (2) 171,000

BYP 19-2 MANAGERIAL ANALYSIS

BYP 19-2 (Continued)

Profits and the break-even point would both increase.

BYP 19-3 REAL-WORLD FOCUS

BYP 19-4 REAL-WORLD FOCUS

BYP 19-5 COMMUNICATION ACTIVITY

To: My Roommate

From: Your Roommate

Subject: Cost-Volume-Profit Questions

In response to your request for help, I provide you the following:

BYP 19-5 (Continued)

BYP 19-6 ETHICS CASE

(a) The stakeholders in this situation are:

BYP 19-7 ALL ABOUT YOU