38

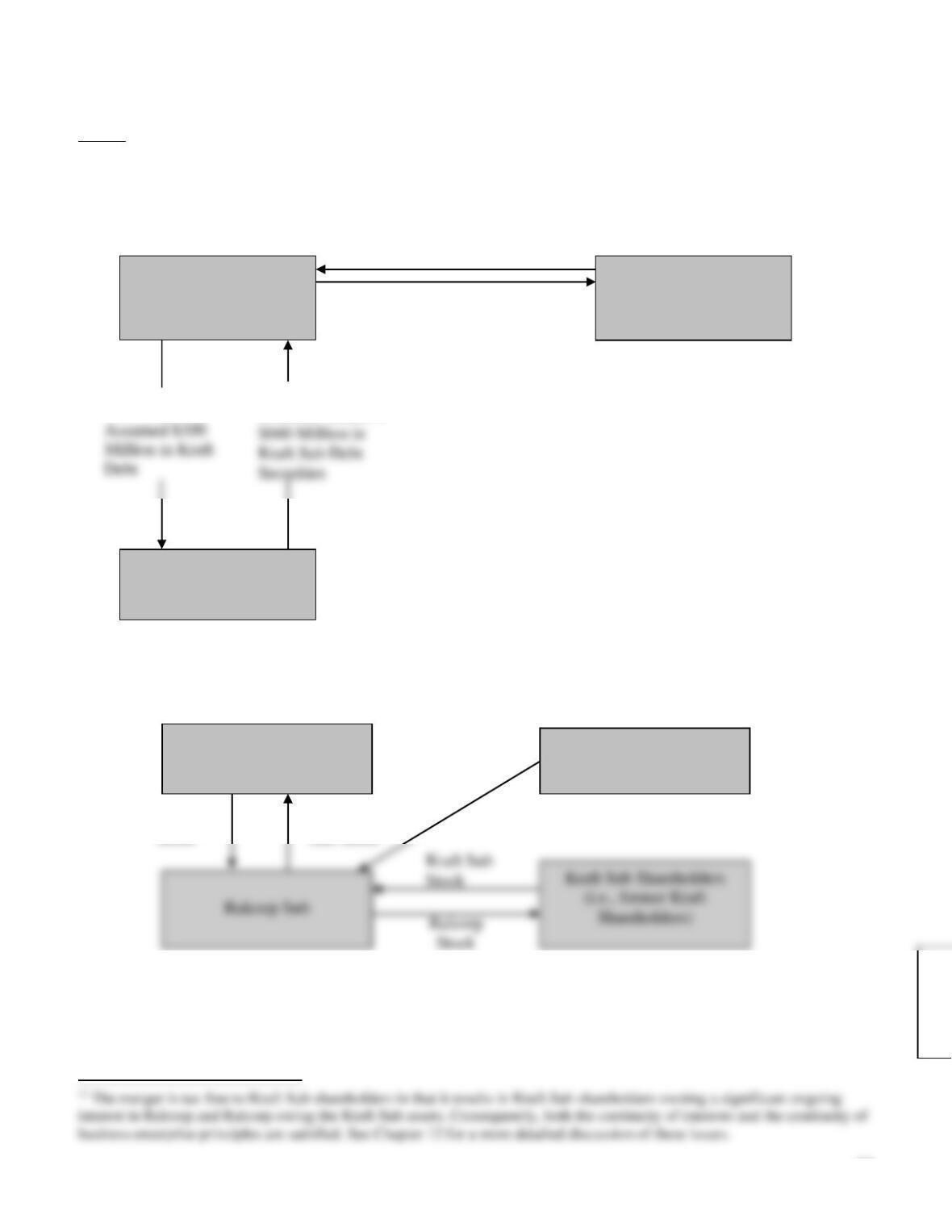

Exhibit 15-1. Structuring the Transaction

Step 1: Kraft creates a shell subsidiary (Kraft Sub) and transfers Post assets and liabilities and

$300 million in Kraft debt into the shell in exchange for Kraft Sub stock plus $660 million in

Kraft Sub debt securities. Kraft also implements an exchange offer of Kraft Sub for Kraft

common stock.

