Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P19-40B, cont.

Requirement 2

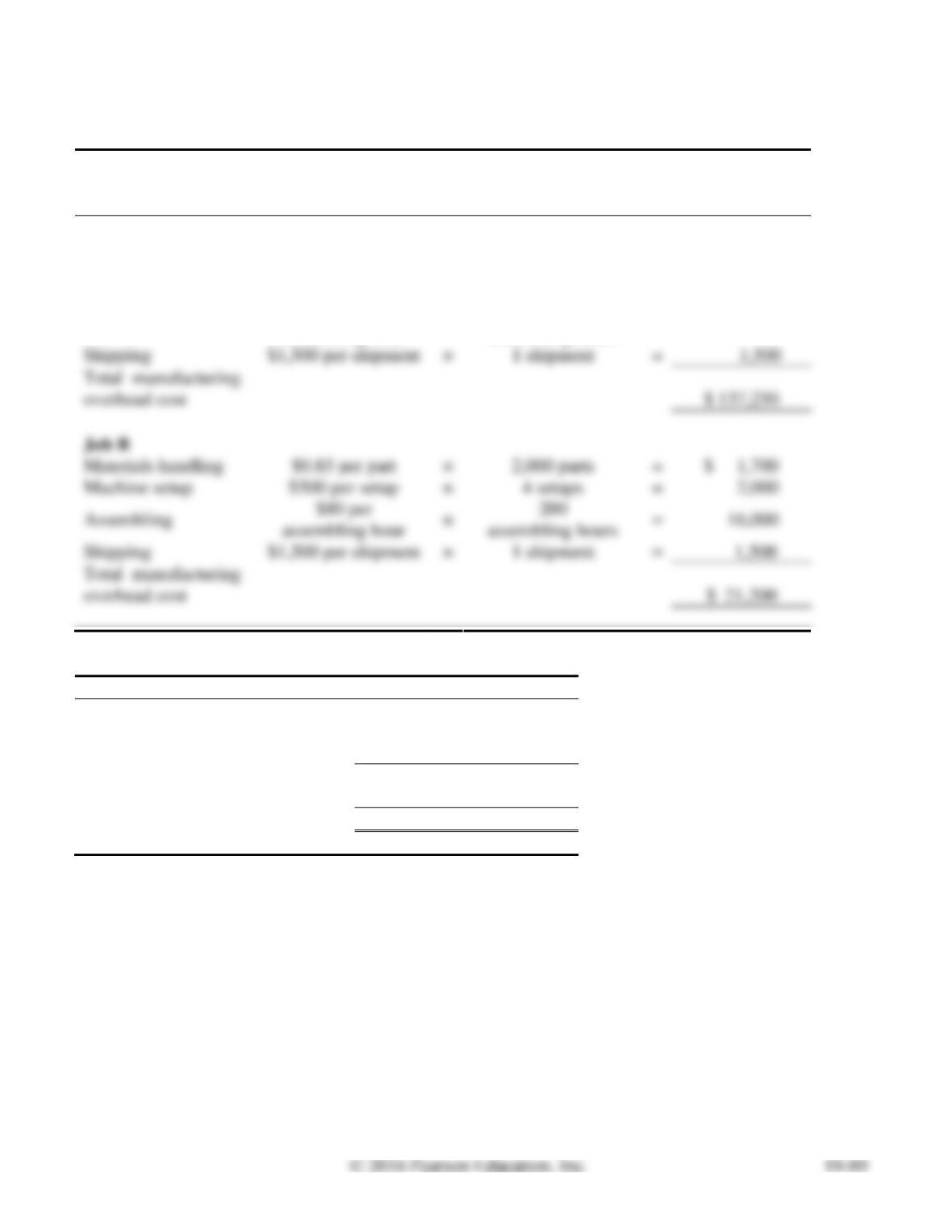

Standard

Unfinished

Requirement 3

Manufacturing product costs are reported in the external financial statements in the inventory accounts

on the balance sheet and Cost of Goods Sold on the income statement. Full product costs are used for

Requirement 4

Sales price per unit

=

Full product cost

+

Net profit

=

$65(b)

