P19-34A Computing product costs in an ABC system

Learning Objectives 2, 3

1. Standard $70 per unit

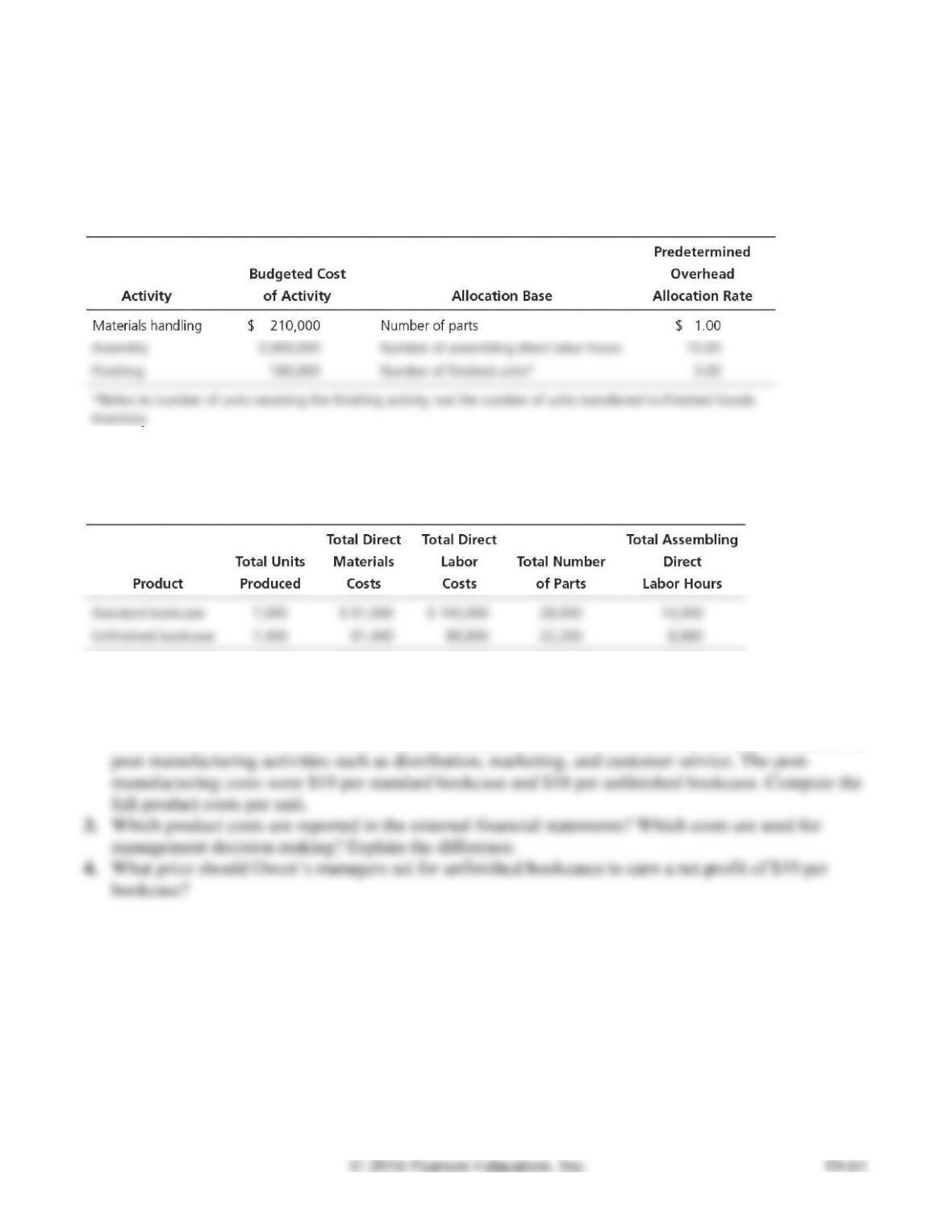

Owen, Inc. manufactures bookcases and uses an activity-based costing system. Owen’s activity areas

and related data follow:

Owen produced two styles of bookcases in October: the standard bookcase and an unfinished bookcase,

which has fewer parts and requires no finishing. The totals for quantities, direct materials costs, and

other data follow:

Requirements

1. Compute the manufacturing product cost per unit of each type of bookcase.

2. Suppose that pre-manufacturing activities, such as product design, were assigned to the standard

bookcases at $5 each and to the unfinished bookcases at $4 each. Similar analyses were conducted of

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Standard bookcases

Materials handling

$1.00 per part

×

28,000 parts

=

$ 28,000

×

14,000 DLHr

=

×

=

Total manufacturing

bookcases

Materials handling

$1.00 per part

×

22,200 parts

=

$ 22,200

×

8,880 DLHr

=

133,200

×

=

Total manufacturing

overhead cost

Standard

bookcases

Unfinished

bookcases

Total direct materials cost

$ 91,000

$ 81,400

Total direct labor cost

140,000

88,800

Total manufacturing overhead cost

259,000

Total manufacturing product cost

$ 490,000

$ 325,600

÷ Number of units

Manufacturing product cost per unit

$ 70

$ 44

P19-34A, cont.

Requirement 2

Standard

bookcases

Unfinished

bookcases

Pre-manufacturing costs per unit

$ 5

$ 4

Post-manufacturing costs per unit

Full product costs per unit

$ 94

$ 66

Requirement 3

Manufacturing product costs are reported in the external financial statements in the inventory accounts

Requirement 4

Sales price per unit

=

Full product cost

+

Net profit

=

P19-35A Using ABC in a service company

Learning Objective 4

1. Total OH cost $620

Mahoney Plant Service completed a special landscaping job for Cory Company. Mahoney uses ABC

and has the following predetermined overhead allocation rates:

Requirements

1. What is the total cost of the Cory job?

2. If Cory paid $2,495 for the job, what is the operating income or loss?

3. If Mahoney desires an operating income of 40% of cost, how much should the company charge for

the Cory job?

SOLUTION

Requirement 1

Allocation Base Used

Overhead Cost

×

=

×

=

Total plant cost

Total direct labor cost

Total overhead cost

Total cost

Predetermined

Overhead

×

Actual Quantity

of the

=

Allocated

Requirement 2

Operating Income

=

$2,495 service revenue

–

$1,995 total cost

=

$500

Requirement 3

=

$1,995 total cost

×

140%

=

$2,793

P19-36A Recording manufacturing costs for a JIT system

Learning Objective 5

2. Conversion Costs $352,000 CR

Freeze Point produces fleece jackets. The company uses JIT costing for its JIT production system.

Freeze Point has two inventory accounts: Raw and In-Process Inventory and Finished Goods

Inventory. On February 1, 2016, the account balances were Raw and In-Process Inventory, $13,000;

Finished Goods Inventory, $2,000.

The standard cost of a jacket is $35, composed of $13 direct materials plus $22 conversion costs. Data

for February’s activities follow:

Requirements

1. What are the major features of a JIT production system such as that of Freeze Point?

2. Prepare summary journal entries for February. Underallocated or overallocated conversion costs are

adjusted to Cost of Goods Sold monthly.

3. Use a T-account to determine the February 29, 2016, balance of Raw and In-Process Inventory.

SOLUTION

Requirement 1

A just-in-time management system is an inventory management system in which a company produces

just in time to satisfy customer needs. Suppliers deliver raw materials just in time to begin production

and finished units are completed just in time for delivery to customers.

P19-36A, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Raw and In-Process Inventory

200,500

Accounts Payable

200,500

Conversion Costs

452,000

Wages Payable, Accumulated Depreciation, etc.

452,000

Finished Goods Inventory

560,000

Raw and In-Process Inventory (16,000 units × $13/unit)

208,000

Conversion Costs (16,000 units × $22/unit)

352,000

Accounts Receivable (15,600 units × $95/unit)

Sales Revenue

Cost of Goods Sold (15,600 units × $35/unit)

546,000

Finished Goods Inventory

546,000

Cost of Goods Sold ($452,000 – $352,000)

100,000

Conversion Costs

100,000

Requirement 3

Raw and In-Process Inventory

Feb. 1 13,000

208,000

200,500

P19-37A Analyzing costs of quality

Learning Objective 6

2. Net benefit $29,265

Lilly, Inc. is using a costs-of-quality approach to evaluate design engineering efforts for a new

skateboard. Lilly’s senior managers expect the engineering work to reduce appraisal, internal failure,

and external failure activities. The predicted reductions in activities over the two-year life of the

skateboards follow. Also shown are the predetermined overhead allocation rates for each activity.

Requirements

1. Calculate the predicted quality cost savings from the design engineering work.

2. Lilly spent $100,000 on design engineering for the new skateboard. What is the net benefit of this

“preventive” quality activity?

3. What major difficulty would Lilly’s managers have in implementing this costs-of- quality approach?

What alternative approach could they use to measure quality improvement?

SOLUTION

Requirement 1

Activity

Predicted

Reduction in

Activity Units

×

Predetermined

Overhead

Allocation Rate

per Unit

=

Predicted

Quality Cost

Savings

Inspection of incoming raw materials

415

×

$ 39

=

$ 16,185

Inspection of finished goods

415

×

=

by customers

Lost sales due to dissatisfied customers

×

=

Total

Requirement 2

Total predicted quality cost savings

$ 129,265

Design engineering cost

(100,000)

Net benefit

$ 29,265

Requirement 3

Problems (Group B)

P19-38B Comparing costs from ABC and single-rate systems

Learning Objectives 1, 2

2. Travel packs $1.70

Haywood Pharmaceuticals manufactures an over-the-counter allergy medication. The company sells

both large commercial containers of 1,000 capsules to health care facilities and travel packs of 20

capsules to shops in airports, train stations, and hotels. The following information has been developed to

determine if an activity-based costing system would be beneficial:

Requirements

1. Compute the predetermined overhead allocation rate for each activity.

2. Use the predetermined overhead allocation rates to compute the activity-based costs per unit of the

commercial containers and the travel packs. Round to two decimal places. (Hint: First compute the

total activity-based costs allocated to each product line, and then compute the cost per unit.)

3. Haywood’s original single plantwide overhead allocation rate system allocated indirect costs to

products at $151.00 per machine hour. Compute the total indirect costs allocated to the commercial

containers and to the travel packs under the original system. Then compute the indirect cost per unit

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

5,475 total estimated machine hours

Requirement 2

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Commercial containers

Materials handling

$4.00 per kilo

×

13,500 kilos

=

$ 54,000

Packaging

$40.00 per MHr

×

2,250 MHr

=

90,000

Quality assurance

$60.00 per sample

×

300 samples

=

18,000

Total activity-based costs

$ 162,000

÷ Number of units

Activity-based cost per unit

$ 54.00

Travel packs

Materials handling

$4.00 per kilo

×

=

$ 22,800

Quality assurance

$60.00 per sample

×

855 samples

=

51,300

Total activity-based costs

$ 96,900

÷ Number of units

÷ 57,000 units

Activity-based cost per unit

$ 1.70

P19-38B, cont.

Requirement 3

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Commercial containers

Total indirect costs

$151.00per MHr

×

2,250 MHr

=

$ 339,750.00

÷ Number of units

÷ 3,000 units

Indirect cost per unit

$ 113.25

Travel packs

Total indirect costs

$151.00 per MHr

×

570 MHr

=

÷ Number of units

Indirect cost per unit

Requirement 4

Comparison of manufacturing overhead cost per unit:

Traditional

System

ABC

System

Difference

Commercial

Containers

$ 113.25 per unit(a)

–

$ 54.00 per unit(b)

=

$59.25

P19-39B Computing product costs in an ABC system

Learning Objective 2

1. Total activity-based costs $56.10

The Arial Manufacturing Company in Rochester, Minnesota, assembles and tests electronic components

used in smartphones. Consider the following data regarding component T24 (amounts are per unit):

Requirements

1. Complete the missing items for the two tables.

2. Why might managers favor this ABC system instead of Arial’s older system, which allocated all

manufacturing overhead costs on the basis of direct labor hours?

SOLUTION

Requirement 1

Activity

Allocation Base

Cost Allocated

to each Unit

Start station

Number of raw component chassis

5

×

$ 1.30

=

$ 6.50

28(a)

Manual insertion

Number of manual insertions

13

0.20

2.60(b)

Wave solder

Number of components soldered

5

×

1.90

=

9.50

0.40(c)

Test

Number of testing hours

0.41

50.00

20.50(d)

Direct materials cost

$ 79.00

Direct labor cost

22.00

Activity-based costs allocated

56.10(f)

Total manufacturing product cost

$ 157.10

Calculations:

(a)

$9.80

/

$0.35

=

28

(b)

13

×

$0.20

=

$2.60

(c)

$3.20

/

8

=

$0.40

(d)

0.41

×

$50.00

=

$20.50

(e)

$4.00

/

0.10

=

$40.00

(f)

Sum of column

Requirement 2

Because the traditional (older) costing system doesn’t reflect the way products actually use the

P19-40B Computing product costs in an ABC system

Learning Objectives 2, 3

1. Standard $75 per unit

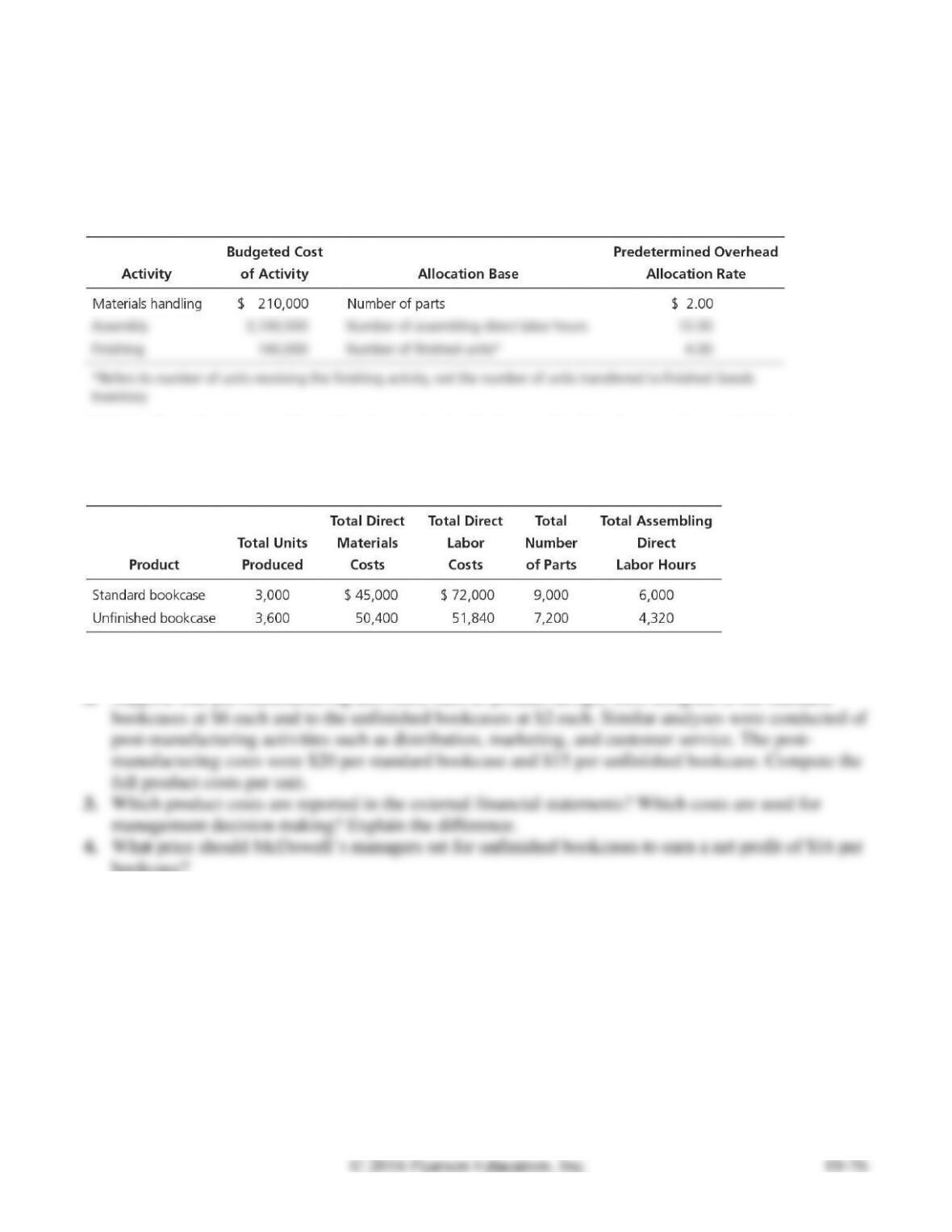

McDowell, Inc. manufactures bookcases and uses an activity-based costing system. McDowell’s activity

areas and related data follow:

McDowell produced two styles of bookcases in April: the standard bookcase and an unfinished

bookcase, which has fewer parts and requires no finishing. The totals for quantities, direct materials

costs, and other data follow:

Requirements

1. Compute the manufacturing product cost per unit of each type of bookcase.

2. Suppose that pre-manufacturing activities, such as product design, were assigned to the standard

bookcase?

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Standard bookcases

Materials handling

×

=

×

=

78,000

×

=

Total manufacturing

bookcases

Materials handling

×

=

×

=

56,160

×

=

Total manufacturing

overhead cost

Standard

bookcases

Unfinished

bookcases

Total direct materials cost

$ 45,000

$ 50,400

Total direct labor cost

72,000

51,840

Total manufacturing overhead cost

70,560

Total manufacturing product cost

$ 225,000

$ 172,800

÷ Number of units

Manufacturing product cost per unit

$ 75

$ 48