P18-37B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Sep. 30

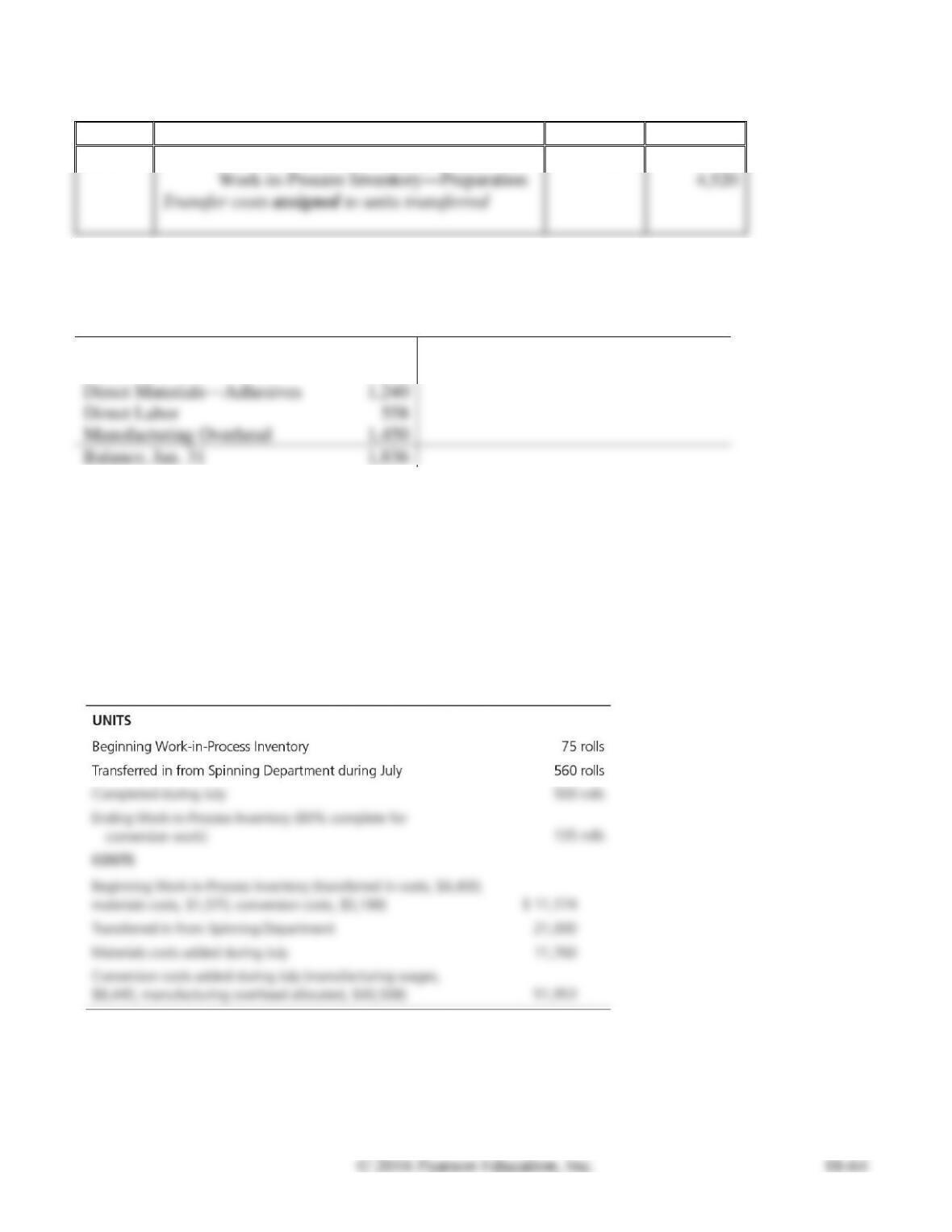

Work-in–Process Inventory―Mixing

5,675

Raw Materials Inventory

5,675

Materials used, direct materials assigned to WIP.

Work-in–Process Inventory―Mixing

Wages Payable

Work-in–Process Inventory―Mixing

6,240

Manufacturing Overhead

6,240

Work-in–Process Inventory―Cooking

P18-38B Preparing a production cost report, two materials added at different points, no beginning

WIP or costs transferred in; journal entries

Learning Objectives 2, 3, 4

1. Total cost per EUP $2.26

3. WIP Balance $1,836

John’s Exteriors produces exterior siding for homes. The Preparation Department begins with wood,

which is chopped into small bits. At the end of the process, an adhesive is added. Then the

wood/adhesive mixture goes on to the Compression Department, where the wood is compressed into

sheets. Conversion costs are added evenly throughout the preparation process. January data for the

Preparation Department are as follows:

Requirements

1. Prepare a production cost report for the Preparation Department for January. (Hint: Each direct

material added at a different point in the production process requires its own equivalent unit of

production computation.)

2. Prepare the journal entry to record the cost of the sheets completed and transferred out to the

Compression Department.

3. Post the journal entries to the Work-in-Process Inventory—Preparation T-account. What is the

ending balance?

SOLUTION

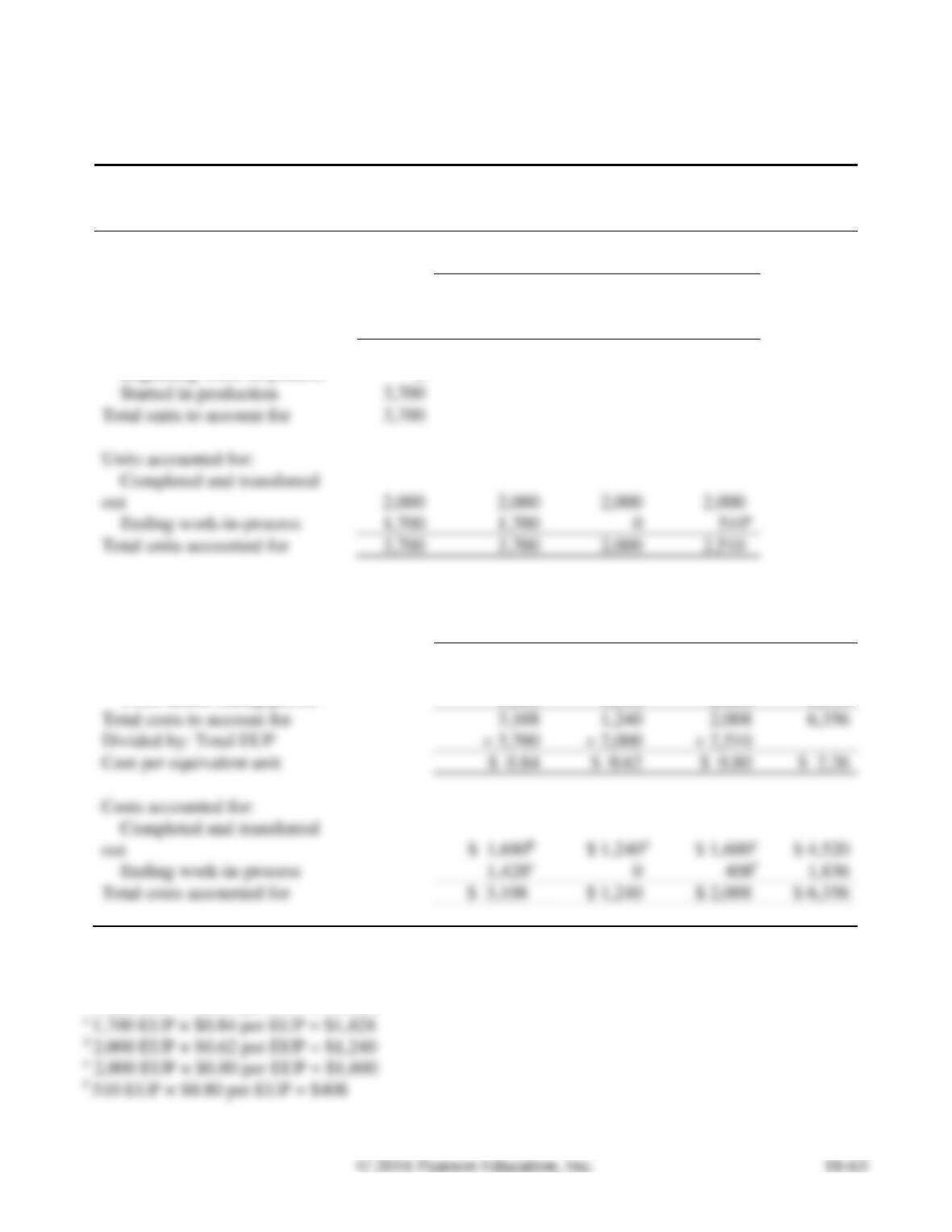

Requirement 1

JOHN’S EXTERIORS

Production Cost Report―PREPARATION DEPARTMENT

Month Ended January 31, 20XX

Equivalent Units

UNITS

Whole

Units

Direct

Materials–

Wood

Direct

Materials–

Adhesive

Conversion

Costs

Units to account for:

Beginning work-in-process

0

Started in production

Total units to account for

Units accounted for:

out

2,000

2,000

Ending work-in-process

1,700

Total units accounted for

3,700

2,000

COSTS

Direct

Materials–

Wood

Direct

Materials–

Adhesive

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

$ 0

$ 0

$ 0

$ 0

Costs added during period

3,108

1,240

2,008

6,356

Total costs to account for

3,108

1,240

Divided by: Total EUP

Cost per equivalent unit

Costs accounted for:

out

$ 4,520

Ending work-in-process

1,836

Total costs accounted for

$ 2,008

$ 6,356

a 1,700 × 30% = 510

b 2,000 EUP × $0.84 per EUP = $1,680

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jan. 31

Work-in–Process Inventory―Compression

4,520

4,520

Requirement 3

Work-in-Process―Preparation

Balance, Jan. 1

0

4,520

Transferred to Compression

Direct Materials––Wood

3,108

Direct Materials––Adhesives

1,240

Direct Labor

Manufacturing Overhead

1,450

Balance, Jan. 31

1,836

P18-39B Preparing a production cost report, second department with beginning WIP; journal

entries

Learning Objectives 2, 3, 4

1. Cost per EUP DM $21.00

Carrie Carpet manufactures broadloom carpet in seven processes: spinning, dyeing, plying, spooling,

tufting, latexing, and shearing. In the Dyeing Department, direct materials (dye) are added at the

beginning of the process. Conversion costs are incurred evenly throughout the process. Information for

July 2016 follows:

Requirements

1. Prepare a production cost report for Carrie’s Dyeing Department for July.

2. Journalize all transactions affecting Carrie’s Dyeing Department during July, including the entries

that have already been posted.

SOLUTION

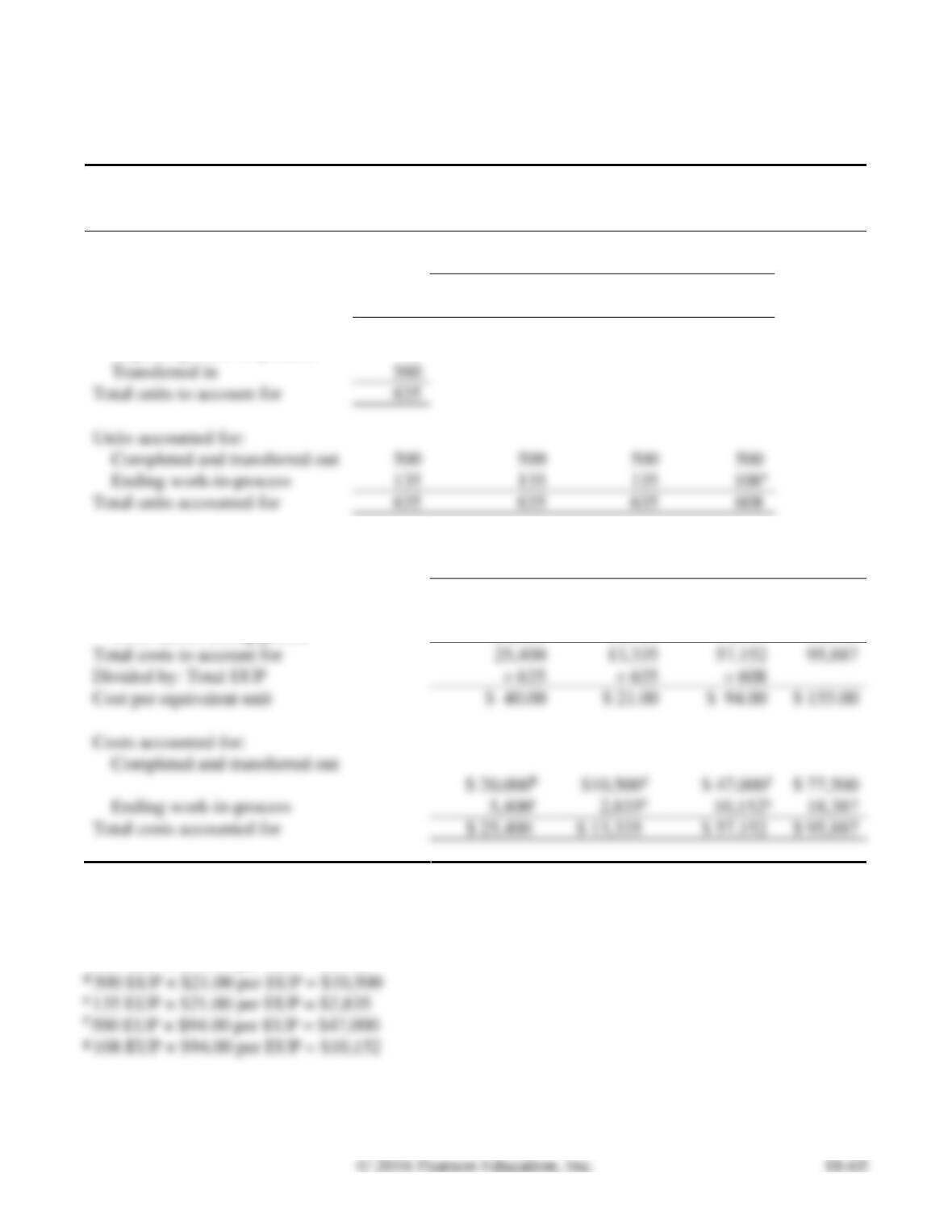

Requirement 1

CARRIE CARPET

Production Cost Report―DYEING DEPARTMENT

Month Ended July 31, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work-in-process

75

Transferred in

Total units to account for

Units accounted for:

Completed and transferred out

Ending work-in-process

Total units accounted for

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

$ 4,400

$ 1,575

$ 5,199

$ 11,174

Costs added during period

21,000

11,760

51,953

84,713

Total costs to account for

25,400

13,335

57,152

Divided by: Total EUP

Cost per equivalent unit

$ 40.00

$ 21.00

$ 94.00

$ 155.00

Costs accounted for:

$ 77,500

Ending work-in-process

18,387

Total costs accounted for

$ 25,400

$ 13,335

$ 95,887

a 135 × 80% = 108

b 500 EUP × $40.00 per EUP = $20,000

c 135 EUP × $40.00 per EUP = $5,400

e 135 EUP × $21.00 per EUP = $2,835

g 108 EUP × $94.00 per EUP = $10,152

P18-39B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 31

Work-in–Process Inventory―Dyeing

21,000

Work-in–Process―Spinning

21,000

Transfer costs assigned to units transferred.

Work-in–Process Inventory―Dyeing

11,760

Raw Materials Inventory

11,760

Work-in–Process Inventory―Dyeing

Wages Payable

Labor incurred, direct labor assigned to WIP.

Work-in–Process Inventory―Dyeing

43,508

Manufacturing Overhead

43,508

Work-in–Process Inventory―Plying

77,500

Work-in–Process Inventory―Dyeing

77,500

Transfer costs assigned to units transferred.

P18-40B Preparing a production cost report, second department with beginning WIP; decision

making

Learning Objectives 2, 3, 5

1. Cost per EUP CC $15.00

Lake Bound uses three processes to manufacture lifts for personal watercrafts: forming a lift’s parts

from galvanized steel, assembling the lift, and testing the completed lift. The lifts are transferred to

finished goods before shipment to marinas across the country.

Lake Bound’s Testing Department requires no direct materials. Conversion costs are incurred evenly

throughout the testing process. Other information follows for October 2016:

The cost transferred into Finished Goods Inventory is the cost of the lifts transferred out of the Testing

Department. Lake Bound uses weighted-average process costing.

Requirements

1. Prepare a production cost report for the Testing Department.

2. What is the cost per unit for lifts completed and transferred out to Finished Goods Inventory? Why

would management be interested in this cost?

SOLUTION

Requirement 1

LAKE BOUND

Production Cost Report―TESTING DEPARTMENT

Month Ended October 31, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work-in-process

Transferred in

Total units to account for

Units accounted for:

Completed and transferred out

n/a

Ending work-in-process

n/a

Total units accounted for

n/a

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Costs to account for:

Beginning work-in-process

$ 93,200

n/a

$ 18,300

$ 111,500

Costs added during period

687,000

n/a

76,800

763,800

Total costs to account for

780,200

n/a

95,100

875,300

Divided by: Total EUP

÷ 9,400

n/a

÷ 6,340

Cost per equivalent unit

$ 83.00

n/a

$ 15.00

$ 98.00

Costs accounted for:

Completed and transferred out

n/a

$ 421,400

Ending work-in-process

n/a

453,900

Total costs accounted for

n/a

$ 95,100

$ 875,300

P18-40B, cont.

Requirement 2

Costs per lift

=

Total Costs

/

Units Completed and Transferred Out

=

$421,400

/

4,300 lifts

=

$98.00 average cost per lift

P18A-41B Preparing a production cost report, second department, with beginning WIP and

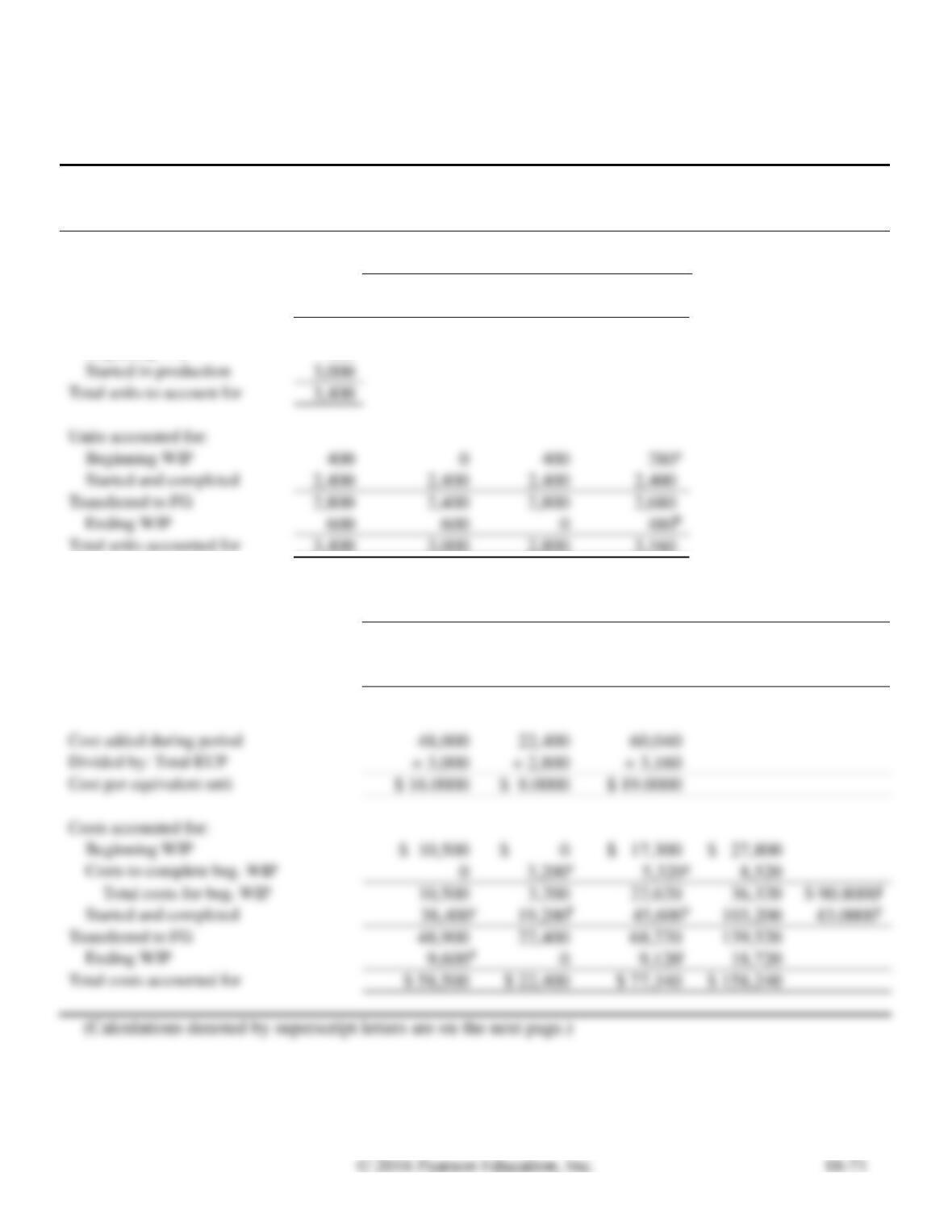

transferred in costs, FIFO method

Learning Objective 6

Appendix 18A

1. Cost per EUP CC $19.0000

Vuma, Inc. manufactures tire tubes in a two-stage process that includes assembly and sealing. The

Sealing Department tests the tubes and adds a puncture-resistant coating to each tube to prevent air

leaks.

The direct materials (coating) are added at the end of the sealing process.

Conversion costs are incurred evenly throughout the process. Work in process of the Sealing

Department on March 31, 2016, consisted of 400 tubes that were 30% of the way through the production

Requirements

1. Prepare a production cost report for the Sealing Department for April.

2. Journalize all transactions affecting the Sealing Department during April, including the entries that

have already been posted.

SOLUTION

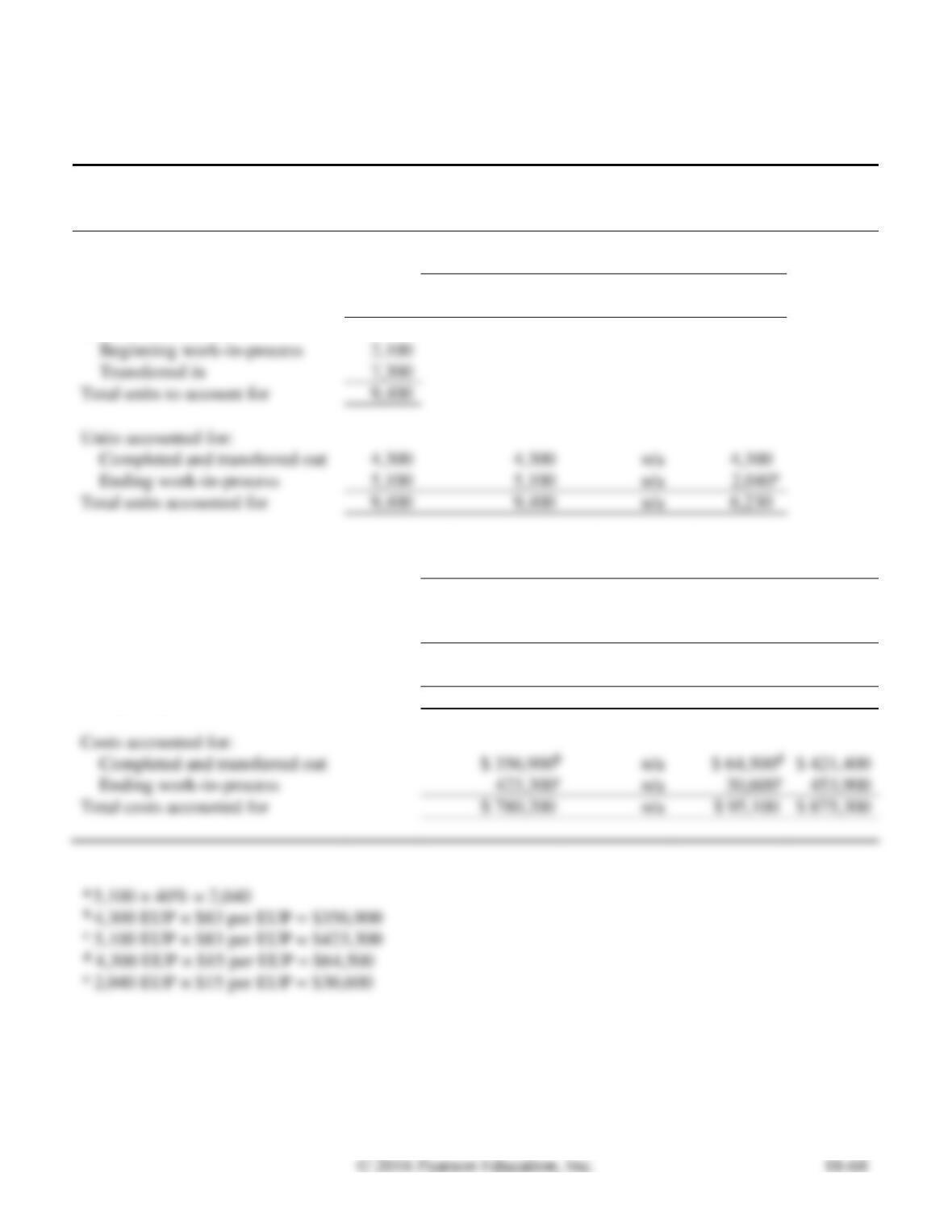

Requirement 1

VUMA, INC.

Production Cost Report―SEALING DEPARTMENT

Month Ended April 30, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning WIP

400

Started in production

3,000

Total units to account for

3,400

Units accounted for:

Beginning WIP

400

Started and completed

2,400

2,400

2,400

2,400

Transferred to FG

2,800

2,400

2,800

2,680

Ending WIP

600

Total units accounted for

3,400

3,000

2,800

3,160

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Cost

per Unit

Costs to account for:

Beginning work-in-process

$ 10,500

$ 0

$ 17,300

$ 27,800

Costs added during period

48,000

22,400

60,040

130,440

Total costs to account for

58,500

22,400

77,340

158,240

Cost added during period

48,000

22,400

60,040

Divided by: Total EUP

÷ 3,160

Cost per equivalent unit

$ 16.0000

$ 8.0000

Costs accounted for:

Beginning WIP

$ 10,500

$ 0

Costs to complete beg. WIP

8,520

Total costs for beg. WIP

10,500

3,200

22,620

36,320

Started and completed

103,200

Transferred to FG

48,900

22,400

68,220

139,520

Ending WIP

18,720

Total costs accounted for

$ 58,500

$ 22,400

P18A-41B, cont.

Requirement 1, cont.

a 400 × 70% = 280

b 600 × 80% = 480

c 2,400 EUP × $16.0000 per EUP = $38,400

g 280 EUP × $19.0000 per EUP = $5,320

h 2,400 EUP × $19.0000 per EUP = $45,600

k $103,200 / 2,400 units = $43.0000 per unit

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Apr. 30

Work-in–Process Inventory―Sealing

48,000

Work-in–Process―Assembly

48,000

Transfer costs assigned to units transferred.

Work-in–Process Inventory―Sealing

22,400

22,400

Work-in–Process Inventory―Sealing

19,850

19,850

Labor incurred, direct labor assigned to WIP.

Work-in–Process Inventory―Sealing

40,190

40,190

Finished Goods Inventory

Work-in–Process Inventory―Sealing

Transfer costs assigned to units transferred.

P18A-42B Preparing a production cost report, second department with beginning WIP; journal

entries

Learning Objective 6

Appendix 18A

1. Cost per EUP DM $21.0000

Work Problem P18-39B using the FIFO method. The Dyeing Department beginning work in process of

75 units is 80% complete as to conversion costs. Round equivalent unit costs to four decimal places.

SOLUTION

Requirement 1

CARRIE CARPET

Production Cost Report―DYEING DEPARTMENT

Month Ended July 31, 2016

Equivalent Units

UNITS

Whole

Units

Transferred

In

Direct

Materials

Conversion

Costs

Units to account for:

Beginning WIP

75

Started in production

Total units to account for

Units accounted for:

Beginning WIP

75

Started and completed

425

Transferred to Plying

440

Ending WIP

Total units accounted for

548

COSTS

Transferred

In

Direct

Materials

Conversion

Costs

Total

Costs

Cost

per Unit

Costs to account for:

Beginning work-in-process

$ 4,400

$ 1,575

$ 5,199

$ 11,174

Costs added during period

21,000

11,760

51,953

84,713

Total costs to account for

25,400

13,335

57,152

95,887

Cost added during period

21,000

11,760

51,953

84,713

Divided by: Total EUP

÷ 560

÷ 548

Cost per equivalent unit

$ 21.0000

Costs accounted for:

Beginning WIP

$ 11,174

Costs to complete beg. WIP

Total costs for beg. WIP

12,596

Started and completed

Transferred to Plying

20,338

10,500

46,913

77,751

Total costs accounted for

$ 25,401

P18A-42B, cont.

Requirement 1, cont.

a 75 × 20% = 15

b 135 × 80% = 108

c 425 EUP × $37.5000 per EUP = $15,938

d 135 EUP × $37.5000 per EUP = $5,063

e 425 EUP × $21.0000 per EUP = $8,925

g 15 EUP × $94.8047 per EUP = $1,422

h 425 EUP × $94.8047 per EUP = $40,292

k $65,155 / 425 units = $153.3059 per unit

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 31

Work-in–Process Inventory―Dyeing

21,000

Work-in–Process―Spinning

21,000

Transfer costs assigned to units transferred.

Work-in–Process Inventory―Dyeing

11,760

11,760

Work-in–Process Inventory―Dyeing

Labor incurred, direct labor assigned to WIP.

Work-in-Process Inventory―Dyeing

43,508

43,508

Work-in–Process Inventory―Plying

77,751

Work-in–Process Inventory―Dyeing

77,751

Transfer costs assigned to units transferred.

CRITICAL THINKING

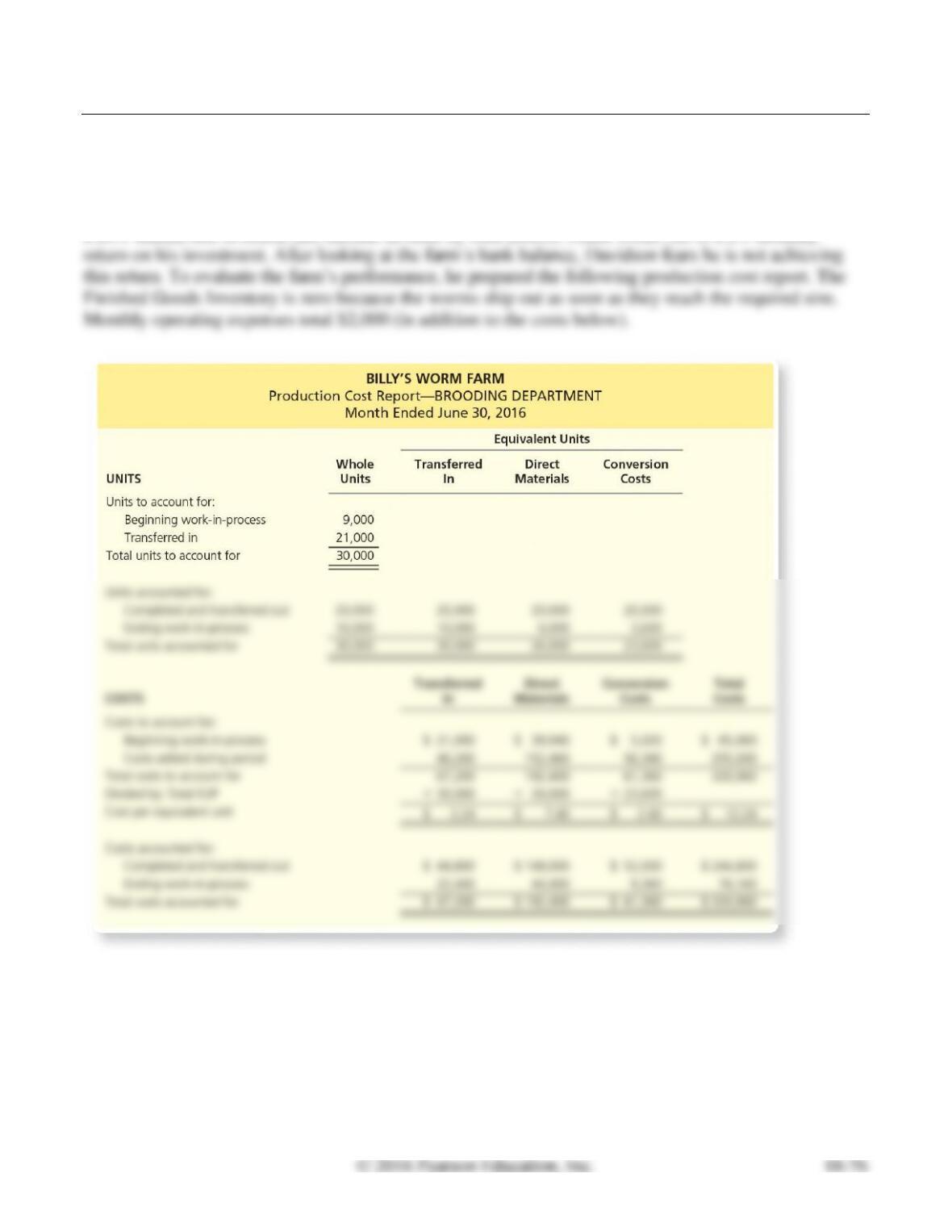

Decision Case 18-1

Billy Davidson operates Billy’s Worm Farm in Mississippi. Davidson raises worms for fishing. He sells

a box of 20 worms for $12.60. Davidson has invested $400,000 in the worm farm. He had hoped to earn

a 24% annual rate of return (net income divided by total assets), which works out to a 2% monthly

Requirements

Billy Davidson has the following questions about the farm’s performance during June.

1. What is the cost per box of worms sold? (Hint: This is the unit cost of the boxes completed and

shipped out of brooding.)

2. What is the gross profit per box?

3. How much operating income did Billy’s Worm Farm make in June?

4. What is the return on Davidson’s investment of $400,000 for the month of June? (Compute this as

June’s operating income divided by Davidson’s $400,000 investment, expressed as a percentage.)

5. What monthly operating income would provide a 2% monthly rate of return? What price per box

would Billy’s Worm Farm have had to charge in June to achieve a 2% monthly rate of return?

SOLUTION

Requirement 1

Cost per box of worms sold

=

Total costs of boxes of worms

completed and transferred out

/

Units completed

and transferred out

=

=

Requirement 2

Gross Profit per Box

=

Sales Price per Box

–

Cost of Goods Sold per Box

=

$12.60

–

$12.24

=

$0.36

Requirement 3

=

Gross Profit per Box

Boxes Sold

=

=

Operating Income

=

–

Operating Expenses

=

–

=

Decision Case 18-1, cont.

Requirement 4

Return on Investment

=

Operating Income

/

Investment

=

/

$400,000

=

Requirement 5

Operating Income

=

Investment

×

Return on Investment

=

$400,000

×

2.0%

=

$8,000

=

Operating Income

+

Operating Expenses

=

+

=

Gross Profit per Box

=

Boxes Sold

=

=

=

Gross Profit per Box

+

Cost of Goods Sold per Box

=

+

=

Ethical Issue 18-1

Rick Pines and Joe Lopez are the plant managers for High Mountain Lumber’s particle board division.

High Mountain Lumber has adopted a just-in-time management philosophy. Each plant combines wood

chips with chemical adhesives to produce particle board to order, and all product is sold as soon as it is

completed. Laura Green is High Mountain Lumber’s regional controller. All of High Mountain

Requirements

1. How would inflating the percentage completion of ending Work-in-Process Inventory help Pines and

Lopez get their bonus?

2. The particle board division is the largest of High Mountain Lumber’s divisions. If Green does not

correct the percentage completion of this year’s ending Work– in-Process Inventory, how will the

misstatement affect High Mountain Lumber’s financial statements?

3. Evaluate Lopez’s justification, including the effect, if any, on next year’s financial statements.

4. Address the following: What is the ethical issue? What are the options? What are the potential

consequences? What should Green do?

SOLUTION

Requirement 1

By inflating the percentage of completion for the work in process, fewer costs would be assigned to the

Requirement 2

The misstatement of the percentage of completion for the work in process will cause the company to

Requirement 3

Lopez’s justification that they would complete the work in process the next year is true, but costs would

Requirement 4

The ethical issue is the willingness to misstate information in order to earn a bonus. If Lopez and Pines