+

$16

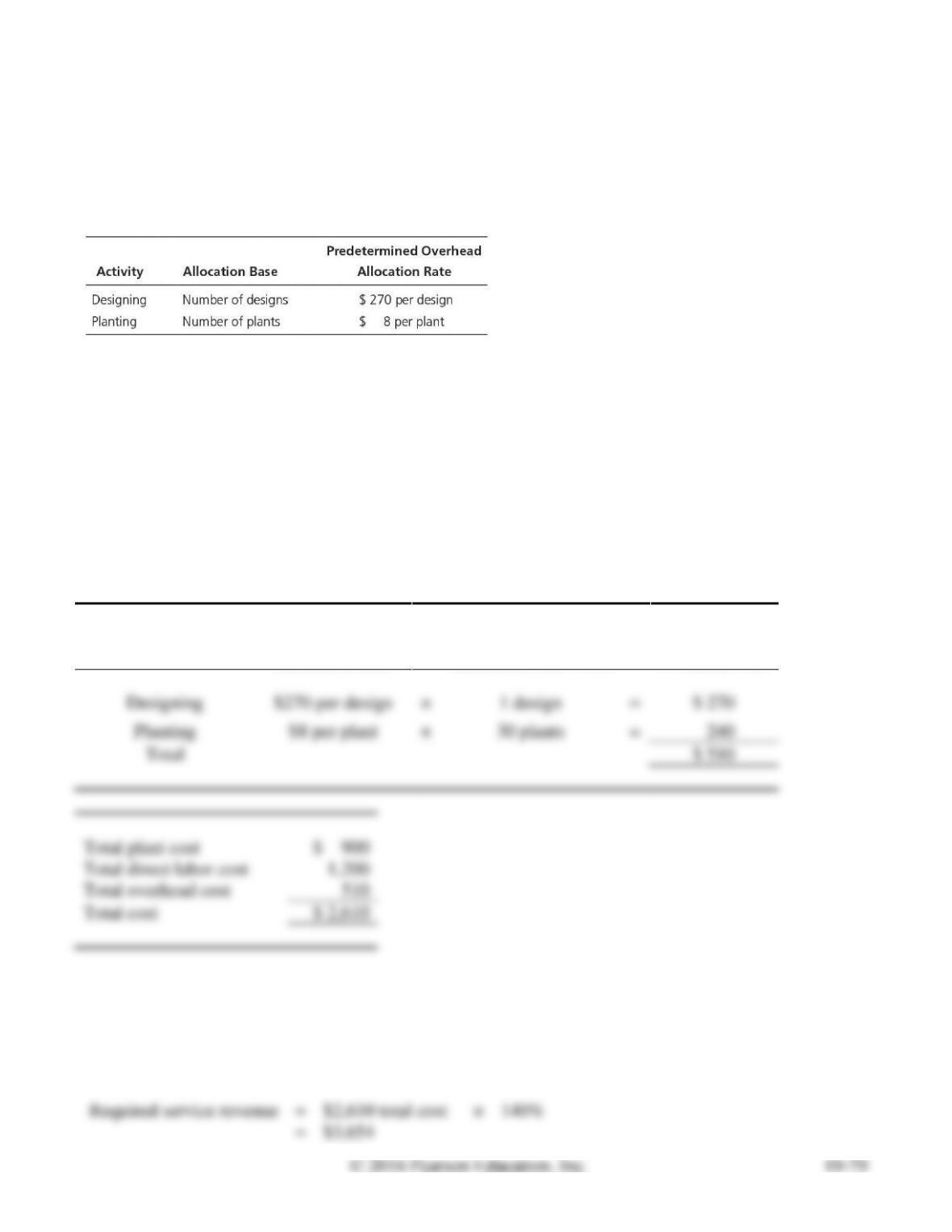

P19-41B Using ABC in a service company

Learning Objective 4

1. Total OH cost $510

Weston Plant Service completed a special landscaping job for Briggs Company. Weston uses ABC and

has the following predetermined overhead allocation rates:

The Briggs job included $900 in plants; $1,200 in direct labor; one design; and 30 plants.

Requirements

1. What is the total cost of the Briggs job?

2. If Briggs paid $3,410 for the job, what is the operating income or loss?

3. If Weston desires an operating income of 40% of cost, how much should the company charge for the

Briggs job?

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Overhead Cost

Requirement 2

Profit

=

$3,410 service revenue

–

$2,610 total cost

=

$800

Requirement 3

P19-42B Recording manufacturing costs for a JIT system

Learning Objective 5

2. Conversion Costs $380,000 CR

High Range produces fleece jackets. The company uses JIT costing for its JIT production system.

