Chapter 19

Management Systems: Activity-Based, Just-In-Time, and Quality

Management Systems

Review Questions

1. What is the formula to compute the predetermined overhead allocation rate?

2. How is the predetermined overhead allocation rate used to allocate overhead?

3. Describe how a single plantwide overhead allocation rate is used.

Using a single plantwide rate is the traditional method of allocating overhead costs and is the

4. Why is using a single plantwide overhead allocation rate not always accurate?

Using a single plantwide overhead allocation rate is not always accurate because it is based on only

5. Why is the use of departmental overhead allocation rates considered a refinement over the use of a

single plantwide overhead allocation rate?

Using departmental overhead allocation rates is considered a refinement over using a single

6. What is activity-based management? How is it different from activity-based costing?

7. How many cost pools are in an activity-based costing system?

An activity-based costing system identifies activities and their corresponding costs (and allocation

8. What are the four steps to developing an activity-based costing system?

The four steps to developing an activity-based costing system are:

9. Why is ABC usually considered more accurate than traditional costing methods?

10. List two ways managers can use ABM to make decisions.

11. Define value engineering. How is it used to control costs?

Value engineering is reevaluating activities to reduce costs while still meeting customer needs. Most

12. Explain the difference between target price and target cost.

Target price is the amount customers are willing to pay for a product or service. Target cost is the

13. How can ABM be used by service companies?

ABM is not just for manufacturing companies. ABM can be used in determining the cost of services

14. What is a just-in-time management system?

A just-in-time management system is an inventory management system in which a company

15. Explain how the work cell manufacturing layout increases productivity.

Production in JIT management systems is completed in self-contained work cells. A work cell is an

area in which everything needed to complete a manufacturing process is readily available. Each

16. What are the inventory accounts used in JIT costing?

17. How is the Conversion Costs account used in JIT costing?

In a JIT costing system, direct labor and manufacturing overhead costs are combined into a single

18. Why is JIT costing sometimes called backflush costing?

19. Which accounts are adjusted for the underallocated or overallocated overhead in JIT costing?

The Conversion Costs account is a temporary account. Actual conversion costs accumulate as debits

20. What is the purpose of quality management systems?

21. List and define the four types of quality costs.

The four types of quality costs and their definitions are as follows:

22. “Prevention is much cheaper than external failure.” Do you agree with this statement? Why or why

not?

I agree with the statement “Prevention is much cheaper than external failure.” Most prevention costs

23. What are quality improvement programs?

Quality improvement programs help managers improve the business’s performance by providing

24. Why are some quality costs hard to measure?

Some quality costs are hard to measure because they don’t appear in a company’s accounting

Short Exercises

S19-1 Computing single plantwide overhead allocation rates

Learning Objective 1

The Oakman Company manufactures products in two departments: Mixing and Packaging. The

company allocates manufacturing overhead using a single plantwide rate with direct labor hours as the

allocation base. Estimated overhead costs for the year are $920,000, and estimated direct labor hours are

400,000. In October, the company incurred 55,000 direct labor hours.

Requirements

1. Compute the predetermined overhead allocation rate. Round to two decimal places.

2. Determine the amount of overhead allocated in October.

SOLUTION

Requirement 1

Predetermined

Total estimated overhead costs

Requirement 2

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

$126,500

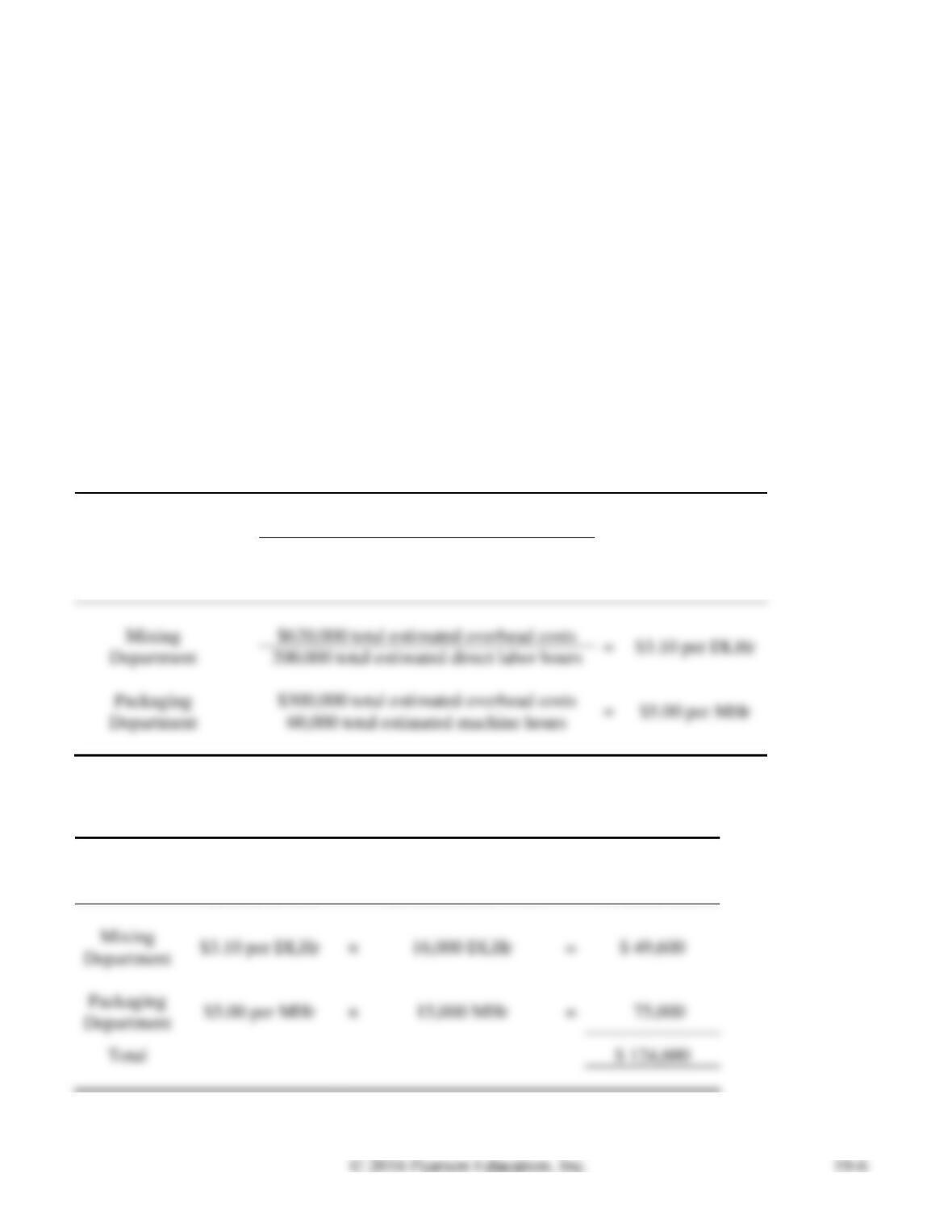

S19-2 Computing departmental overhead allocation rates

Learning Objective 1

The Oakman Company (see Short Exercise S19-1) has refined its allocation system by separating

manufacturing overhead costs into two cost pools—one for each department. The estimated costs for the

Mixing Department, $620,000, will be allocated based on direct labor hours, and the estimated direct

labor hours for the year are 200,000. The estimated costs for the Packaging Department, $300,000, will

be allocated based on machine hours, and the estimated machine hours for the year are 60,000. In

October, the company incurred 16,000 direct labor hours in the Mixing Department and 15,000 machine

hours in the Packaging Department.

Requirements

1. Compute the predetermined overhead allocation rates. Round to two decimal places.

2. Determine the total amount of overhead allocated in October.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

Requirement 2

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Packaging

S19-3 Using activity-based costing

Learning Objective 2

Activity-based costing requires four steps. List the four steps in the order they are performed.

SOLUTION

Step 1: Identify activities and estimate their total indirect costs.

