CHAPTER 17

Process Costing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

* 1. Discuss the uses of a

process cost system and

how it compares to a job

order system.

1, 2, 3, 4, 5,

20

1

1

costs.

10, 11, 13, 14,

5A, 6A

14, 15

method.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize transactions.

Moderate

20–30

2A

Complete four steps necessary to prepare a production

cost report.

Simple

30–40

3A

Complete four steps necessary to prepare a production

cost report.

Simple

30–40

4A

Assign costs and prepare production cost report.

Moderate

20–30

assign costs.

cost report.

costs for processes; prepare production cost report.

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Discuss the uses of a process cost

system and how it compares to a job

order system.

Q17-1

Q17-2

Q17-3

Q17-4

Q17-5

Q17–20

E17-1

DI17-1

* 2. Explain the flow of costs in a process

cost system and the journal entries to

assign manufacturing costs.

Q17-6

Q17-7

BE17-1

BE17-2

BE17-3

DI17-2

E17-2

E17-3

E17-4

P17-1A

DI17-3

E17–10

P17-4A

Q17–22

BE17–10

BE17–11

E17–17

E17–18

P17–7A

ANSWERS TO QUESTIONS

1. (a) Process cost.

(b) Process cost.

(c) Job order.

(d) Job order.

4. The features of process cost accounting are: (1) separate work in process accounts for each

process, (2) production cost reports, (3) product costs computed for each accounting period, and

(4) unit costs computed based on total manufacturing costs.

5. Sam is correct. The flow of costs is the same in process cost accounting as in job order cost

accounting. The method of assigning costs, however, is significantly different.

7. The entry to assign overhead to production is:

July 31 Work in Process—Machining ……………………………………………. 15,000

Work in Process—Assembly …………………………………………….. 12,000

Manufacturing Overhead …………………………………………… 27,000

Questions Chapter 17 (Continued)

13.

Equivalent Units

Materials

Conversion Costs

14.

Units transferred out were 3,200*

Units to be accounted for

Work in process (beginning)

Started into production

Total units

500

3,000

3,500

Units accounted for

Completed and transferred out

Work in process (ending)

Total units

3,200*

300

3,500

*3,500 – 300

18. The per unit conversion cost is $11.25. [Conversion costs = $6,000 – $2,400 = $3,600. Equivalent units

for conversion costs are 320 (800 X 40%); $3,600 ÷ 320 = $11.25.]

19. Operations costing is similar to process costing in that standardized methods are used to manufacture

the product. At the same time, the product may have some customized individual features that

require the use of a job order cost system.

Units transferred out

Work in process

500 X 100%

500 X 20%

Total equivalent units

500

12,500

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 17-1

BRIEF EXERCISE 17-2

BRIEF EXERCISE 17-3

BRIEF EXERCISE 17-4

BRIEF EXERCISE 17-5

BRIEF EXERCISE 17-6

BRIEF EXERCISE 17-7

BRIEF EXERCISE 17-8

BRIEF EXERCISE 17-9

*BRIEF EXERCISE 17–10

*BRIEF EXERCISE 17–11

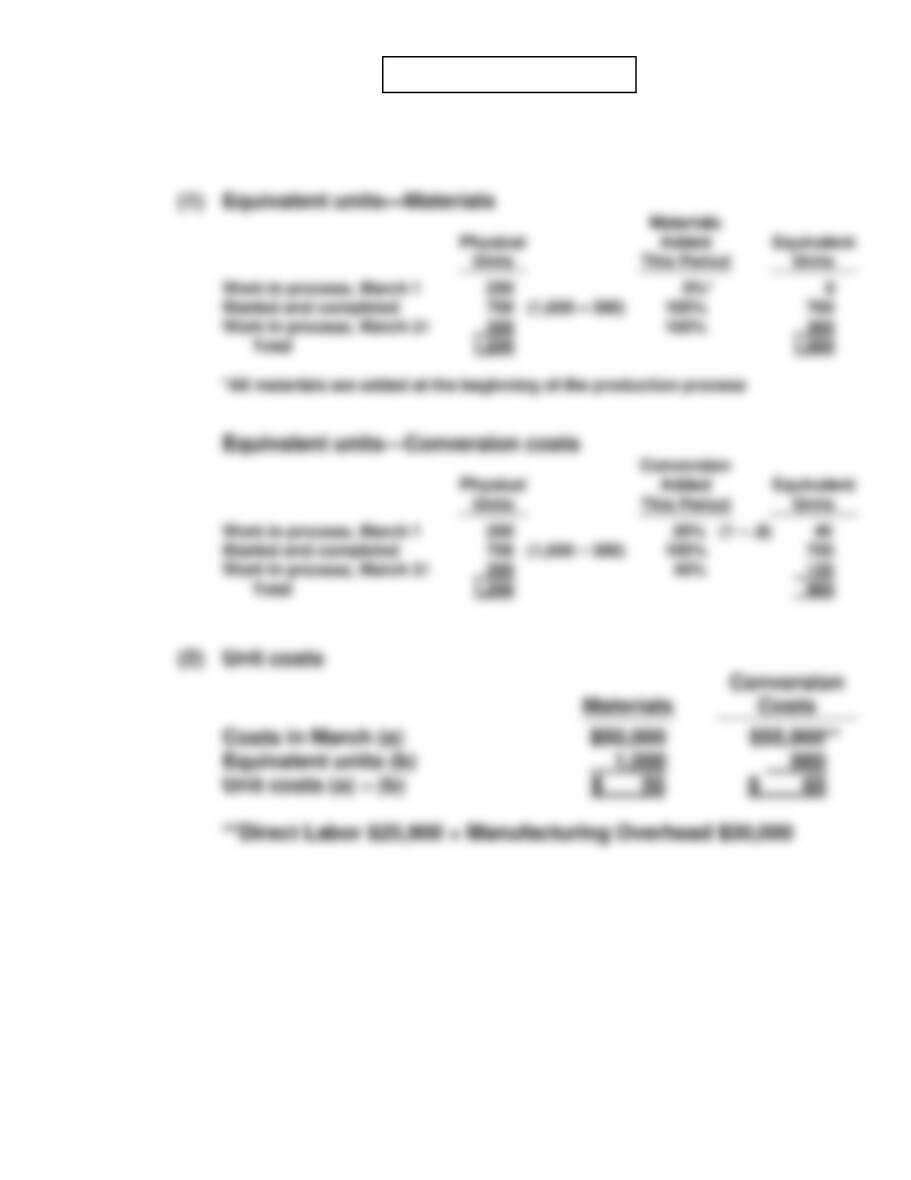

Equivalent Units

PIX COMPANY

(Partial) Production Cost Report

For the Month Ended March 31

*BRIEF EXERCISE 17–12

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 17-1

DO IT! 17-2

DO IT! 17-2 (Continued)