Step 2: Kraft Sub, as an independent company, is merged in a forward triangular tax-free merger with a sub of Ralcorp

(Ralcorp Sub) in which Kraft Sub shares are exchanged for Ralcorp shares, with Ralcorp Sub surviving.12

Sara Lee Attempts to Create Value through Restructuring

Kraft Sub (Post)

Kraft Shareholders

Tendering Kraft Shares

Kraft Foods

Post Assets &

Liabilities +

Kraft Sub

Common Shares +

Kraft Shares

Kraft Sub Shares

Ralcorp

Kraft Sub (Post)

Ralcorp

Stock

Ralcorp

Sub Stock

Kraft Sub Assets & Liabilities

39

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention

to split the firm into two separate publicly traded companies. The two companies would consist of the firm’s North American

retail and food service division and its international beverage business. The announcement comes after a long string of

restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful

than earlier efforts.

In September 1997, Sara Lee embarked on a major restructuring effort designed to boost both profits, which had been

growing by about 6% during the previous five years, and the company’s lagging share price. The restructuring program was

intended to reduce the firm’s degree of vertical integration, shifting from a manufacturing and sales orientation to one focused

on marketing the firm’s top brands. The firm increasingly viewed itself as more of a marketing than a manufacturing

enterprise.

Sara Lee outsourced or sold 110 manufacturing and distribution facilities over the next two years. Nearly 10,000 employees,

representing 7% of the workforce, were laid off. The proceeds from the sale of facilities and the cost savings from outsourcing

were either reinvested in the firm’s core food businesses or used to repurchase $3 billion in company stock. 1n 1999 and 2000,

the firm acquired several brands in an effort to bolster its core coffee operations, including such names as Chock Full o’Nuts,

Hills Bros, and Chase & Sanborn.

Despite these restructuring efforts, the firm’s stock price continued to drift lower. In an attempt to reverse the firm’s

misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas:

food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and

European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded

Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from

the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business.

In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter &

Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee’s outstanding

shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If

completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

40

A shareholder owning 100 Sara Lee shares when the spin-off was announced would have been entitled to 12.5 HanesBrands

shares. However, they would have actually received 12 shares plus $11.03 for fractional shares (i.e., 0.5 × $22.06).

A shareholder of record who had 100 Sara Lee shares on the announcement date of the restructuring program and held their

shares until the end of 2010 would have seen their investment decline 24% from $1,956 (100 shares × $19.56 per share) to

$1,486.56 by the end of 2010. However, this would have been partially offset by the appreciation of the HanesBrands shares

between 2006 and 2010. Therefore, the total value of the hypothetical shareholder’s investment would have decreased by 7.5%

from $1,956 to $1,809.47 (i.e., $1,486.56 + 12 HanesBrands shares × $25.99 + $11.03). This compares to a more modest 5%

loss for investors who put the same $1,956 into a Standard & Poor’s 500 stock index fund during the same period.

Case Study Discussion Questions:

1. In what sense is the Sara Lee business strategy in effect a breakup strategy? Be specific.

Answer: Sara Lee’s stated strategy was to increase focus on the firm’s highest growth businesses by exiting the

slower growing or underperforming operations. The firm also hoped to create shareholder value through spin-offs

2. Would you expect investors to be better off buying Sara Lee stock or investing in a similar set of consumer

product businesses in their own personal investment portfolios? Explain your answer.

Answer: In general, it is less expensive for individual investors to assemble a diversified portfolio of stocks on

3. Speculate as to why the 2005 restructure program appears to have been unsuccessful in achieving a sustained

increase in Sara Lee’s earnings per share and in turn creating value for the Sara Lee shareholders?

