Chapter 18

Process Costing

Review Questions

1. What types of companies use job order costing systems?

Companies that manufacture batches of unique products or provide specialized services use job

2. What types of companies use process costing systems?

3. What are the primary differences between job order costing systems and process costing systems?

The primary differences between job order costing and process costing are how and when costs are

4. List ways in which job order costing systems are similar to process costing systems.

Ways in which job order costing systems are similar to process costing systems are that both:

5. Describe the flow of costs through a process costing system.

Each process is a separate department and each department has its own Work-in-Process Inventory

6. What are equivalent units of production?

Equivalent units of production are used to measure the amount of materials added to or work done

on partially completed units and are expressed in terms of fully completed units.

7. Why is the calculation of equivalent units of production needed in a process costing system?

The calculation of equivalents units of production is needed in a process costing system because the

8. What are conversion costs? Why do some companies using process costing systems use conversion

costs?

Conversion costs are the combination of manufacturing overhead and direct labor; this represents the

9. What is a production cost report?

A production cost report is completed for each department for each month. It shows the calculations

10. What are the four steps in preparing a production cost report?

The four steps in preparing a production cost report are: 1) summarize the flow of physical units, 2)

11. Explain the terms to account for and accounted for.

12. If a company began the month with 50 units in process, started another 600 units during the month,

and ended the month with 75 units in process, how many units were completed?

13. Most companies using process costing systems have to calculate more than one EUP. Why? How

many do they have to calculate?

EUP are calculated separately because the direct materials are usually added at the beginning of the

14. How is the cost per equivalent unit of production calculated?

The cost per equivalent unit of production is calculation for each input. To calculate the Cost per

15. What is the purpose of the Costs Accounted For section of the production cost report?

The purpose of the Costs Accounted For section of the production cost report is to assign costs to the

16. What are transferred in costs? When do they occur?

Transferred in costs are the costs that were incurred in a previous process and brought into a later

17. What is the weighted-average method for process costing systems?

18. Explain the additional journal entries required by process costing systems that are not needed in job

order costing systems.

19. Department 1 is transferring units that cost $40,000 to Department 2. Give the journal entry.

Date

Accounts and Explanation

Debit

Credit

Work-in–Process Inventory―Department 2

40,000

20. Department 4 has completed production on units that have a total cost of $15,000. The units are

ready for sale. Give the journal entry.

Date

Accounts and Explanation

Debit

Credit

Finished Goods Inventory

15,000

21. Describe ways the production cost report can be used by management.

The production cost report can be used by managers to make decisions for their company. This

22A. Describe how the FIFO method is different from the weighted-average method.

The FIFO method accounts for the costs from the beginning balance in Work–in-Process Inventory

23A. Describe the three groups of units that must be accounted for when using the FIFO method.

The three groups of units to be accounted for when using the FIFO method are units in the

24A. When might it be beneficial for a company to use the FIFO method? When is the weighted-average

method more practical?

If a business operates in an industry that experiences significant cost changes, it would be to their

Short Exercises

For all Short Exercises, assume the weighted-average method is to be used unless you are told

otherwise.

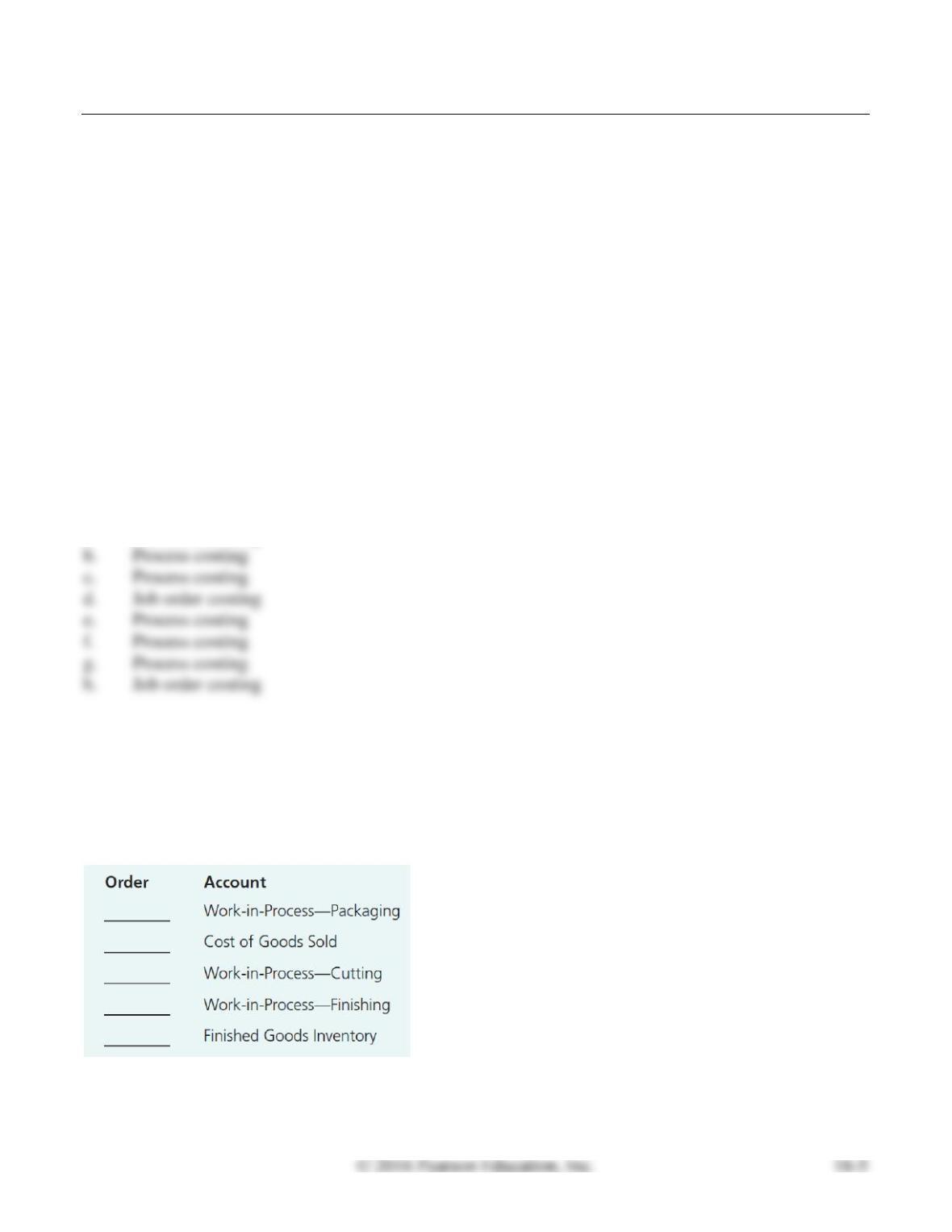

S18-1 Comparing job order costing versus process costing

Learning Objective 1

Identify each costing system characteristic as job order costing or process costing.

a. One Work-in-Process Inventory account

b. Production cost reports

c. Cost accumulated by process

d. Job cost sheets

e. Manufactures homogenous products through a series of uniform steps

f. Multiple Work-in-Process Inventory accounts

g. Costs transferred at end of period

h. Manufactures batches of unique products or provides specialized services

SOLUTION

a.

Job order costing

b.

Process costing

c.

Process costing

d.

Job order costing

e.

Process costing

g.

Process costing

h.

Job order costing

S18-2 Tracking the flow of costs

Learning Objective 1

The Jimenez Toy Company makes wooden toys. Arrange the company’s accounts in the order the

production costs are most likely to flow, using 1 for the first account, 2 for the second, and so on.

SOLUTION

3.

Work-in-Process—Packaging

OR

1.

Work-in–Process―Cutting

5.

Cost of Goods Sold

2.

Work-in–Process―Finishing

1.

Work-in–Process―Cutting

3.

Work-in-Process—Packaging

2.

Work-in–Process―Finishing

4.

Finished Goods Inventory

4.

Finished Goods Inventory

5.

Cost of Goods Sold

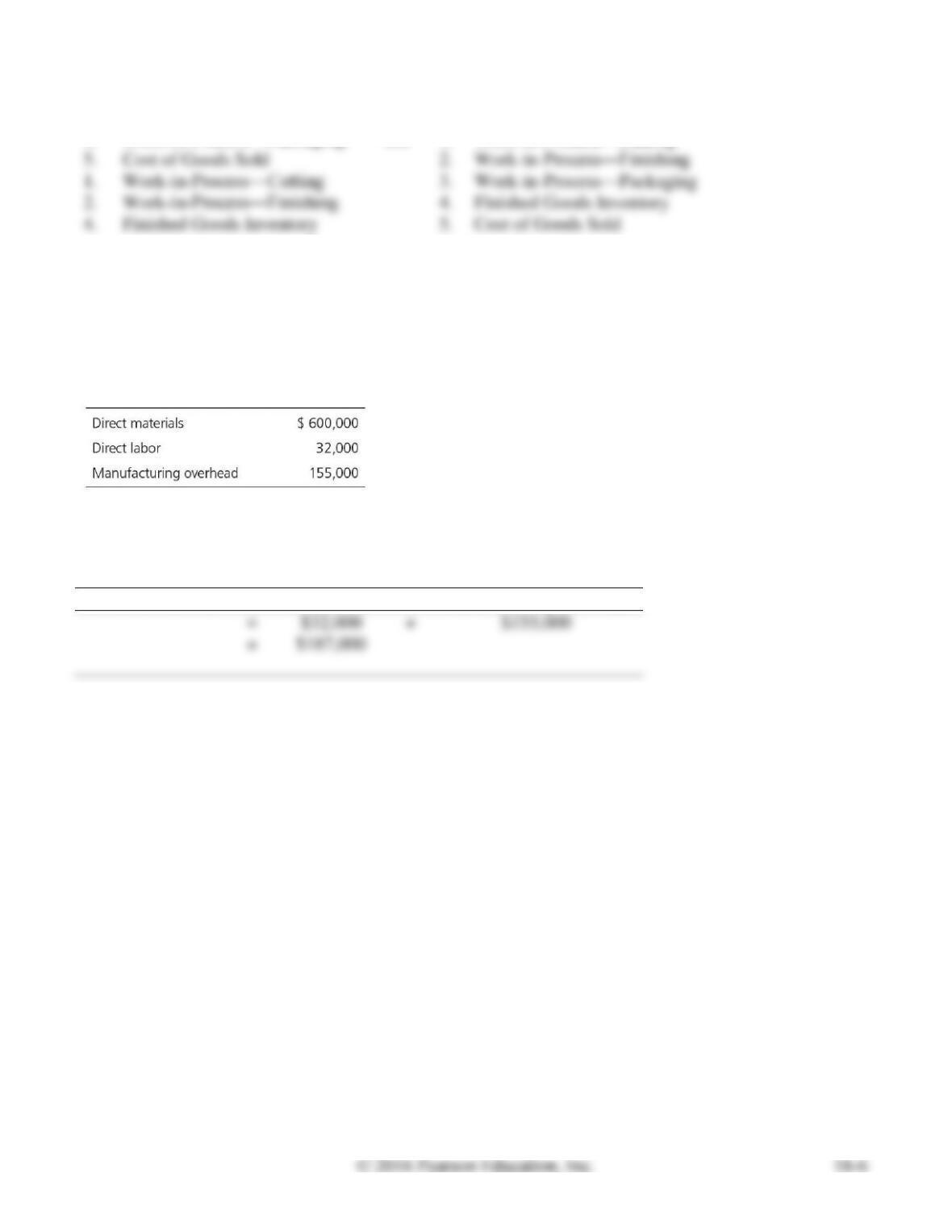

S18-3 Calculating conversion costs

Learning Objective 2

Hamlin Orange manufactures orange juice. Last month’s total manufacturing costs for the Jacksonville

operation included:

What was the conversion cost for Hamlin Orange’s Jacksonville operation last month?

SOLUTION

Conversion Costs

=

Direct Labor

+

Manufacturing Overhead

=

+

S18-4 Calculating EUP

Learning Objective 2

Monga manufactures cell phones. The conversion costs to produce cell phones for November are added

evenly throughout the process in the Assembly Department. For each of the following separate

assumptions, calculate the equivalent units of production for conversion costs in the ending Work-in–

Process Inventory for the Assembly Department:

1. 7,000 cell phones were 85% complete

2. 24,000 cell phones were 15% complete

SOLUTION

1.

Equivalent Units

=

Cell phones

×

Completion Percentage

=

=

Equivalent Units

=

Cell phones

×

Completion Percentage

=

=

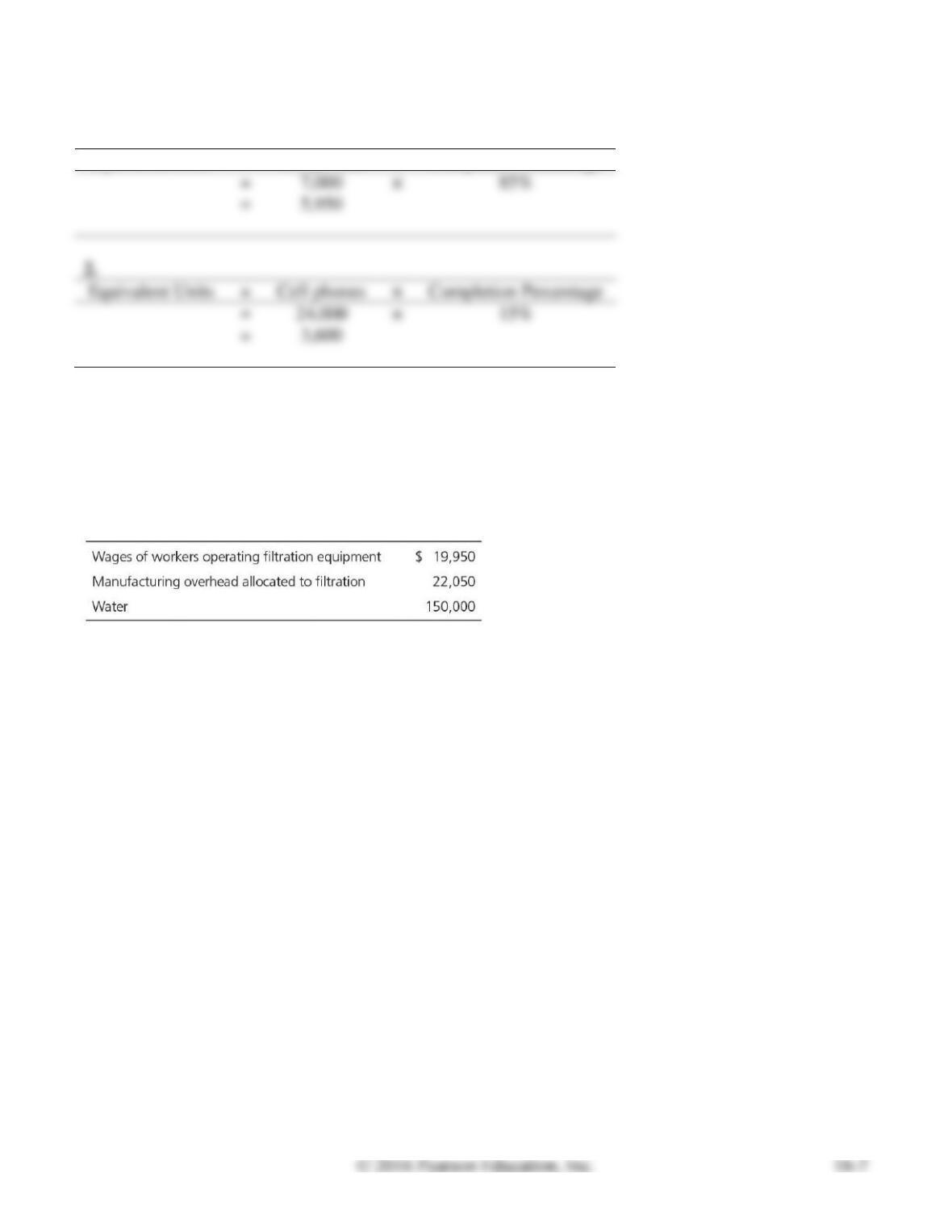

S18-5 Calculating conversion costs and unit cost

Learning Objective 2

Russia Spring produces premium bottled water. Russia Spring purchases artesian water, stores the water

in large tanks, and then runs the water through two processes: filtration and bottling.

During February, the filtration process incurred the following costs in processing 150,000 liters:

Russia Spring had no beginning Work-in-Process Inventory in the Filtration Department in February.

Requirements

1. Compute the February conversion costs in the Filtration Department.

2. The Filtration Department completely processed 150,000 liters in February. What was the filtration

cost per liter?

SOLUTION

Requirement 1

Conversion Costs

=

Direct Labor

+

Manufacturing Overhead

=

$19,950

+

$22,050

=

$42,000

Total Costs

=

+

Conversion Costs

=

+

=

Cost per liter

=

Total Costs

=

150,000

=

Note: Short Exercise S18-5 must be completed before attempting Short Exercise S18-6.

S18-6 Computing EUP

Learning Objective 2

Refer to Short Exercise S18-5. At Russia Spring, water is added at the beginning of the filtration

process. Conversion costs are added evenly throughout the process. Now assume that in February,

80,000 liters were completed and transferred out of the Filtration Department into the Bottling

Department. The 70,000 liters remaining in Filtration’s ending Work–in-Process Inventory were 80% of

the way through the filtration process. Recall that Russia Spring has no beginning inventories.

Compute the equivalent units of production for direct materials and conversion costs for the Filtration

Department.

SOLUTION

150,000 EUP for direct materials

80,000 EUP for conversion costs

56,000 EUP for conversion costs

80,000 units × 100%

=

80,000 EUP for direct materials

S18-7 Computing costs transferred

Learning Objective 3

The Finishing Department of Carter and Nelson, Inc., the last department in the manufacturing process,

incurred production costs of $310,000 during the month of June. If the June 1 balance in Work-in–

Process—Finishing is $0 and the June 30 balance is $70,000, what amount was transferred to Finished

Goods Inventory?

SOLUTION

Work-in-Process Inventory, June 1

$ 0

S18-8 Computing EUP

Learning Objectives 2, 3

The Mixing Department of Fresh Foods had 50,000 units to account for in October. Of the 50,000 units,

40,000 units were completed and transferred to the next department, and 10,000 units were 20%

complete. All of the materials are added at the beginning of the process. Conversion costs are added

evenly throughout the mixing process.

Compute the total equivalent units of production for direct materials and conversion costs for

October.

SOLUTION

Completed units:

40,000 units × 100%

=

40,000 EUP for direct materials

In process units:

10,000 units × 100%

=

10,000 EUP for direct materials

Total EUP for direct materials:

=

50,000 EUP for direct materials

Completed units:

40,000 units × 100%

=

In process units:

10,000 units × 20%

=

Total EUP for conversion costs:

=

Note: Short Exercise S18-8 must be completed before attempting Short Exercise S18-9.

S18-9 Computing the cost per EUP

Learning Objective 3

SOLUTION

Cost per EUP for direct materials

=

Total direct materials costs

Equivalent units of production for direct materials

=

=

Cost per EUP for conversion costs

=

=

Note: Short Exercises S18-8 and S18-9 must be completed before attempting Short Exercise S18-10.

S18-10 Assigning costs

Learning Objective 3

Refer to Short Exercises S18-8 and S18-9. Use Fresh Foods’s costs per equivalent unit of production for

direct materials and conversion costs that you calculated in Short Exercise S18-9.

Calculate the cost of the 40,000 units completed and transferred out and the 10,000 units, 20%

complete, in the ending Work-in-Process Inventory.

SOLUTION

Direct Materials:

Completed

40,000 EUP

×

$ 0.96 per EUP

=

$ 38,400

In Process

10,000 EUP

×

$ 0.96 per EUP

=

9,600

Total

$ 48,000

Conversion Costs:

Completed

40,000 EUP

×

$ 0.70 per EUP

=

$ 28,000

In Process

×

$ 0.70 per EUP

=

1,400

Total

$ 29,400

=

+

=

=

Direct Materials

=

=

Note: Short Exercises S18-8, S18-9, and S18-10 must be completed before attempting Short Exercise

S18-11.

S18-11 Preparing journal entry

Learning Objective 4

Refer to Short Exercise S18-10. Prepare the journal entry to record the transfer of costs from the Mixing

Department to the Packaging Department.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

S18-12 Making decisions

Learning Objective 5

Miller Company sells several products. Sales reports show that the sales volume of its most popular

product has increased the past three quarters while overall profits have decreased. How might

production cost reports assist management in making decisions about this product?

SOLUTION

The production report will help managers see how much the product is costing to make. They can

S18A-13 Calculating conversion costs and unit cost—FIFO method

Learning Objective 6

Appendix 18A

Spring Rain produces premium bottled water. Spring Rain purchases artesian water, stores the water in

large tanks, and then runs the water through two processes: filtration and bottling.

During February, the filtration process incurred the following costs in processing 100,000 liters:

Spring Rain had no beginning Work-in-Process Inventory in the Filtration Department in February.

Requirements

1. Use the FIFO method to compute the February conversion costs in the Filtration Department.

2. The Filtration Department completely processed 100,000 liters in February. Use the FIFO method to

determine the filtration cost per liter.

SOLUTION

Requirement 1

Conversion Costs

=

Direct Labor

+

Manufacturing Overhead

=

+

=

Beginning WIP units:

=

Started and completed units:

=

In process units:

=

Total EUP for direct materials:

=

Beginning WIP units:

=

Started and completed units:

=

In process units:

=

Total EUP for conversion costs:

=

Cost per EUP for direct materials

=

Total direct materials costs

Equivalent units of production for direct materials

=

$170,000

100,000 EUP

=

$1.70 per EUP

Cost per EUP for conversion costs

=

=

Direct Materials

=

+

=

Note: Short Exercise S18A-13 must be completed before attempting Short Exercise S18A-14.

S18A-14 Computing EUP—FIFO Method

Learning Objective 6

Appendix 18A

Refer to Short Exercise S18A-13. At Spring Rain, water is added at the beginning of the filtration

process. Conversion costs are added evenly throughout the process. Now assume that in February,

80,000 liters were completed and transferred out of the Filtration Department into the Bottling

Department. The 20,000 liters remaining in Filtration’s ending Work–in-Process Inventory were 70% of

the way through the filtration process. Recall that Spring Rain has no beginning inventories.

Compute the equivalent units of production for direct materials and conversion costs for the Filtration

Department using the FIFO method.

SOLUTION

Beginning WIP units:

0 units

=

0 EUP for direct materials

Started and completed units:

=

In process units:

=

Total EUP for direct materials:

=

Beginning WIP units:

0 units

=

Started and completed units:

=

In process units:

=

Total EUP for conversion costs:

=

Exercises

For all Exercises, assume the weighted-average method is to be used unless you are told otherwise.

E18-15 Comparing job order costing versus process costing

Learning Objective 1

For each of the following products or services, indicate if the cost would most likely be determined

using a job order costing system or a process costing system.

a. Soft drinks

b. Automobile repairs

c. Customized furniture

d. Aluminum foil

e. Lawn chairs

f. Chocolate candy bars

g. Hospital surgery

h. Pencils

SOLUTION

a.

Process costing

Job order costing

c.

Job order costing

Process costing

e.

Process costing

Process costing

Job order costing

Process costing

E18-16 Understanding terminology

Learning Objectives 1, 2, 3

Match the following terms to their definitions.

SOLUTION

1.

d

2.

3.

a

4.

b

5.

c

6.

e

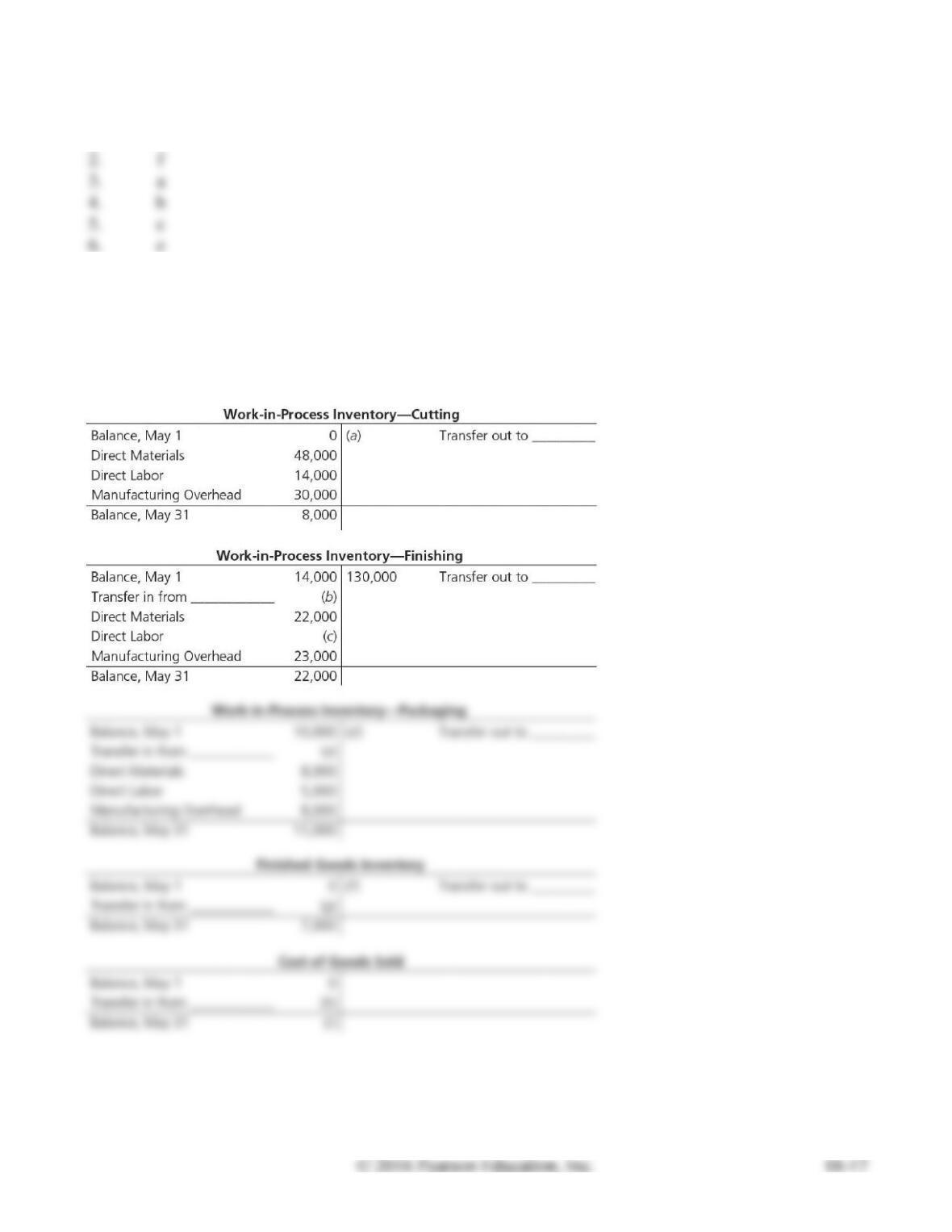

E18-17 Tracking the flow of costs

Learning Objectives 1, 4

c. $9,000

Complete the missing amounts and labels in the T-accounts.

SOLUTION

Work-in-Process—Cutting

Balance, May 1

0

(a) 84,000

Transfer out to WIP—Finishing

Direct Materials

48,000

Direct Labor

14,000

Manufacturing Overhead

30,000

Balance, May 31

8,000

Balance, May 1

14,000

130,000

Transfer out to WIP—Packaging

Transfer in from WIP—Cutting

Direct Materials

22,000

Direct Labor

Manufacturing Overhead

23,000

Balance, May 31

22,000

Work-in-Process—Packaging

Balance, May 1

10,000

(d) 150,000

Transfer out to FG Inventory

Transfer in from WIP—Finishing

(e) 130,000

Direct Materials

8,000

Direct Labor

5,000

Manufacturing Overhead

8,000

Balance, May 31

11000

Balance, May 1

0

Transfer out to COGS

Transfer in from WIP—Packaging

Balance, May 31

7,000

Balance, May 1

0

Transfer in from FG Inventory

Balance, May 31

E18-18 Computing EUP

Learning Objective 2

3. EUP for DM 1,900

Collins Company has the following data for the Assembly Department for August:

Conversion costs are added evenly throughout the process. Compute the equivalent units of production

for direct materials and conversion costs for each independent scenario:

1. Units in process at the beginning of August are 40% complete; units in process at the end of August

are 30% complete; materials are added at the beginning of the process.

2. Units in process at the beginning of August are 60% complete; units in process at the end of August

are 70% complete; materials are added at the beginning of the process.

3. Units in process at the beginning of August are 40% complete; units in process at the end of August

are 30% complete; materials are added at the end of the process.

4. Units in process at the beginning of August are 60% complete; units in process at the end of August

are 70% complete; materials are added at the halfway point.

SOLUTION

Requirement 1

Completed units:

1,900 units × 100%

=

1,900 EUP for direct materials

In process units:

=

Total EUP for direct materials:

=

2,100 EUP for direct materials

Completed units:

1,900 units × 100%

=

In process units:

=

Total EUP for conversion costs:

=

Completed units:

1,900 units × 100%

=

1,900 EUP for direct materials

In process units:

=

Total EUP for direct materials:

=

2,100 EUP for direct materials

Completed units:

1,900 units × 100%

=

In process units:

=

Total EUP for conversion costs:

=

Requirement 3

Completed units:

1,900 units × 100%

=

1,900 EUP for direct materials

In process units:

200 units × 0%

=

0 EUP for direct materials

Total EUP for direct materials:

=

1,900 EUP for direct materials

Completed units:

1,900 units × 100%

=

In process units:

200 units × 30%

=

Total EUP for conversion costs:

=

Requirement 4

Completed units:

1,900 units × 100%

=

1,900 EUP for direct materials

In process units:

200 units × 100%

=

Total EUP for direct materials:

=

2,100 EUP for direct materials

Completed units:

1,900 units × 100%

=

In process units:

200 units × 70%

=

Total EUP for conversion costs:

=

E18-19 Computing EUP, assigning cost, no beginning WIP or cost transferred in

Learning Objectives 2, 3

1. Total EUP for CC 7,050

Ceramic Painting prepares and packages paint products. Ceramic Painting has two departments:

Blending and Packaging. Direct materials are added at the beginning of the blending process (dyes) and

at the end of the packaging process (cans). Conversion costs are added evenly throughout each process.

Data from the month of May for the Blending Department are as follows: