SOLUTION

Requirement 1

Predetermined

Requirement 2

49,000

86,000

Bal.

60,350

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Dec 31

Cost of Goods Sold

60,350

Manufacturing Overhead

60,350

Requirement 4

Manufacturing Overhead

29,500

246,000*

48,000

P17-38B Preparing comprehensive accounting for manufacturing transactions

Learning Objectives 2, 3, 4, 5

4. COGM $46,750

5. NI $19,150

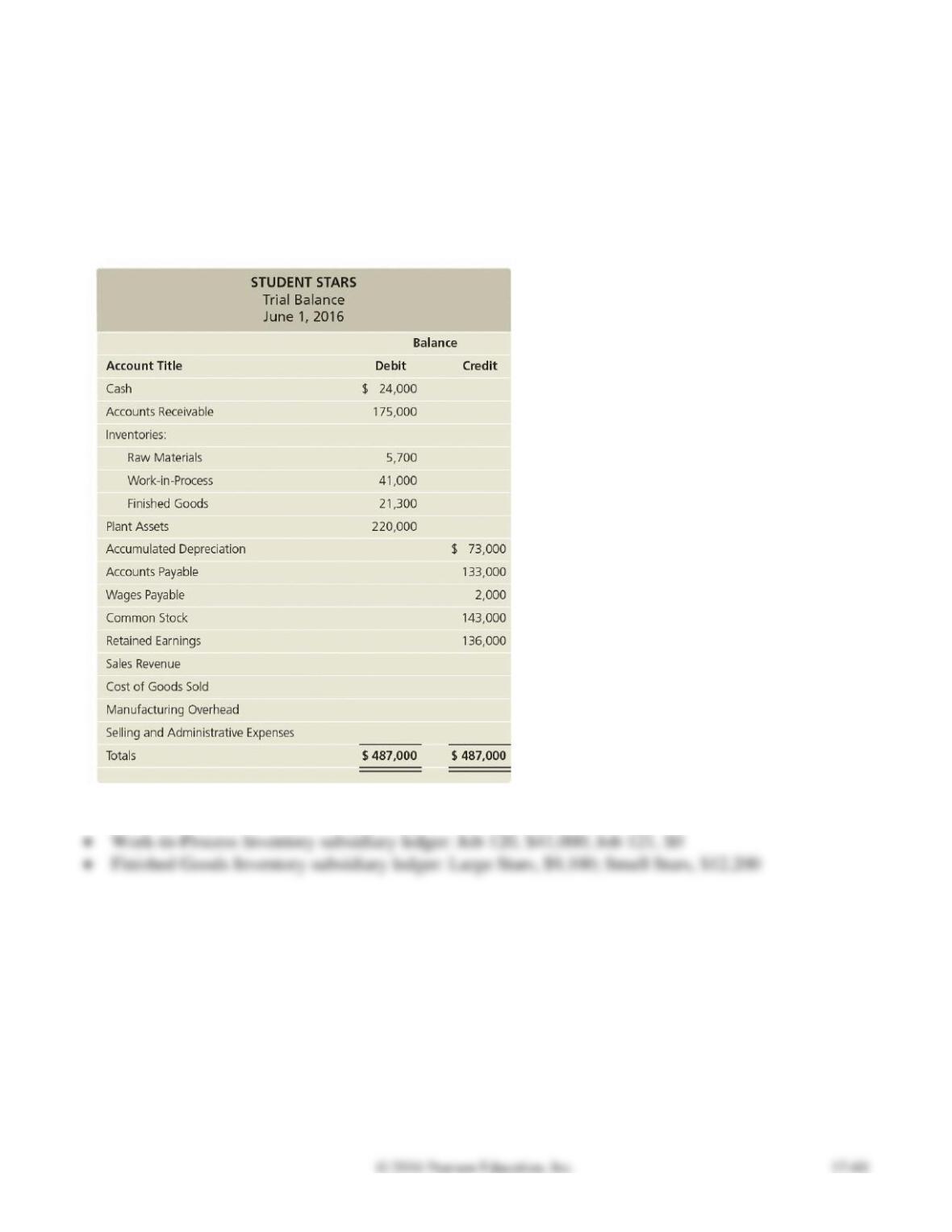

Student Stars produces stars for elementary teachers to reward their students. Student Stars’ trial balance

on June 1 follows:

June 1 balances in the subsidiary ledgers were as follows:

• Raw Materials Inventory subsidiary ledger: Paper, $4,300; indirect materials, $1,400

June transactions are summarized as follows:

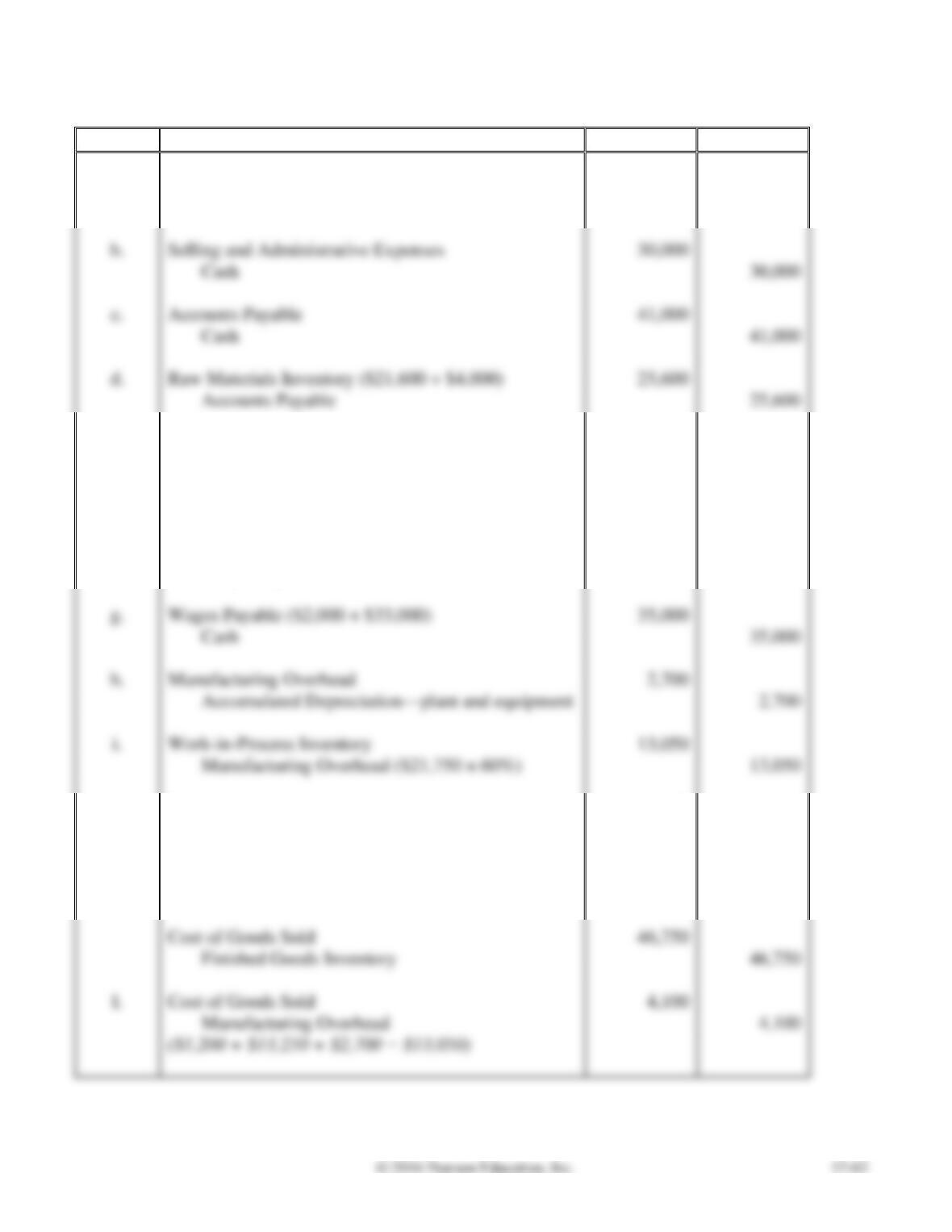

a. Collections on account, $154,000.

b. Selling and administrative expenses incurred and paid, $30,000.

c. Payments on account, $41,000.

f. Wages incurred during June, $35,000. Labor time records for the month: Job 120,

$3,250; Job 121, $18,500; indirect labor, $13,250.

g. Wages paid in June include the balance in Wages Payable at May 31 plus $33,000 of wages incurred

during June.

Requirements

1. Journalize the transactions for the company.

2. Open T-accounts for the general ledger, the Raw Materials Inventory subsidiary ledger, the Work-in–

Process Inventory subsidiary ledger, and the Finished Goods Inventory subsidiary ledger. Insert each

account balance as given, and use the reference Bal. Post the journal entries to the T-accounts using

the transaction letters as a reference.

3. Prepare a trial balance at June 30, 2016.

4. Use the Work-in-Process Inventory T-account to prepare a schedule of cost of goods manufactured

for the month of June.

5. Prepare an income statement for the month of June.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 30

a.

Cash

154,000

Accounts Receivable

154,000

b.

Selling and Administrative Expenses

30,000

Cash

30,000

c.

Accounts Payable

41,000

Cash

41,000

d.

Raw Materials Inventory ($21,600 + $4,000)

25,600

Accounts Payable

25,600

e.

Work-in-Process Inventory ($550 + $7,850)

8,400

Manufacturing Overhead

1,200

Raw Materials Inventory

9,600

f.

Work-in-Process Inventory ($3,250 + $18,500)

21,750

Manufacturing Overhead

13,250

Wages Payable

35,000

g.

Wages Payable ($2,000 + $33,000)

35,000

Cash

35,000

h.

Manufacturing Overhead

2,700

Accumulated Depreciation—plant and equipment

2,700

i.

Work-in-Process Inventory

13,050

Manufacturing Overhead ($21,750 × 60%)

13,050

j.

Finished Goods Inventory

46,750

Work-in-Process Inventory

46,750

k.

Accounts Receivable

100,000

Sales Revenue

100,000

Cost of Goods Sold

46,750

46,750

l.

Cost of Goods Sold

4,100

Manufacturing Overhead

4,100

P17-38B, cont.