Answer: The aggressiveness of the program may have prevented management from managing effectively their

4. Why is a breakup strategy conceptually simple to explain but often difficult to implement? Be specific.

Answer: A breakup strategy is one in which a firm’s operations are offered for sale as independent, standalone

41

5. Explain why Sara Lee may have chosen to spin-off rather than to divest HanesBrands Inc.? Be specific.

Answer: A spin-off may have been preferable because Sara Lee was unable to get what they thought the business

Bristol-Myers Squibb Splits Off Rest of Mead Johnson

Facing the loss of patent protection for its blockbuster drug Plavix, a blood thinner, in 2012, Bristol-Myers Squibb Company

decided to split off its 83% ownership stake in Mead Johnson Nutrition Company in late 2009 through an offer to its

shareholders to exchange their Bristol-Myers shares for Mead Johnson shares. The decision was part of a longer-term

restructuring strategy that included the sale of assets to raise money for acquisitions of biotechnology drug companies and the

elimination of jobs to reduce annual operating expenses by $2.5 billion by the end of 2012.

Bristol-Myers anticipated a significant decline in operating profit following the loss of patent protection as increased

competition from lower-priced generics would force sizeable reductions in the price of Plavix. Furthermore, Bristol-Myers

considered Mead Johnson, a baby formula manufacturer, as a noncore business that was pursuing a focus on biotechnology

drugs. Bristol-Myers shareholders greeted the announcement positively, with the firm’s shares showing the largest one-day

increase in eight months.

British Petroleum Sells Oil and Gas Assets to Apache Corporation

In the months that followed the oil spill in the Gulf of Mexico, British Petroleum agreed to create a $20 billion fund to help

cover the damages and cleanup costs associated with the spill. The firm had agreed to contribute $5 billion to the fund before

the end of 2010. To help meet this obligation and to help finance the more than $4 billion already spent on the spill, the firm

announced on July 20, 2010, that it had reached an agreement to sell Apache Corporation its oil and gas fields in Texas and

southeast New Mexico worth $3.1 billion; gas fields in Western Canada for $3.25 billion; and oil and gas properties in Egypt

for $650 million. All of these properties had been in production for years, and their output rates were declining.

42

Apache is a Houston, Texas–based independent oil and gas exploration firm with a reputation for being able to extract

additional oil and gas from older properties. Also, Apache had operations near each of the BP properties, enabling them to take

control of the acquired assets with existing personnel.

Ideally, buyers would like to purchase assets “free and clear” of the environmental liabilities associated with the Gulf oil

spill. Consequently, a buyer of BP assets would have to incorporate such risks in determining the purchase price for such

assets. In some instances, buyers will buy assets only after the seller has gone through the bankruptcy process in order to limit

fraudulent conveyance risks.

Discussion Questions

1. In what sense were the BP properties strategically more valuable to Apache than to British Petroleum?

2. How could Apache have protected itself from risks that they might be required at some point in the future to be liable

for some portion of the BP Gulf–related liabilities? What are some of the ways Apache could have estimated the

potential costs of such liabilities? Be specific.

Anatomy of a Spin-Off

On October 18, 2006, Verizon Communication’s board of directors declared a dividend to the firm’s shareholders consisting of

shares in a company comprising the firm’s domestic print and Internet yellow pages directories publishing operations (Idearc

Inc.). The dividend consisted of 1 share of Idearc stock for every 20 shares of Verizon common stock. Idearc shares were

valued at $34.47 per share. On the dividend payment date, Verizon shares were valued at $36.42 per share. The 1-to–20 ratio

constituted a 4.73% yield—that is, $34.47/ ($36.42 × 20)—approximately equal to Verizon’s then current cash dividend yield.

Because of the spin-off, Verizon would contribute to Idearc all its ownership interest in Idearc Information Services and

other assets, liabilities, businesses, and employees currently employed in these operations. In exchange for the contribution,

Idearc would issue to Verizon shares of Idearc common stock to be distributed to Verizon shareholders. In addition, Idearc

43

1. How do you believe the Idearc shares were valued for purposes of the spin-off? Be specific.

2. Do you believe that it is fair for Idearc to repay a portion of the debt incurred by Verizon relating to Idearc’s operations even

though Verizon included Idearc’s earnings in its consolidated income statement? Is the transfer of excess cash to the parent

fair? Explain your answer.