S19-4 Calculating costs using traditional and activity-based systems

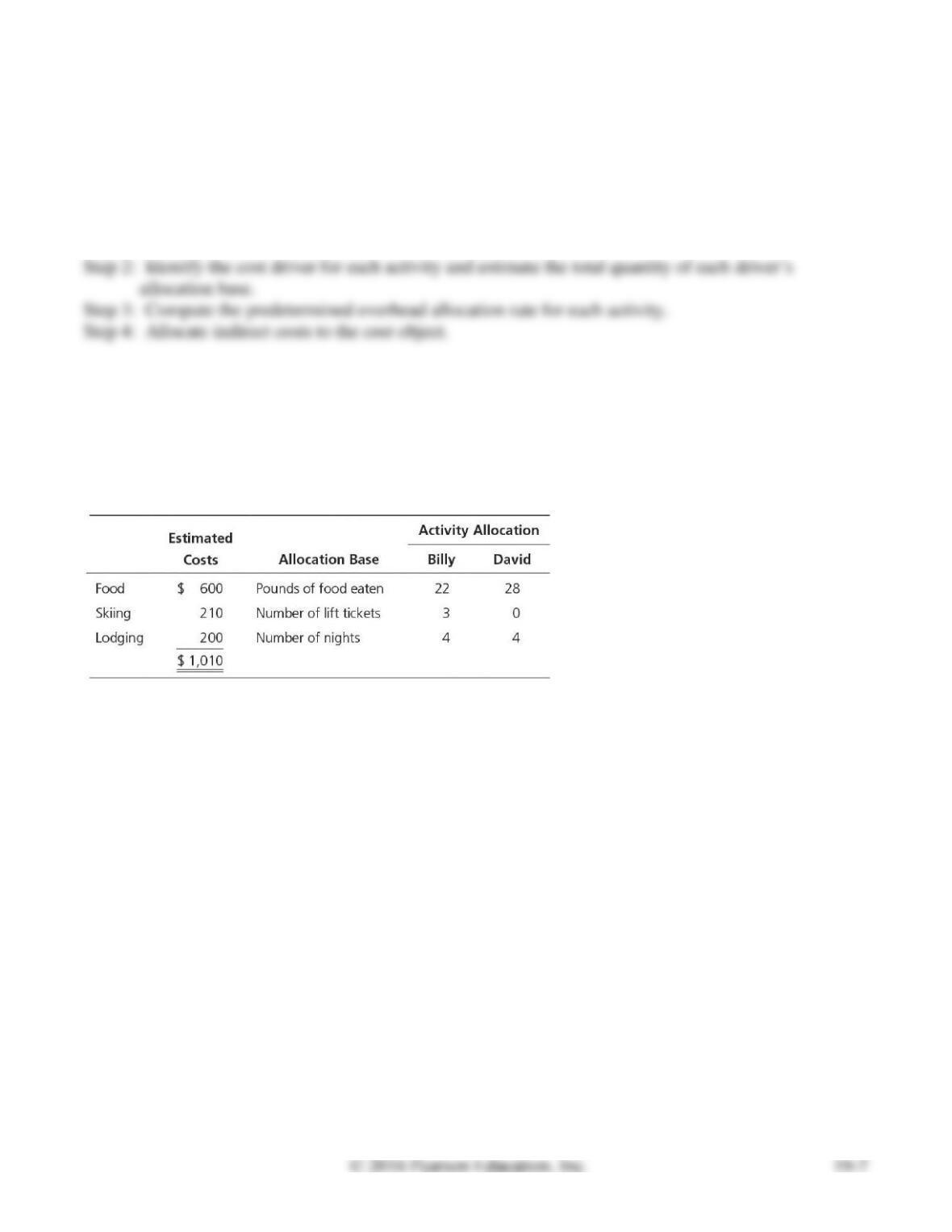

Learning Objectives 1, 2

Billy and David are college friends planning a skiing trip to Killington before the new year. They

estimated the following for the trip:

Requirements

1. Billy suggests that the costs be shared equally. Calculate the amount each person would pay.

2. David does not like the idea because he plans to stay in the room rather than ski. David suggests that

each type of cost be allocated to each person based on the above-listed allocation bases. Using the

activity allocation for each person, calculate the amount that each person would pay based on his

own consumption of the activity.

SOLUTION

Requirement 1

Cost per person

=

$1,010 total cost

/

2 people

=

$505 per person

Requirement 2

Billy

+

David

=

Total

Total pounds of food eaten

=

22 pounds

+

28 pounds

=

50 pounds

Total number of lift tickets

=

3 tickets

+

0 tickets

=

3 tickets

Total number of nights

=

4 nights

+

4 nights

=

8 nights

S19-4, cont.

Requirement 2, cont.

Predetermined

Overhead

Allocation Rate

×

Quantity

of the

Allocation Base

Used

=

Allocated

Cost

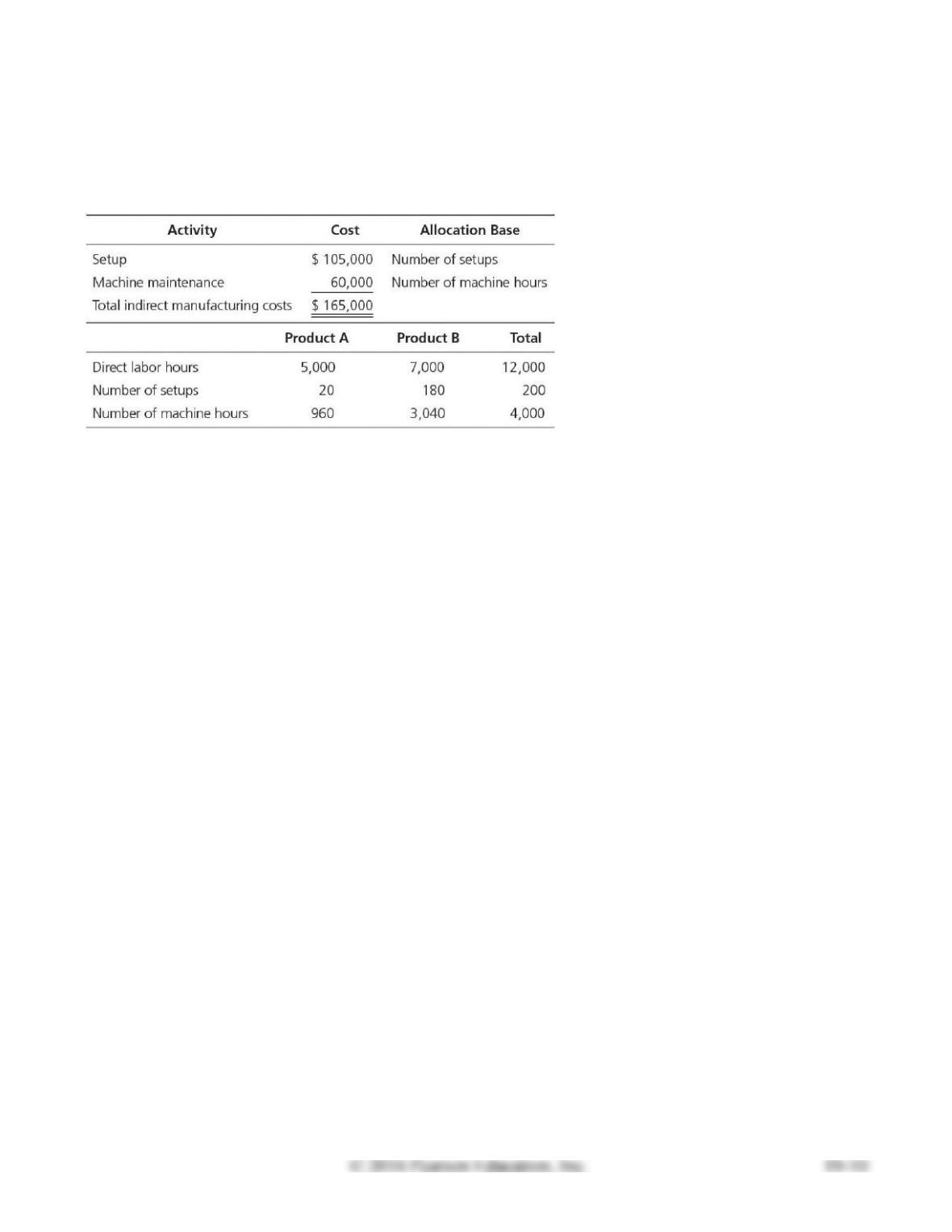

S19-5 Computing indirect manufacturing costs per unit

Learning Objective 2

Daily Corp. is considering the use of activity-based costing. The following information is provided for

the production of two product lines:

Daily plans to produce 200 units of Product A and 300 units of Product B. Compute the ABC indirect

manufacturing cost per unit for each product.