DO IT! 17-3

DO IT! 17-4

DO IT! 17-4 (Continued)

SOLUTIONS TO EXERCISES

EXERCISE 17-1

10. True.

EXERCISE 17-2

EXERCISE 17-3

EXERCISE 17-4

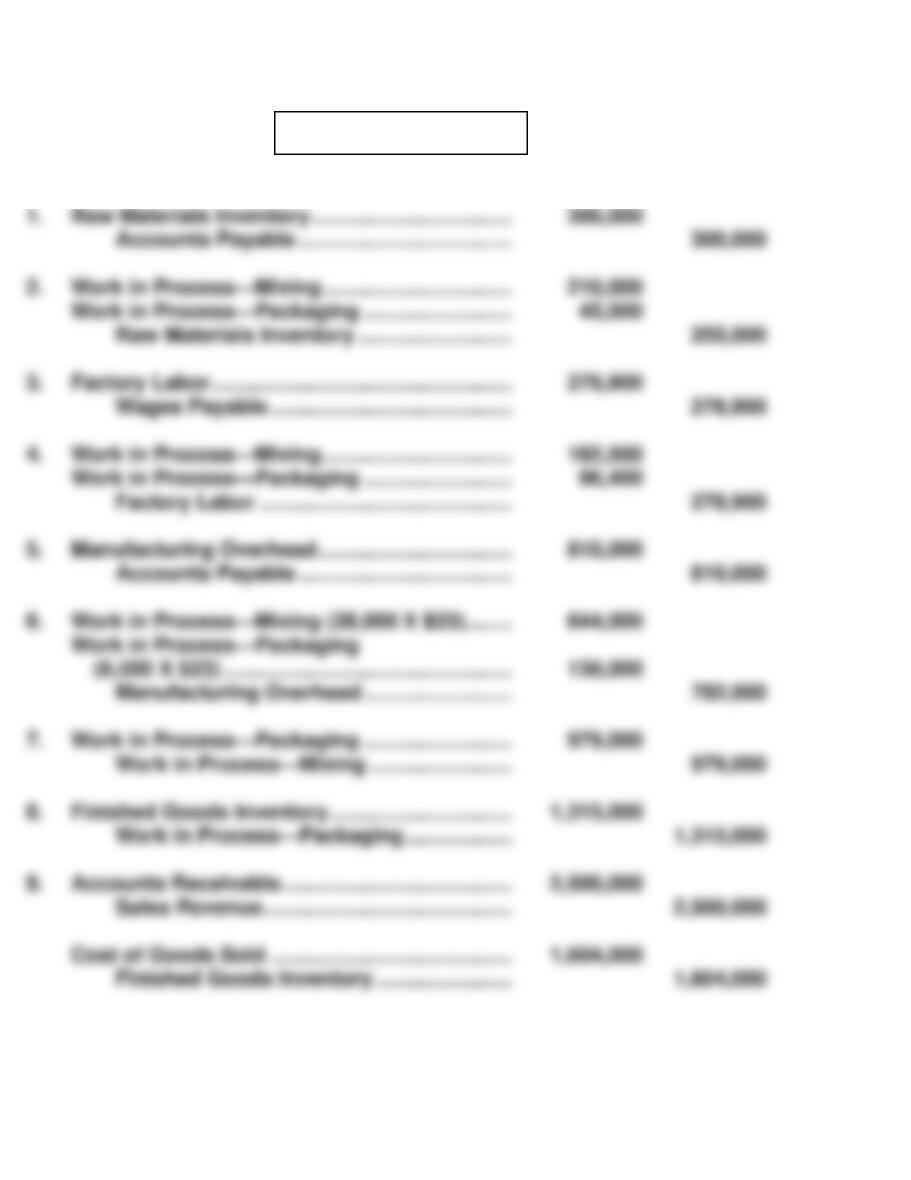

1. Raw Materials Inventory …………………………………… 62,500

Accounts Payable …………………………………….. 62,500

5. Work in Process—Cutting ………………………………… 33,000

Work in Process—Assembly ……………………………. 27,000

Factory Labor …………………………………………… 60,000

6. Work in Process—Cutting (1,680 X $18) ……………. 30,240

Work in Process—Assembly (1,720 X $18) ………… 30,960

Manufacturing Overhead …………………………... 61,200

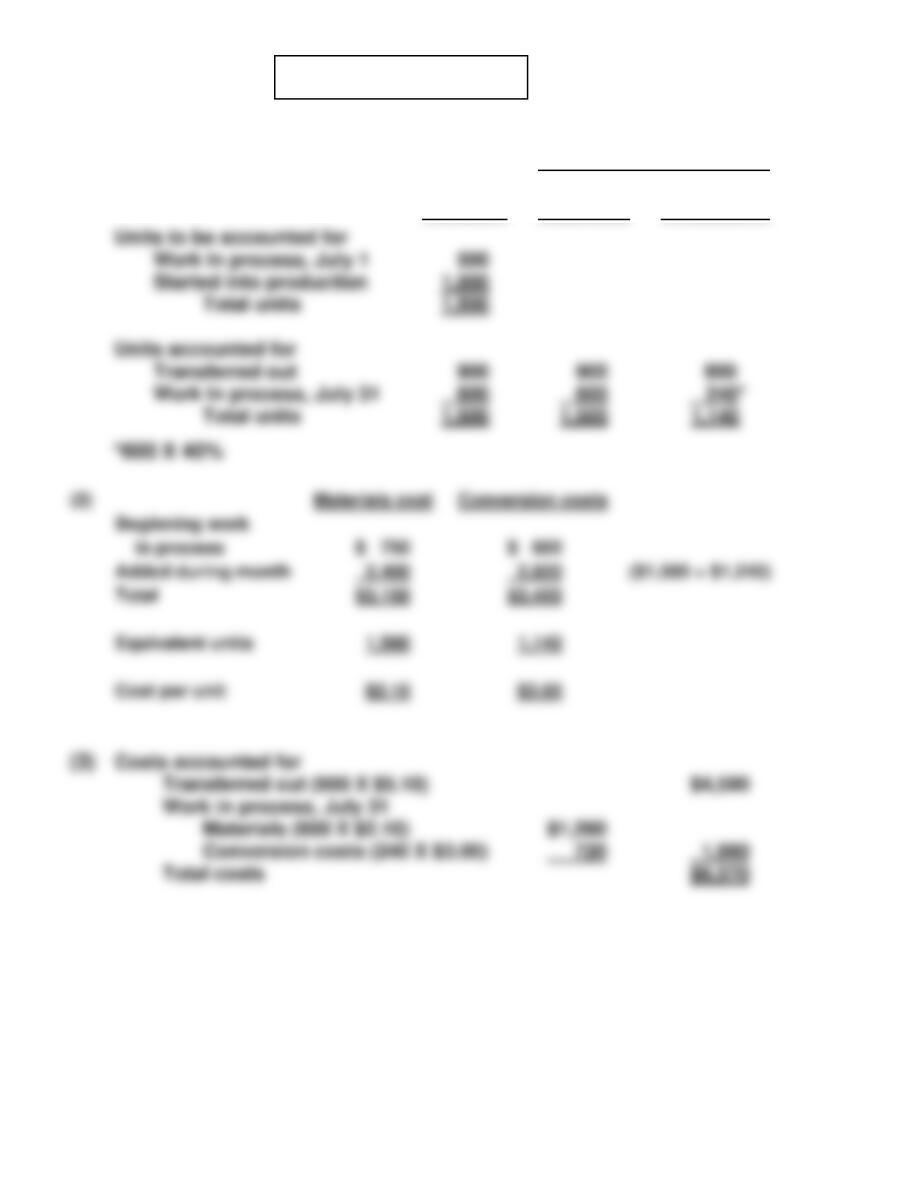

EXERCISE 17-5

(a)

January

May

(b)

(1)

Materials

(2)

Conversion Costs

11,500 (10,000 + 1,500)

EXERCISE 17-6

(a)

(1)

Materials

(2)

Conversion Costs

Total units

EXERCISE 17-7

QUIK FURNITURE COMPANY

Sanding Department

Production Cost Report

For the Month Ended March 31, 2017

EXERCISE 17-8

(a)

(1)

Materials

(2)

Conversion

Costs

EXERCISE 17-9

Unit costs

Materials (1,000 X $50)

Total costs

EXERCISE 17–10

(a)

Physical

Units

Equivalent Units

(b)

Conversion

Materials

Costs

Total

Equivalent units

Unit costs

(c)

Assignment of costs:

Transferred out (160,000 X $2.55)

EXERCISE 17–11

(a)

Work in process, September 30

Physical

EXERCISE 17-11 (Continued)

Equivalent Units

(c) Costs accounted for