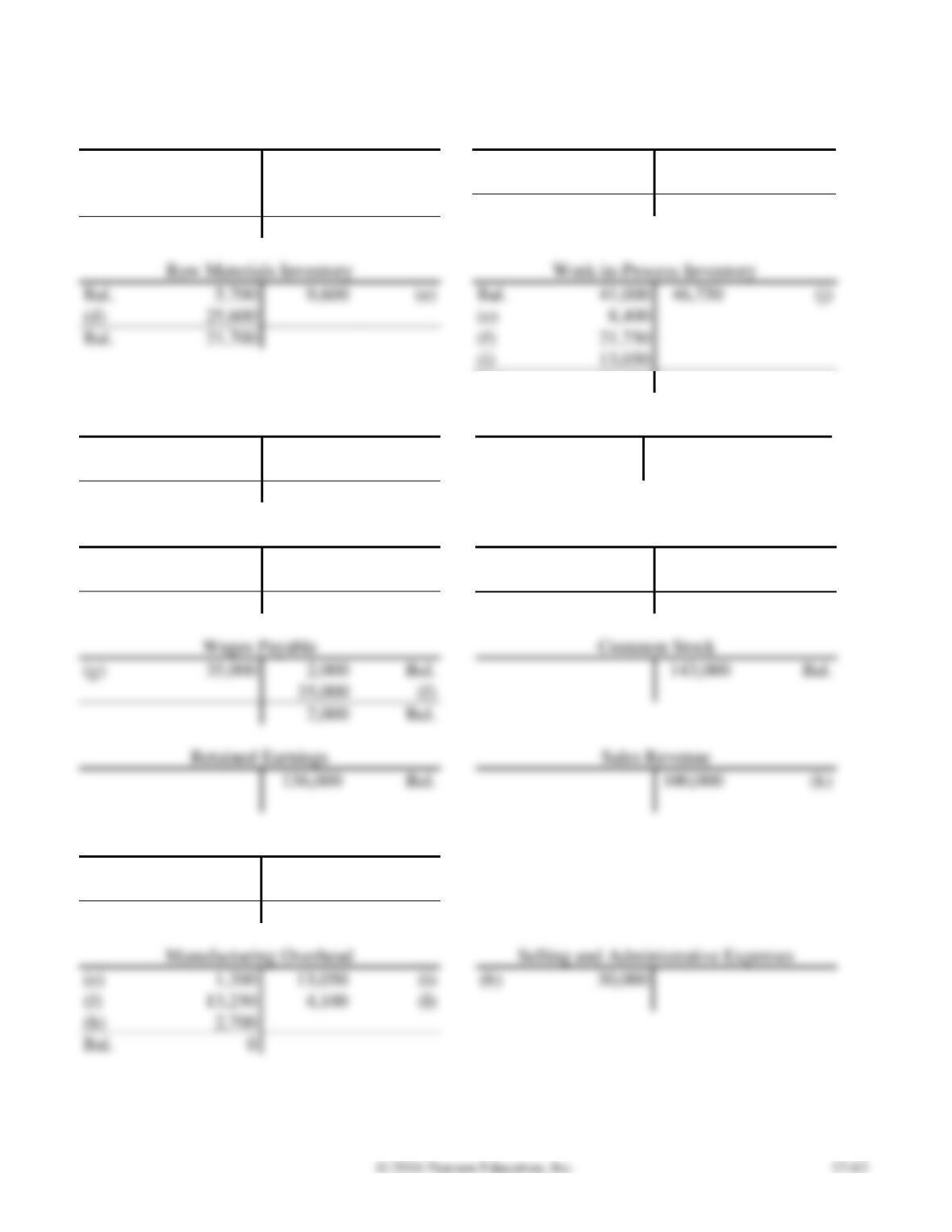

Requirement 2

Cash

Accounts Receivable

Bal.

24,000

30,000

(b)

Bal.

175,000

154,000

(a)

(a)

154,000

41,000

(c)

(k)

100,000

35,000

(g)

Bal.

121,000

Bal.

72,000

Raw Materials Inventory

Bal.

5,700

9,600

(e)

Bal.

41,000

(j)

(d)

25,600

(e)

8,400

Bal.

21,700

21,750

(i)

13,050

Bal.

37,450

Finished Goods Inventory

Plant Assets

Bal.

21,300

46,750

(k)

Bal.

220,000

(j)

46,750

Bal.

21,300

Accumulated Depreciation

Accounts Payable

73,000

Bal.

(c)

41,000

133,000

Bal.

2,700

(h)

25,600

(d)

75,700

Bal.

117,600

Bal.

(g)

35,000

2,000

Bal.

35,000

2,000

Bal.

100,000

(k)

Cost of Goods Sold

(k)

46,750

(l)

4,100

Bal.

50,850

Manufacturing Overhead

(e)

1,200

13,050

(b)

30,000

13,250

4,100

(h)

2,700

Bal.

P17-38B, cont.

Requirement 2, cont.

Raw Materials Inventory subsidiary ledger:

Bal.

4,300

8,400

Bal.

1,400

1,200

(d)

21,600

(d)

4,000

Bal.

17,500

Bal.

4,200

Work-in-Process Inventory subsidiary ledger:

Job 120

Job 121

Bal.

41,000

46,750

(j)

Bal.

0

(e)

550

(e)

7,850

(f)

3,250

(f)

18,500

(i)

1,950

(i)

11,100

Bal.

0

Bal.

37,450

Balance equals balance of Work-in-Process Inventory, $37,450 ($0 + $37,450).

Finished Goods Inventory subsidiary ledger:

Bal.

9,100

46,750

Bal.

12,200

(j)

46,750

Bal.

12,200

Bal.

9,100

P17-38B, cont.

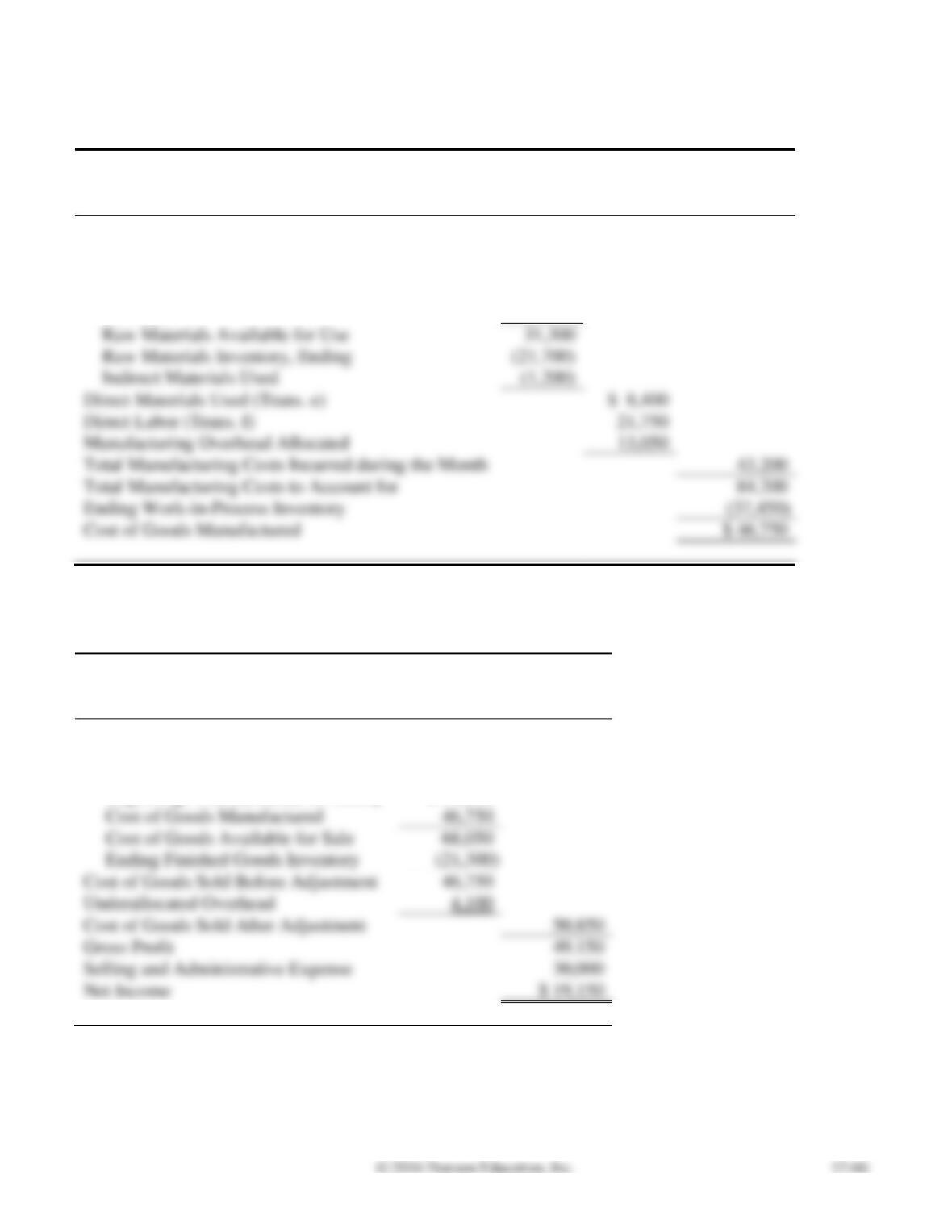

Requirement 3

STUDENT STARS

Trial Balance

June 30, 2016

Account Title

Debit

Credit

Cash

$ 72,000

Accounts Receivable

121,000

Inventories:

Raw Materials

21,700

37,450

Finished Goods

21,300

Plant Assets

220,000

Accumulated Depreciation

$ 75,700

Accounts Payable

117,600

Wages Payable

Common Stock

143,000

Retained Earnings

136,000

Sales Revenue

100,000

Cost of Goods Sold

50,850

Selling and Administrative Expenses

30,000

Totals

$ 574,300

$ 574,300

P17-38B, cont.

Requirement 4

STUDENT STARS

Schedule of Cost of Goods Manufactured

Month Ended June 30, 2016

Beginning Work-in-Process Inventory

$ 41,000

Direct Materials Used:

Raw Materials Inventory, Beginning

$ 5,700

Purchases

25,600

Raw Materials Available for Use

31,300

Raw Materials Inventory, Ending

Indirect Materials Used

Direct Materials Used (Trans. e)

Direct Labor (Trans. f)

Manufacturing Overhead Allocated

Total Manufacturing Costs Incurred during the Month

Total Manufacturing Costs to Account for

Ending Work-in-Process Inventory

Cost of Goods Manufactured

$ 46,750

Requirement 5

STUDENT STARS

Income Statement

Month Ended June 30, 2016

Sales Revenue

$ 100,000

Cost of Goods Sold:

Beginning Finished Goods Inventory

$ 21,300

Cost of Goods Manufactured

Cost of Goods Available for Sale

Ending Finished Goods Inventory

Cost of Goods Sold Before Adjustment

Cost of Goods Sold After Adjustment

Gross Profit

Selling and Administrative Expense

Net Income

P17-39B Using job order costing in a service company

Learning Objective 6

2. Food Co-op $277,600

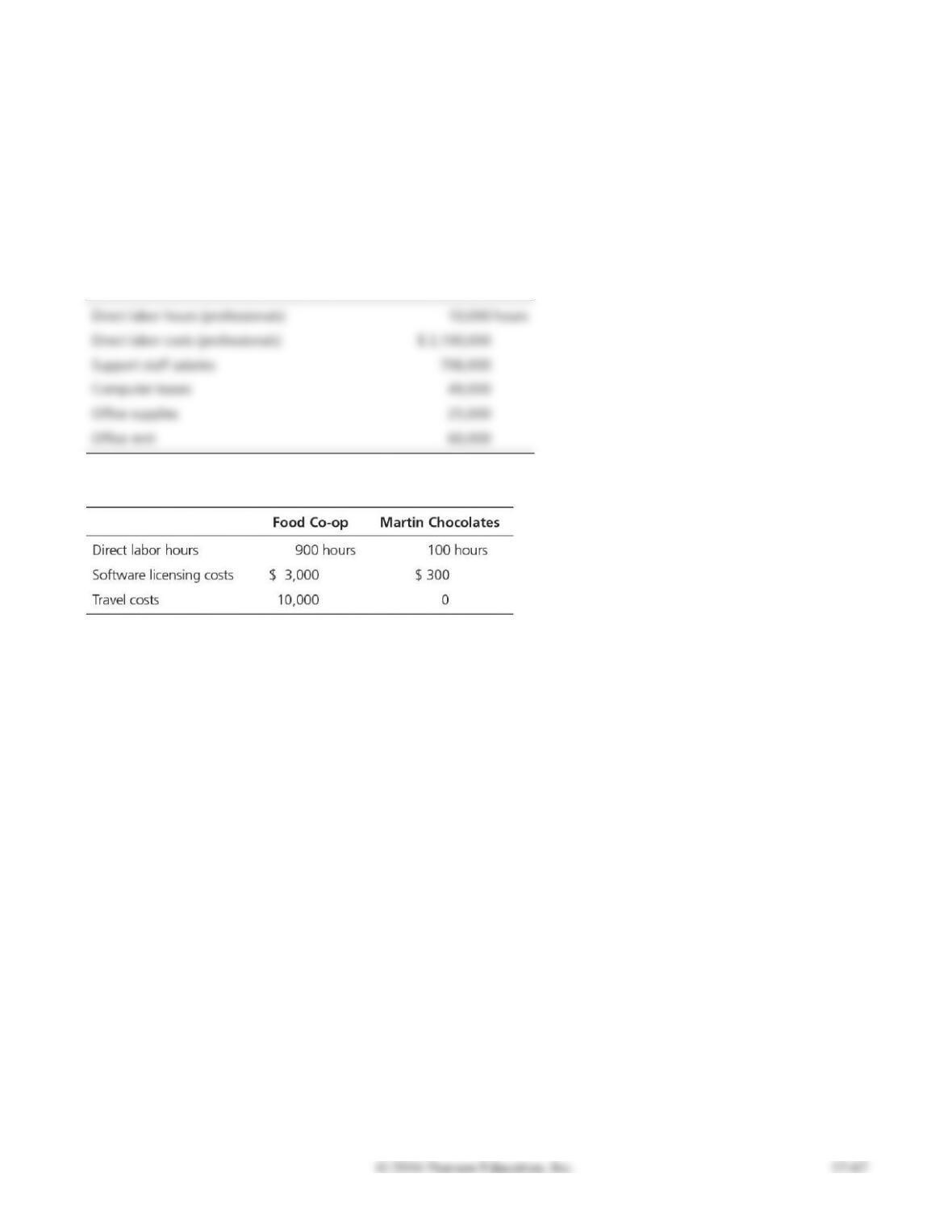

Robin Design, Inc. is a Web site design and consulting firm. The firm uses a job order costing system in

which each client is a different job. Robin Design assigns direct labor, licensing costs, and travel costs

directly to each job. It allocates indirect costs to jobs based on a predetermined overhead allocation rate,

computed as a percentage of direct labor costs.

At the beginning of 2016, managing partner Judi Jacquin prepared the following budget estimates:

In November 2016, Robin Design served several clients. Records for two clients appear here:

Requirements

1. Compute Robin Design’s direct labor rate and its predetermined overhead allocation rate for 2016.

2. Compute the total cost of each job.

3. If Judi wants to earn profits equal to 20% of service revenue, what fee should she charge each of

these two clients?

4. Why does Robin Design assign costs to jobs?

SOLUTION

Requirement 1

Hourly rate

to the employer

=

$2,100,000 per year

=

$210 per hour

10,000 hours per year

=

Total estimated quantity of the overhead allocation base

=

*$706,000 + $49,000 + $25,000 + $60,000 = $840,000

Requirement 2

ROBIN DESIGN, INC.

Total Cost of Food Co-ops’ and Martin Chocolates’ Jobs

For the Month of November

Food

Co-op

Martin

Chocolates

Total Costs

P17-39B, cont.

Requirement 3

If profits are 20% of sales, then total costs are 80% of sales. Therefore, Sales Revenue = Total Costs /

80%.

Continuing Problem

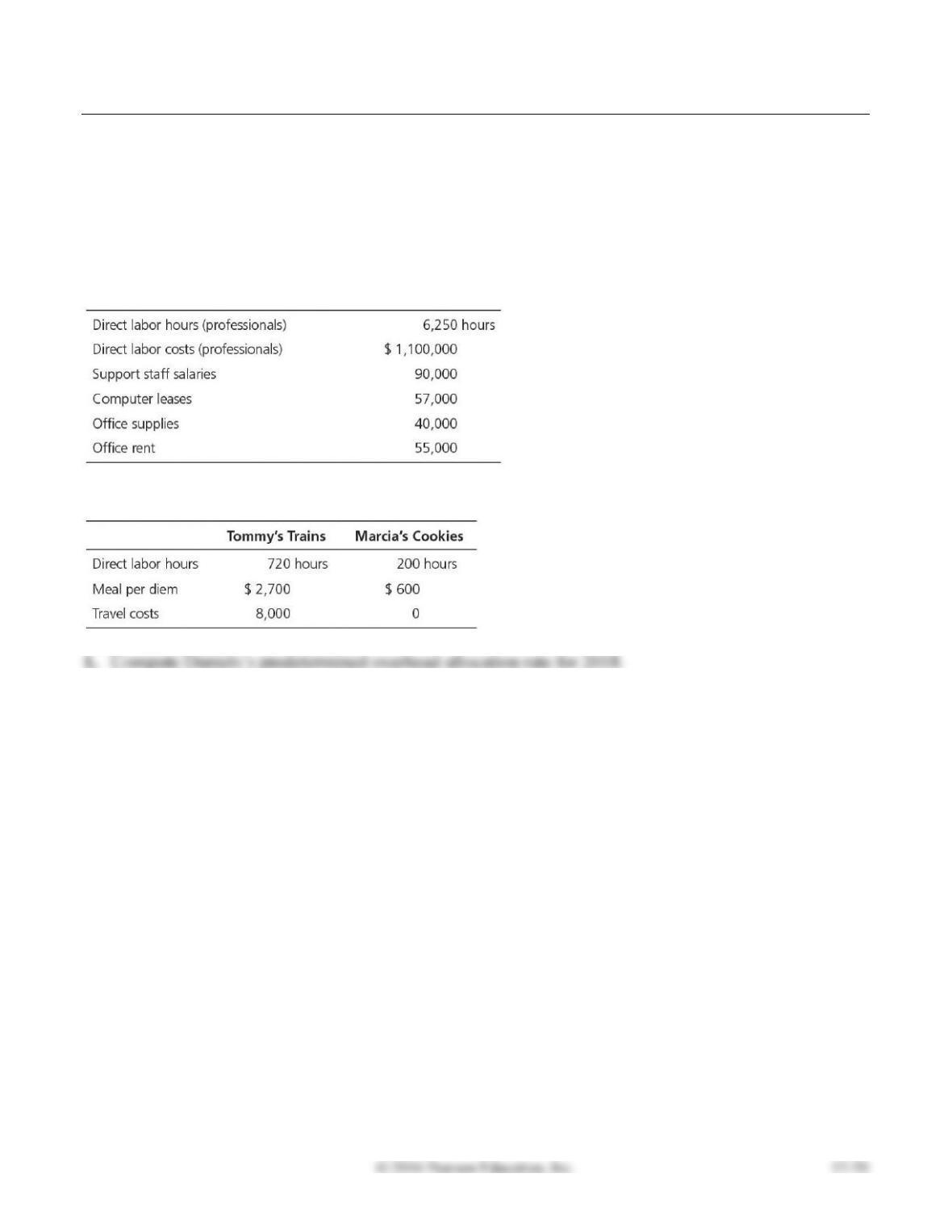

P17-40 Accounting for manufacturing overhead

This problem continues the Daniels Consulting situation from Problem P16-42 of Chapter 16. Daniels

Consulting uses a job order costing system in which each client is a different job. Daniels assigns direct

labor, meal per diem, and travel costs directly to each job. It allocates indirect costs to jobs based on a

predetermined overhead allocation rate, computed as a percentage of direct labor costs.

At the beginning of 2018, the controller prepared the following budget:

In November 2018, Daniels served several clients. Records for two clients appear here:

Requirements

2. Compute the total cost of each job.

3. If Daniels wants to earn profits equal to 25% of sales revenue, what fee should it charge each of

these two clients?

4. Why does Daniels assign costs to jobs?

SOLUTION

Requirement 1

Predetermined

Requirement 2

DANIELS CONSULTING

Total Cost of Tommy’s Trains and Marcia’s Cookies Jobs

For the Month of November

Tommy’s

Trains

Marcia’s

Cookies

Direct labor

$ 126,720

Meal per diem

Travel costs

$ 165,298

P17-40, cont.

Requirement 3

If profits are 25% of sales, then total costs are 75% of sales. Therefore, Sales Revenue = Total Costs /

75%.

Critical Thinking

Decision Case 17-1

Hiebert Chocolate, Ltd. is located in Memphis. The company prepares gift boxes of chocolates for

private parties and corporate promotions. Each order contains a selection of chocolates determined by

the customer, and the box is designed to the customer’s specifications. Accordingly, Hiebert uses a job

order costing system and allocates manufacturing overhead based on direct labor cost.

Ben Hiebert, president of Hiebert Chocolate, Ltd., priced the order at $20 per box.

In the past few months, Hiebert has experienced price increases for both dark chocolate and direct

labor. All other costs have remained the same. Hiebert budgeted the cost per box for the second order as

follows:

Requirements

1. Do you agree with the cost analysis for the second order? Explain your answer.

2. Should the two orders be accounted for as one job or two in Hiebert’s system?

3. What sale price per box should Ben Hiebert set for the second order? What are the advantages and

disadvantages of this price?

SOLUTION

Requirement 1

The cost analysis for the second order is correct. The problem tells us that overhead is allocated “based

on direct labor cost,” and we can see from the first order that the allocation rate is 50% of direct labor

Requirement 2

Hiebert should account for each order as a separate job. The orders were received at different times, for

different amounts, and the costs per box of the orders are not the same.

Requirement 3

Student responses will vary. Answers should make it clear that Hiebert is free to price his products any

Fraud Case 17-1

Jerry never imagined he’d be sitting there in Washington being grilled mercilessly by a panel of

congressmen. But a young government auditor picked up on his scheme last year. His company

produced high-tech navigation devices that were sold to both military and civilian clients. The military

contracts were “cost–plus,” meaning that payments were calculated based on actual production costs plus

a profit markup. The civilian contracts were bid out in a very competitive market, and every dollar

counted. Jerry knew that because all the jobs were done in the same factory, he could manipulate the

allocation of overhead costs in a way that would shift costs away from the civilian contracts and into the

military “cost–plus” work. That way, the company would collect more from the government and be able

to shave its bids down on civilian work. He never thought anyone would discover the alterations he had

made in the factory workers’ time sheets, but one of his accountants had noticed and tipped off the

government auditor. Now, as the congressman from Michigan rakes him over the coals, Jerry is trying to

figure out his chances of dodging jail time.

Requirements

1. Based on what you have read above, what was Jerry’s company using as a cost driver to allocate

overhead to the various jobs?

2. Why does the government consider Jerry’s actions fraudulent?

3. Name two ways that reducing costs on the civilian contracts would benefit the company and

motivate Jerry to commit fraud.

SOLUTION

Requirement 1

The company is using direct labor hours as a cost driver to allocate overhead. By showing more hours

spent on military jobs, more overhead would be allocated to these jobs over civilian contracts.