SOLUTION

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Product A

Setup

$525.00 per setup

×

20 setups

=

$ 10,500

Machine maintenance

$15.00 per MHr

×

960 MHr

=

14,400

Total manufacturing

overhead costs

Manufacturing

overhead cost per unit

$ 124.50

Product B

Setup

$525.00 per setup

×

=

$ 94,500

Machine maintenance

$15.00 per MHr

×

=

45,600

Total manufacturing

overhead costs

Manufacturing

overhead cost per unit

$ 467.00

S19-6 Computing indirect manufacturing costs per unit, traditional and ABC

Learning Objectives 1, 2

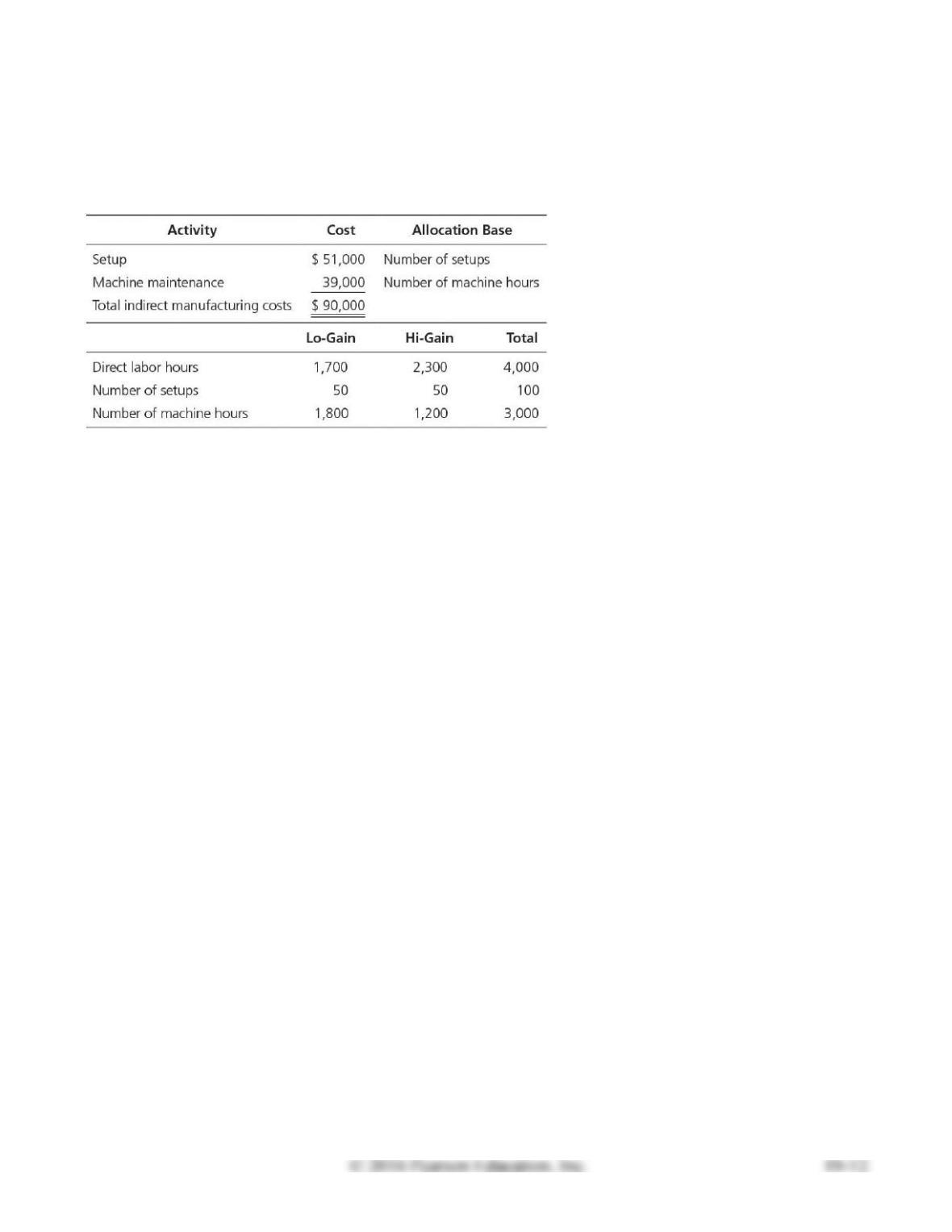

The following information is provided for Space Antenna Corp., which manufactures two products: Lo-

Gain antennas and Hi-Gain antennas for use in remote areas.

Space Antenna plans to produce 175 Lo-Gain antennas and 350 Hi-Gain antennas.

Requirements

1. Compute the ABC indirect manufacturing cost per unit for each product.

2. Compute the indirect manufacturing cost per unit using direct labor hours for the single plantwide

predetermined overhead allocation rate.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Lo-Gain antennas

Setup

$510 per setup

×

50 setups

=

$ 25,500

Machine maintenance

$13 per MHr

×

1,800 MHr

=

23,400

Total manufacturing

overhead costs

$ 48,900

÷ Number of units

Manufacturing

overhead cost per unit

Setup

$510 per setup

×

50 setups

=

$ 25,500

Machine maintenance

$13 per MHr

×

1,200 MHr

=

15,600

Total manufacturing

overhead costs

$ 41,100

÷ Number of units

S19-6, cont.

Requirement 2

Predetermined

Overhead

Allocation Rate

=

Total estimated overhead costs

Total estimated quantity of the

overhead allocation base

Overhead Cost

S19-7 Using ABC to compute product costs per unit

Learning Objective 2

Johnstone Corp. manufactures mid-fi and hi-fi stereo receivers. The following data have been

summarized:

Indirect manufacturing cost information includes the following:

SOLUTION

Predetermined Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Mid-Fi receivers

Setup

$1,300 per setup

×

35 setups

=

$ 45,500

Inspections

$900 per inspection hour

×

25 inspection hours

=

22,500

Machine maintenance

$12 per MHr

×

1,600 MHr

=

19,200

Total manufacturing

overhead costs

÷ Number of units

$ 436.00

Hi-Fi receivers

Setup

$1,300 per setup

×

35 setups

=

$ 45,500

Inspections

$900 per inspection hour

×

10 inspection hours

=

9,000

Machine maintenance

$12 per MHr

×

1,350 MHr

=

16,200

Total manufacturing

overhead costs

÷ Number of units

Manufacturing

overhead cost per unit

$ 282.80

Mid-Fi receivers

Hi-Fi receivers

Direct materials cost per unit

$ 800.00

$ 1,500.00

Direct labor cost per unit

200.00

100.00

Manufacturing overhead cost per unit

436.00

282.80

Total product cost per unit

$ 1,436.00

$ 1,882.80

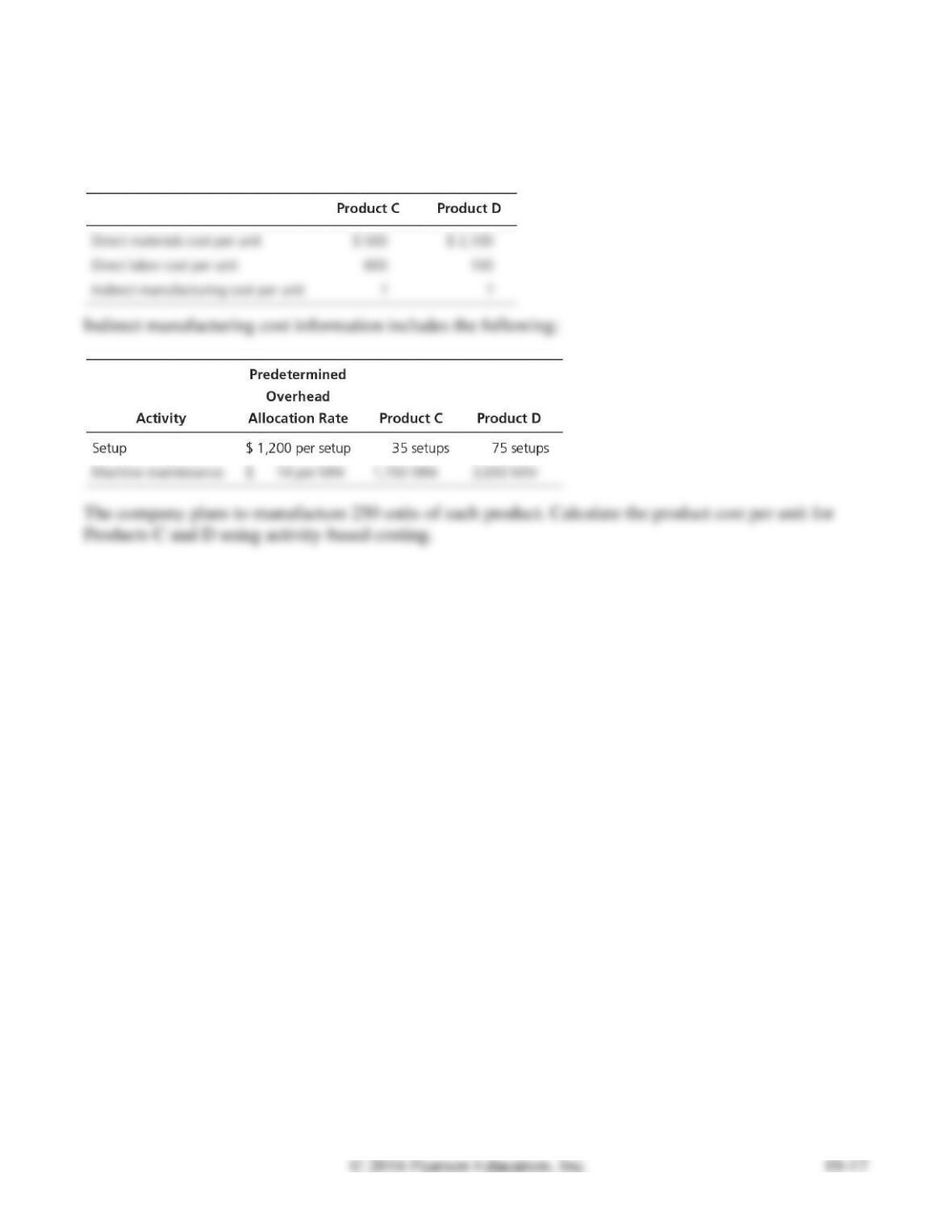

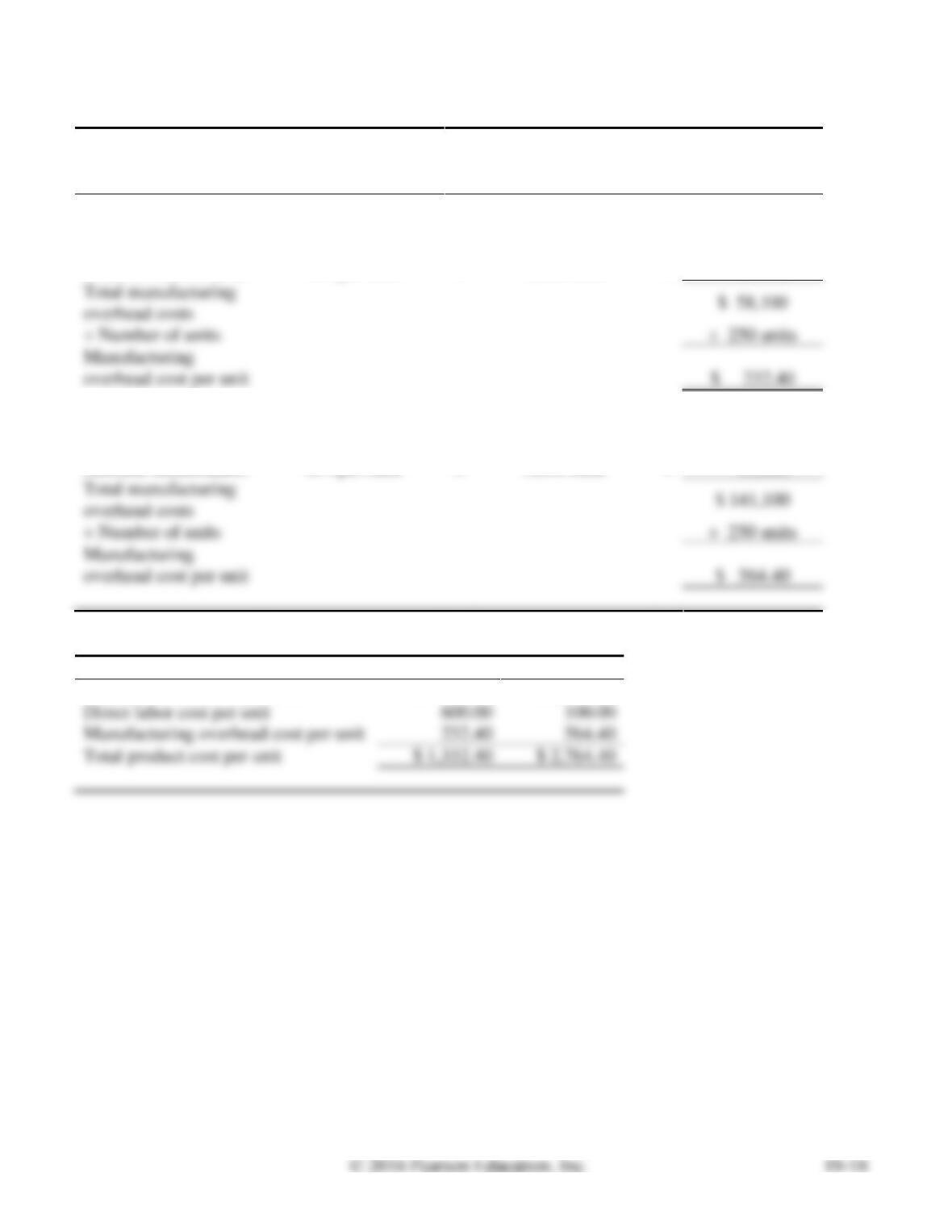

S19-8 Using ABC to compute product costs per unit

Learning Objective 2

Elm Corp. makes two products: C and D. The following data have been summarized:

SOLUTION

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Product C

Setup

$1,200 per setup

×

35 setups

=

$ 42,000

Machine maintenance

$14 per MHr

×

1,150 MHr

=

16,100

Total manufacturing

÷ Number of units

Manufacturing

overhead cost per unit

$ 232.40

Product D

Setup

$1,200 per setup

×

75 setups

=

$ 90,000

Machine maintenance

$14 per MHr

×

3,650 MHr

=

51,100

Total manufacturing

overhead costs

÷ Number of units

Manufacturing

overhead cost per unit

$ 564.40

Product C

Product D

Direct materials cost per unit

$ 500.00

$ 2,100.00

Direct labor cost per unit

Manufacturing overhead cost per unit

Total product cost per unit

$ 1,332.40

$ 2,764.40

Note: Short Exercise S19-8 must be completed before attempting Short Exercise S19-9.

S19-9 Using ABM to achieve target profit

Learning Objective 3

Refer to Short Exercise S19-8. Elm Corp. desires a 25% target gross profit after covering all product

costs. Considering the total product costs assigned to the Products C and D in Short Exercise S19-8,

what would Elm have to charge the customer to achieve that gross profit? Round to two decimal places.

SOLUTION

Desired gross profit per unit

=

Required sales price per unit

–

Product cost per unit

Required sales price per unit × 25%

=

Required sales price per unit

–

Product cost per unit

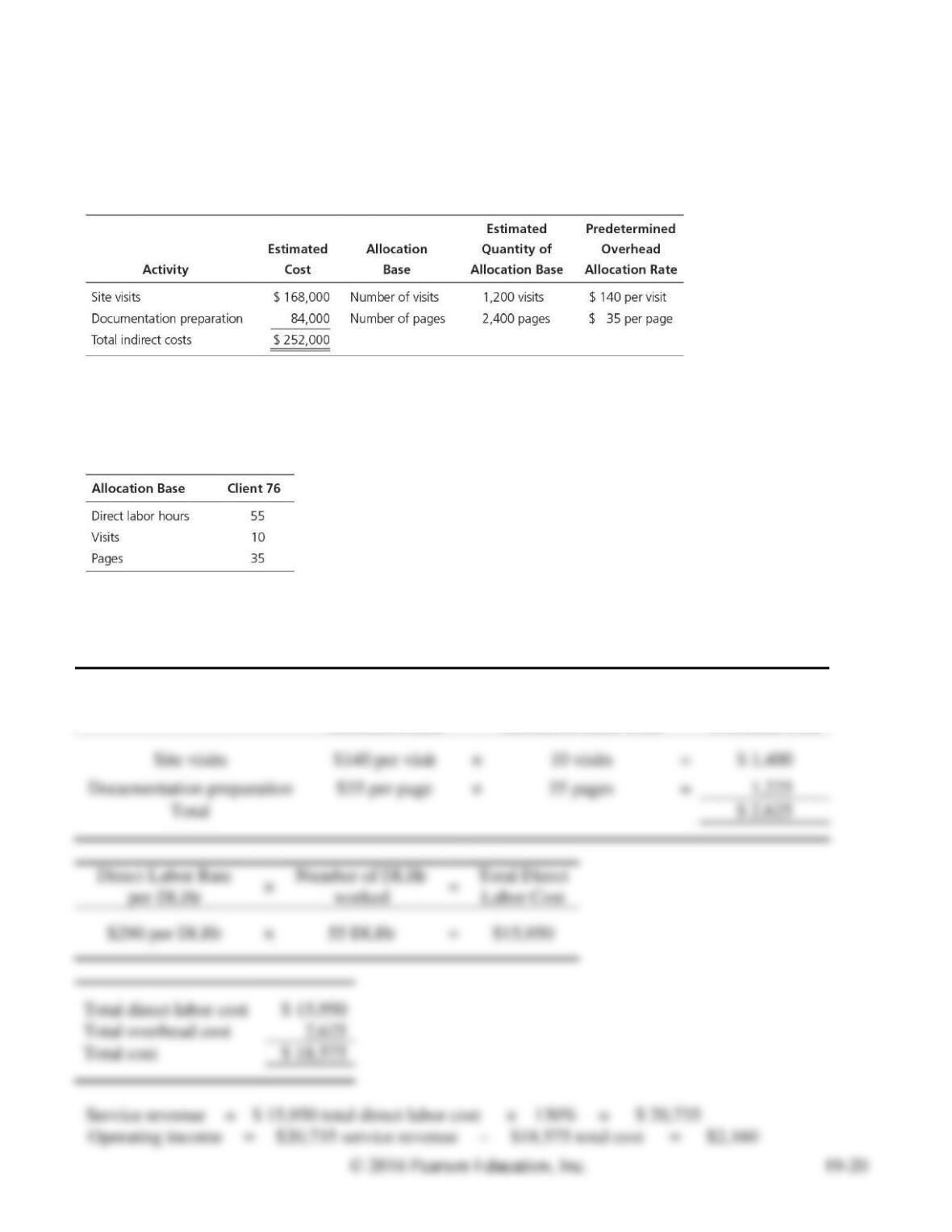

S19-10 Using ABM in a service company

Learning Objective 4

Western Company is a management consulting firm. The company expects to incur $252,000 of indirect

costs this year. Indirect costs are allocated based on the following activities:

Western bills clients at 130% of the direct labor costs. The company has estimated direct labor costs at

$290 per hour. Last month, Western completed a consulting job for Client 76 and used the following

resources:

Determine the total cost of the consulting job and the operating income earned.

SOLUTION

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Overhead Cost

×

=

×

=

×

=

Total direct labor cost

Total overhead cost

Total cost