EXERCISE 17–12

To: David Skaros

From: Student

Re: Ending inventory

EXERCISE 17–13

HEALTHY COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversio

n

Costs

Units accounted for

Total units

Costs

Work in process, February 1

Materials (11,000 X $3.00)

Total costs

EXERCISE 17–14

EXERCISE 17–15

(a)

Materials

Conversion

Costs

Work in process, September 30

Equivalent units

(b)

Conversion costs: $25,480* ÷ 980 = $26.00

Costs accounted for:

Work in process, September 30

Materials (300 X $5.00)

Total costs

*($3,960 + $12,000 + $9,520)

Containers off-loaded

Containers in transit, April 30

*EXERCISE 17–16

Equivalent Units

(a)

Physical

Units

Materials

Conversion

Costs

(b)

Materials: $4,500 ÷ 1,000 = $4.50

Conversion costs: $21,620* ÷ 940 = $23.00

1,350

Applications completed:

Work in process, September 1

100

Started and completed

700

Work in process, September 30

Total units

*EXERCISE 17–17

(a) (1) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

(2) Conversion Costs:

Production Data

Physical

Units

Work Added

This Period

Equivalent

Units

Total

Work in process, August 31

Total

*EXERCISE 17–18

(a)

(1)

Materials

Physical

Units

Materials Added

This Period

Equivalent

Units

(2)

Conversion Costs

Physical

Units

Work Added

This Period

Equivalent

Units

(c)

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

4,800

Total

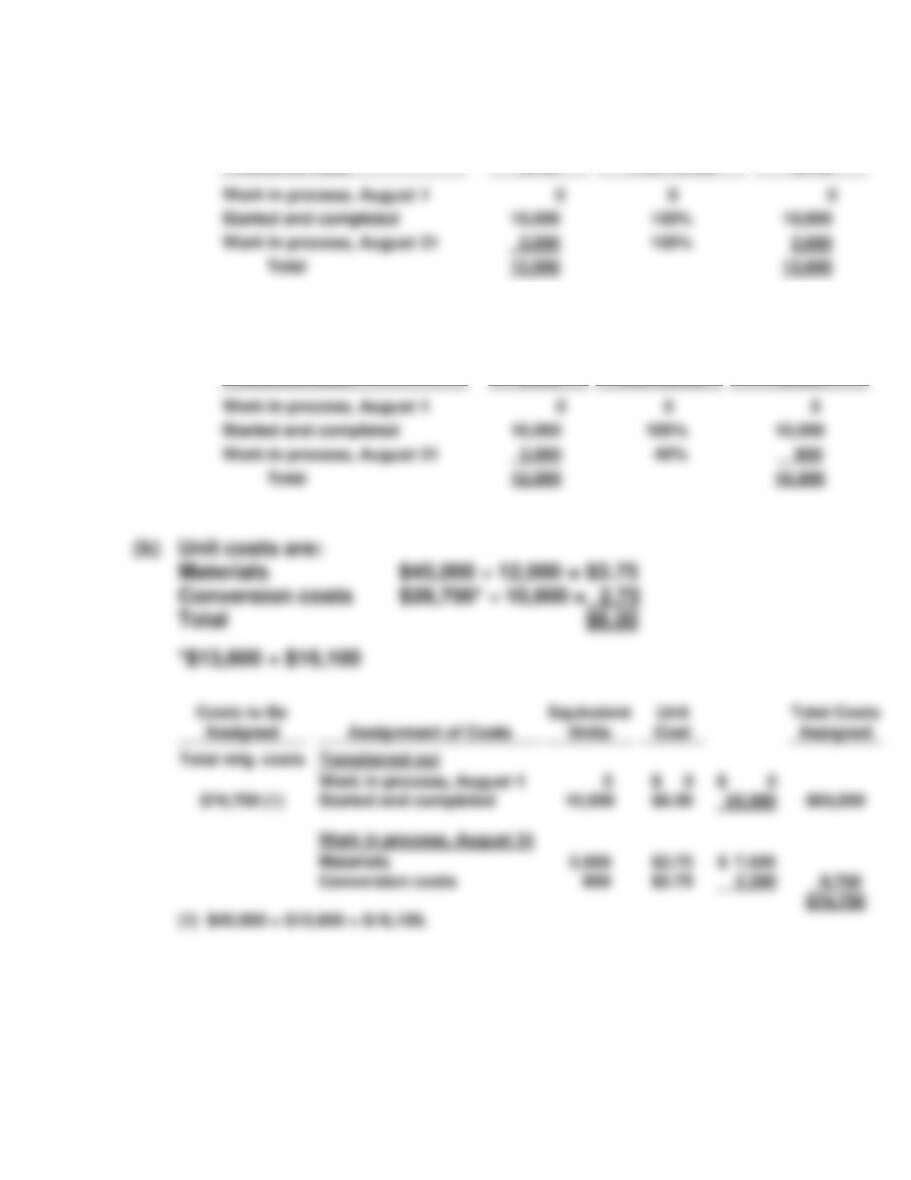

*EXERCISE 17–19

(b) Materials:

Production Data

Physical

Units

Materials Added

This Period

Equivalent

Units

Work in process, March 31

Total

(c) Conversion costs:

Production Data

Physical

Units

Work Added

This Period

Equivalent

Units

Work in process, March 31

Total

*EXERCISE 17–20

MAJESTIC COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

Costs

Materials

Costs

Started into production

Total costs

Conversion

Total

Units accounted for

Total

Work in process, February 28

Total units

*EXERCISE 17-20 (Continued)

SOLUTIONS TO PROBLEMS

PROBLEM 17–1A

PROBLEM 17–2A

(b)

Equivalent units

Total equivalent units

Total unit cost

Total units

PROBLEM 17-2A (Continued)

(e) ROSENTHAL COMPANY

Molding Department

Production Cost Report

For the Month Ended June 30, 2017

Costs

Materials

Conversion

Costs

Total

Total costs

Total costs

6,400

24,400

Quantities

Materials

Conversion

Costs

Work in process, June 30

(2,000 X 40%)

Total units

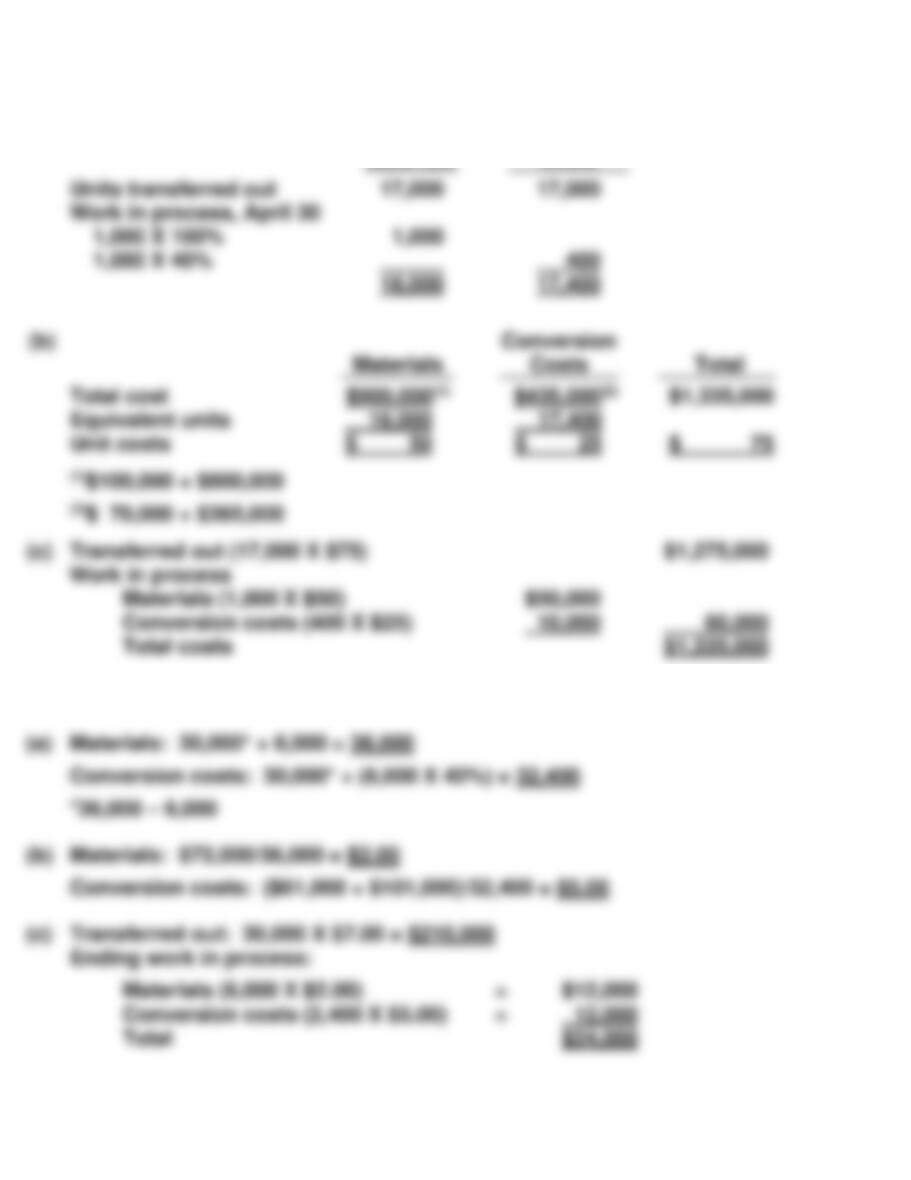

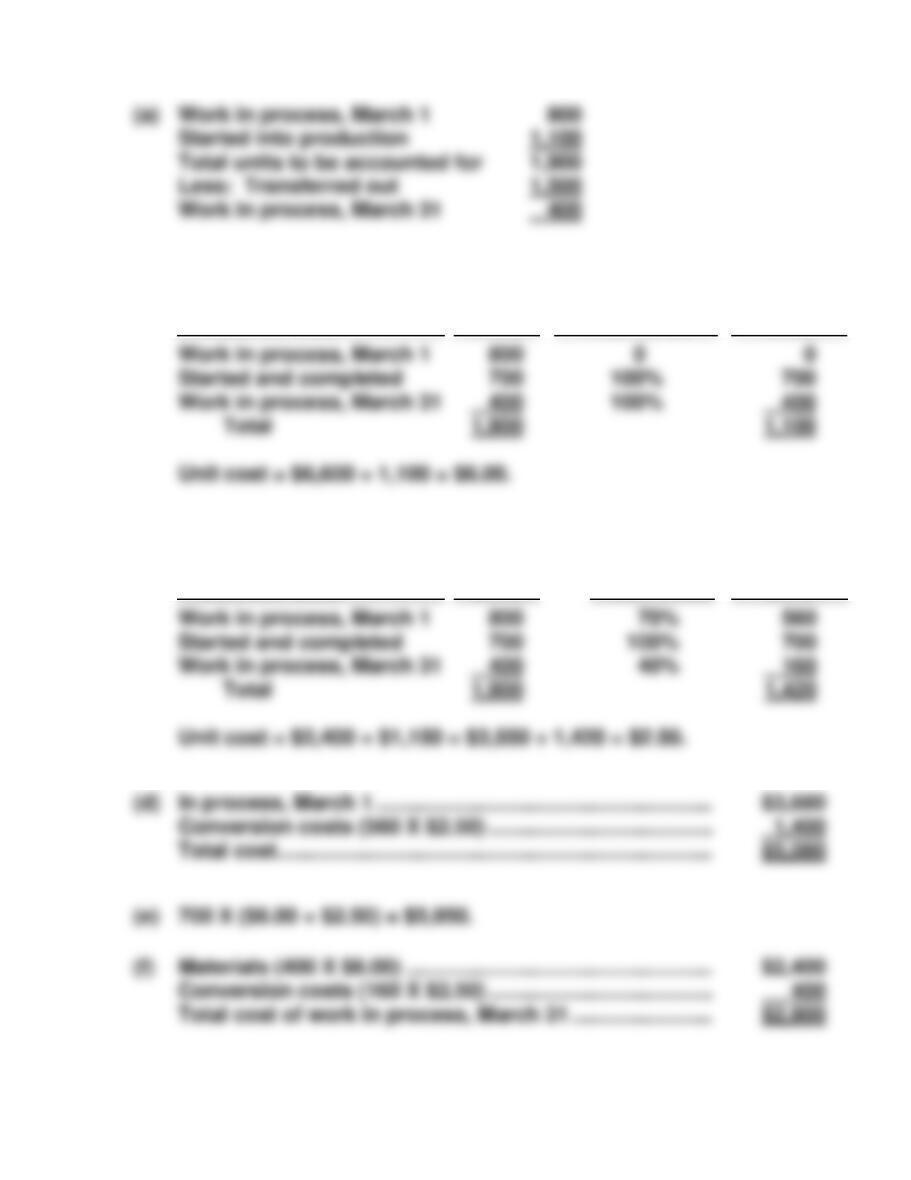

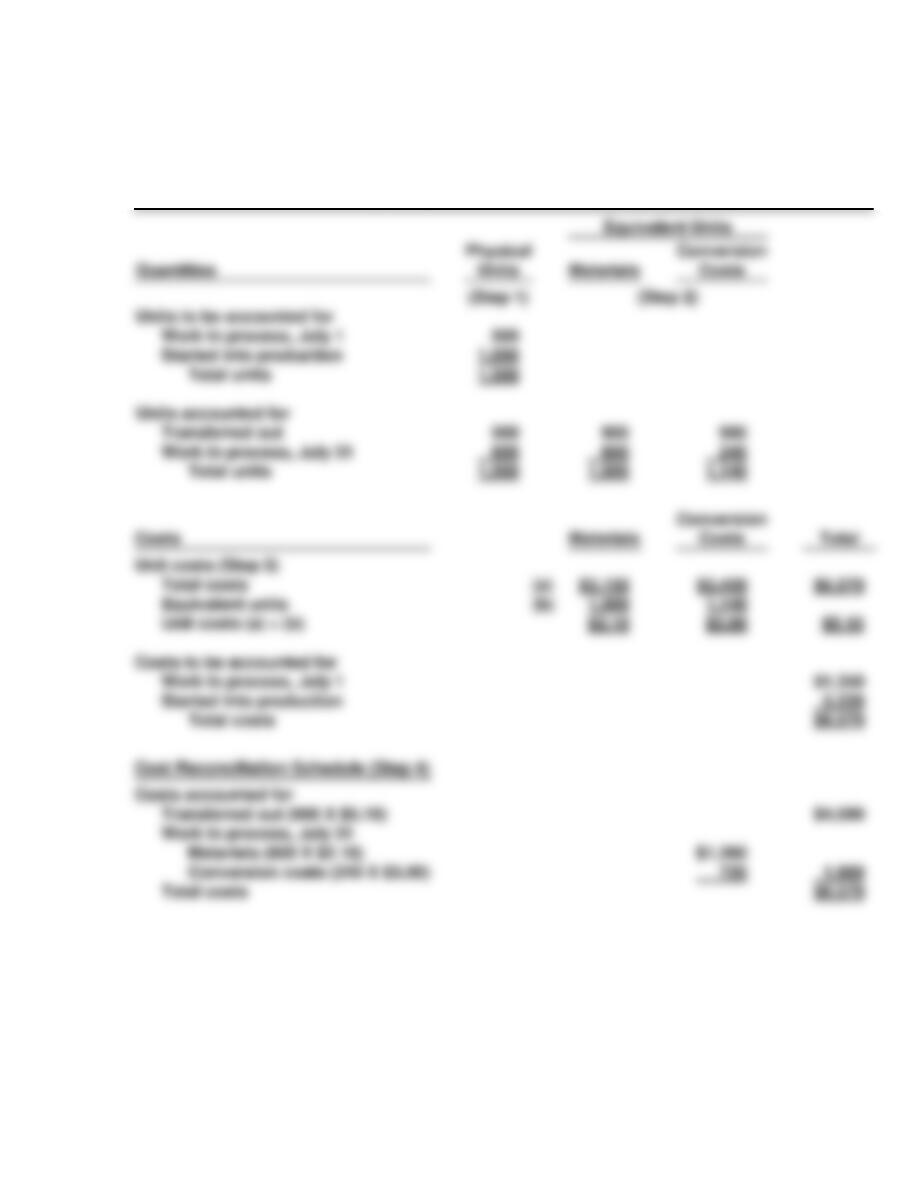

PROBLEM 17–3A

(a) (1) Physical units

(2) Equivalent units

PROBLEM 17-3A (Continued)

(3) Unit costs

PROBLEM 17-3A (Continued)

(b) THAKIN INDUSTRIES INC.

Cutting Department—Plant 1

Production Cost Report

For the Month Ended July 31, 2017

PROBLEM 17–4A

(a)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Work in process, November 30

Total units

25,000

695,000

25,000

695,000

Total costs

PROBLEM 17-4A (Continued)

(c) RIVERA COMPANY

Assembly Department

Production Cost Report

For the Month Ended November 30, 2017

PROBLEM 17–5A

(a)

(1)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

PROBLEM 17-5A (Continued)

(b) POLK COMPANY

Basketball Department

Production Cost Report

For the Month Ended July 31, 2017

PROBLEM 17–6A

(a) Computation of equivalent units:

*PROBLEM 17–7A

(a) Bicycles

*PROBLEM 17-7A (Continued)

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

Tricycles

Total costs transferred out

Work in process, March 31

Total costs

*PROBLEM 17-7A (Continued)

(3) Assignment of costs to units transferred out and in process

Costs to Be

Assigned

Assignment of Costs

Equivalent

Units

Unit

Cost

Total Costs

Assigned

*PROBLEM 17-7A (Continued)

(b) OWEN COMPANY

Production Cost Report—Bicycles

For the Month Ended March 31

CD–17 DECISION-MAKING AT CURRENT DESIGNS

CURRENT DESIGNS

Fabrication Department

Production Cost Report

For the Month Ended April 30, 2017

Equivalent Units

Physical

Conversion

Quantities

Materials

(Step 2)

Costs

BYP 17-1 DECISION-MAKING ACROSS THE ORGANIZATION

BYP 17-1 (Continued)

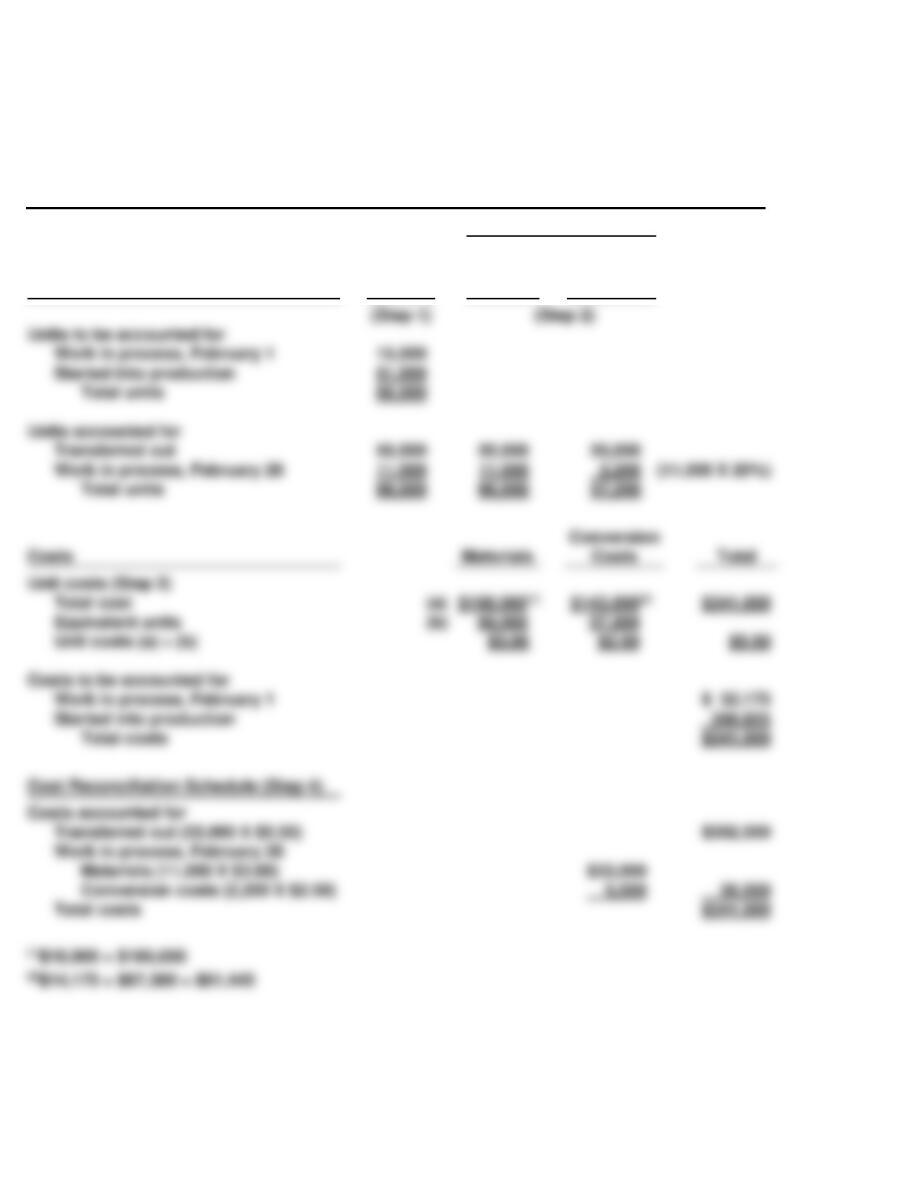

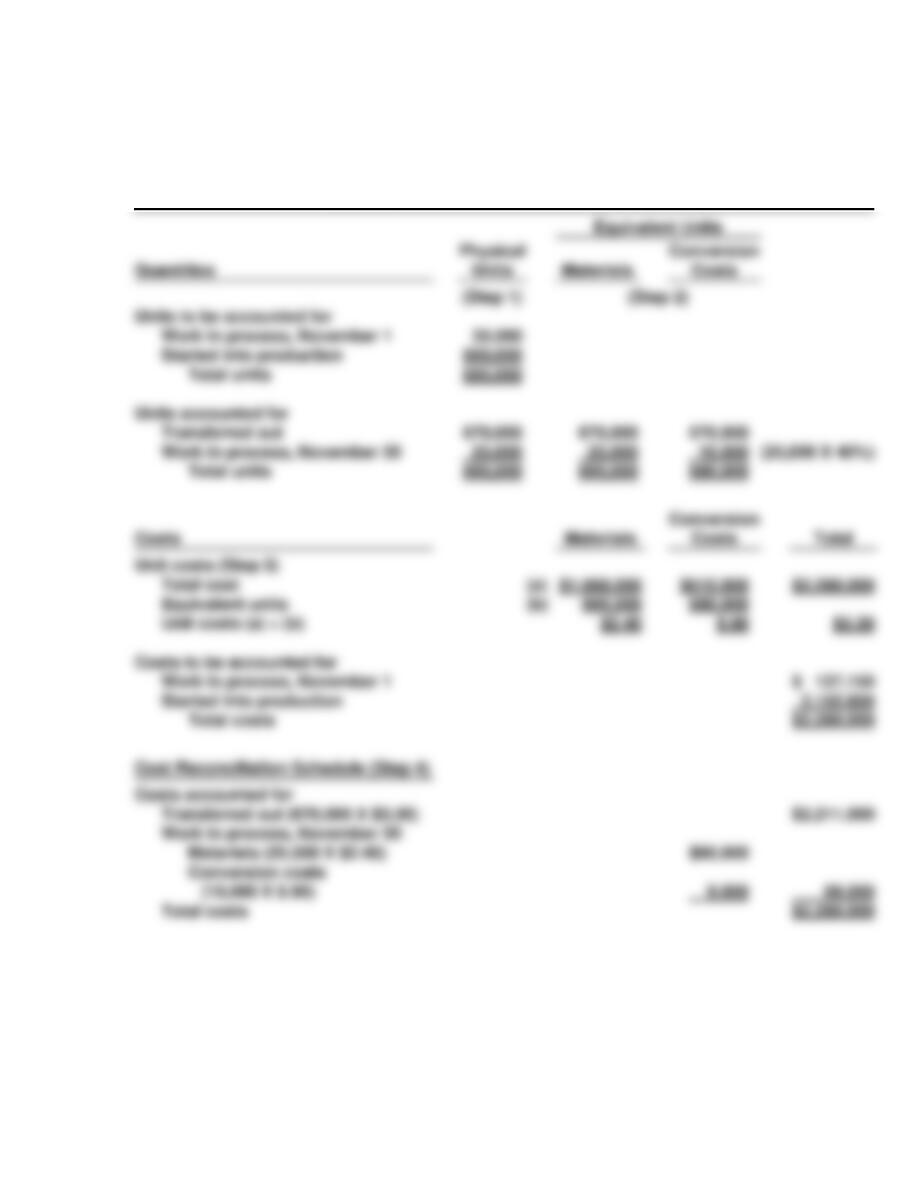

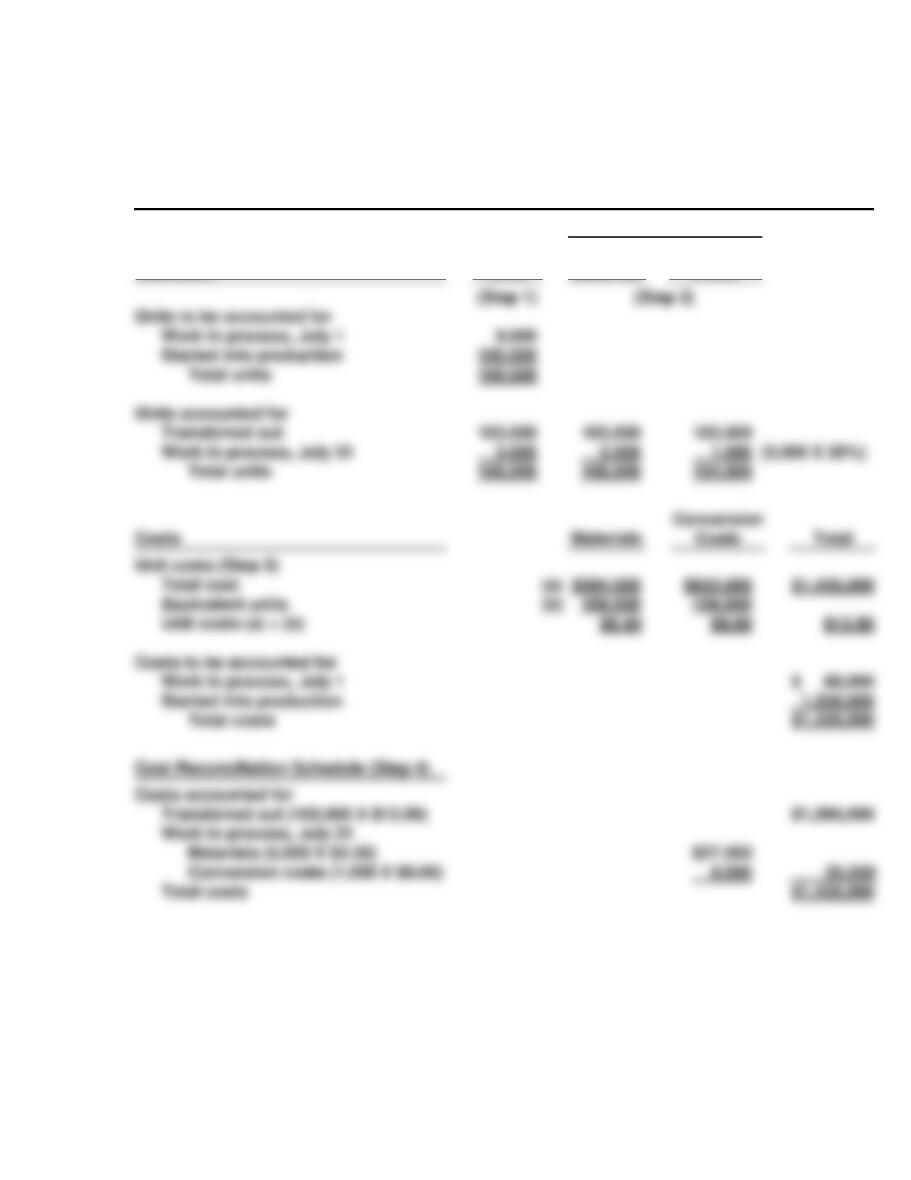

(c) FLORIDA BEACH COMPANY

Mixing Department

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

Units accounted for

Transferred out

Work in process, July 31

(5,000 X 20%)

Total units

108,000

Costs

Materials

Conversion

Total costs

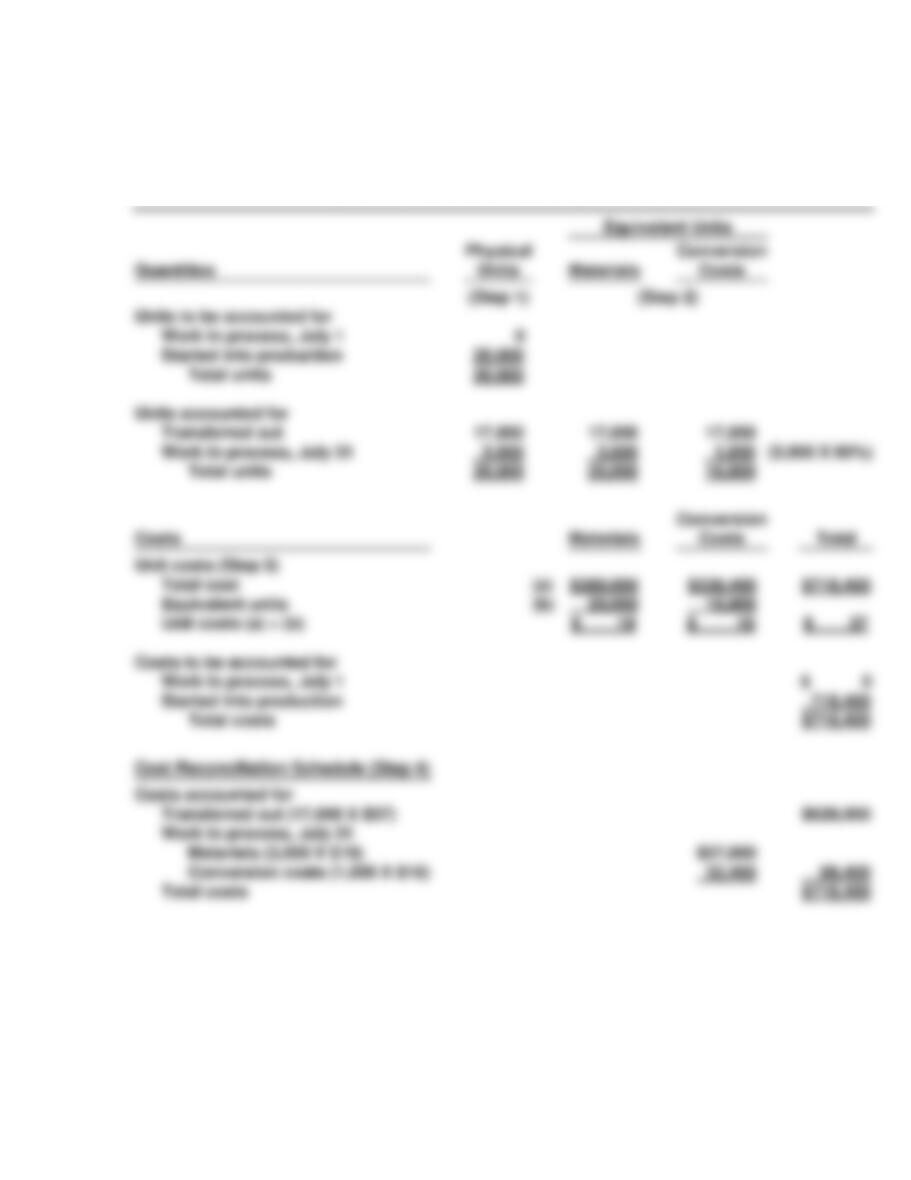

Cost Reconciliation Schedule (Step 4)

Total costs

$1,426,000

BYP 17-2 MANAGERIAL ANALYSIS

BYP 17-3 REAL-WORLD FOCUS

(a) The outer shell of the paintballs is made from a mixture that includes

water, sweeteners, food ingredients, and most importantly, gelatin. All

of the ingredients used to make paintballs are food grade, biodegradable

products. The “paint” filling inside a paintball is comprised of the same

inert ingredient used in cough syrup, as well as crayon wax.

(b) Materials: water, sweeteners, food ingredients, gelatin, “cough syrup

material”, crayon wax, and food coloring.

BYP 17-4 COMMUNICATION ACTIVITY

To: Diane Barone, Regional Sales Manager

From: Student, Accounting Manager

Re: Production Cost Reports

BYP 17-4 (Continued)

BYP 17-5 ETHICS CASE

(a) The stakeholders in this situation are:

BYP 17-6 CONSIDERING PEOPLE, PLANET, AND PROFIT

(a) Some of the costs that the company now faces include: