Requirements

1. Compute the Blending Department’s equivalent units of production for direct ma– terials and for

conversion costs.

2. Compute the total costs of the units (gallons)

a. completed and transferred out to the Packaging Department.

b. in the Blending Department ending Work-in-Process Inventory.

SOLUTION

Requirement 1

Completed units:

6,000 units × 100%

=

6,000 EUP for direct materials

In process units:

3,500 units × 100%

=

3,500 EUP for direct materials

Total EUP for direct materials:

=

9,500 EUP for direct materials

Completed units:

6,000 units × 100%

=

In process units:

3,500 units × 30%

=

Total EUP for conversion costs:

=

Requirement 2

Cost per EUP for direct materials

=

Total direct materials costs

Equivalent units of production for direct materials

=

=

Direct Materials:

Completed

6,000 EUP

×

$ 0.60 per EUP

=

$ 3,600

In Process

3,500 EUP

×

$ 0.60 per EUP

=

2,100

Total

$ 5,700

Conversion Costs:

Completed

6,000 EUP

×

$ 0.58 per EUP

=

$ 3,480

In Process

1,050 EUP

×

$ 0.58 per EUP

=

Total

$ 4,089

E18–19, cont.

Requirement 2, cont.

a.

Completed and Transferred Out

=

Direct Materials

+

Conversion Costs

=

$3,600

+

$3,480

=

$7,080

=

+

Conversion Costs

=

$2,100

+

=

$2,709

Note: Exercise E18-19 must be completed before attempting Exercise E18-20.

E18-20 Preparing journal entries, posting to T-accounts, making decisions

Learning Objectives 4, 5

2. WIP Balance $2,709

Refer to your answers from Exercise E18-19.

Requirements

1. Prepare the journal entries to record the assignment of direct materials and direct labor and the

allocation of manufacturing overhead to the Blending Department. Also, prepare the journal entry to

record the costs of the gallons completed and transferred out to the Packaging Department.

2. Post the journal entries to the Work-in-Process Inventory—Blending T-account. What is the ending

balance?

3. What is the average cost per gallon transferred out of the Blending Department into the Packaging

Department? Why would the company managers want to know this cost?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

May 31

Work-in–Process Inventory―Blending

5,700

Raw Materials Inventory

5,700

Direct materials assigned to WIP.

Work-in–Process Inventory―Blending

2,085

Wages Payable

2,085

Direct labor assigned to WIP.

Work-in–Process Inventory―Blending

2,004

Manufacturing Overhead

2,004

Overhead allocated to WIP.

Work-in-Process Inventory―Packaging

7,080

7,080

Transfer costs assigned to units transferred.

Requirement 2

Work-in–Process―Blending

Balance, May 1

0

7,080

Transferred to Packaging

Direct Labor

Manufacturing Overhead

Balance, May 31

Requirement 3

Cost per gallon

=

Total Costs

/

Units Completed and Transferred Out

=

$7,080

/

6,000 gallons

=

$1.18 per gallon

E18-21 Computing EUP, assigning costs, no beginning WIP or cost transferred in

Learning Objectives 2, 3

1. EUP for CC 7,200

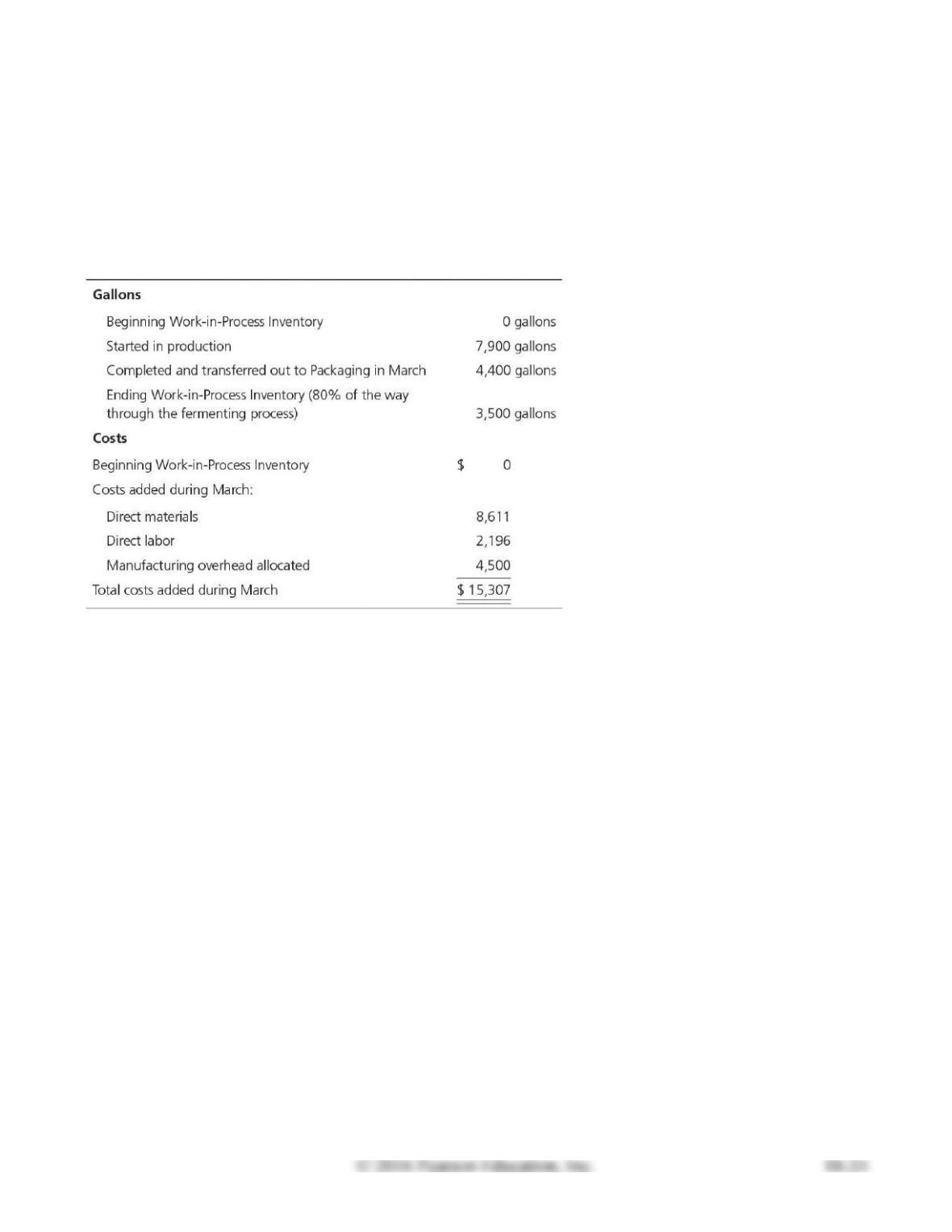

Anderson Winery in Pleasant Valley, New York, has two departments: Fermenting and Packaging.

Direct materials are added at the beginning of the fermenting process (grapes) and at the end of the

packaging process (bottles). Conversion costs are added evenly throughout each process. Data from the

month of March for the Fermenting Department are as follows:

Requirements

1. Compute the Fermenting Department’s equivalent units of production for direct materials and for

conversion costs.

2. Compute the total costs of the units (gallons)

a. completed and transferred out to the Packaging Department.

b. in the Fermenting Department ending Work-in-Process Inventory.

SOLUTION

Requirement 1

Completed units:

4,400 units × 100%

=

4,400 EUP for direct materials

In process units:

3,500 units × 100%

=

3,500 EUP for direct materials

Total EUP for direct materials:

=

7,900 EUP for direct materials

Completed units:

4,400 units × 100%

=

In process units:

3,500 units × 80%

=

Total EUP for conversion costs:

=

Requirement 2

Cost per EUP for direct materials

=

Total direct materials costs

Equivalent units of production for direct materials

=

=

E18-21, cont.

Direct Materials:

Completed

4,400 EUP

×

$ 1.09 per EUP

=

$ 4,796

In Process

3,500 EUP

×

$1.09 per EUP

=

3,815

Total

$ 8,611

Conversion Costs:

Completed

4,400 EUP

×

$ 0.93 per EUP

=

$ 4,092

In Process

2,800 EUP

×

$ 0.93 per EUP

=

2,604

Total

$ 6,696

Completed and Transferred Out

=

Direct Materials

+

Conversion Costs

=

+

=

Note: Exercise E18-21 must be completed before attempting Exercise E18-22.

E18-22 Preparing journal entries and posting to T-accounts

Learning Objectives 4, 5

2. WIP Balance $6,419

Refer to the data and your answers from Exercise E18-21.

Requirements

1. Prepare the journal entries to record the assignment of direct materials and direct labor and the

allocation of manufacturing overhead to the Fermenting Department. Also prepare the journal entry

to record the cost of the gallons completed and transferred out to the Packaging Department.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Mar. 31

Work-in–Process Inventory―Fermenting

8,611

Raw Material Inventory

8,611

Direct materials assigned to WIP.

Work-in–Process Inventory―Fermenting

2,196

Wages Payable

2,196

Direct labor assigned to WIP.

Work-in–Process Inventory―Fermenting

4,500

Manufacturing Overhead

4,500

Overhead allocated to WIP.

Work-in-Process Inventory―Packaging

8,888

8,888

Transfer costs assigned to units transferred.

Requirement 2

Work-in–Process―Fermenting

Balance, Mar. 1

0

8,888

Transferred to Packaging

Direct Labor

Manufacturing Overhead

Balance, Mar. 31

Requirement 3

Cost per gallon

=

Total Costs

/

Units Completed and Transferred Out

=

$8,888

/

4,400 gallons

=

$2.02 per gallon

E18-22, cont.

Requirement 3, cont.

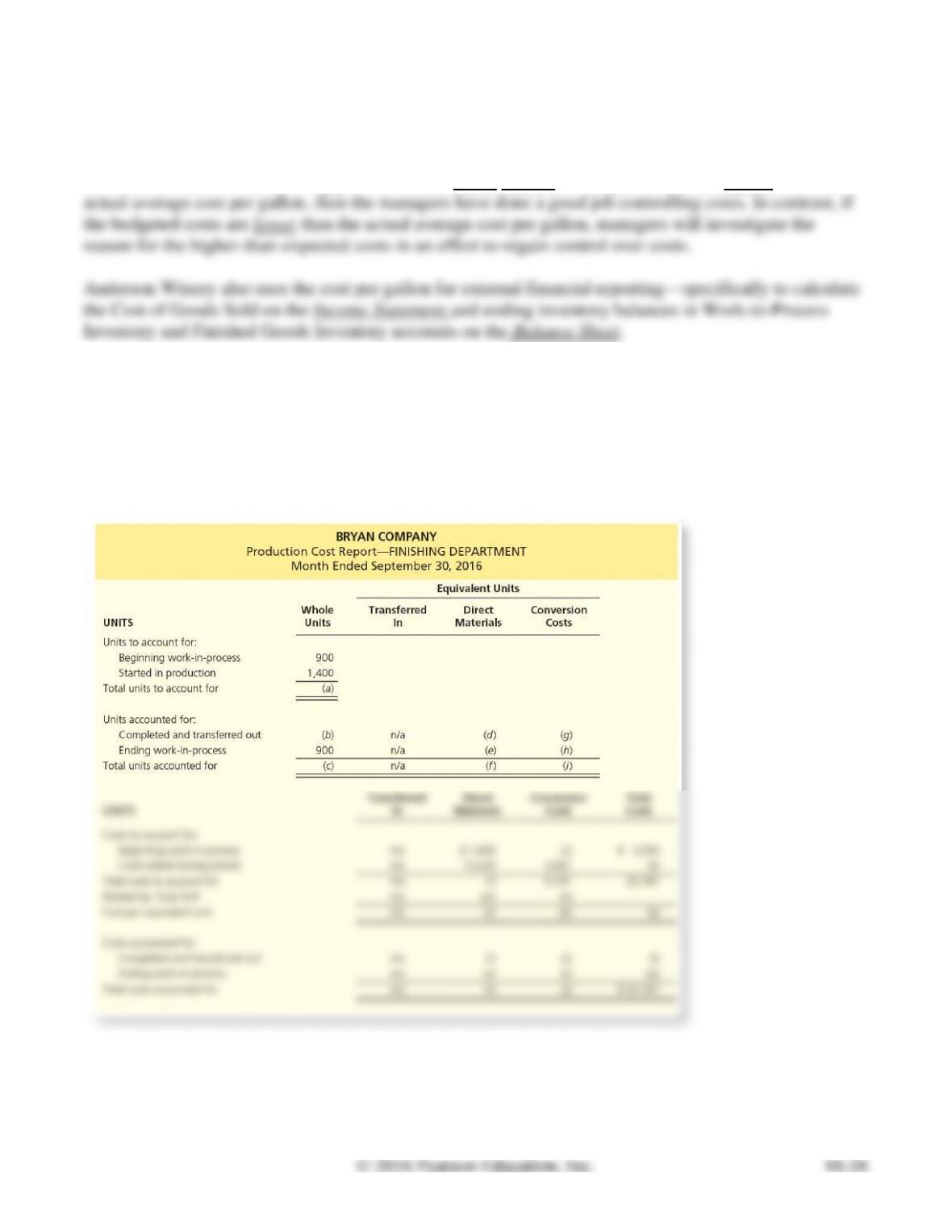

The managers would compare the average cost per gallon against their budgeted costs to determine

whether the costs of the blending process remain under control. If budgeted costs are higher than the

E18-23 Preparing production cost report, missing amounts

Learning Objectives 2, 3

(p) $2.65

Complete the missing amounts in the following production report. Materials are added at the beginning

of the process; conversion costs are incurred evenly; the ending inventory is 60% complete.

SOLUTION

BRYAN COMPANY

Production Cost Report―FINISHING DEPARTMENT

Month Ended September 30, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work-in-process

Started in production

Total units to account for

(a) 2,300

Units accounted for:

Completed and transferred out

(b) 1,400

n/a

Ending work-in-process

n/a

(h) 540

Total units accounted for

n/a

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

n/a

$ 1,600

(j) 1,450

$ 3,050

Costs added during period

n/a

15,420

3,691

(k) 19,111

Total costs to account for

n/a

(l) 17,020

5,141

22,161

Divided by: Total EUP

n/a

(m) 2,300

(n) 1,940

Cost per equivalent unit

n/a

(o) $7.40

(p) $2.65

(q) $10.05

Costs accounted for:

Completed and transferred out

n/a

Ending work-in-process

n/a

(u) 6,660

Total costs accounted for

n/a

E18-23, cont.

a.

2,300 units

900 + 1,400

b.

1,400

2,300 – 900

c.

2,300

Equal to total units to account for (a) 2,300

d.

1,400

1,400 × 100%

e.

900

900 × 100%

f.

2,300

1,400 + 900

g.

1,400

1,400 × 100%

h.

540

900 × 60%

i.

1,940

1,400 + 540

k.

$22,161 – $3,050 or $15,420 + $3,691

l.

$1,600 + $15,420

m.

2,300 units

Transferred from above total units accounted for (f)

n.

1,940

Transferred from above total units accounted for (i)

o.

$17,020 / 2,300 units

p.

$5,141 / 1,940 units

q.

$7.40 + $2.65

r.

(d) 1,400 units × (o) $7.40

(g) 1,400 units × (p) $2.65

t.

$10,360 + $3,710

u.

(e) 900 units × (o) $7.40

v.

(h) 540 units × (p) $2.65

$6,660 + $1,431

x.

$10,360 + $6,660

y.

$ 3,710 + $1,431

E18-24 Computing EUP, first and second departments

Learning Objectives 2, 3

2. EUP for DM 85,000

Selected production and cost data of Sharon’s Color Co. follow for May 2016:

On May 31, the Mixing Department ending Work-in-Process Inventory was 65% complete for

materials and 25% complete for conversion costs. The Heating Department ending Work-in-Process

Inventory was 75% complete for materials and 60% complete for conversion costs.

Requirements

1. Compute the equivalent units of production for direct materials and for conversion costs for the

Mixing Department.

2. Compute the equivalent units of production for transferred in costs, direct materials, and conversion

costs for the Heating Department.

SOLUTION

Requirement 1

Mixing Department

Completed units:

80,000 units × 100%

=

80,000 EUP for direct materials

In process units:

15,000 units × 65%

=

Total EUP for direct materials:

=

89,750 EUP for direct materials

In process units:

15,000 units × 25%

=

Total EUP for conversion costs:

=

Requirement 2

Heating Department

Completed units:

76,000 units × 100%

=

76,000 EUP for transferred in

In process units:

12,000 units × 100%

=

12,000 EUP for transferred in

Total EUP for transferred in

=

88,000 EUP for transferred in

Completed units:

76,000 units × 100%

=

In process units:

12,000 units × 75%

=

Total EUP for direct materials:

=

Completed units:

76,000 units × 100%

=

In process units:

12,000 units × 60%

=

Total EUP for conversion costs:

=

E18-25 Preparing production cost report, journalizing, second department

Learning Objectives 2, 3, 4

3. WIP Balance $20,700

(Requirement 1 only)

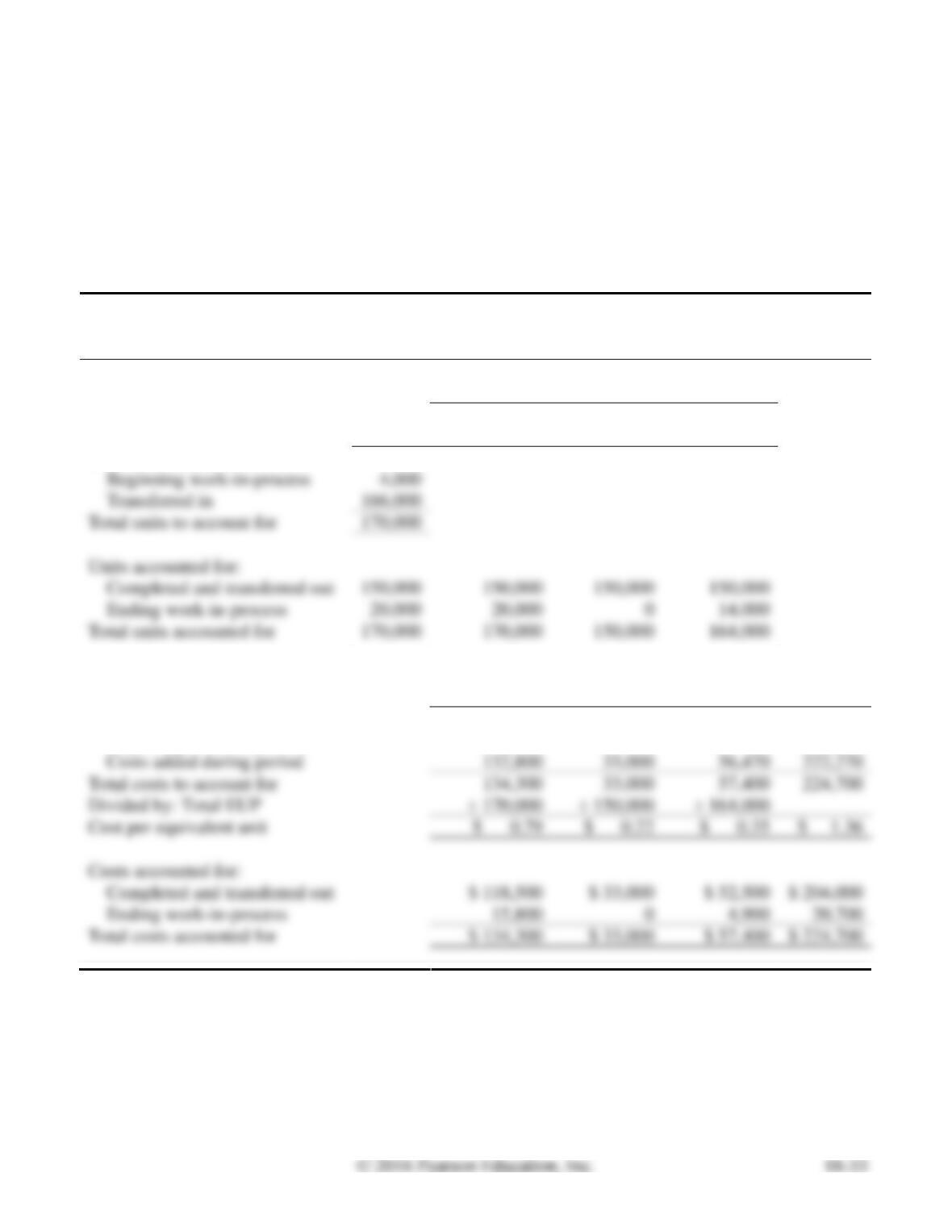

Pure Spring Company produces premium bottled water. In the second department, the Bottling

Requirements

1. Prepare a production cost report for the Bottling Department for the month of February.

2. Prepare the journal entry to record the cost of units completed and transferred out.

3. Post all transactions to the Work-in-Process Inventory—Bottling T-account. What is the ending

balance?

SOLUTION

Requirement 1

PURE SPRING COMPANY

Production Cost Report―BOTTLING DEPARTMENT

Month Ended February 29, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work-in-process

Transferred in

166,000

Total units to account for

170,000

Units accounted for:

Completed and transferred out

150,000

150,000

Ending work-in-process

Total units accounted for

170,000

150,000

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

$ 1,500

$ 0

$ 930

$ 2,430

Costs added during period

Total costs to account for

Divided by: Total EUP

Cost per equivalent unit

$ 0.79

Costs accounted for:

Completed and transferred out

$ 52,500

Ending work-in-process

Total costs accounted for

$ 57,400

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Feb. 29

Finished Goods Inventory

204,000

204,000

Requirement 3

Work-in–Process―Bottling

Balance, Feb. 1

2,430

204,000

Transferred to Finished Goods

Transferred In

Direct Materials

Direct Labor

Manufacturing Overhead

Balance, Feb. 29

E18-26 Preparing journal entries—inputs

Learning Objective 4

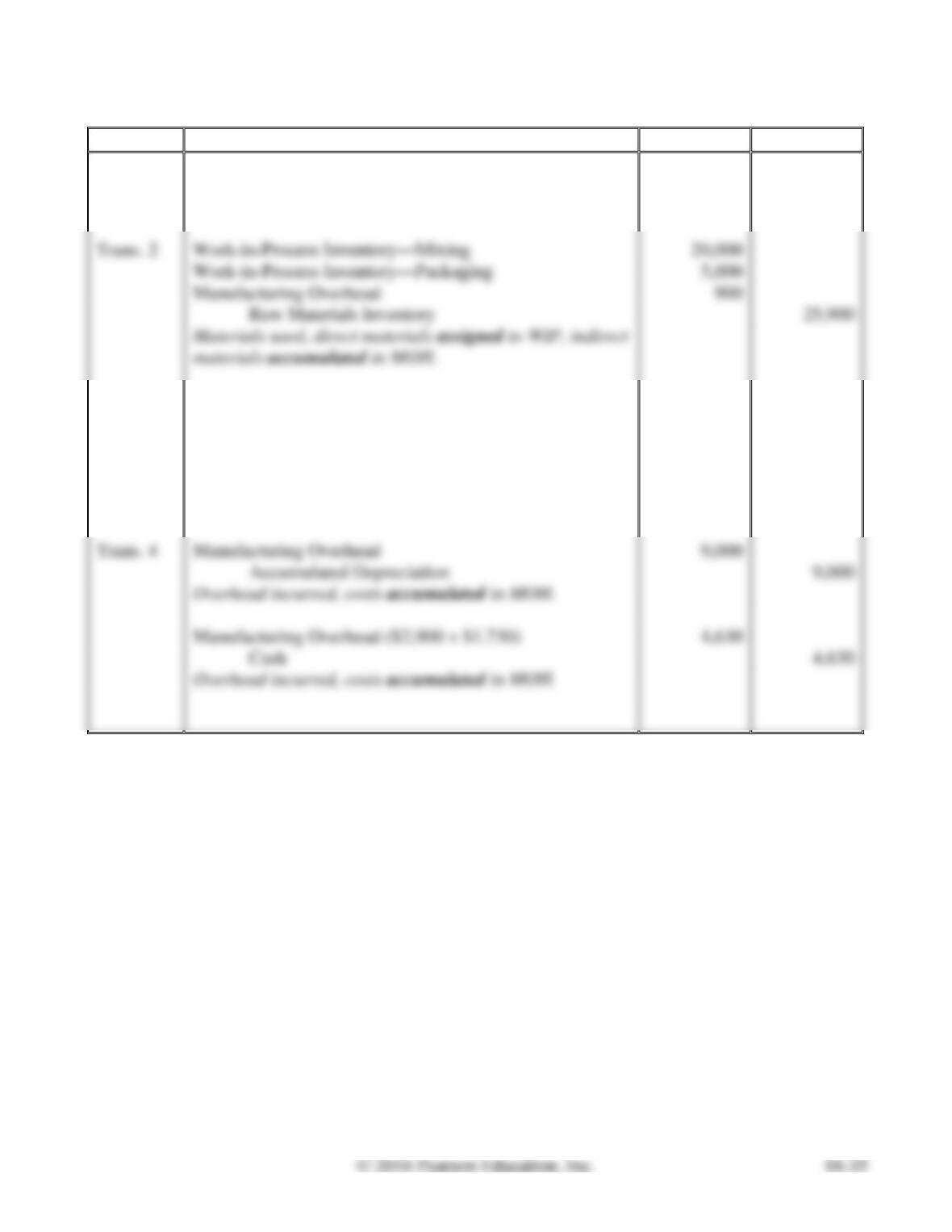

Austin Company had the following transactions in October:

• Purchased raw materials on account, $50,000

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Trans. 1

Raw Materials Inventory

50,000

Accounts Payable

50,000

Materials purchased, accumulated in RM.

Trans. 2

Work-in–Process Inventory―Mixing

20,000

Work-in–Process Inventory―Packaging

5,000

Manufacturing Overhead

Raw Materials Inventory

25,900

Materials used, direct materials assigned to WIP, indirect

materials accumulated in MOH.

Trans. 3

Work-in–Process Inventory―Mixing

8,000

Work-in–Process Inventory―Packaging

3,500

Manufacturing Overhead

2,400

Wages Payable

13,900

Labor incurred, direct labor assigned to WIP, indirect

labor accumulated in MOH.

Trans. 4

Manufacturing Overhead

9,000

Accumulated Depreciation

9,000

Overhead incurred, costs accumulated in MOH.

Manufacturing Overhead ($2,900 + $1,730)

4,630

Cash

4,630

E18-27 Preparing journal entries—outputs

Learning Objective 4

Galvan Company has a production process that involves three processes. Units move through the

processes in this order: cutting, stamping, and then polishing. The company had the following

transactions in November:

• Cost of units completed in the Cutting Department, $19,000

• Cost of units completed in the Stamping Department, $23,000

• Cost of units completed in the Polishing Department, $39,000

• Sales on account, $20,000

• Cost of goods sold is 40% of sales

Prepare the journal entries for Galvan Company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Nov. 30

Work-in-Process Inventory―Stamping

19,000

Work-in–Process Inventory―Cutting

19,000

Transfer costs assigned to units transferred.

Work-in–Process Inventory―Polishing

23,000

Work-in–Process Inventory―Stamping

23,000

Transfer costs assigned to units transferred.

Work-in–Process Inventory―Polishing

39,000

Transfer costs assigned to finished goods.

Accounts Receivable

20,000

20,000

Cost of Goods Sold ($20,000 × 40%)

Units sold, costs assigned to COGS.

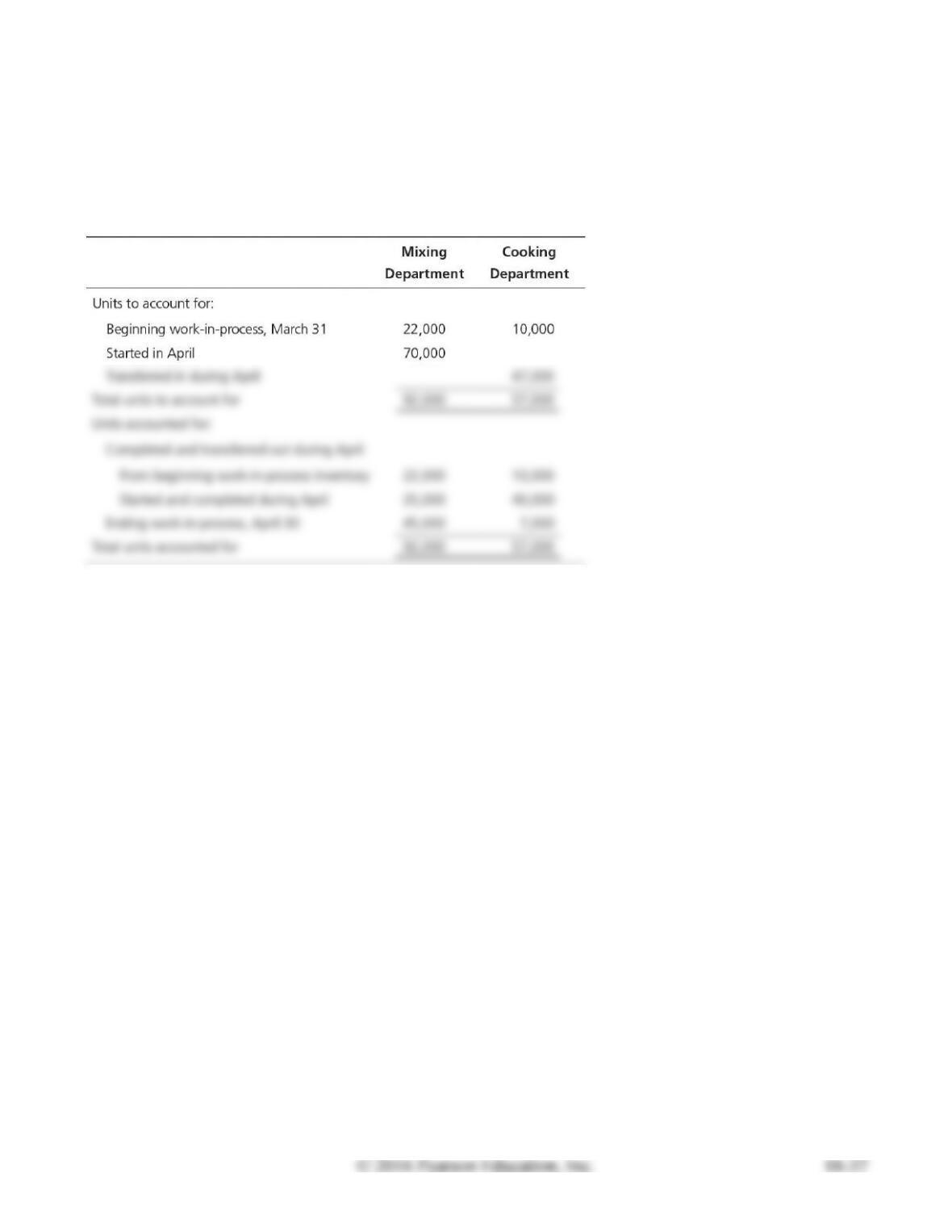

E18A-28 Computing EUP—FIFO method

Learning Objective 6

Appendix 18A

Paul’s Frozen Pizzas uses FIFO process costing. Selected production and cost data fol– low for April

2016.

Requirements

1. Calculate the following:

a. On March 31, the Mixing Department beginning Work-in-Process Inventory was 30% complete

for materials and 45% complete for conversion costs. This means that for the beginning

inventory ____ % of the materials and ____ % of the conversion costs were added during April.

b. On April 30, the Mixing Department ending Work-in-Process Inventory was 65% complete for

materials and 75% complete for conversion costs. This means that for the ending inventory ____

% of the materials and ____ % of the conversion costs were added during April.

c. On March 31, the Cooking Department beginning Work-in-Process Inventory was 70% complete

for materials and 80% complete for conversion costs. This means that for the beginning

inventory ____ % of the materials and ____ % of the conversion costs were added during April.

d. On April 30, the Cooking Department ending Work-in-Process Inventory was 55% complete for

materials and 80% complete for conversion costs. This means that for the ending inventory ____

% of the materials and ____ % of the conversion costs were added during April.

2. Use the information in the table and the information in Requirement 1 to compute the equivalent

units of production for transferred in costs, direct materials, and conversion costs for both the

Mixing and the Cooking Departments.

SOLUTION

Requirement 1

a.

70%, 55%

65%, 75%

c.

30%, 20%

55%, 80%

Requirement 2

Mixing Department

Total EUP for transferred in = 0 EUP (Mixing Department is the first process, so there is no

transferred in.)

Beginning WIP units:

22,000 units × 70%

=

Started and completed units:

25,000 units × 100%

=

In process units:

45,000 units × 65%

=

Total EUP for direct materials:

=

Beginning WIP units:

22,000 units × 55%

=

Started and completed units:

25,000 units × 100%

=

In process units:

45,000 units × 75%

=

Total EUP for conversion costs:

=

Cooking Department

Beginning WIP units:

10,000 units × 0%

=

0 EUP for transferred in

Completed units:

40,000 units × 100%

=

40,000 EUP for transferred in

In process units:

7,000 units × 100%

=

7,000 EUP for transferred in

Total EUP for direct materials:

=

47,000 EUP for transferred in

Beginning WIP units:

10,000 units × 30%

=

Completed units:

40,000 units × 100%

=

In process units:

7,000 units × 55%

=

Total EUP for direct materials:

=

Beginning WIP units:

10,000 units × 20%

=

Completed units:

40,000 units × 100%

=

In process units:

7,000 units × 80%

=

Total EUP for conversion costs:

=

Problems (Group A)

For all Problems, assume the weighted-average method is to be used unless you are told otherwise.

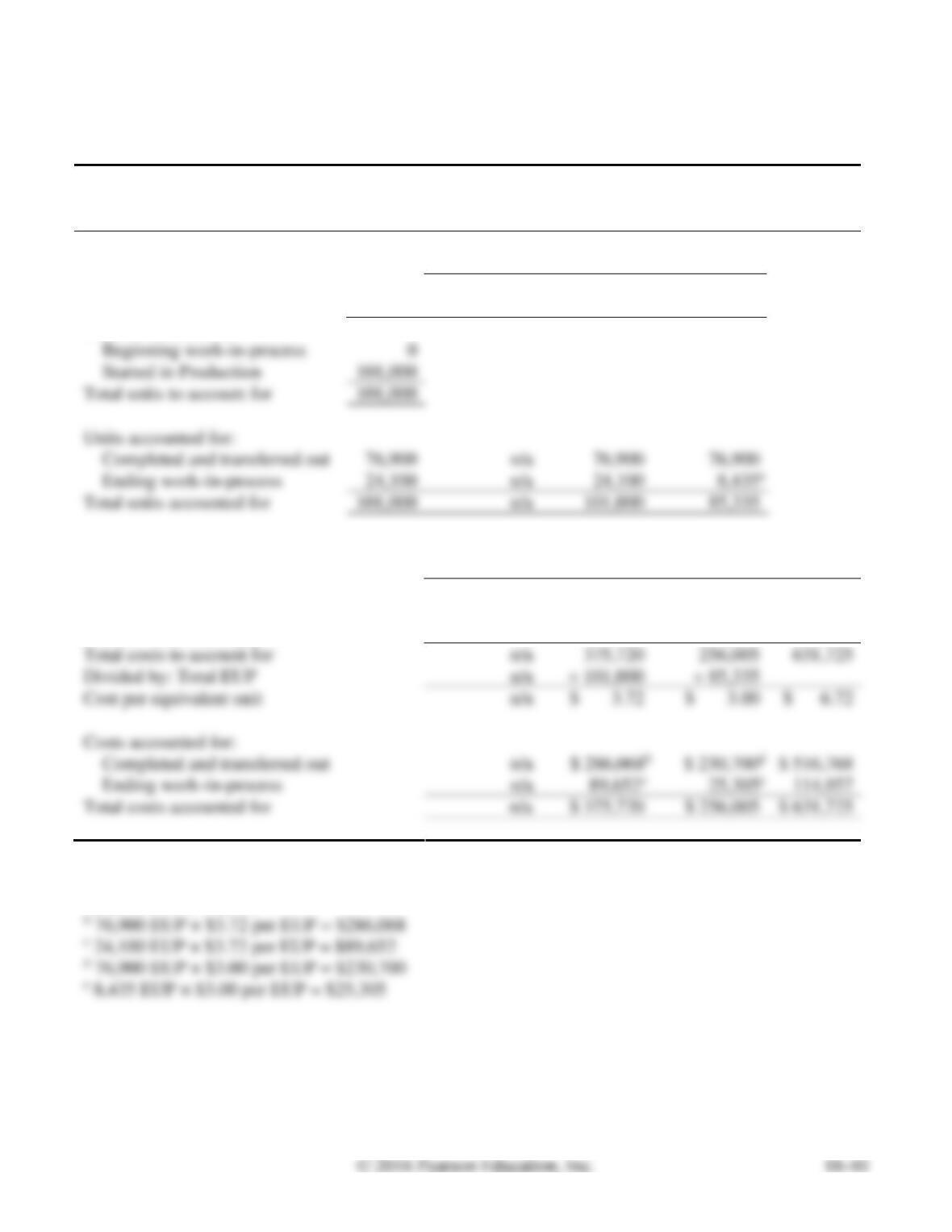

P18-29A Preparing a production cost report, no beginning WIP or costs transferred in

Learning Objectives 2, 3

1. Cost per EUP for DM $3.72

2. WIP Balance $114,957

Abby Electronics makes DVD players in three processes: assembly, programming, and packaging.

Direct materials are added at the beginning of the assembly process. Conversion costs are incurred

evenly throughout the process. The Assembly Department had no Work-in-Process Inventory on

October 31. In mid-November, Abby Electronics started production on 101,000 DVD players. Of this

number, 76,900 DVD players were assembled during November and transferred out to the Programming

Department. The November 30 Work-in-Process Inventory in the Assembly Department was 35% of the

way through the assembly process. Direct materials costing $375,720 were placed in production in

Assembly during November, direct labor of $157,500 was assigned, and manufacturing overhead of

$98,505 was allocated to that department.

Requirements

1. Prepare a production cost report for the Assembly Department for November.

SOLUTION

Requirement 1

ABBY ELECTRONICS

Production Cost Report―ASSEMBLY DEPARTMENT

Month Ended November 30.

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work-in-process

Started in Production

101,000

Total units to account for

101,000

Units accounted for:

Completed and transferred out

n/a

Ending work-in-process

n/a

Total units accounted for

101,000

n/a

101,000

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

n/a

$ 0

$ 0

$ 0

Costs added during period

n/a

375,720

256,005

631,725

Total costs to account for

n/a

375,720

256,005

631,725

Divided by: Total EUP

n/a

Cost per equivalent unit

n/a

$ 3.00

Costs accounted for:

Completed and transferred out

n/a

$ 516,768

Ending work-in-process

n/a

114,957

Total costs accounted for

n/a

$ 256,005

$ 631,725

a 24,100 × 35% = 8,435