E19-22, cont.

Requirement 3

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

$9.20 per DLHr

×

14,000 DLHr

=

$128,800

Total manufacturing overhead cost

128,800

Total cost

=

×

125% markup

=

$504,750

Requirement 4

Activity-based costing allocation of manufacturing overhead is more accurate than traditional single

plantwide rate allocation of manufacturing overhead. Activity-based costing considers the resources

E19-23 Allocating indirect costs and computing income, service company

Learning Objective 4

2. Total OH cost $28,500

Requirements

1. Compute Southern’s predetermined overhead allocation rate per direct labor hour.

2. Compute the total cost assigned to the Halbert engagement.

3. Compute the operating income from the Halbert engagement.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

=

$150 per DLHr

Requirement 2

Allocation Base Used

Overhead Cost

×

190 DLHr

=

×

=

Total direct labor cost

Total overhead cost

Total cost

Predetermined

Overhead

×

Actual Quantity

of the

=

Allocated

Requirement 3

Service revenue

=

$64,600 total direct labor cost

×

160%

=

$103,360

=

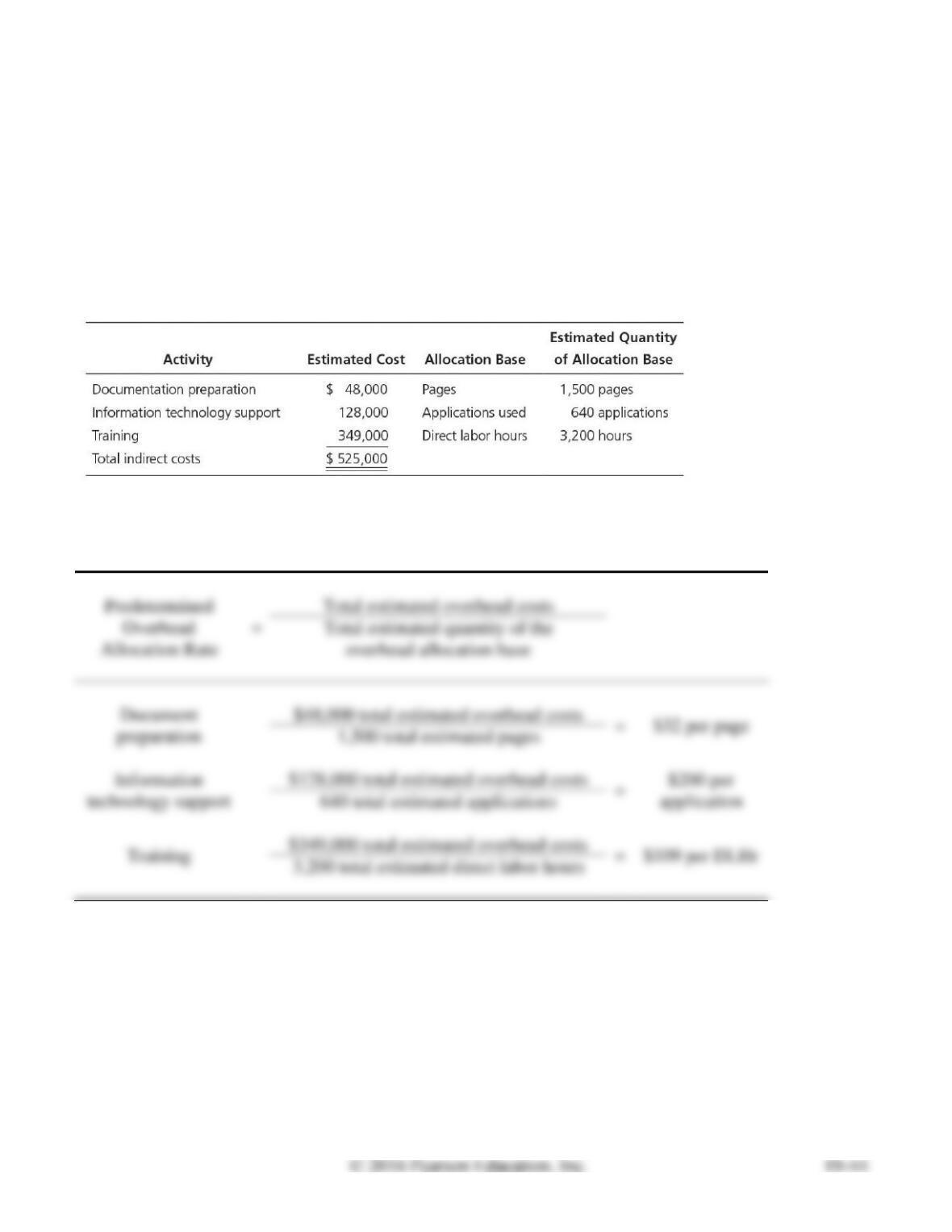

E19-24 Computing ABC allocation rates, service company

Learning Objective 4

POHR training $109 per DLHr

Refer to Exercise E19-23. The president of Southern suspects that her allocation of indirect costs could

be giving misleading results, so she decides to develop an ABC system. She identifies three activities:

documentation preparation, information technology support, and training. She figures that

documentation costs are driven by the number of pages, information technology support costs are driven

by the number of software applications used, and training costs are driven by the number of direct labor

hours worked. Estimates of the costs and quantities of the allocation bases follow:

Compute the predetermined overhead allocation rate for each activity. Round to the nearest dollar.

SOLUTION

Note: Exercises E19-23 and E19-24 must be completed before attempting Exercise E19-25.

E19-25 Using ABC to allocate costs and compute profit, service company

Learning Objective 4

1. Total OH cost $47,990

Refer to Exercises E19-23 and E19-24. Suppose Southern’s direct labor rate was $340 per hour. The

Halbert engagement used the following resources last month:

Requirements

1. Compute the cost assigned to the Halbert engagement, using the ABC system.

2. Compute the operating income or loss from the Halbert engagement, using the ABC system.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate(a)

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Overhead Cost

×

=

×

=

×

=

20,710

$ 47,990

Direct Labor Rate

per DLHr

×

Number of DLHr

worked

=

Total Direct

Labor Cost

$340 per DLHr

×

190 DLHr

=

$64,600

Total direct labor cost

Total overhead cost

Total cost

Requirement 2

Service revenue

=

$64,600 total direct labor cost

×

160%

=

$103,360

=

$112,590 total cost

=

Note: Exercise E19-25 must be completed before attempting Exercise E19-26.

E19-26 Using ABC to achieve target profit, service company

Learning Objective 4

$187,650.00

Refer to Exercise E19-25. Southern desires a 40% target net profit after covering all costs. Considering

the total costs assigned to the Halbert engagement in Exercise E19-25, what would Southern have to

charge the customer to achieve that net profit? Round to two decimal places.

SOLUTION

Desired net profit

=

Required service revenue

–

Total cost

=

Required service revenue

–

Total cost

=

=

E19-27 Recording manufacturing costs in a JIT costing system

Learning Objective 5

1. COGS $21,840 DR

Requirements

1. Prepare summary journal entries for January.

2. The January 1, 2016, balance of the Raw and In-Process Inventory account was

$60. Use a T-account to find the January 31 balance.

3. Use a T-account to determine whether conversion costs are overallocated or underallocated for the

month. By how much? Prepare the journal entry to adjust the Conversion Costs account.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Raw and In-Process Inventory

6,000

Accounts Payable

6,000

Conversion Costs

Wages Payable, Accumulated Depreciation, etc.

Finished Goods Inventory

Raw and In-Process Inventory (525 units × $10/unit)

5,250

Conversion Costs (525 units × $32/unit)

Accounts Receivable (520 units × $58/unit)

Sales Revenue

Cost of Goods Sold (520 units × $42/unit)

Finished Goods Inventory

Requirement 2

Raw and In-Process Inventory

Jan. 1 60

5,250

Jan. 31 810

Requirement 3

Conversion costs are overallocated by $800.

16,800

800 Jan. 31

Date

Accounts and Explanation

Debit

Credit

Conversion Costs

Cost of Goods Sold

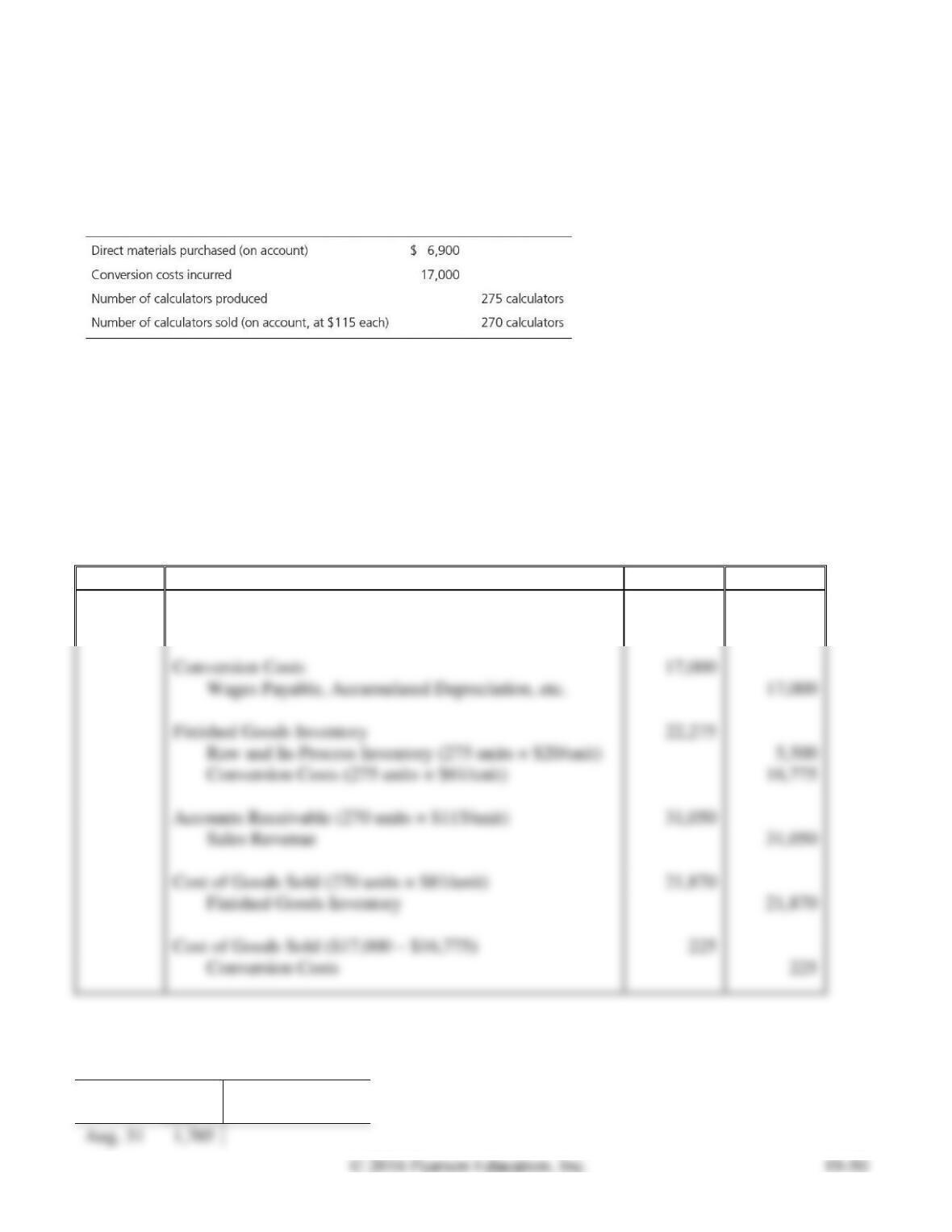

E19-28 Recording manufacturing costs in a JIT costing system

Learning Objective 5

1. R&IP $5,500 CR

Golner produces electronic calculators. Suppose Golner’s standard cost per calculator is $20 for direct

materials and $61 for conversion costs. The following data apply to August activities:

Requirements

1. Prepare summary journal entries for August using JIT costing, including the entry to adjust the

Conversion Costs account.

2. The beginning balance of Finished Goods Inventory was $1,300. Use a T-account to find the ending

balance of Finished Goods Inventory.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Raw and In-Process Inventory

6,900

Accounts Payable

6,900

Conversion Costs

Wages Payable, Accumulated Depreciation, etc.

Finished Goods Inventory

Raw and In-Process Inventory (275 units × $20/unit)

5,500

Conversion Costs (275 units × $61/unit)

Accounts Receivable (270 units × $115/unit)

Sales Revenue

Cost of Goods Sold (270 units × $81/unit)

Cost of Goods Sold ($17,000 – $16,775)

Conversion Costs

Requirement 2

Finished Goods Inventory

Aug. 1 1,300

21,870

22,275

E19-29 Classifying quality costs

Learning Objective 6

Total external failure costs $103,500

Decker & Co. makes electronic components. Chris Decker, the president, recently instructed Vice

President Jim Bruegger to develop a total quality control program. “If we don’t at least match the quality

improvements our competitors are making,” he told Bruegger, “we’ll soon be out of business.” Bruegger

began by listing various “costs of quality” that Decker incurs. The first six items that came to mind

were:

a. Costs incurred by Decker customer representatives traveling to customer sites to repair defective

products, $13,500.

b. Lost profits from lost sales due to reputation for less-than-perfect products,

$35,000.

c. Costs of inspecting components in one of Decker’s production processes, $22,500.

d. Salaries of engineers who are redesigning components to withstand electrical overloads, $90,000.

e. Costs of reworking defective components after discovery by company inspectors,

$25,000.

f. Costs of electronic components returned by customers, $55,000.

Classify each item as a prevention cost, an appraisal cost, an internal failure cost, or an external failure

cost. Then determine the total cost of quality by category.

SOLUTION

Prevention

Cost

Appraisal

Cost

Internal Failure

Cost

External Failure

Cost

a.

$ 13,500

c.

e.

55,000

Total

$ 103,500

E19-30 Classifying quality costs and using these costs to make decisions

Learning Objective 6

2. Total cost to undertake $185,000

Clegg, Inc. manufactures door panels. Suppose Clegg is considering spending the

following amounts on a new total quality management (TQM) program:

Requirements

1. Classify each cost as a prevention cost, an appraisal cost, an internal failure cost, or an external

failure cost.

2. Should Clegg implement the new quality program? Give your reason.

SOLUTION

Requirements 1 and 2

Undertake the New TQM Program

Prevention

Training employees in TQM

$ 22,000

Training suppliers in TQM

38,000

quality materials

Total prevention costs

Strength-testing one item from each batch of panels

70,000

Total appraisal costs

Do Not Undertake the New TQM Program

Appraisal

Avoid inspection of raw materials

$ 52,000

Total appraisal costs

$ 52,000

Avoid rework and spoilage

Total internal failure costs

Avoid lost profits from lost sales due to disappointed customers

Avoid warranty costs

Total external failure costs

Total costs of not undertaking the new TQM program

$ 220,000

Clegg should implement the new TQM program. The total cost of undertaking the new TQM program

($185,000) is less than the total cost of not undertaking the new TQM program ($220,000) by $35,000.

Clegg would save $35,000 by undertaking the program.

E19-31 Classifying quality costs and using these costs to make decisions

Learning Objective 6

2. Total cost to undertake $2,240,000

Langley manufactures high-quality speakers. Suppose Langley is considering spending the following

amounts on a new quality program:

Requirements

1. Classify each of these costs into one of the four categories of quality costs (prevention, appraisal,

internal failure, external failure).

2. Should Langley implement the quality program? Give your reasons.

SOLUTION

Requirements 1 and 2

Undertake the New Quality Program

Prevention

Negotiating and training suppliers to obtain higher-quality materials

and on-time delivery

$ 350,000

Do Not Undertake the New Quality Program

Appraisal

Avoid inspection of raw materials

$ 550,000

Total appraisal costs

$ 550,000

Lost production time due to rework

Total internal failure costs

Reduce warranty repair costs

Lost sales due to disappointed customers

Total external failure costs

Total costs of not undertaking the new quality program

$ 2,728,000

Langley should implement the new quality program. The total cost of undertaking the new quality

program ($2,240,000) is less than the total cost of not undertaking the new quality program ($2,728,000)

by $488,000. Langley would save $488,000 by undertaking the program.

Problems (Group A)

P19-32A Comparing costs from ABC and single-rate systems

Learning Objectives 1, 2

2. Travel packs $1.80

Crescent Pharmaceuticals manufactures an over-the-counter allergy medication. The company sells both

large commercial containers of 1,000 capsules to health care facilities and travel packs of 20 capsules to

shops in airports, train stations, and hotels. The following information has been developed to determine

if an activity-based costing system would be beneficial:

Requirements

1. Compute the predetermined overhead allocation rate for each activity.

2. Use the predetermined overhead allocation rates to compute the activity-based costs per unit of the

commercial containers and the travel packs. Round to two decimal places. (Hint: First compute the

total activity-based costs allocated to each product line, and then compute the cost per unit.)

3. Crescent’s original single plantwide overhead allocation rate costing system allocated indirect costs

to products at $153.00 per machine hour. Compute the total indirect costs allocated to the

commercial containers and to the travel packs under the original system. Then compute the indirect

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

4,140 total estimated machine hours

Requirement 2

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Commercial containers

Materials handling

$4 per kilo

×

14,000 kilos

=

$ 56,000

Packaging

$50 per MHr

×

3,000 MHr

=

150,000

Quality assurance

$60 per sample

×

400 samples

=

24,000

Total activity-based costs

$ 230,000

÷ Number of units

Activity-based cost per unit

$ 57.50

Travel packs

Materials handling

$4 per kilo

×

5,400 kilos

=

$ 21,600

Packaging

$50 per MHr

×

=

27,000

Total activity-based costs

$ 97,200

÷ 54,000 units

Activity-based cost per unit

$ 1.80

P19-32A, cont.

Requirement 3

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Commercial

containers

Total indirect costs

$153.00 per MHr

×

3,000 MHr

=

$ 459,000.00

÷ Number of units

Indirect cost per unit

Travel packs

Total indirect costs

$153.00 per MHr

×

540 MHr

=

÷ Number of units

Indirect cost per unit

Requirement 4

Comparison of manufacturing overhead cost per unit:

Traditional

System

ABC

System

Difference

Commercial

Containers

$ 114.75 per unit(a)

–

$ 57.50 per unit(b)

=

$57.25

Travel packs

$ 1.53 per unit(a)

–

$ 1.80 per unit(b)

=

($0.27)

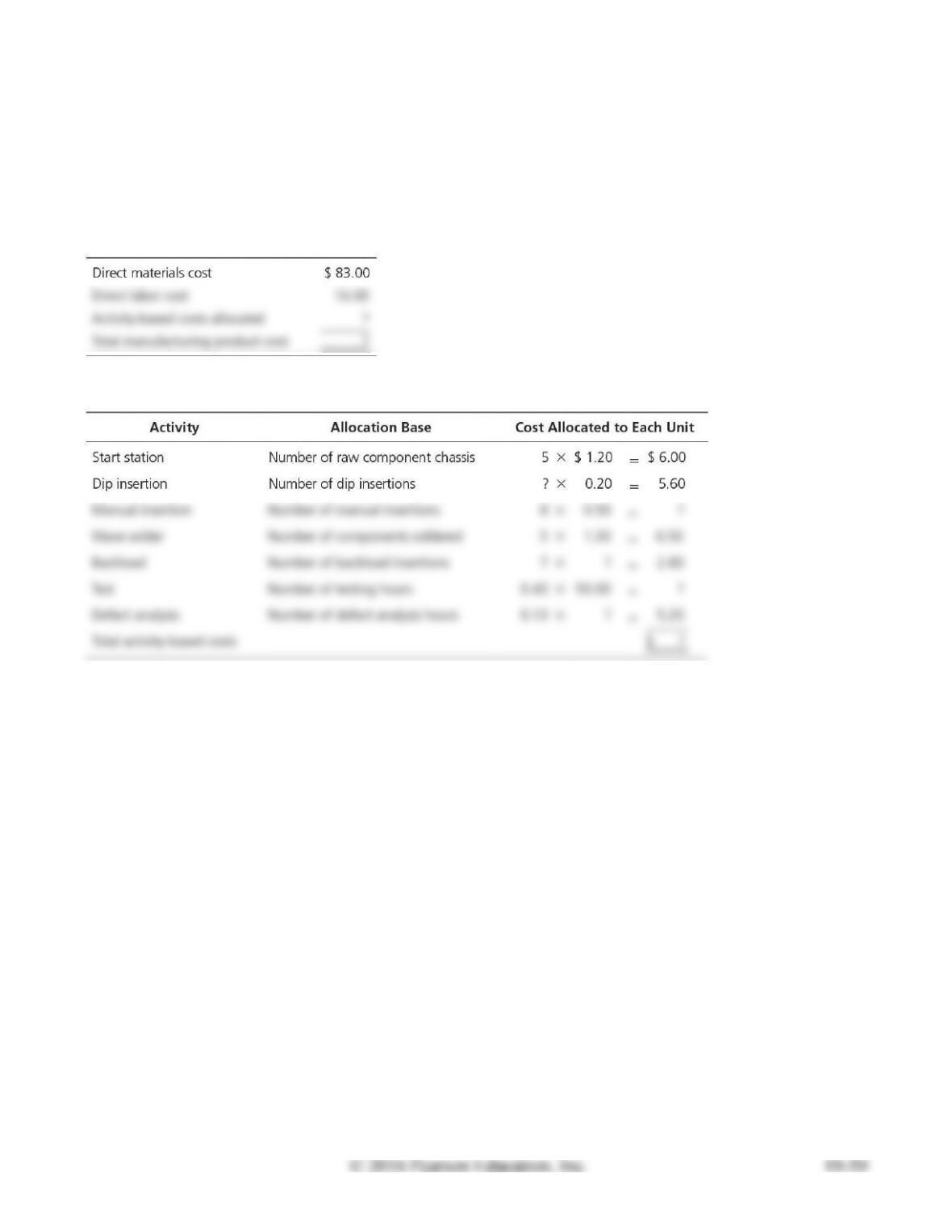

P19-33A Computing product costs in an ABC system

Learning Objective 2

1. Total activity-based costs $51.60

The Adam Manufacturing Company in Rochester, Minnesota, assembles and tests electronic

components used in smartphones. Consider the following data regarding component T24 (amounts are

per unit):

The activities required to build the component follow:

Requirements

1. Complete the missing items for the two tables.

2. Why might managers favor this ABC system instead of Adam’s older system, which allocated all

manufacturing overhead costs on the basis of direct labor hours?

SOLUTION

Requirement 1

Activity

Allocation Base

Cost Allocated

to each Unit

Start station

Number of raw component chassis

5

×

$ 1.20

=

$ 6.00

28(a)

Manual insertion

Number of manual insertions

8

0.50

4.00(b)

Wave solder

Number of components soldered

5

×

1.30

=

6.50

Test

Number of testing hours

0.43

50.00

Direct materials cost

$ 83.00

Direct labor cost

16.00

Activity-based costs allocated

51.60(f)

Total manufacturing product cost

$ 150.60

(a)

$5.60

=

(b)

8

×

$0.50

(c)

$2.80

(d)

×

=

(e)

$5.20

=

Sum of column

Requirement 2

Because the traditional (older) costing system doesn’t reflect the way products actually use the