Chapter 17: Alternative Exit and Restructuring Strategies

Divestitures, Spin-Offs, Carve-Outs, Split-Ups, and Split-Offs

Answers to End of Chapter Discussion Questions

16.1 What are the advantages and disadvantages of tracking or target stocks to investors and to the firm?

Answer: The purpose in creating tracking stock is to enable the financial markets to value the different operations

within a corporation based on their own performance. Tracking or targeted stocks provide the parent company with an

alternative means of raising capital for a specific operation by selling a portion of the stock to the public and an

16.2 How would you decide when to sell a business?

Answer: Many corporations review their business portfolio periodically to determine which operations continue to fit

their core strategies. Changes in the parent’s strategy or a desire to achieve a more focused business portfolio can

result in certain operations becoming strategically redundant. Such operations become prime candidates for

divestiture. Even if a business ‘‘fits’’ within the parent corporation’s current strategy, the business may not be earning

16.3 What factors influence a parent firm’s decision to undertake a spin-off rather than a divestiture or equity carve-out?

Answer: The decision as to which of these three strategies to use is often heavily influenced by the parent firm’s need

for cash, the degree of synergy between the business to be divested or spun-off and the parent’s other operating units,

16.4 How might the form of payment affect the abnormal return to sellers and buyers?

Answer: Abnormal returns to sellers are much smaller when the seller receives cash rather than buyer equity. Asset

for buyer equity sales generate excess returns of about 10 percent for buyers and 3 percent for sellers. The higher

2

16.5 How might spin-offs result in a wealth transfer from bondholders to shareholders?

Answer: There is evidence that spin-offs transfer wealth from bondholders to stockholders for several reasons. First,

16.6 Explain how executing successfully a large-scale divestiture can be highly complex. This is especially true when the

divested unit is integrated with the parent’s functional departments and with other units operated by the parent.

Consider the challenges of interdependencies, regulatory requirements, and customer and employee perceptions.

Answer: In many instances, units within larger organizations share resources such as human resources, accounting,

tax, public relations, data centers, and other functions which are often centralized at the parent level. An effort must be

made to reassign individuals from these functions to the unit to be divested. In other instances, the parent may

In addition, units within the parent may supply to or receive from the divested unit certain products and services. As

part of the agreement of purchase and sale, these relationships are often continued well beyond closing. Regulatory

submissions are often required by both parties. For tax purposes, both parties must account for the transaction in the

same way in terms of how the purchase price will be allocated. Employees must be notified well in advance of

16.7 On April 25, 2001, in an effort to increase shareholder value, USX announced its intention to split U.S. Steel and

Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity

to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX–U.S. Steel Group

common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel

Corporation. What other alternatives could USX have pursued to increase shareholder value? Why do you believe

they pursued the breakup strategy rather than some of the alternatives?

Answer: USX could have sold the businesses separately or could have created equity carve-outs to value the

16.8 Hewlett Packard (HP) announced the spin-off of its Agilent Technologies unit to focus on its main business of

computers and printers. Hewlett Packard provided Agilent with $983 million in start-up funding. HP retained a

controlling interest until mid-2000, when it spun-off the rest of its shares in Agilent to HP shareholders as a tax-free

transaction. Discuss the reasons why HP may have chosen a staged transaction rather than an outright divestiture of

the business.

Answer: The first stage was undertaken in the form of an equity carve-out to value the business, perhaps with the

intent on selling it if it could be priced attractively, and to raise cash. Based on the results of the first stage, HP

3

16.9 After months of trying to sell its 81 percent stake in Blockbuster Inc., Viacom undertook a spin-off in mid 2004. Why

would Viacom choose to spin-off rather than divest its Blockbuster unit? Explain your answer.

Answer: With the emergence of online movies on demand, the demand for rentals is rapidly falling. There may

have been few buyers for the business. Moreover, Blockbuster’s financial performance may have suffered if the

16.10 Since 2001, GE, the world’s largest conglomerate, had been underperforming the S&P 500 stock index. In late 2008,

the firm announced that it was considering spinning off its consumer and industrial unit. What do you believe are

GE’s motives for their proposed restructuring? Why do you believe they chose a spin-off rather than an alternative

restructuring strategy?

Answer: GE’s long-term underperformance had disappointed stockholders for years. They were under pressure to

restructure to enhance market value by streamlining the firm and achieving better focus in potentially higher growth

Solutions to End of Chapter Case Questions

Gardner Denver and Ingersoll Rand’s Industrial Segment

Merge in a Reverse Morris Trust Deal

Discussion Questions and Solutions:

1. The merger of Gardner Denver and Ingersoll Rand’s IndustrialCo segment could have been achieved as a result of a split-off

of IndustrialCo. Explain the details of how this might happen.

Answer: By creating a wholly-owned shell subsidiary, Ingersoll could have implemented a split-off transaction which would

have involved an offer to its shareholders to exchange their Ingersoll shares for shares in IndustrialCo. Any IndustrialCo

2. Speculate as to why Ingersoll chose a spin-off rather than a split-off of IndustrialCo as part its plan to merge Gardner with

IndustrialCo. Be specific.

Answer: Ingersoll chose a spin-off rather than split-off even though the split-off would have reduced the number of parent

shares outstanding and for an unchanged level of earnings would increase earnings per share. The spin-off is a simpler

3. What are the Morris Trust tax regulations? How did they affect how this deal was structured? Why was the final ownership

distribution important?