3. Do you believe shareholders should have the right to approve a spin-off? Explain your answer?

4. To what extent do you believe that Verizon’s activities could be viewed as fraudulent? Explain your answer.

Anatomy of a Split-Off: Bristol-Myers Squibb

Under the Bristol-Myers Squibb exchange offer of Mead Johnson shares for shares of its common stock, announced on

November 16, 2009, each BMS shareholder would receive $1.11 for each $1 of BMS stock tendered and accepted in the

exchange offer. The exchange was subject to an upper limit of 0.6027 shares of MJ common stock per share of BMS common.

On December 4, 2009, BMS amended the offer by increasing the maximum share exchange ratio to 0.6313, indicating it

would accept for exchange a maximum of 269,281,601 shares of its stock and that if the exchange offer were oversubscribed,

all shares tendered would be subject to proration. The proration formula was be determined by dividing the maximum number

of MJ shares BMS was willing to exchange by the number of BMS shares actually tendered.

Discussion Questions:

1. Why did Bristol-Myers Squibb offer its shareholders $1.11 worth of Mead Johnson stock for each $1 of Bristol-Myers

Squibb stock tendered and accepted in the exchange offer?

2. Why did Bristol-Myers Squibb prorate the number of shares tendered in the exchange offer?

Inside M&A. Financial Services Firms Streamline their Operations

During 2005 and 2006, a wave of big financial services firms announced their intentions to spin-off operations that did

not seem to fit strategically with their core business. In addition to realigning their strategies, the parent firms noted the

favorable tax consequences of a spin-off, the potential improvement in the parent’s financial returns, the elimination of

conflicts with customers, and the removal of what, for some, had become a management distraction.

44

Investment bank Morgan Stanley announced in mid-2005 its intent to spin-off its Discover Credit Card operation.

While Discover Card generated about one fifth of the firm’s pretax profits, Morgan Stanley had been unable to realize

significant synergies with its other operations. The move represented an attempt by senior Morgan Stanley management to

mute shareholder criticism of the company’s lackluster stock performance due to what many viewed had been the firm’s

excessive diversification.

Discussion Questions:

1. Speculate as to why a firm may choose to spin-off rather than divest a business?

2. In what ways might the spin-offs harm parent firm shareholders?

Answer: Business units that are spun-off are often emaciated by debt that is transferred by the parent firm to the

AT&T (1984 – 2005)—A POSTER CHILD

FOR RESTRUCTURING GONE AWRY

Between 1984 and 2000, AT&T underwent four major restructuring programs. These included the government-mandated

breakup in 1984, the 1996 effort to eliminate customer conflicts, the 1998 plan to become a broadband powerhouse, and the

most recent restructuring program announced in 2000 to correct past mistakes. It is difficult to identify another major

corporation that has undergone as much sustained trauma as AT&T. Ironically, a former AT&T operating unit acquired its

former parent in 2005.

The 1984 Restructure: Changed the Organization But Not the Culture

The genesis of Ma Bell’s problems may have begun with the consent decree signed with the Department of Justice in 1984,

which resulted in the spin-off of its local telephone operations to its shareholders. AT&T retained its long-distance and

The 1996 Restructure: Lack of a Coherent Strategy

Cash accumulated from the long-distance business was spent on a variety of ill-conceived strategies such as the firm’s foray

into the personal computer business. After years of unsuccessfully attempting to redefine the company’s strategy, AT&T once

The 1998 Restructure: Vision Exceeds Ability to Execute

In its third major restructure since 1984, AT&T CEO Michael Armstrong passionately unveiled in June of 1998 a daring

strategy to transform AT&T from a struggling long-distance telephone company into a broadband internet access and local

45

Notwithstanding these achievements, AT&T experienced major missteps. Employee turnover became a big problem,

especially among senior managers. Armstrong also bought Telecommunications and MediaOne when valuations for cable-

television assets were near their peak. He paid about $106 billion in 2000, when they were worth about $80 billion. His failure

AT&T May Have Become Overwhelmed by the Rate of Change

What happened? Perhaps AT&T fell victim to the same problems many other acquisitive companies have. AT&T is a company

capable of exceptional vision but incapable of effective execution. Effective execution involves buying or building assets at a

reasonable cost. Its substantial overpayment for its cable acquisitions meant that it would be unable to earn the returns required

by investors in what they would consider a reasonable period. Moreover, Armstrong’s efforts to shift from the firm’s historical

business by buying into the cable-TV business through acquisition had saddled the firm with $62 billion in debt.