High Range has two inventory accounts: Raw and In-Process Inventory and Finished Goods

Inventory. On February 1, 2016, the account balances were Raw and In-Process Inventory, $13,000;

Finished Goods Inventory, $2,000.

The standard cost of a jacket is $36, composed of $16 direct materials plus $20 conversion costs. Data

for February’s activities follow:

Requirements

1. What are the major features of a JIT production system such as that of High Range?

2. Prepare summary journal entries for February. Underallocated or overallocated conversion costs are

adjusted to Cost of Goods Sold monthly.

3. Use a T-account to determine the February 29, 2016, balance of Raw and In-Process Inventory.

SOLUTION

Requirement 1

A just-in-time management system is an inventory management system in which a company produces

just in time to satisfy customer needs. Suppliers deliver raw materials just in time to begin production

and finished units are completed just in time for delivery to customers.

P19-42B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Raw and In-Process Inventory

299,000

Accounts Payable

299,000

Requirement 3

Raw and In-Process Inventory

Feb. 1 13,000

304,000

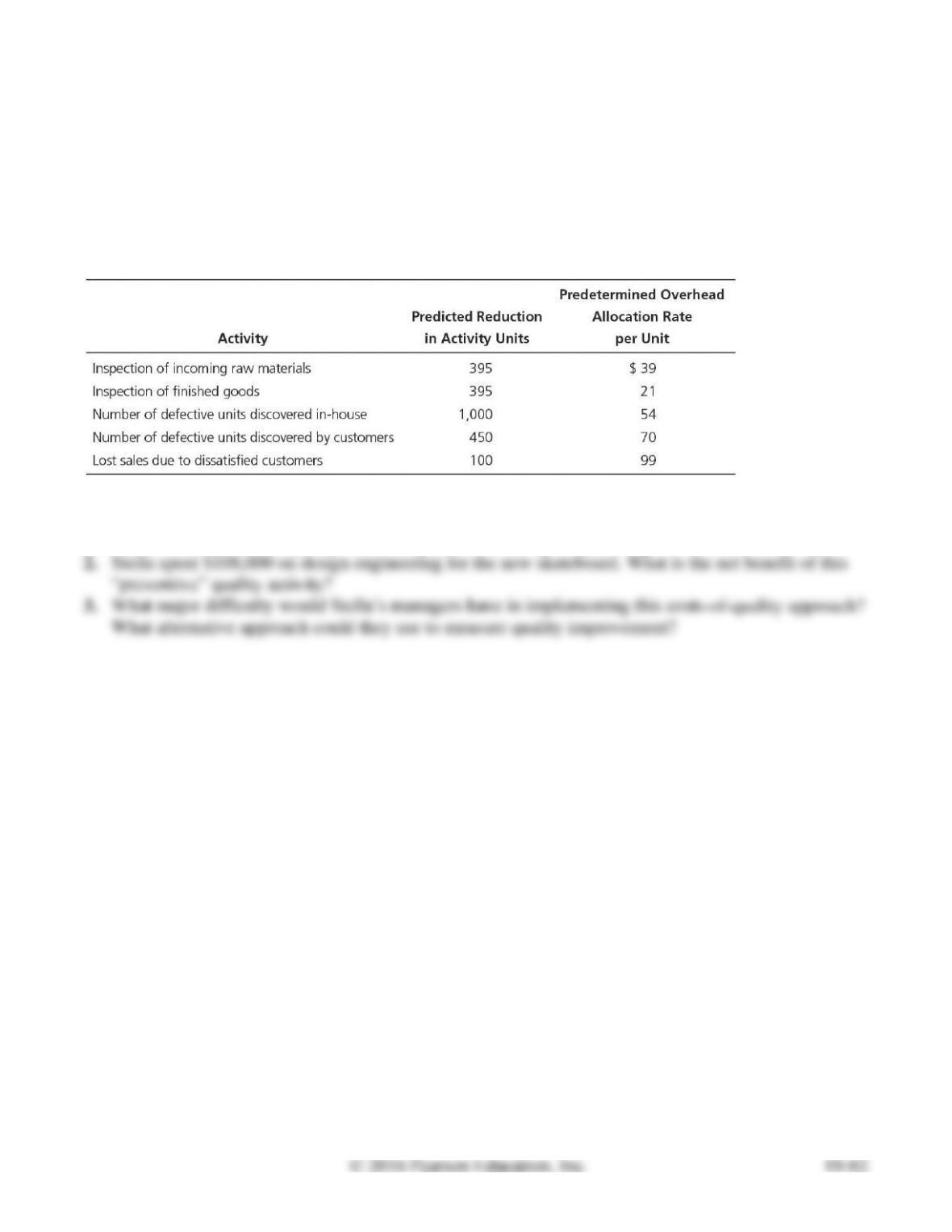

P19-43B Analyzing costs of quality

Learning Objective 6

2. Net benefit $11,100

Stella, Inc. is using a costs-of-quality approach to evaluate design engineering efforts for a new

skateboard. Stella’s senior managers expect the engineering work to reduce appraisal, internal failure,

and external failure activities. The predicted reductions in activities over the two-year life of the

skateboards follow. Also shown are the predetermined overhead allocation rates for each activity.

Requirements

1. Calculate the predicted quality cost savings from the design engineering work.

SOLUTION

Requirement 1

Activity

Predicted

Reduction in

Activity Units

×

Predetermined

Overhead

Allocation Rate

per Unit

=

Predicted

Quality Cost

Savings

Inspection of incoming raw

materials

395

×

$ 39

=

$ 15,405

Requirement 2

Total predicted quality cost savings

$ 119,100

Requirement 3

Some quality costs are hard to measure because they don’t appear in a company’s accounting records;

Continuing Problem

P19-44 Comparing costs from ABC and single-rate systems

This problem continues the Daniels Consulting situation from Problem P17-40 of Chapter 17. Recall

that Daniels allocated indirect costs to jobs based on a predetermined overhead allocation rate, computed

as a percentage of direct labor costs. Because Daniels provides a service, there are no direct materials

costs. Daniels is now considering using an ABC system. Information about ABC costs follows:

Records for two clients appear here:

Requirements

1. Compute the total cost for each job. The cost of direct labor is $176 per hour.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Overhead

Cost

Tommy’s Trains

Design

$1,350 per design

×

3 designs

=

$ 4,050

Marcia’s Cookies

Design

$1,350 per design

×

4 designs

=

$ 5,400

Direct Labor Rate

per DLHr

×

Number of DLHr

worked

=

Total Direct

Labor Cost

Tommy’s

Trains

Marcia’s

Cookies

Total travel and meal costs

$ 10,700

$ 600

P19-44, cont.

Requirement 2

Compared with Problem P17-40, the total cost of the Tommy’s Trains is $2,828 less tahn using ABC

($162,470 – $165,298) and the total cost of Marcia’s Cookies is $5,656 greater using ABC ($49,200 –

$43,544).

