CHAPTER 18

Activity-Based Costing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Discuss the difference

between traditional costing

and activity-based costing.

1, 2, 3, 4, 5

1, 2

1

1, 2, 3, 4, 5,

10, 11

1A, 3A,

4A, 5A

*2. Apply activity-based

costing to a manufacturer.

6, 7, 9, 10,

11, 12

3, 4, 5, 6, 7

2

1, 3, 4, 5, 6,

7, 8, 9, 10,

11

1A, 2A, 3A,

4A, 5A

*3. Explain the benefits and

8, 13, 14, 15,

16, 17, 19

8, 9, 10, 11,

3

9, 10, 11, 12,

1A, 5A

*4. Apply activity-based

costing to service

9, 12

4

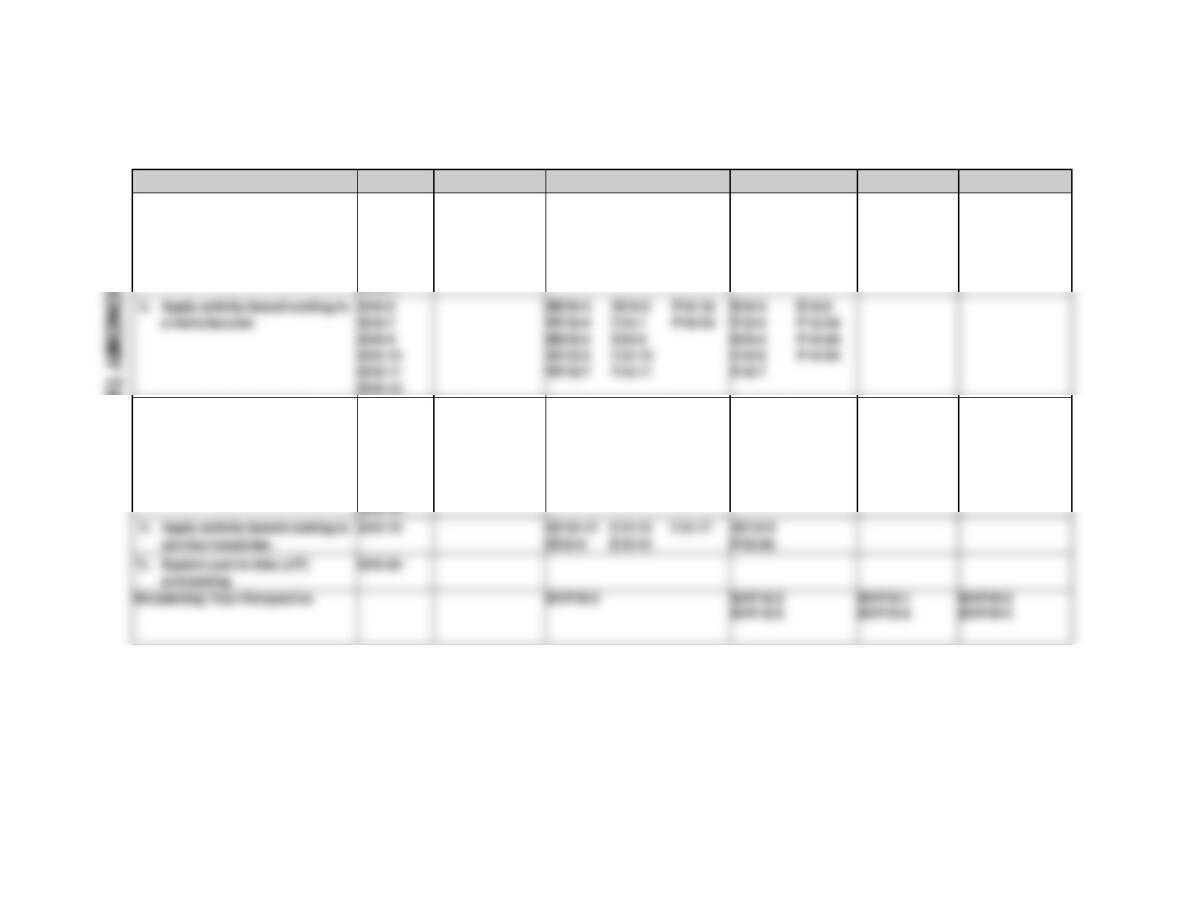

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Assign overhead using traditional costing and ABC;

compute unit costs; classify activities as value- or

non-value-added.

Moderate

35–45

Assign overhead to products using ABC and evaluate

Assign overhead costs using traditional costing and ABC;

5A

Assign overhead costs to services using traditional

Moderate

35–45

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End-of–Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Discuss the difference

between traditional costing and

activity-based costing.

Q18-1

Q18-2

Q18-3

Q18-4

Q18-5

DI18-1

BE18-1

BE18-2

E18-1

E18-2

E18–10

E18–11

P18–1A

E18-3

E18-4

E18-5

P18–3A

P18–4A

P18–5A

**3. Explain the benefits and

limitations of activity-based

costing.

Q18–18

DI18-4

E18–14

E18–17

Q18–20

Q18-8

Q18–13

Q18–14

A18–15

Q18–16

Q18–17

DI18-3

BE18–11

BE18–12

E18-9

E18–10

E18–11

P18–1A

BE18-8

BE18-9

BE18–10

E18–12

E18–13

E18–16

P18–5A

Q18–11

ANSWERS TO QUESTIONS

1. Direct labor is a valid basis for allocating overhead when: (a) direct labor constitutes a significant

Questions Chapter 18 (Continued)

19. Greater accuracy in cost allocation is achieved by recognizing the four levels of activity. Some

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 18-1

BRIEF EXERCISE 18-2

Under ABC, overhead costs are shifted from the high-volume products to

BRIEF EXERCISE 18-3

BRIEF EXERCISE 18-4

BRIEF EXERCISE 18-5

BRIEF EXERCISE 18-6

BRIEF EXERCISE 18-7

BRIEF EXERCISE 18-8

BRIEF EXERCISE 18-9

BRIEF EXERCISE 18–10

BRIEF EXERCISE 18–11

BRIEF EXERCISE 18–12

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 18-1

DO IT! 18-2

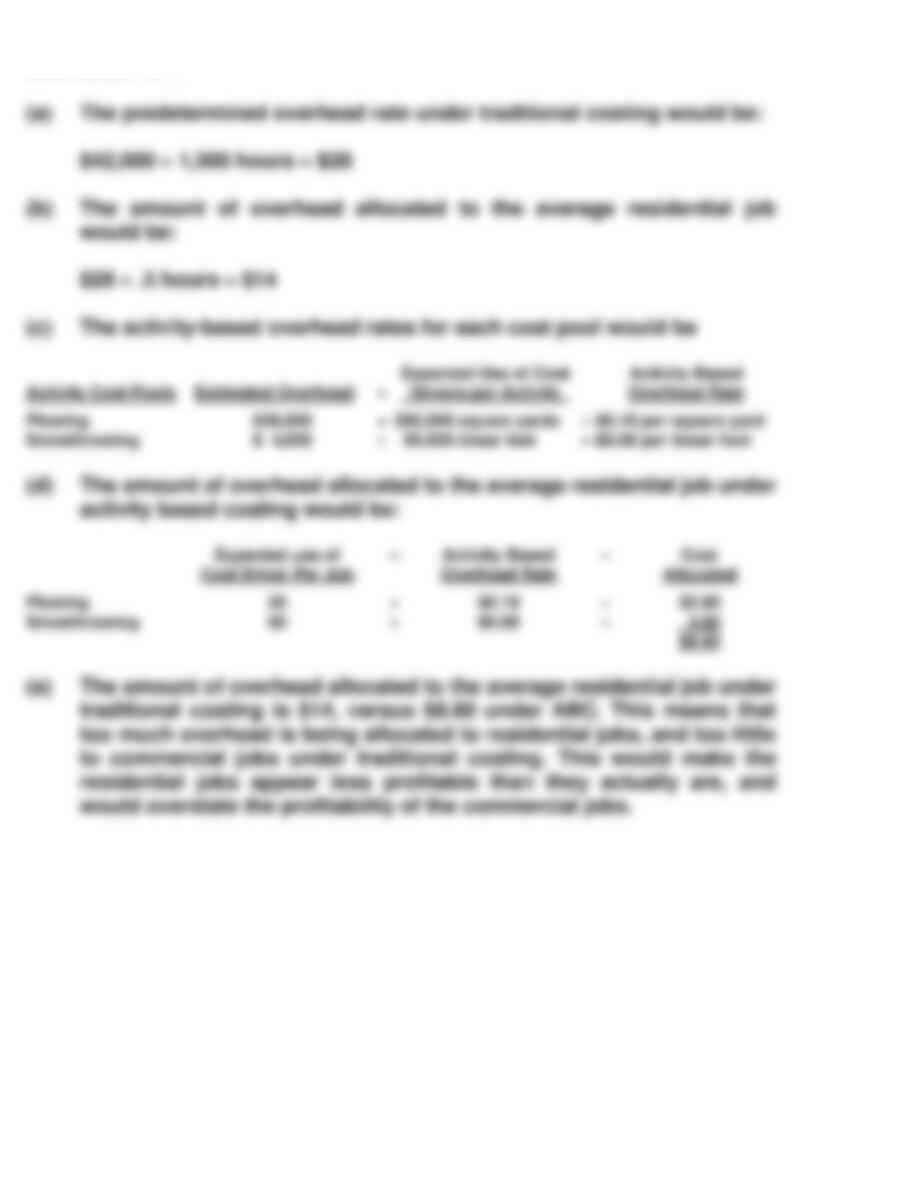

(a) Computations of activity-based overhead rates per cost driver:

(b) Assignment of each activity’s overhead cost to products using ABC:

DO IT! 18-2 (Continued)

DO IT! 18-4

SOLUTIONS TO EXERCISES

EXERCISE 18-1

EXERCISE 18-2

(a)

Traditional costing system

(b)

Activity-based costing system

EXERCISE 18-3

EXERCISE 18-4

EXERCISE 18-4 (Continued)

(c)

Truck Wheels

EXERCISE 18-5

EXERCISE 18-5 (Continued)

(b) Activity-based costing:

EXERCISE 18-6

Budgeted Costs

Activity Cost Pool

Cost Driver

EXERCISE 18-7

EXERCISE 18-8

EXERCISE 18-9

EXERCISE 18-9 (Continued)

(c) MEMO

To: President, Air United, Inc.

From: Student

Re: Benefits of activity-based costing (ABC)

EXERCISE 18-10

(a) (1) Traditional product costing system:

EXERCISE 18-11

EXERCISE 18-12

EXERCISE 18-13

EXERCISE 18–14

EXERCISE 18–14 (Continued)

EXERCISE 18–15

EXERCISE 18-16

EXERCISE 18-17

SOLUTIONS TO PROBLEMS

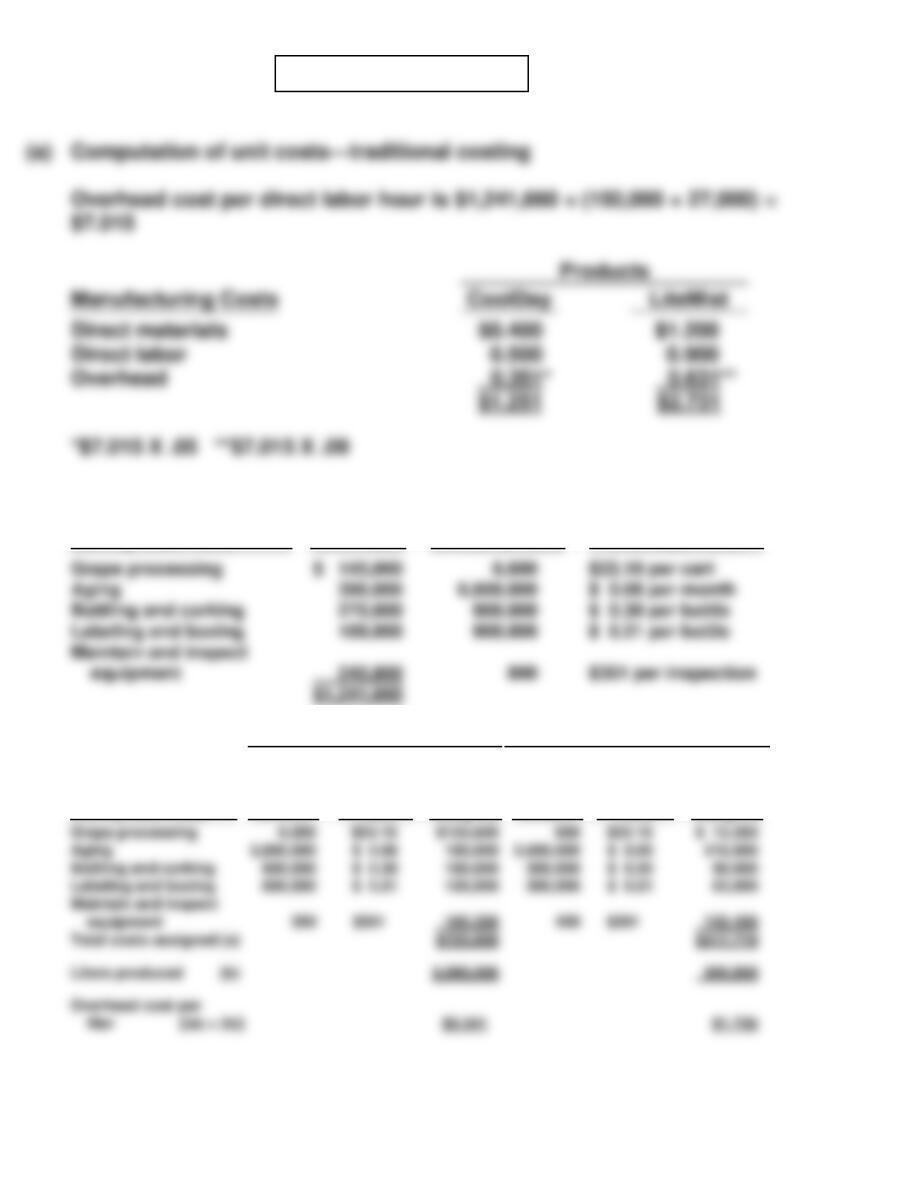

PROBLEM 18–1A

(a) Computation of unit costs—traditional costing.

(c)

PROBLEM 18-1A (Continued)

(d)

PROBLEM 18–2A

(b) The cost per unit and gross profit of each model under ABC costing

were:

PROBLEM 18–3A

(a) Predetermined overhead rate using machine hours:

(c) Manufacturing cost per stairway under activity-based costing:

PROBLEM 18-3A (Continued)

PROBLEM 18-4A

(b)

Activity Cost Pools

Estimated

Overhead

÷

Expected Use

of Cost Drivers

=

Activity-Based

Overhead Rates

equipment

(c)

CoolDay

LiteMist

Activity Cost Pools

Expected

Use of

Cost

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

Expected

Use of

Cost

Drivers

X

Activity-

Based

Overhead

Rates

=

Cost

Assigned

PROBLEM 18-4A (Continued)

(d)

Products

(e) To: Mr. Jack Eller

From: Student

Subject: Product costs using traditional approach versus ABC

The memorandum covers the following points:

PROBLEM 18–5A

(2) Assignment of overhead to audit and tax services:

PROBLEM 18-5A (Continued)

(c) Overhead is assigned to the two service lines as follows:

CD18 CURRENT DESIGNS

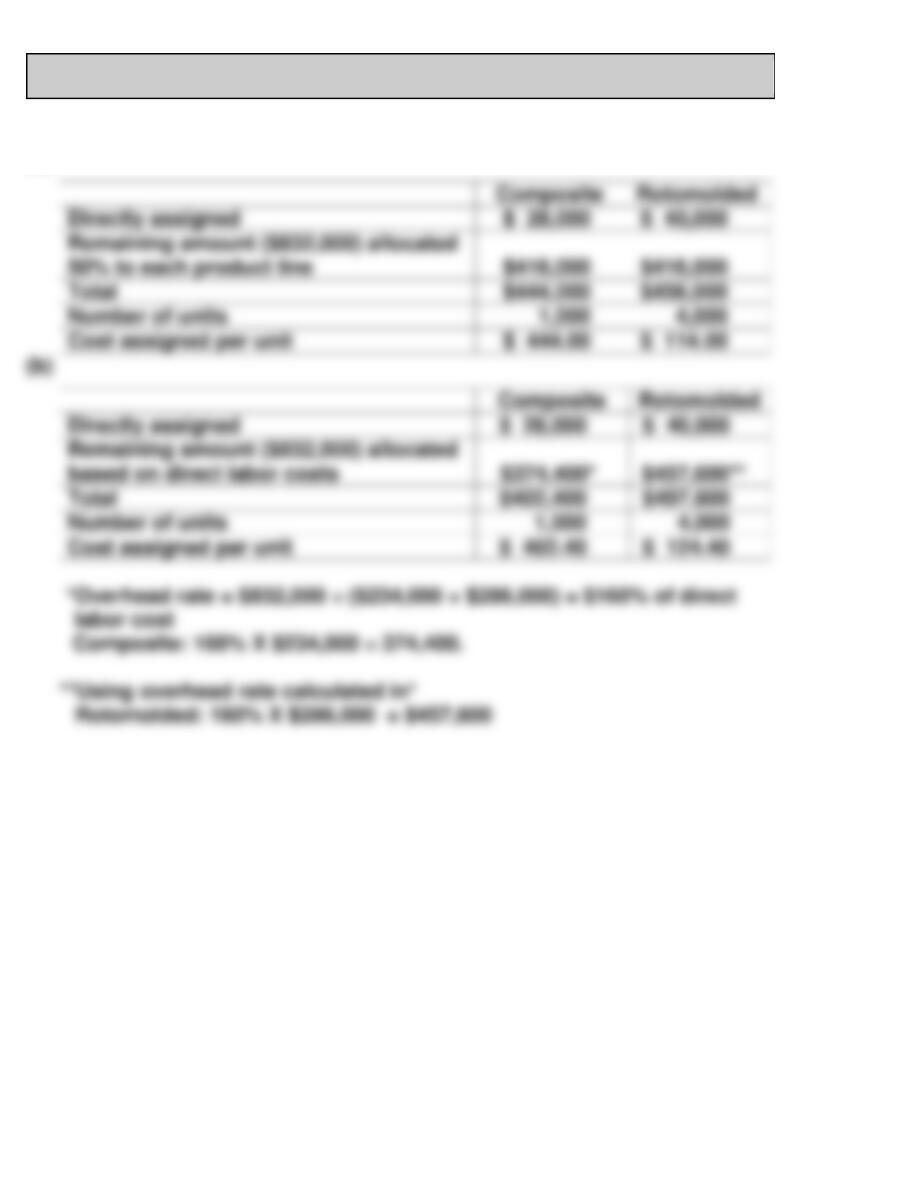

(a)

CD18 (Continued)

(c)

against the benefits that it provides.

BYP 18-1 DECISION-MAKING ACROSS THE ORGANIZATION

The following activities and cost drivers might be submitted:

(a) Activities

(b) Cost Drivers

BYP 18-2 MANAGERIAL ANALYSIS

(a) Computation of activity-based overhead rate:

(b) Charges to in-house manufacturing department:

In-House Manufacturing Department

(c) Charges to outside R & D contractor:

BYP 18-2 (Continued)

BYP 18-3 REAL-WORLD FOCUS

(a) Some of the benefits of ABC for the financial services industry include:

BYP 18-4 ETHICS CASE

(a) The stakeholders (parties affected by Curtis’s and Ed’s actions) in this

case are:

BYP 18-5 ALL ABOUT YOU

(a) The three main tools for time management for students are:

BYP 18-6 CONSIDERING YOUR COSTS AND BENEFITS