AT&T tried to do too much too quickly. New initiatives such as high-speed internet access and local telephone services

over cable-television network were too small to pick up the slack. Much time and energy seems to have gone into planning and

acquiring what were viewed as key building blocks to the strategy. However, there appears to have been insufficient focus and

Investors Lose Patience

Although all of these actions created a sense that grandiose change was imminent, investor patience was wearing thin.

Profitability foundered. The market share loss in its long-distance business accelerated. Although cash flow remained strong, it

was clear that a cash machine so dependent on the deteriorating long-distance telephone business soon could grind to a halt.

Investors’ loss of faith was manifested in the sharp decline in AT&T stock that occurred in 2000.

The 2000 Restructure: Correcting the Mistakes of the Past

Pushed by investor impatience and a growing realization that achieving AT&T’s vision would be more time and resource

consuming than originally believed, Armstrong announced on October 25, 2000 the breakup of the business for the fourth time.

46

The plan involved the creation of four new independent companies including AT&T Wireless, AT&T Consumer, AT&T

Broadband, and Liberty Media.

By breaking the company into specific segments, AT&T believed that individual units could operate more efficiently and

aggressively. AT&T’s consumer long-distance business would be able to enter the digital subscriber line (DSL) market. DSL is

a broadband technology based on the telephone wires that connect individual homes with the telephone network. AT&T’s

cable operations could continue to sell their own fast internet connections and compete directly against AT&T’s long-distance

The More Things Change The More They Stay The Same

On July 10, 2001, AT&T Wireless Services became an independent company, in accordance with plans announced during the

2000 restructure program. AT&T Wireless became a separate company when AT&T converted the tracking shares of the

mobile-phone business into common stock and split-off the unit from the parent. AT&T encouraged shareholders to exchange

their AT&T common shares for Wireless common shares by offering AT&T shareholders 1.176 Wireless shares for each share

of AT&T common. The exchange ratio represented a 6.5 percent premium over AT&T’s current common share price. AT&T

Wireless shares have fallen 44 percent since AT&T first sold the tracking stock in April 2000. On August 10, 2001, AT&T

spun off Liberty Media.

1. What were the primary factors contributing to AT&T’s numerous restructuring efforts since 1984? How did they

differ? How were they similar?

Answer: Between 1984 and 2000, AT&T experienced four major restructurings, of which three were voluntary and

one involuntary. Each was undertaken for a different reason. The first restructuring was mandated by the government

in 1984, while the second in 1996 was undertaken to eliminate conflicts between customers of its equipment business

2. Why do you believe that AT&T chose to split-off its wireless operations rather than to divest the unit? What might

you have done differently?

Answer: On the surface, it may seem that a divestiture or carve-out would generally be preferable to a split–off. Unlike

a split-off, a divestiture or carve-out generates a cash infusion to the firm, which can either be reinvested or paid to

47

3. Was AT&T proactive or reactive in initiating its 2000 restructuring program? Explain your answer.

Answer: Investors never seemed to share fully Armstrong’s vision for the company articulated in 1998. It is unclear

if given more time the firm would have been able to make it work. What is clear is that investors demonstrated their

4. AT&T overpaid for many of its largest acquisitions made during the 1990s? How might this have contributed to its

subsequent restructuring efforts?

Answer: The case indicates that AT&T built its cable empire when prices for such businesses were at their peak.

Armstrong was willing to pay an excessive premium for the cable companies he acquired because of his great faith

5. To what extent did AT&T’s ineffectual restructuring reflect factors beyond their control and to what extent was it

poor implementation?

Answer:

Beyond their control: The landline business eroded faster than expected, they were confronted by the 2000 recession,

and the Internet bubble made it more difficult to grow the broadband business.

6. What challenges did AT&T face in trying to split-up the company in 2000? What might you have done differently to

overcome these obstacles?

Answer: The firm was immediately confronted with the challenges of reconciling the competing interests of the four

businesses that were to be created following the restructure. Both AT&T Wireless and AT&T Business Services

Viacom to Spin Off Blockbuster

After months of trying to sell its 81% stake in Blockbuster Inc. undertook a tax-free spin-off in mid 2004. Viacom shareholders

will have the option to swap their Viacom shares for Blockbuster shares and a special cash payout. Blockbuster had been hurt

by competition from low-priced rivals and the erosion of video rentals by accelerating DVD sales. Despite Blockbuster’s

steady contribution to Viacom’s overall cash flow, Viacom believed that the growth prospects for the unit were severely

48

limited. In preparation for the spin-off, Viacom had reported a $1.3 billion charge to earnings in the fourth quarter of 2003 in

writing down goodwill associated with its acquisition of Blockbuster. By spinning off Blockbuster, Viacom Chairman and

ECO Sumner Redstone statd that the firm would now be able to focus on its core TV (i.e., CBS and MTV) and movie (i.e.,

Paramount Studios) businesses. Blockbuster shares fell by 4% and Viacom shares rose by 1% on the day of the announcement.

Discussion Questions:

1. Why would Viacom choose to spin-off rather than divest its Blockbuster unit? Explain your answer.

Answer: With the emergence of online movies on demand, the demand for rentals is rapidly falling.

2. In your opinion, why did Viacom and Blockbuster share prices react the way they did to the announcement of the

spin-off?

Answer: Viacom investors saw Blockbuster as a management distraction from its core entertainment businesses. The

Baxter to Spin Off Heart Care Unit

Baxter International Inc. announced in late 1999 its intention to spin off its underperforming cardiovascular business, creating a

new company that will specialize in treatments for heart disease. The new company will have 6000 employees worldwide and

annual revenue in excess of $1 billion. The unit sells biological heart valves harvested from pigs and cows, catheters and other

products used to monitor hearts during surgery, and heart-assist devices for patients awaiting surgery. Baxter conceded that

they have been ‘‘optimizing’’ the cardiovascular business by not making the necessary investments to grow the business. In

contrast, the unit’s primary competitors, Guidant, Medtronic, and Boston Scientific, are spending more on research and

investing more on start-up companies that are developing new technologies than is Baxter.

With the spin-off, the new company will have the financial resources that formerly had been siphoned off by the parent, to

create an environment that will more directly encourage the speed and innovation necessary to compete effectively in this

industry. The unit’s stock will be used to provide additional incentive for key employees and to serve as a means of making

future acquisitions of companies necessary to extend the unit’s product offering.

Discussion Questions

1. In your judgment, what did Baxter’s management mean when they admitted that they had not been “optimizing” the

cardiovascular business in recent years? Explain both the strategic and financial implications of this strategy.

Answer: Baxter’s management had not been investing adequately in the cardiovascular business to enable it to remain

2. Discuss some of the reasons why you believe the unit may prosper more as an independent operation than as part of

Baxter?

Answer: As an independent entity, the unit is likely to be able to be more competitive as its board and management

Gillette Announces Divestiture Plans

49

With 1998 sales of $10.1 billion, Gillette is the world leader in the production of razor blades, razors, and shaving cream.

Gillette also has a leading position in the production of pens and other writing instruments. Gillette’s consolidated operating

performance during 1999 depended on its core razor blade and razor, Duracell battery, and oral care businesses. Reflecting

disappointment in the performance of certain operating units, Gillette’s CEO, Michael Hawley, announced in October 1999 his

intention to divest poorly performing businesses unless he could be convinced by early 2000 that they could be turned around.

The businesses under consideration at that time comprised about 15% of the company’s $10 billion in annual sales. Hawley

saw the new focus of the company to be in razor blades, batteries, and oral care. To achieve this new focus, Hawley intended to

prune the firm’s product portfolio. The most likely targets for divestiture at the time included pens (i.e., PaperMate, Parker, and

Waterman), with the prospects for operating performance for these units considered dismal. Other units under consideration for

divestiture included Braun and toiletries. With respect to these businesses, Hawley apparently intended to be selective. At

Braun, where overall operating profits plunged 43% in the first three quarters of 1999, Hawley has announced that Gillette will

keep electric shavers and electric toothbrushes. However, the household and personal care appliance units are likely divestiture

candidates. The timing of these sales may be poor. A decision to sell Braun at this time would compete against Black &

Decker’s recently announced decision to sell its appliance business.

Although Gillette would be smaller, the firm believes that its margins will improve and that its earnings growth will be more

rapid. Moreover, divesting such problem businesses as pens and appliances would let management focus on the units whose

prospects are the brightest. These are businesses that Gillette’s previous management was simply not willing to sell because of

their perceived high potential.

Discussion Questions:

1. Which of the major restructuring motives discussed in this chapter seem to be a work in this business case? Explain

your answer.

Answer: Gillette was motivated by a desire to strategically realign its core businesses to areas believed more rapidly

1. Describe the process Gillette’s management may have gone through to determine which business units to sell and

which to keep.

Answer: Gillette evaluated each business in its portfolio as a standalone entity. Cash flows projected for each unit

2. Comment on the timing of the sale.

United Parcel Service Goes Public in an Equity IPO

On November 10, 1999, United Parcel Service (UPS) raised $5.47 billion by selling 109.4 million shares of Class B common

stock at an offering price of $50 per share in the biggest IPO by any U.S. firm in history. The share price exploded to $67.38 at

the end of the first day of trading. The IPO represented 9% of the firm’s stock and established the firm’s total market value at

$81.9 billion (i.e., [$67.38 x 109.4 / .09]). With 1998 revenue of $24.8 billion, UPS transports more than 3 billion parcels and

documents annually. The company provides services in more than 200 countries.

By issuing only a portion of its Class B stock to the public, UPS was interested in ensuring that control would remain in the

hands of current management. The cash proceeds of the stock issue were used to buy back about 9% of the Class A voting

50

Discussion Questions:

1. Describe the motivation for UPS to undertake this type of transaction.

Answer: The IPO was undertaken to raise cash, value the business, create a liquid market for employees to sell their

Hewlett Packard Spins Out Its Agilent Unit in a Staged Transaction

Hewlett Packard (HP) announced the spin-off of its Agilent Technologies unit to focus on its main business of computers and

printers, where sales have been lagging behind such competitors as Sun Microsystems. Agilent makes test, measurement, and

monitoring instruments; semiconductors; and optical components. It also supplies patient-monitoring and ultrasound-imaging

equipment to the health care industry. HP will retain an 85% stake in the company. The cash raised through the 15% equity

carve-out will be paid to HP as a dividend from the subsidiary to the parent. Hewlett Packard will provide Agilent with $983

million in start-up funding. HP retained a controlling interest until mid-2000, when it spun-off the rest of its shares in Agilent

to HP shareholders as a tax-free transaction.

Case Study Discussion Questions

1. Discuss the reasons why HP may have chosen a staged transaction rather than an outright divestiture of the business.

2. Discuss the conditions under which this spin-off would constitute a tax-free transaction.

Answer: The parent firm must have a controlling interest in the subsidiary prior to its being spun-off and after the

spin-off both the parent and the subsidiary must remain in the same line of business in which each was involved for at

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the

firm into two pieces. After experiencing a sharp “boom/bust” cycle throughout the 1970s, U.S. Steel had acquired Marathon

Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had

shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for

both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create “pure plays” in its primary businesses—

51

:

Discussion Questions:

1. Why do you believe U.S. Steel may have decided to acquire Marathon Oil? Does this combination make economic

sense? Explain your answer.

Answer: U.S. Steel acquired Marathon Oil in an effort to smooth out the business cycle in steel. Such diversification

2. Why do you think USX issued separate tracking stocks for its oil and steel businesses?

3. Why do you believe USX shareholders were not content to continue to hold tracking stocks in Marathon Oil and U.S.

Steel?

4. In your judgment, did the breakup of USX into Marathon Oil and United States Steel

Corporation make sense? Why or why not?

Answer: The break-up/spin-off made sense to Marathon shareholders since it eliminated the conflict in allocating

5. What other alternatives could USX have pursued to increase shareholder value? Why do you believe they pursued the

breakup strategy rather than some of the alternatives?

Answer:. USX could have sold the businesses separately or could have created equity carve-outs to value the

Hughes Corporation’s Dramatic Transformation

In one of the most dramatic redirections of corporate strategy in U.S. history, Hughes Corporation transformed itself from a

defense industry behemoth into the world’s largest digital information and communications company. Once California’s largest

manufacturing employer, Hughes Corporation built spacecraft, the world’s first working laser, communications satellites, radar

To accomplish this transformation, Hughes divested its communications satellite businesses and its auto electronics

operation. The corporate overhaul created a firm focused on direct-to-home satellite broadcasting with its DirecTV service

offering. DirecTV’s introduction to nearly 12 million U.S. homes was a technology made possible by U.S. military spending

52

For the next several years, Hughes attempted to find profitable niches in the rapidly consolidating U.S. defense contracting

industry. Hughes acquired General Dynamics’ missile business and made 15 smaller defense-related acquisitions. Eventually,

Hughes’ parent firm, General Motors, lost enthusiasm for additional investment in defense-related businesses. GM decided that,

if Hughes could not participate in the shrinking defense industry, there was no reason to retain any interests in the industry at

Hughes’ telecommunications unit was its smallest operation but, with DirecTV, its fastest growing. The transformation was

to exact a huge cultural toll on Hughes’ employees, most of whom had spent their careers dealing with the U.S. Department of

Defense. Hughes moved to hire people aggressively from the cable and broadcast businesses. By the late 1990s, former

Hughes’ employees constituted only 15–20 percent of DirecTV’s total employees.

Restructuring continued through the end of the 1990s. In 2000, Hughes sold its satellite manufacturing operations to Boeing

for $3.75 billion. This eliminated the last component of the old Hughes and cut its workforce in half. In December 2000,

Hughes paid about $180 million for Telocity, a firm that provides digital subscriber line service through phone lines. This

acquisition allowed Hughes to provide high-speed Internet connections through its existing satellite service, mainly in more

Case Study Discussion Questions:

1. How did changes in Hughes’ external environment contribute to its dramatic 20-year restructuring effort? Cite

specific influences in answering this question. (Hint: Consider some of the motivations discussed in this chapter for

engaging in restructuring activities.). Cite examples of how Hughes took advantage of their core competencies in

pursuing other alternatives?

Answer: With the reduction in defense spending, U.S. defense contractors facing increasing competition in a shrinking

market. Pricing pressures limited the ability to pass along increasing costs in what is a high fixed cost industry.

2. Why did Hughes’ board and management seem to rely heavily on divestitures rather than other restructuring

strategies discussed in this chapter to achieve the radical transformation of the firm? Be specific.

Answer: Hughes exited many of its mature, slow growing businesses. However, such units often generate significant

3. What risks did Hughes face in moving completely away from its core defense business and into a high-technology

commercial business? In your judgment, did Hughes move too quickly or too slowly? Explain your answer.

Answer: Hughes’ workforce and corporate culture had historically been focused on the space and defense industry.

The firm was accustomed to dealing with a relatively few customers who were not particularly price sensitive.

53

4. Why did Hughes move so aggressively to hire employees from the cable TV and broadcast industry?

Answer: Hughes recognized that they would be penalized competitively if they continued to rely on employees

5. Speculate as to why News Corp, a major entertainment industry content provider, might have been interested in

acquiring Hughes. Be specific.