Requirement 3

Desired

Operating Income

=

Total Cost

×

25%

Tommy’s Trains

=

$ 162,470

×

25%

=

$ 40,618

CRITICAL THINKING

Decision Cases

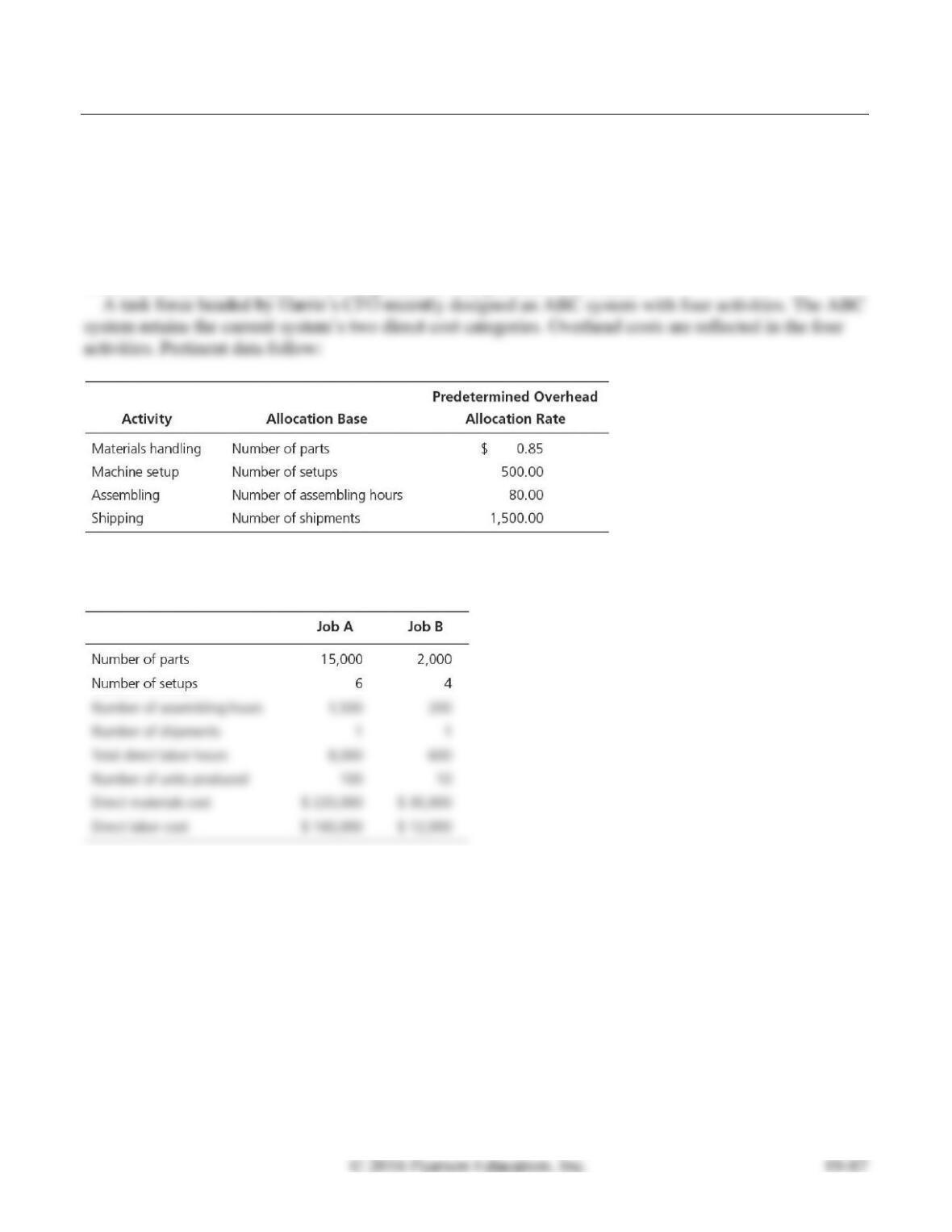

Decision Case 19-1

Harris Systems specializes in servers for workgroup, e-commerce, and ERP applications. The

company’s original job costing system has two direct cost categories: direct materials and direct labor.

Overhead is allocated to jobs at the single rate of $22 per direct labor hour.

Harris Systems has been awarded two new contracts, which will be produced as Job A and Job B.

Budget data relating to the contracts follow:

Requirements

1. Compute the budgeted product cost per unit for each job, using the original costing system (with two

direct cost categories and a single overhead allocation rate).

2. Suppose Harris Systems adopts the ABC system. Compute the budgeted product cost per unit for

each job using ABC.

3. Which costing system more accurately assigns to jobs the costs of the resources consumed to

produce them? Explain.

SOLUTION

Requirement 1

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base

Used

=

Allocated

Manufacturing

Overhead Cost

Job A

Job B

Total direct materials cost

$ 220,000

$ 30,000

Total direct labor cost

160,000

12,000

Decision Case 19-1, cont.

Requirement 2

Predetermined

Overhead

Allocation Rate

×

Actual Quantity

of the

Allocation Base Used

=

Allocated

Manufacturing

Overhead Cost

Job A

Materials handling

$0.85 per part

×

15,000 parts

=

$ 12,750

Machine setup

$500 per setup

×

6 setups

=

3,000

Assembling

$80 per

assembling hour

×

1,500

assembling hours

=

120,000

Job A

Job B

Total direct materials cost

$ 220,000

$ 30,000

Total direct labor cost

160,000

12,000

Total manufacturing overhead cost

137,250

21,200

Total product cost

$ 517,250

$ 63,200

÷ Number of units

÷ 100 units

÷ 10 units

Product cost per unit

$ 5,172.50

$ 6,320

Decision Case 19-1, cont.

Requirement 3

Total Direct

Labor Hours

/

Number

of units

=

Direct Labor Hours

per Unit

Total Quantity

of the

Allocation Base Used

/

Number

of units

=

Quantity of

the Allocation Base

Used per Unit

Job A

Materials handling

15,000 parts

/

100 units

=

150 parts

Total

manufacturing

overhead cost

/

Number

of units

=

Manufacturing overhead

cost per unit

Job A

Traditional System

$176,000(a)

/

100 units

=

$ 1,760.00 per unit

ABC System

$137,250(b)

/

100 units

=

$ 1,372.50 per unit

Decision Case 19-1, cont.

Requirement 3, cont.

Comparison of manufacturing overhead cost per unit:

Traditional System

ABC System

Difference

Job A

$ 1,760.00 per unit

–

$ 1,372.50 per unit

=

$ 387.50

Job B

$ 1,320.00 per unit

–

$ 2,120.00 per unit

=

$ (800.00)

One unit of Job A requires 1.33 times as many direct labor hours than does one unit of Job B (80 direct

labor hours per unit / 60 direct labor hours per unit). However, one unit of Job B actually requires more

activity allocation base quantities using ABC for all four activities, as shown in the following table:

Quantity of the

Allocation Base

Used per Unit

for Job B

/

Quantity of the

Allocation Base

Used per Unit

for Job A

=

Ratio of the

Quantity of the

Allocation Base

Used per Unit

Materials handling

200 parts

/

150 parts

=

1.33 times

Decision Case 19-2

Harris Systems has decided to adopt ABC. To remain competitive, Harris Systems’s management

believes the company must produce the type of servers produced in Job B (from Decision Case 19-1) at

a target cost of $5,400. Harris Systems has just joined a B2B e-market site that management believes

will enable the firm to cut direct materials costs by 10%. Harris’s management also believes that a value

engineering team can reduce assembly time.

Compute the assembling cost savings required per Job B-type server to meet the

$5,400 target cost. (Hint: Begin by calculating the direct materials, direct labor, and

allocated overhead costs per server.)

SOLUTION

Revised total direct materials cost

=

Original total cost

×

(1 – 10%)

=

$30,000

×

90%

=

$27,000

Original assembling

cost per server

=

Original total

assembling cost

/

Number

of servers

=

$16,000 (c)

/

10

=

$1,600

(c)

Calculated in Decision Case 19-1

© 2016 Pearson Education, Inc.

19-93

Ethical Issue 19-1

Cassidy Manning is assistant controller at LeMar Packaging, Inc., a manufacturer of cardboard boxes

and other packaging materials. Manning has just returned from a packaging industry conference on

activity-based costing. She realizes that ABC may help LeMar meet its goal of reducing costs by 5%

over each of the next three years.

LeMar Packaging’s Order Department is a likely candidate for ABC. While orders are entered into a

computer that updates the accounting records, clerks manually check customers’ credit history and hand-

deliver orders to shipping. This process occurs whether the sales order is for a dozen specialty boxes

worth $80 or 10,000 basic boxes worth $8,000.

Manning believes that identifying the cost of processing a sales order would justify (1) further

computerization of the order process and (2) changing the way the company processes small orders.

However, the significant cost savings would arise from elimination of two positions in the Order

Department. The company’s sales order clerks have been with the company many years. Manning is

uncomfortable with the prospect of proposing a change that will likely result in terminating these

employees.

Use the IMA’s ethical standards (see Chapter 16) to consider Manning’s responsibility when cost

savings come at the expense of employees’ jobs.

SOLUTION

The IMA standard of competence states that management accountants should “provide decision support

information and recommendations that are accurate, clear, concise, and timely”.

Fraud Case 19-1

Anu Ghai was a new production analyst at RHI, Inc., a large furniture factory in North Carolina. One of

her first jobs was to update the predetermined overhead allocation rates for factory production costs.

This was normally done once a year, by analyzing the previous year’s actual data, factoring in projected

changes, and calculating a new rate for the coming year. What Anu found was strange. The activity rate

for “maintenance” had more than doubled in one year, and she was puzzled how that could have

happened. When she spoke with Larry McAfee, the factory manager, she was told to spread the

increases out over the other activity costs to “smooth out” the trends. She was a bit intimidated by Larry,

an imposing and aggressive man, but she knew something wasn’t quite right. Then one night she was at

a restaurant and overheard a few employees who worked at RHI talking. They were joking about the

work they had done fixing up Larry’s home at the lake last year. Suddenly everything made sense. Larry

had been using factory labor, tools, and supplies to have his lake house renovated on the weekends. Anu

had a distinct feeling that if she went up against Larry on this issue, she would come out the loser. She

decided to look for work elsewhere.

Requirements

1. Besides spotting irregularities, like the case above, what are some other ways that ABC cost data are

useful for manufacturing companies?

2. What are some of the other options that Anu might have considered?

SOLUTION

Requirement 1

An ABC system reflects the way products actually use a company’s resources (activities). Thus ABC

Requirement 2

Anu might have considered communicating with the company’s audit committee (if the company has