Answer: The U.S. Tax Code restricts how certain types of corporate transactions can be structured to avoid taxes. Specifically,

split-offs or spin-offs implemented as part of a merger must be structured to satisfy Morris Trust tax code rules if the

transaction is to be deemed tax-free. The IRS’ concern is that a split-off or spin-off of a wholly-owned parent subsidiary is

4

4. How is value created for the Gardner and Ingersoll shareholders in this type of a transaction?

Answer: Ingersoll Rand pre-merger was a highly diversified company. Empirical studies indicate that shareholders of focused

companies are more likely to see their investment appreciate than those of highly diversified firms. The spin-off of the

5. What are the advantages and disadvantages of a Reverse Morris Trust structure?

Answer: An advantage the Reverse Morris Trust is that it does not require approval by the parent shareholders for the spin-off

or merger. This is so because the spin-off firm is merging or combining with the merger partner and the parent approves this

6. Is KKR actually exiting its investment in Gardner? Explain your answer.

Answer: KKR is changing the nature of its investment. Rather than owning 100% of Gardner Denver, they now own 49.9% of

7. Speculate as to why the postmerger governance structure may have played a role in getting the parties to agree on a final

deal? Be specific.

Answer: All parties to the deal had to be motivated to reach agreement. This often involves giving senior managers and board

Examination Questions and Answers

True/False Questions: Answer True or False to the following questions:

1. Divestitures, spin-offs, equity carve-outs, split-ups, and bust-ups are commonly used strategies to exit businesses.

True or False

2. Empirical studies show that the desire by parent firms to increase strategic focus is an important motive for exiting

businesses. True or False

5

3. Antitrust regulatory agencies may make their approval of a merger contingent on the willingness of the merger

partners to divest certain businesses. True or False

4. In deciding to sell a business, a parent firm should compare the business’ after-tax value in sale with its pre-tax value

to the parent as part of the parent.

True or False

5. The timing of a divestiture is important. If the business to be sold is highly cyclical, the sale should be timed to

coincide with the firm’s peak year earnings. True or False

6. A spin-off is a transaction involving a separate legal entity whose shares are sold to the parent firm’s shareholders.

True or False

7. A spin-off is a transaction in which a parent creates a new legal subsidiary and distributes shares it owns in the

subsidiary to its current shareholders as a stock dividend. True or False

8. In a spin-off, the proportional ownership of shares in the new legal subsidiary is the same as the stockholders’

proportional ownership of shares in the parent firm. True or False

9. In a spin-off, the board of directors is the same as the board of directors of the parent firm. True or False

10. A split-up involves the creation of a new class of stock for each of the parent’s operating subsidiaries, paying current

shareholders a dividend of each new class of stock, and then dissolving the remaining corporate shell. True or False

11. Spin-offs are generally immediately taxable to shareholders. True or False

12. Both a divestiture and a spin-off generally generate a cash infusion for the parent. True or False

13. Equity carve-outs have some of the characteristics of both divestitures and spin-offs. True or False

14. The parent firm generally retains control of the business involved in an equity carve-out. True or False

15. An equity carve-out is often a prelude to a complete divestiture of a business by the parent. True or False

16. Although the parent often retains control in an equity carve-out, the shareholder base of the subsidiary may be

different that that of the parent. True or False

17. In an equity carve-out, the cash raised by the subsidiary in this manner may be transferred to the parent as a dividend

or as an inter-company loan. True or False

18. When a parent creates a tracking stock for a subsidiary, it is giving up all control of that subsidiary. True or False

19. Tracking stocks are often created to give investors a pure play investment opportunity in one of the parent’s

subsidiaries. True or False

20. Tracking stocks may create internal operating conflicts among the parent’s business units in terms of how the

consolidated firm’s cash is allocated among its business units. True or False

21. Voluntary bust-ups or liquidations by the parent firm reflect management’s judgment that the sale of individual parts

of the firm could realize greater value than the value created by a continuation of the combined corporation. True or

False

22. In general, a voluntary bust-up or liquidation has the advantage over mergers of deferring the recognition of a gain by

the stockholders of the selling company until they eventually sell the stock. True or False

23. When a firm is unable to pay its liabilities as they come due, it is said to be in bankruptcy. True or False

24. Equity carve-outs are similar to divestitures and spin-offs in that they provide a cash infusion to the parent. True or

False

25. The divesting firm is required to recognize a gain or loss for financial reporting purposes equal to the difference

between the book value of the consideration received for the divested operation and its fair value. True or False

26. In a private solicitation, the parent firm may hire an investment banker or undertake on its own to identify potential

buyers to be contacted. True or False

27. A parent firm’s decision to sell or to retain a subsidiary is often made by comparing the after-tax equity value of the

subsidiary with the pre-tax and interest sale value of the business. True or False

28. A parent firm rarely chooses to divest an undervalued business and return the cash to shareholders either through a

liquidating dividend or share repurchase. True or False

29. The divestiture of a business always results in the parent receiving cash from the buyer? True or False

30. Management may sell assets to fund diversification opportunities? True or False

31. Many corporations, particularly large, highly diversified organizations, constantly are reviewing ways in which they

can enhance shareholder value by changing the composition of their assets, liabilities, equity, and operations. True or

False

32. Divestitures, spin-offs, equity carve-outs, split-ups, split-offs, and bust-ups are commonly used strategies to exit

businesses and to redeploy corporate assets by returning cash or noncash assets through a special dividend to

shareholders. True or False

33. Managing highly diverse and complex portfolios of businesses is both time consuming and distracting. This is

particularly true when the businesses are in largely related industries. True or False

34. A business that is rich in high-growth opportunities may be an excellent candidate for divestiture to a strategic buyer

with significant cash resources and limited growth opportunities. True or False

35. A substantial body of evidence indicates that increasing a firm’s degree of diversification can improve substantially

financial returns to shareholders. True or False

36. Empirical studies show that exit strategies, which return cash to shareholders, tend to have a highly unfavorable

impact on shareholder wealth creation. True or False

37. Acquiring companies often find themselves with certain assets and operations of the acquired company that do not fit

their primary strategy. Such assets may be divested to fund future investments. True of False

38. Divestitures always result in the parent receiving stock or debt from the buyer. True or False

39. The decision to sell or to retain the business depends on a comparison of the pre-tax value of the business to the parent

with the after-tax proceeds from the sale of the business. True or False

40. Although the sale value may exceed the equity value of the business, the parent may choose to retain the business for

strategic reasons. True or False

41. In a public solicitation, a firm can announce publicly that it is putting itself, a subsidiary, or a product line up for sale.

Either potential buyers contact the seller or the seller actively solicits bids from potential buyers or both. True or

False

42. In either a public or private solicitation, interested parties are asked to sign confidentiality agreements after they are

given access to proprietary information but before they are asked to make a bid. True or False

43. The divesting firm is required to recognize a gain or loss for financial reporting purposes equal to the difference

between the fair value of the consideration received for the divested operation and its market value. True or False

44. In a spin-off, some shareholders receive proportionately more shares than others. True or False

45. Like divestitures or equity carve-outs, the spin-off generally results in an infusion of cash to the parent company.

True or False

46. A split-up involves carving out a portion of the equity of each of the parent’s operating subsidiaries and selling the

shares to the public. True or False

47. Parent firms with a high tax basis in a business may choose to spin-off the unit as a tax-free distribution to

shareholders rather than sell the business and incur a substantial tax liability. True or False

8

48. Split-ups and spin-offs generally are taxable to shareholders. True or False

49. For financial reporting purposes, the parent firm should account for the spin-off of a subsidiary’s stock to its

shareholders at book value with no gain or loss recognized, other than any reduction in value due to impairment. True

or False

50. In an equity carve-out, minority shareholders are eliminated. True or False

51. Although the parent retains control, the shareholder base of the subsidiary that has undergone an equity carve-out is

unlikely to be different than that of the parent as a result of the public sale of equity. True or False

52. In addition, stock-based incentive programs to attract and retain key managers can be implemented for each operation

with its own tracking stock. True or False

53. For financial reporting purposes, a distribution of tracking stock splits the parent firm’s equity structure into separate

classes of stock without a legal split-up of the firm. True or False

54. Unlike a spin-off or carve-out, the parent retains complete ownership of the business for which it has created a

tracking stock. True or False

55. A disadvantage of a split-off is that they tend to increase the pressure on the spun-off firm’s share price, because

shareholders who exchange their stock are more likely to sell the new stock. True or False

56. Equity ownership changes in spin-offs, but it does not change in split-ups. True or False

57. The reasons for selecting a divestiture, carve-out, or spin-off strategy are basically the same. True or False

58. A spin-off is tax free to the shareholders if it is properly structured. In contrast, the cash proceeds from an outright sale

may be taxable to the parent to the extent a gain is realized. True or False

59. Restructuring actions may provide tax benefits that cannot be realized without undertaking a restructuring of the

business. True or False

60. Parent firms often exit businesses that consistently fail to meet or exceed the parent’s hurdle rate requirements. True

or False

61. Divestitures are always taxable to the selling firm? True or False

Multiple Choice Questions: Answer only one alternative for each question.

1. Which of the following is generally considered a motive for exiting businesses?

a. Changing corporate strategy or focus

b. Underperforming businesses

c. Regulatory concerns

d. Lack of fit

e. All of the above

2. To decide if a business is worth more to the shareholder if sold, the parent firm generally considers all of the

following factors except for

a. The after-tax cash flows of the business to be sold

b. The after-tax sale value of the business to be sold

c. The parent’s cost of capital

d. A and B

e. A, B, and C

3. Which of the following is not a characteristic of a spin-off?

a. The parent creates a new legal subsidiary for the business to be spun-off

b. The shares of the new subsidiary are sold to the public

c. The ownership of shares in the new legal subsidiary is the same as the stockholders’ proportional ownership

of shares in the parent firm

d. The new business once spun-off has its own management and board

e. Spin-offs are generally not taxable to the parent’s shareholders if properly structured

4. A spin-off may create shareholder wealth for all of the following reasons except for

a. Spin-offs are generally not taxable if properly structured

b. The spin-off’s management and board is independent of the former parent

c. Investors will be better able to value the spin-off

d. The cost of capital of the spin-off is generally higher than when it was part of the parent

e. The spin-off may be subsequently acquired by another firm

5. An equity carve-out differs from a spin-off for all but which one of the following reasons?

a. Generates a cash infusion into the parent

b. Is undertaken when the unit has very little synergy with the parent

c. The proceeds often are taxable to the parent

d. Continues to be influenced by the parent’s management and board

e. The carve-out’s shareholders may differ from those of the parent’s shareholders

6. Which one of the following is generally not a reason for issuing tracking stocks?

a. To give investors a “pure play” in a specific business owned by the parent

b. To create a currency for the business to acquire other firms

c. To enhance the likelihood that the business will be acquired

d. To create an incentive for management receiving the stock

e. To raise capital for the parent or for the business for which the tracking stock is created

7. For a spin-off to be tax-free to the shareholder it must satisfy which of the following:

a. The parent firm must have a controlling interest in the subsidiary before it is spun off.

b. After the spin-off, both the parent and the subsidiary must remain in the same line of business in which each

was involved for at least 5 years before the spin-off.

c. The spin-off cannot have been used as a means of avoiding dividend taxation by converting ordinary income

into capital gains.

d. The parent’s shareholders must maintain significant ownership in both the parent and the subsidiary

following the transactions.

e. All of the above

10

8. Which of the following is not true of a divestiture?

a. May create cash infusion for the parent firm

b. Parent ceases to exist

c. Proceeds of sale taxable if returned to shareholders through a dividend or stock buyback

d. A new legal subsidiary may be created

e. B and C

9. Which of the following is not true of a spin-off?

a. Creates cash infusion for parent

b. Change in equity ownership of the spin-off

c. New legal entity created

d. New shares issued to the public

e. A, B, and D

10. Which of the following is not true of an equity carve-out?

a. Creates cash infusion for the parent

b. Change in equity ownership of the unit involved in the carve-out

c. New shares issued to the public

d. Taxable if proceeds returned to shareholders through a dividend or stock buyback

e. Parent ceases to exist

11. Which of the following is true about a voluntary bust-up?

a. Parent ceases to exist

b. Cash infusion to the parent

c. Parent stock is exchanged for subsidiary stock

d. New shares issued to the public

e. Parent remains in control

12. Which of the following is generally not considered a common motive for exiting businesses?

a. Changing strategy or focus

b. Desire to achieve economies of scale

c. Lack of fit with the parent’s other businesses

d. Discarding unwanted businesses from prior acquisitions

e. All of the above

13. An equity carve-out by a parent of one of its subsidiaries is often a precursor to a

a. Complete divestiture or spin-off of the subsidiary

b. An acquisition

c. A merger

d. Joint venture

e. The creation of a tracking stock

14. Which of the following is a common problem associated with tracking stocks?

a. Tracking stocks often de-motivate managers of the business for which the stock is created

b. Such stocks are too complicated for investors to understand

c. Tracking stocks may create internal operating conflicts among the parent’s business units

d. Such stocks often create huge tax liabilities for the parent

e. None of the above

15. Which of the following is not true of a split-off?

a. A split-off is a variation of a spin-off

11

b. Parent company shareholders receive shares in a subsidiary in return for surrendering their parent company

shares

c. Split-offs are best suited for disposing of a less than 100 percent investment stake in a subsidiary,

d. A split-off reduces the parent firm’s earnings per share.

e. The split-off reduces the pressure on the spun-off firm’s share price

16. A diversified automotive parts supplier has decided to sell its valve manufacturing business. This sale is referred to as

a

a. Merger

b. Divestiture

c. Spin-off

d. Equity carveout

e. Liquidation

17. As part of its restructuring plan, a holding company plans to undertake an IPO for 35 percent of the shares it owns in a

subsidiary. The sale of these shares would be called a

a. Divestiture

b. Split-off

c. Split-up

d. Equity carveout

e. Breakup

18. A firm decides to distribute all of the shares it holds in a subsidiary to its shareholders. The distribution would be

called a

a. Divestiture

b. Split-up

c. Spin-off

d. Split-up

e. Equity carveout

19. The board of directors of a large conglomerate has decided that the investment opportunities for the firm are limited

and that greater value could be created for the shareholders if the firm were divided into four independent businesses.

Following approval by shareholders, the firm executed this strategy which is best described as a

a. Split-up

b. Split-off

c. Spin-off

d. Equity carveout

e. Reverse merger

20. The board of directors of a firm approves an exchange offer in which their shareholders are offered stock in one of the

firm’s subsidiaries in exchange for their holdings of parent company stock. This offer is best described as a

a. Split-up

b. Split-off

c. Equity carve-out

d. Spin-off

e. Tender offer

Case Study Short Essay Examination Questions

CBS Corporation and Entercom Merge

in a Reverse Morris Trust Deal

12

______________________________________________________________________________

Key Points:

• Greater shareholder value may be created by exiting rather than operating a business.

• How? By increasing the focus of the parent firm exiting the business.

• The deal structure also can create shareholder value.

_____________________________________________________________________________

In early 2016, CBS Inc. (CBS) considered “strategic options” for its radio business, CBS Radio. The unit’s operating

performance had been deteriorating in recent years due to declining ad revenues and profit pressures due to internet

competition. While radio reaches more Americans than any other medium and offers advertisers the ability to target local

markets, CBS Radio simply did not have the geographic coverage and content to achieve sustained profitability.

It was no secret that CBS wanted any deal for its radio operations to be tax-free. A Reverse Morris Trust is a tax-

optimization strategy in which a company wishing to spin off and subsequently sell assets (CBS) to another party (Entercom)

can do so and avoid taxes on any gains that would have been incurred had the assets been sold outright. The deal if properly

structured would also be tax-free to CBS shareholders. The Reverse Morris Trust acquisition combines a divisive

reorganization (e.g., a spin-off or split-off) with an acquisitive reorganization (e.g., a statutory merger) to allow a tax-free

transfer of a subsidiary.2

The deal would create the largest U.S. radio network consisting of 244 stations, including 23 of the 25 top markets. The

combined firms will have the rights to broadcast 45 professional sports teams, a leadership position in news and talk formats, a

diverse array of music and entertainment formats, a growing portfolio of digital content, and the ability to distribute dozens of

major market radio shows across multiple media platforms.3 The merger also allows the combined firms to achieve the scale

necessary to achieve the cost savings through the elimination of duplicate functions to compete profitably with other media.

On a proforma basis, the combined firms will have $1.7 billion in annual revenue, making it the second largest radio station

owner in the U.S., and an annual EBITDA of almost $500 million, including an expected $25 million in annual cost savings

related synergies.

Entercom chairman Joe Field, the firm’s controlling shareholder, agreed to vote in favor of the transaction and

recommended that the other shareholders vote for the merger. The firm’s board unanimously approved the merger and related

agreements just prior to the deal’s public announcement. Progress in the deal was slowed by a “second request” for data by the

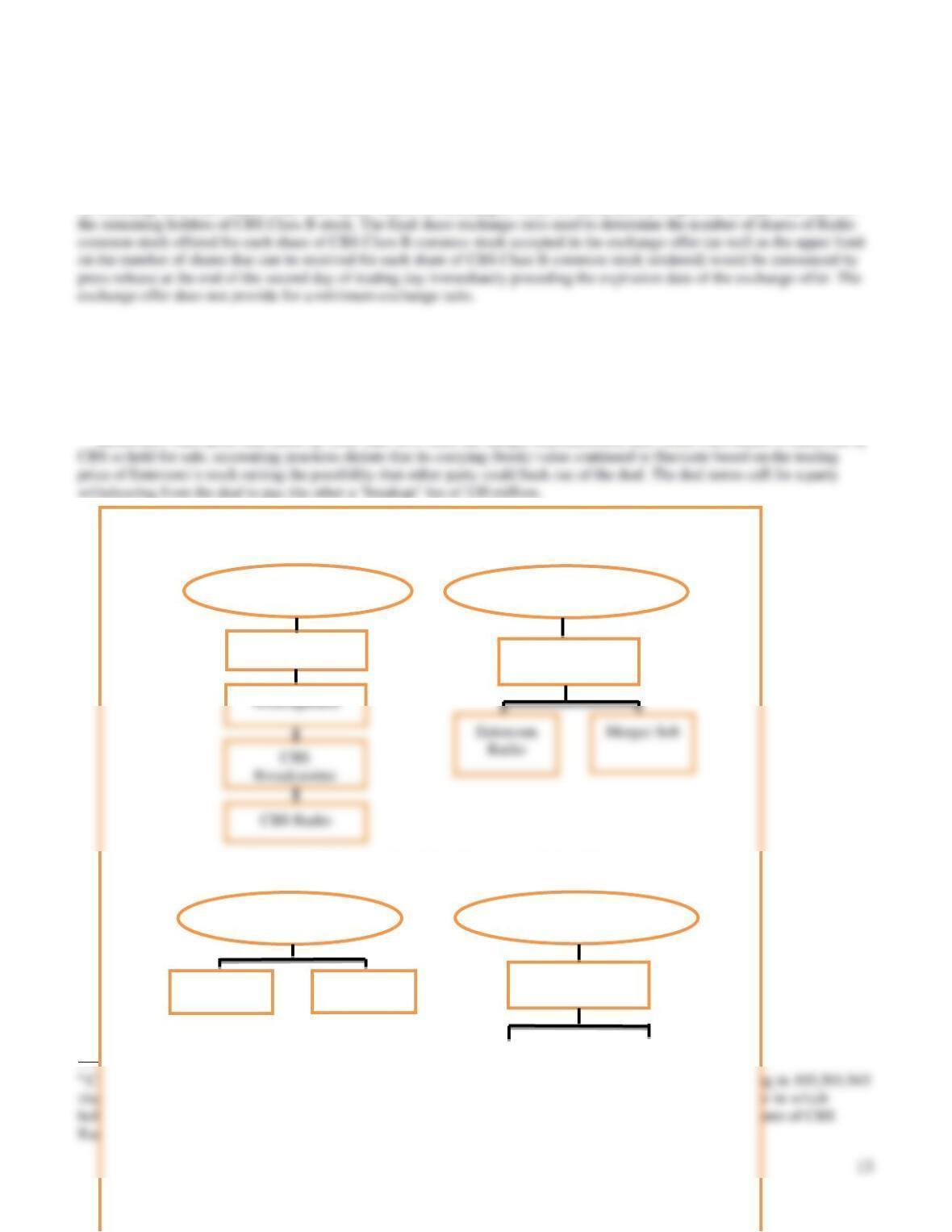

Justice Department. Figure 17.3 illustrates the three stages of the deal. These include the following: (1) the creation of the CBS

Radio subsidiary directly owned by CBS, (2) the exchange offer, and (3) the reverse merger of CBS Radio into Entercom’s

Merger Sub with CBS Radio surviving.

Prior to the exchange offer, Westinghouse directly owned 100% of CBS Broadcasting, and CBS Broadcasting directly

owned 100% of the equity of CBS Radio. As a result of an internal CBS reorganization, CBS Broadcasting would distribute all

of the outstanding equity of CBS Radio to Westinghouse, which then would distribute all of its equity in CBS Radio to CBS,

making CBS Radio a directly owned subsidiary of CBS. 4

In the exchange proposal, CBS shareholders could buy all, some, or none of the 105, 501, 945 CBS Radios shares offered

by tendering their CBS shares. Any CBS Radio shares not exchanged would be distributed in a spin-off on a pro rata basis to

Immediately following the final distribution (split-off plus any spin-off shares if necessary) of CBS Radio shares,

Entercom’s Merger Sub would merge with CBS Radio, with the latter surviving as a subsidiary of Entercom. Each share of

CBS Radio common would be converted into the right to receive one share of Entercom Class A common stock. Following the

merger, Entercom would contribute all the outstanding equity interests in Entercom Radio to CBS Radio such that Entercom

Radio would become a wholly owned subsidiary of CBS Radio.

Entercom’s share price had fallen by more than 40% since the merger announcement date. Since CBS Radio is classified by

CBS Shareholders

Entercom Shareholders

CBS

Entercom

Structure Before Final Distribution and Before Merger

Structure Following Final Distribution but Before Merger

CBS Shareholders

CBS

Entercom Shareholders

CBS Radio

Entercom

14

CBS Corporation and Entercom Merger in a Reverse Morris Trust Deal

Discussion Questions and Solutions:

1. The merger of CBS Radio and Entercom could have been achieved as a result of a CBS spin-off of CBS Radio. Explain the

details of how this might happen.

Answer: By creating a wholly-owned shell subsidiary, CBS could have distributed the shares to its shareholders as a dividend

2. Speculate as to why CBS chose to split-off rather than spin-off CBS Radio as part its plan to merge CBS Radio with

Entercom. Be specific.

Answer: CBS chose a split-off rather than spin-off even though either would have resulted in a tax-free transaction for its

3. What are the Morris Trust tax regulations? How did they affect how this deal was structured? Why was the final ownership

distribution important?

Answer: The U.S. Tax Code restricts how certain types of corporate transactions can be structured to avoid taxes. Specifically,

split-offs or spin-offs implemented as part of a merger must be structured to satisfy Morris Trust tax code rules if the

Entercom

Radio

Merger Sub

Structure Following Merger

Entercom

CBS Radio

Entercom

Radio

CBS

Figure 17.3. Structuring a Reverse Morris Trust Split-Off Transaction (Adapted from

SEC filings)

15

4. How is value created for the CBS and Entercom shareholders in this type of a transaction?

Answer: Ideally, the impact of taxes on investment decisions would be neutral, such that taxes would not impact how the free

market allocates capital. Resources would be transferred to those who can use them most efficiently, as they would be able to

offer the highest risk adjusted financial returns to attract investors.

CBS shareholders participating in the split-off would do so only if they believed the appreciation potential of the Entercom

5. What are the advantages and disadvantages of a Reverse Morris Trust structure?

Answer: An advantage the Reverse Morris Trust is that it does not require approval by the parent shareholders for the spin-off

or merger. This is so because the spin-off firm is merging or combining with the merger partner and the parent approves this

INSIDE M&A: MANAGING RISK THROUGH RESTRUCTURING

_____________________________________________________________________________________

Key Points

• Firms often restructure to realign their business focus or to exploit perceived future opportunities.

• The deals such firms make reflect their differing perceptions about the future.

• Like many things, timing is the critical factor determining success or failure.

______________________________________________________________________________

The comparative stability in global energy prices and diminishing cost cutting opportunities have encouraged consolidation

among large exploration and development companies. The need to achieve economies of scale to spread fixed costs and new

extraction technologies encourages additional industry mergers and acquisitions. The historical route of using business

alliances to defray the cost and associated risk of exploiting new oil and gas discoveries has given way to growth by acquiring

known energy fields.

16

resulting in the Danish conglomerate having a 3.76% stake in Total. In addition, Total will assume responsibility for $2.5

billion in Maersk Oil debt.

Total will assume control over Maersk Oil’s entire operation, including reserve portfolio, obligations, and rights. Denmark

will become the regional hub for all of Total’s operations in Denmark, Norway, and the Netherlands due to Maersk Oil’s strong

position in the North Sea. Maersk intends to issue a special dividend consisting of a portion of the Total shares it received as a

result of the sale of Maersk Oil.

On a per barrel basis, Total is paying $13.40 per barrel of reserves. This is consistent with what Royal Dutch Shell paid to

acquire competitor BG Group Plc in 2015. In undertaking this deal, Total is reducing its exposure to higher risk regions such as

Iran and Qatar and toward OECD regions. Total will be adding about one million barrels of output to its current two million

barrels pumped per day in the North Sea region. Total expects to realize $400 million in annual cost savings by combining its

GE RETURNS TO ITS INDUSTRIAL ROOTS

_____________________________________________________________________________________

Key Points

• Firms often restructure to realign their business focus

• Restructuring strategies can range from divestitures to spin-offs to split-offs of unwanted businesses

• Companies interested in divesting specific operating units often undertake “controlled auctions” to minimize

disruption to the business

______________________________________________________________________________

As part of GE’s strategy to focus the conglomerate on its industrial businesses, the firm announced in late 2015 that it had sold

the bulk of its private equity lending business to the Canada Pension Plan Investment Board (CPPIB) for $12 billion. Known

within GE as the Financial Sponsor Group (FSG), FSG finances leveraged buyouts. FSG consists of Antares Capital (a private

equity lender) and a $3 billion bank loan portfolio. The unit for years had been considered a “crown jewel” within GE’s

financial services business. Under the terms of the deal, Antares Capital will retain its name and operate as a standalone

business within CPPIB. The sale represents a substantial part of GE’s campaign to withdraw from its financial services arm

known as GE Capital.

GE had relied on profits generated by GE Capital for the bulk of its earnings growth for more than three decades. However,

since the financial crisis surrounding the 2007 – 2009 recession, which savaged the conglomerate’s profits, and the increase in

regulation of financial services firms, GE’s CEO Jeffrey Immelt has moved to restructure the firm. The goal was to create a

17

to buyout firms that are investing in midsize U.S. businesses. The pension fund has been increasingly active in private-equity

investing and ranks as one of the most aggressive private equity lenders today. As a pension fund, CPPIB is focused on

investments that generate steady returns over the long term to help fund its future pension obligations. The GE loan portfolio

aligns with that goal by providing it with a bigger source of recurring interest rate income from the outstanding loans, and

Antares Capital provides the infrastructure to increase substantially its origination of new loans.

The Anatomy of a Reverse Morris Trust Transaction—

The Coty Cosmetics Saga

______________________________________________________________________________

Key Points:

• Greater shareholder value may be created by exiting rather than operating a business.

• How? By increasing the focus of the parent firm exiting the business.

• How the deal is structured also can create shareholder value.

_____________________________________________________________________________

Consumer product giant Proctor & Gamble (P&G) agreed to sell its portfolio of 43 beauty brands to beauty products maker

Coty Inc. (Coty) for $12.5 billion on July 8, 2015. Included in the deal are professional salon and retail hair products like

Nice & Easy and VS Salonist, as well as cosmetics and fine fragrances from Gucci and Dolce & Gabbana. The deal is part of

P&G’s strategy to shed more than 100 brands and focus on 10 core product lines, like Tide, that tend to grow faster than the

beauty brands.

Coty, owned by European firm JAB Cosmetis B. V., sells fragrances, skin products and cosmetics from brands including

Calvin Klein, Marc Jacobs and Chloe. This transaction creates one of the world’s largest beauty products companies. Coty

hopes its global marketing and distribution network and widely recognized brand will reinvigorate growth for many of the

beauty products acquired from P&G.

Neither the split-off nor the spin-off creates an immediate tax liability for the firm’s shareholders, as any taxes owed

would be deferred until shareholders sold their shares in the newly created subsidiary. The new entity created by the split off

is immediately merged with a new wholly-owned merger subsidiary created by Coty. The Reverse Morris Trust acquisition

combines a divisive reorganization (e.g., a spin-off or split-off) with an acquisitive reorganization (e.g., a statutory merger) to

allow a tax-free transfer of a subsidiary under U.S. law. The use of a divisive reorganization results in the creation of a public

company which is subsequently merged into a shell subsidiary of another firm, with the shell surviving.

18

$25.79 per share (i.e., $10.6 billion/ Coty’s then share price = 411 million shares). The Coty share price was allowed to

fluctuate within a $22.06 and $27.06 collar based on the trading price of Coty’s stock prior to the close of the transaction.

The tax-efficient nature of the $12.5 billion offer maximizes value for P&G shareholders and minimizes annual earnings

dilution. P&G’s earnings per share will be impacted by two offsetting factors. The loss of the earnings per share associated

with the divested beauty brands will be more than offset on an annualized basis following the closing of the transaction

through a combination of P&G shares retired via the split-off and a reduction in overhead expenses associated with the P&G

subsidiary containing the divested brands.

Discussion Questions:

1. The merger of Coty and the P&G subsidiary RMT Brands could have been achieved as a result of a P&G spin-

off of RMT Brands. Explain the details of how this might have happened.

Answer: By creating a wholly-owned shell subsidiary, P&G could have distributed the shares to its

shareholders as a dividend prior to the unit merging with Coty. If properly structured, this would have

2. Speculate as to why P&G chose to split-off rather than spin-off RMT Brands as part its plan to merge RMT

Brands with Coty. Be specific.

Answer: P&G chose a split-off rather than spin-off even though either would have resulted in a tax-free

transaction for its shareholders, because the split-off reduced the number of parent shares outstanding and

3. What are the Morris Trust tax regulations? How did they affect how this deal was structured?

Answer: The U.S. Tax Code restricts how certain types of corporate transactions can be structured to avoid

taxes. Specifically, split-offs or spin-offs implemented as part of a merger must be structured to satisfy

Morris Trust tax code rules if the transaction is to be deemed tax free. The IRS’ concern is that a split-off or

spin-off of a wholly-owned parent subsidiary could be undertaken in which the transaction would be tax free

19

4. How is value created for the P&G and Coty shareholders in this type of transaction?

Answer: Ideally, the impact of taxes on investment decisions would be neutral, such that taxes would not

impact how the free market allocates capital. Resources would be transferred to those who can use them most

efficiently, as they would be able to offer the highest risk adjusted financial returns to attract investors.

P&G shareholders participating in the split-off would do so only if they believed the appreciation potential of

more in taxes than it would have paid if it had remained part of P&G.

5. Why is the percentage distribution of ownership in the newly created firm following closing important in a

Reverse Morris Trust transaction?

Answer: For the deal to satisfy such a transaction from a tax standpoint, the shareholders of the parent firm

6. What was the purpose of the collar arrangement used in this deal? How could it protect both P&G and Coty

shareholders?

Answer: Reverse Morris Trust split-off mergers are very complicated, often taking up to a year between

signing and closing of a deal. During this time the value of the deal based on a fixed exchange ratio could

20

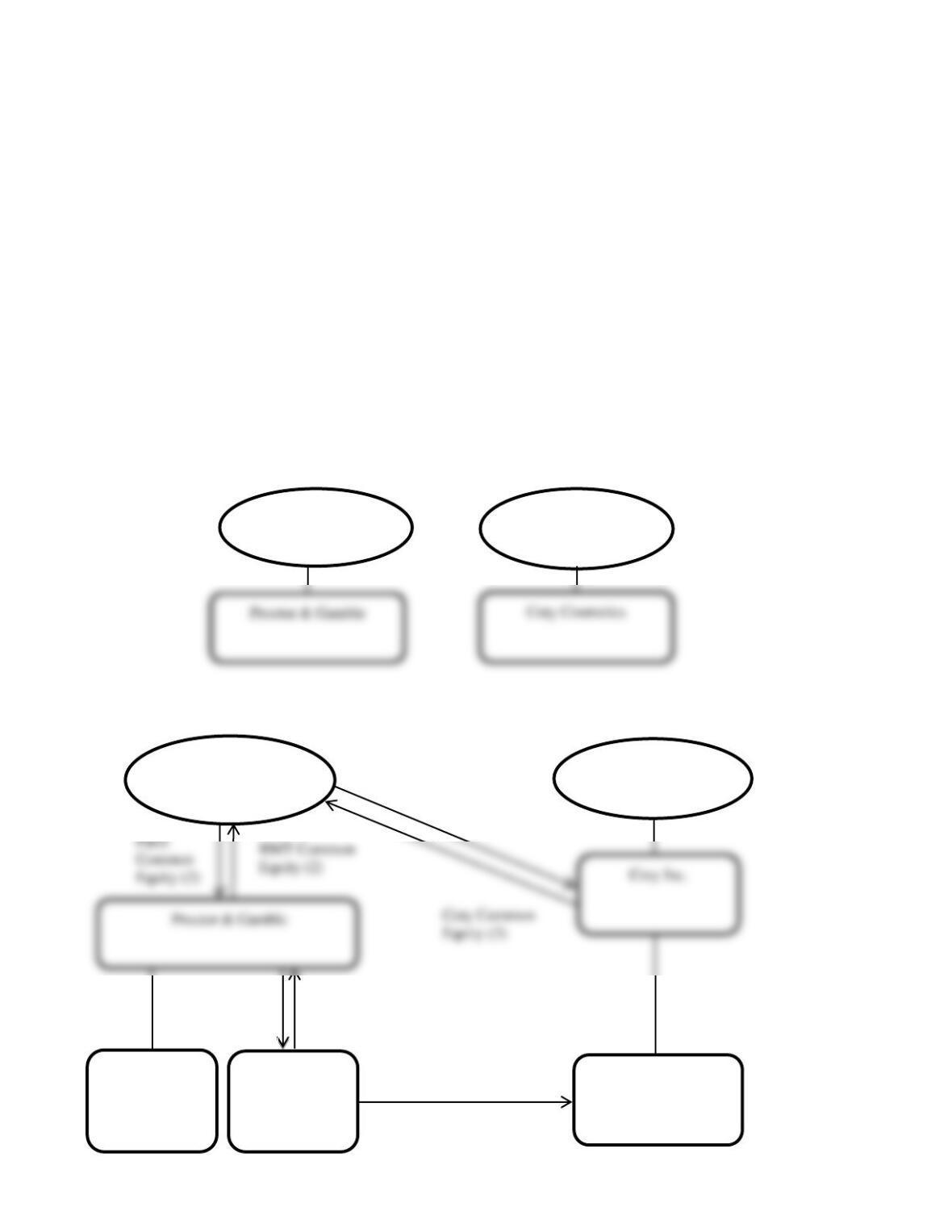

P&G Shareholders

Coty Shareholders

Pre-Merger and Pre-Split-Off Structure

Reverse Morris Trust Split-Off Structure

RMT Brands

Subsidiary

P&G Shareholders

46 Beauty

Brands (1)

RMT Common

Equity (1)

Coty Shareholders

Coty Merger Sub

(Merger Sub

Survives)

P&G Assets &

Liabilities

(Excl. divested

brands)

RMT Common

Equity (3)

RMT Brands Merges

into Merger Sub