June transactions are summarized as follows:

a. Collections on account, $150,000.

b. Selling and administrative expenses incurred and paid, $33,000.

f. Wages incurred during June, $37,000. Labor time records for the month: Job 120,

$3,750; Job 121, $18,500; indirect labor, $14,750.

g. Wages paid in June include the balance in Wages Payable at May 31 plus $35,000 of wages incurred

during June.

h. Depreciation on plant and equipment, $3,000.

i. Manufacturing overhead allocated at the predetermined overhead allocation rate of 50% of direct

labor cost.

j. Jobs completed during the month: Job 120 with 300,000 Large Stars at a total cost of $47,275.

k. Sales on account: all of Job 120 for $105,000.

l. Adjusted for overallocated or underallocated manufacturing overhead.

Requirements

1. Journalize the transactions for the company.

2. Open T-accounts for the general ledger, the Raw Materials Inventory subsidiary ledger, the Work-in–

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

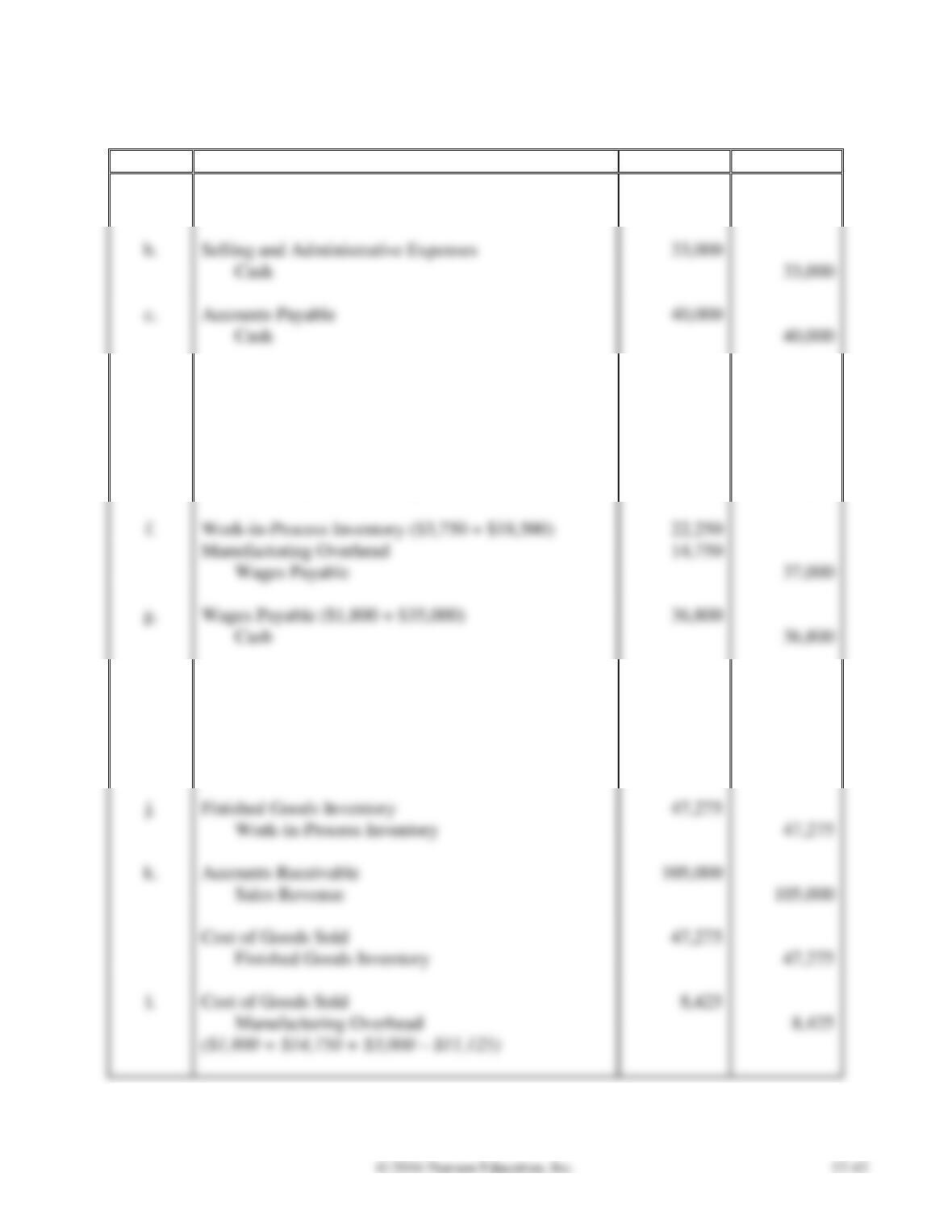

a.

Cash

150,000

Accounts Receivable

150,000

b.

Selling and Administrative Expenses

33,000

Cash

33,000

c.

Accounts Payable

40,000

Cash

40,000

d.

Raw Materials Inventory ($20,000 + $5,000)

25,000

Accounts Payable

25,000

e.

Work-in-Process Inventory ($550 + $7,750)

8,300

Manufacturing Overhead

1,800

Raw Materials Inventory

10,100

Work-in-Process Inventory ($3,750 + $18,500)

22,250

Manufacturing Overhead

14,750

Wages Payable

37,000

g.

Wages Payable ($1,800 + $35,000)

36,800

Cash

36,800

h.

Manufacturing Overhead

3,000

Accumulated Depreciation—plant and equipment

3,000

i.

Work-in-Process Inventory

11,125

Manufacturing Overhead ($22,250 × 50%)

11,125

j.

Finished Goods Inventory

47,275

47,275

k.

Accounts Receivable

105,000

Sales Revenue

105,000

Cost of Goods Sold

47,275

Finished Goods Inventory

47,275

l.

Cost of Goods Sold

8,425

Manufacturing Overhead

8,425

P17-32A, cont.

Requirement 2

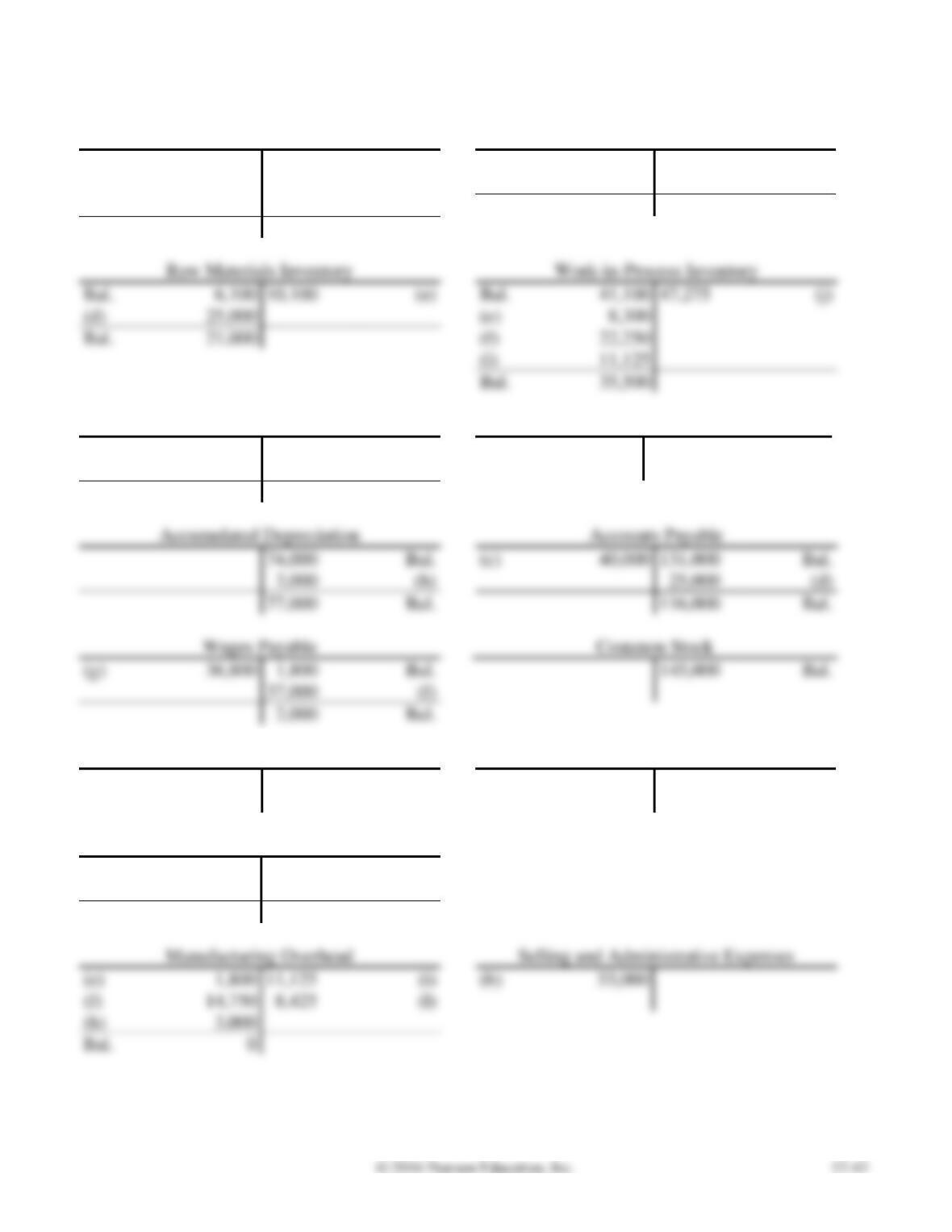

Cash

Accounts Receivable

Bal.

18,000

33,000

(b)

Bal.

180,000

150,000

(a)

(a)

150,000

40,000

(c)

(k)

105,000

36,800

(g)

Bal.

135,000

Bal.

58,200

Bal.

6,100

10,100

(e)

Bal.

47,275

(d)

(e)

8,300

Bal.

(i)

Finished Goods Inventory

Plant Assets

Bal.

21,100

47,275

(k)

Bal.

210,000

(j)

47,275

Bal.

21,100

74,000

Bal.

(c)

131,000

Bal.

3,000

(h)

25,000

(d)

77,000

Bal.

Bal.

(g)

1,800

145,000

Bal.

37,000

2,000

Retained Earnings

Sales Revenue

124,500

Bal.

105,000

(k)

Cost of Goods Sold

(k)

47,275

(l)

8,425

Bal.

55,700

Manufacturing Overhead

(e)

1,800

11,125

(b)

8,425

(h)

3,000

Bal.

P17-32A, cont.

Requirement 2, cont.

Raw Materials Inventory subsidiary ledger:

Bal.

4,100

8,300

Bal.

2,000

1,800

(d)

20,000

(d)

5,000

Bal.

15,800

Bal.

5,200

Work-in-Process Inventory subsidiary ledger:

Job 120

Job 121

Bal.

41,100

47,275

(j)

Bal.

(e)

0

7,750

(e)

550

(f)

3,750

(f)

18,500

(i)

1,875

(i)

9,250

Bal.

0

Bal.

35,500

Balance equals balance of Work-in-Process Inventory, $35,500 ($0 + $35,500).

Bal.

9,400

47,275

Bal.

11,700

(j)

47,275

Bal.

9,400

P17-32A, cont.

Requirement 3

LEARNING STARS

Trial Balance

June 30, 2016

Account

Debit

Credit

Cash

$ 58,200

Accounts Receivable

135,000

Inventories:

Raw Materials

21,000

35,500

Finished Goods

21,100

Plant Assets

210,000

Accumulated Depreciation

$ 77,000

Accounts Payable

116,000

Wages Payable

Common Stock

145,000

Retained Earnings

124,500

Sales Revenue

105,000

Cost of Goods Sold

55,700

Selling and Administrative Expenses

33,000

Totals

$ 569,500

$ 569,500

P17-32A, cont.

Requirement 4

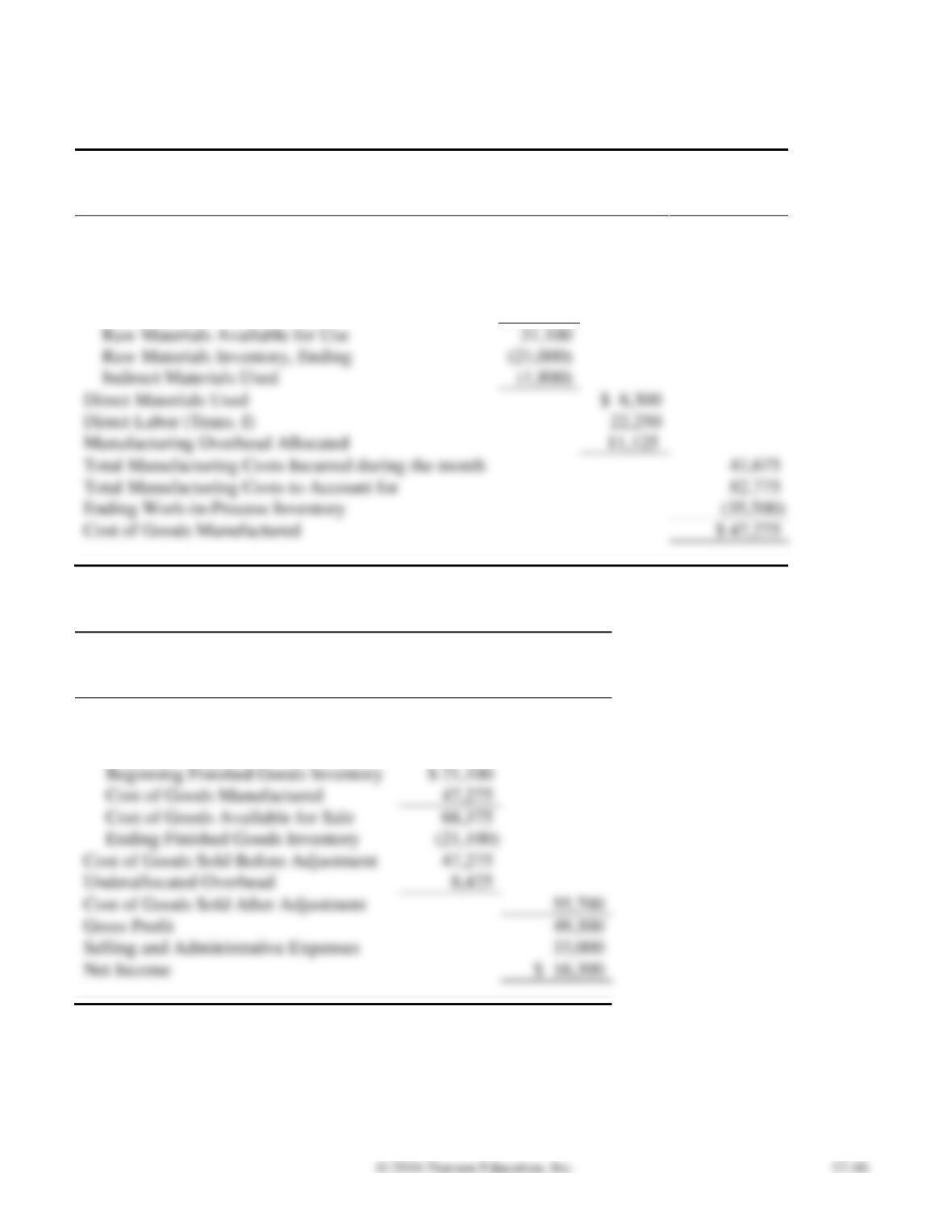

LEARNING STARS

Schedule of Cost of Goods Manufactured

Month Ended June 30, 2016

Beginning Work-in-Process Inventory

$ 41,100

Direct Materials Used:

Raw Materials Inventory, Beginning

$ 6,100

Purchases

25,000

Raw Materials Available for Use

31,100

Raw Materials Inventory, Ending

(21,000)

Indirect Materials Used

(1,800)

Direct Materials Used

Direct Labor (Trans. f)

Manufacturing Overhead Allocated

11,125

Total Manufacturing Costs Incurred during the month

Total Manufacturing Costs to Account for

Ending Work-in-Process Inventory

Cost of Goods Manufactured

$ 47,275

Requirement 5

LEARNING STARS

Income Statement

Month ended June 30, 2016

Sales Revenue

$ 105,000

Cost of Goods Sold:

(21,100)

Cost of Goods Sold Before Adjustment

Underallocated Overhead

Gross Profit

Selling and Administrative Expenses

Net Income

P17-33A Using job order costing in a service company

Learning Objective 6

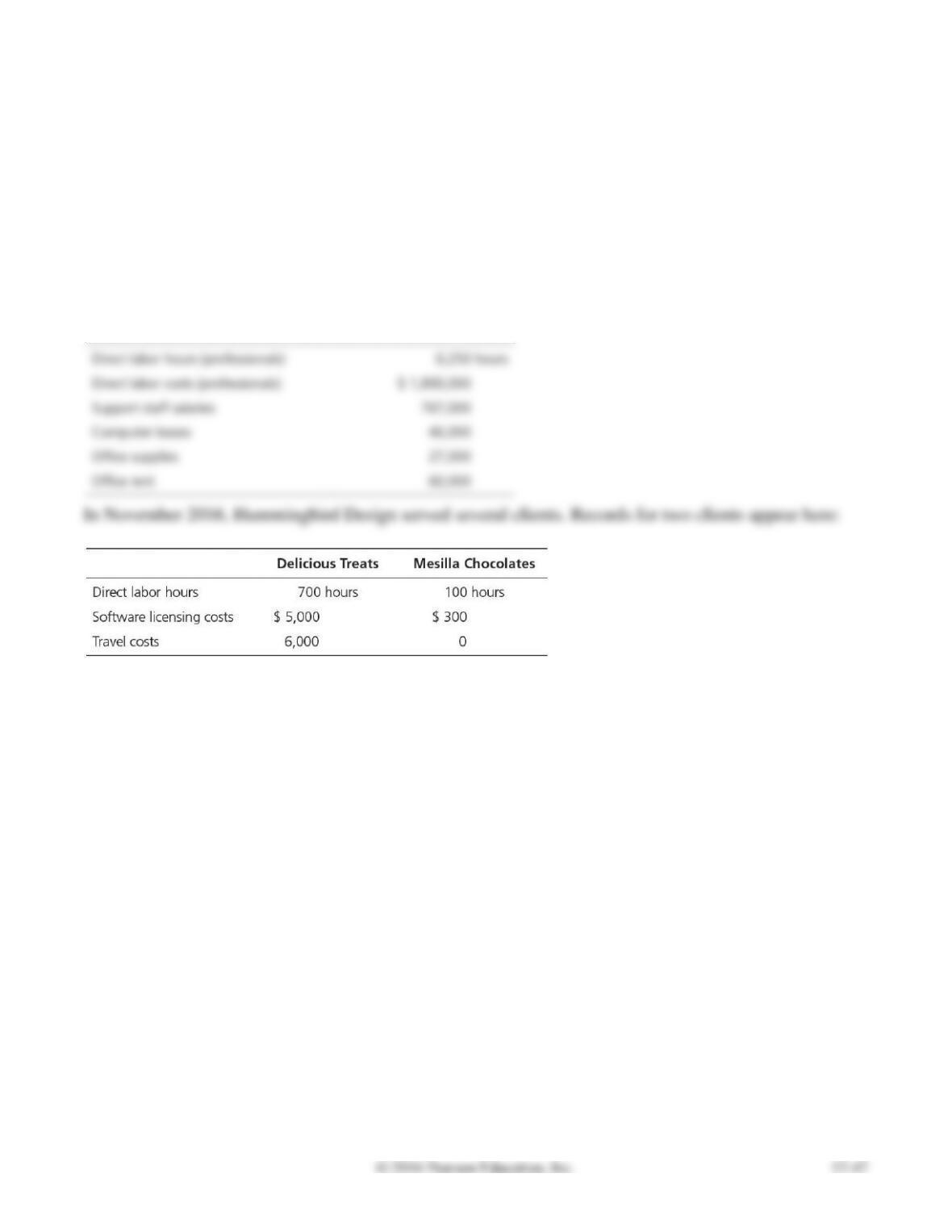

2. Delicious Treats $313,400

(Requirements 1 and 2 only)

Hummingbird Design, Inc. is a Web site design and consulting firm. The firm uses a job order costing

system in which each client is a different job. Hummingbird Design assigns direct labor, licensing costs,

and travel costs directly to each job. It allocates in– direct costs to jobs based on a predetermined

overhead allocation rate, computed as a percentage of direct labor costs.

At the beginning of 2016, managing partner Sally Simone prepared the following budget estimates:

Requirements

1. Compute Hummingbird Design’s direct labor rate and its predetermined overhead allocation rate for

2016.

2. Compute the total cost of each job.

3. If Simone wants to earn profits equal to 20% of service revenue, what fee should she charge each of

these two clients?

4. Why does Hummingbird Design assign costs to jobs?

SOLUTION

Requirement 1

$1,800,000

Hourly rate

$1,800,000 per year

Requirement 2

HUMMINGBIRD DESIGN, INC.

Total Cost of Delicious Treats’ and Mesilla Chocolates’ Jobs

For the month of November

P17-33A, cont.

Requirement 3

If profits are 20% of sales, then total costs are 80% of sales.

Therefore, Sales Revenue = Total Costs / 80%.

Requirement 4

Hummingbird Design, Inc. assigns costs to jobs to help the company set fees that cover all costs and

Problems (Group B)

P17-34B Analyzing cost data, recording completion and sales of jobs

Learning Objectives 1, 2, 4

5. Gross profit $400

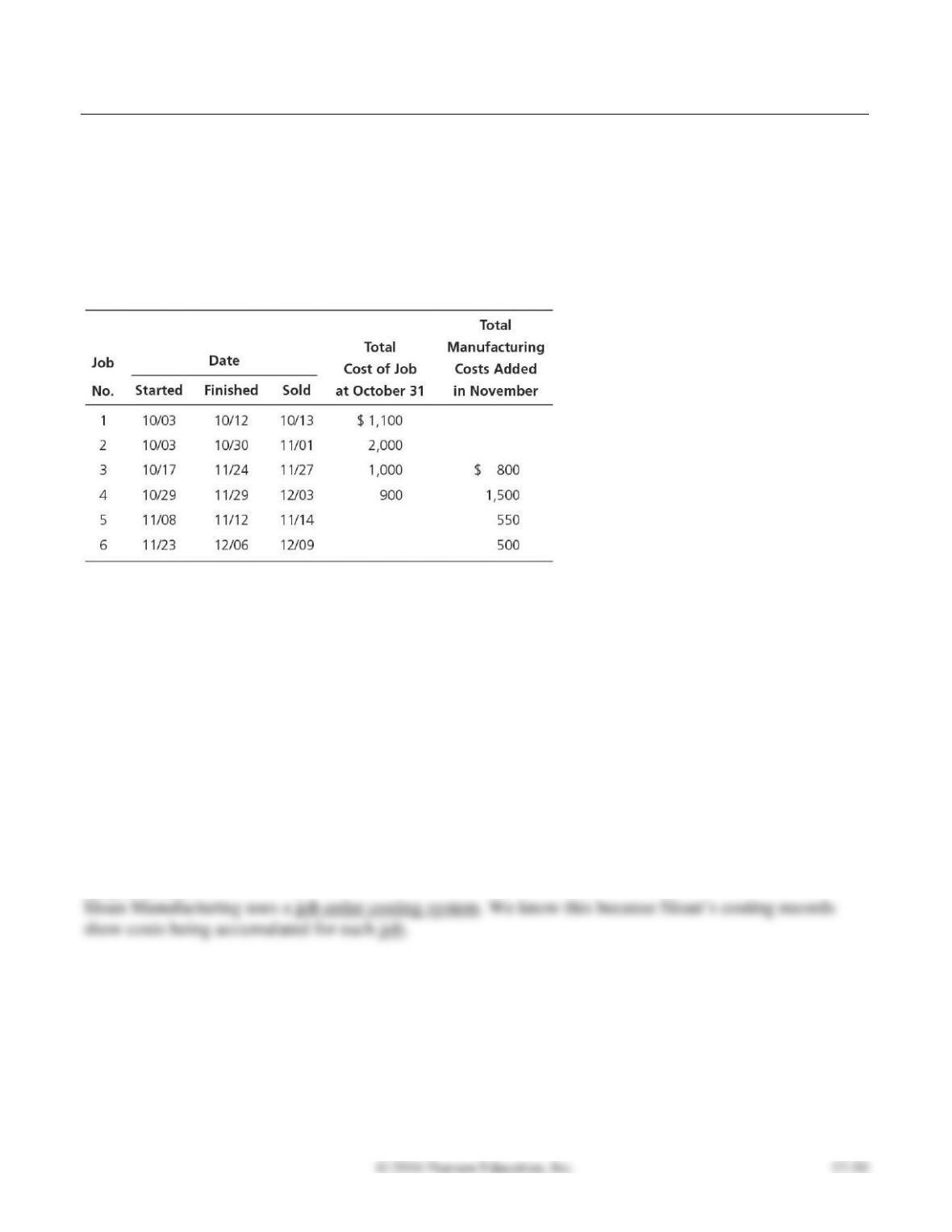

Sloan Manufacturing makes carrying cases for portable electronic devices. Its costing records yield the

following information:

Requirements

1. Which type of costing system is Sloan using? What piece of data did you base your answer on?

2. Use the dates in the table to identify the status of each job at October 31 and November 30. Compute

Sloan’s account balances at October 31 for Work–in-Process Inventory, Finished Goods Inventory,

and Cost of Goods

Sold. Compute, by job, account balances at November 30 for Work-in-Process Inventory, Finished

Goods Inventory, and Cost of Goods Sold.

3. Prepare journal entries to record the transfer of completed jobs from Work-in– Process Inventory to

Finished Goods Inventory for October and November.

4. Record the sale of Job 3 for $2,200 on account.

5. What is the gross profit for Job 3?

SOLUTION

Requirement 1

Requirement 2

SLOAN MANUFACTURING

Computation of Work-in-Process Inventory, Finished Goods Inventory,

and Cost of Goods Sold for October and November

Sold

Job

Cost

$ 2,000

$ 2,000

$ 2,400

$ 2,400

Work-in-Process

Finished Goods

Cost of Goods

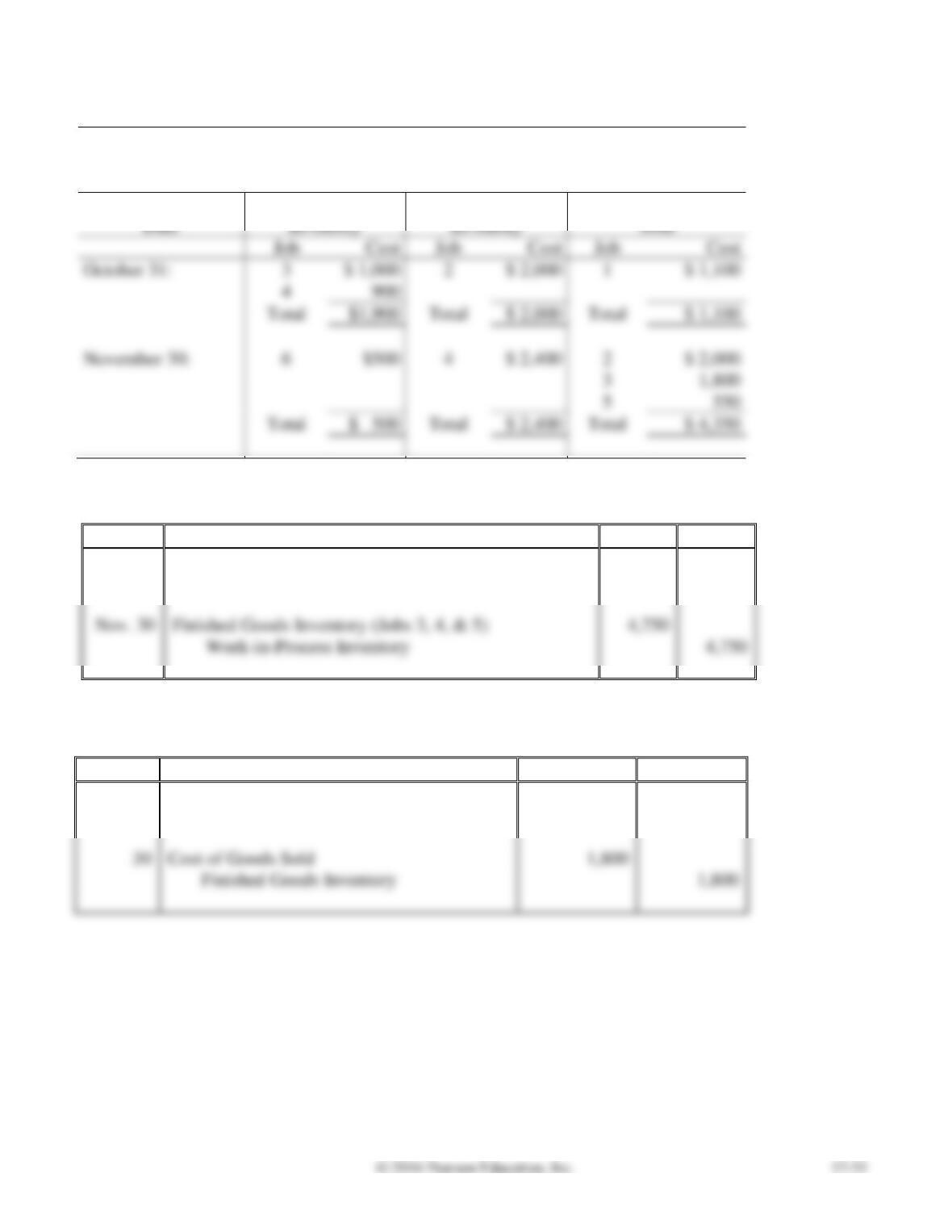

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Finished Goods Inventory (Jobs 1 & 2)

3,100

Work-in-Process Inventory

3,100

Finished Goods Inventory (Jobs 3, 4, & 5)

4,750

Work-in-Process Inventory

4,750

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Nov. 30

Accounts Receivable

2,200

Sales Revenue

2,200

Cost of Goods Sold

1,800

Finished Goods Inventory

1,800

Requirement 5

The gross profit for Job 3 is:

P17-35B Preparing and using a job cost record to prepare journal entries

Learning Objectives 2, 3, 4

1. Cost per DVD $0.39

Tu Technology Co. manufactures CDs and DVDs for computer software and entertainment companies.

Tu uses job order costing.

On November 2, Tu began production of 5,700 DVDs, Job 423, for Cyclorama Pictures for $1.50 sales

price per DVD. Tu promised to deliver the DVDs to Cyclorama by November 5. Tu incurred the

following costs:

Requirements

1. Prepare a job cost record for Job 423. Calculate the predetermined overhead allocation rate; then

allocate manufacturing overhead to the job.

2. Journalize in summary form the requisition of direct materials and the assignment of direct labor and

the allocation of manufacturing overhead to Job 423. Wages are not yet paid.

3. Journalize completion of the job and the sale of the 5,700 DVDs on account.

SOLUTION

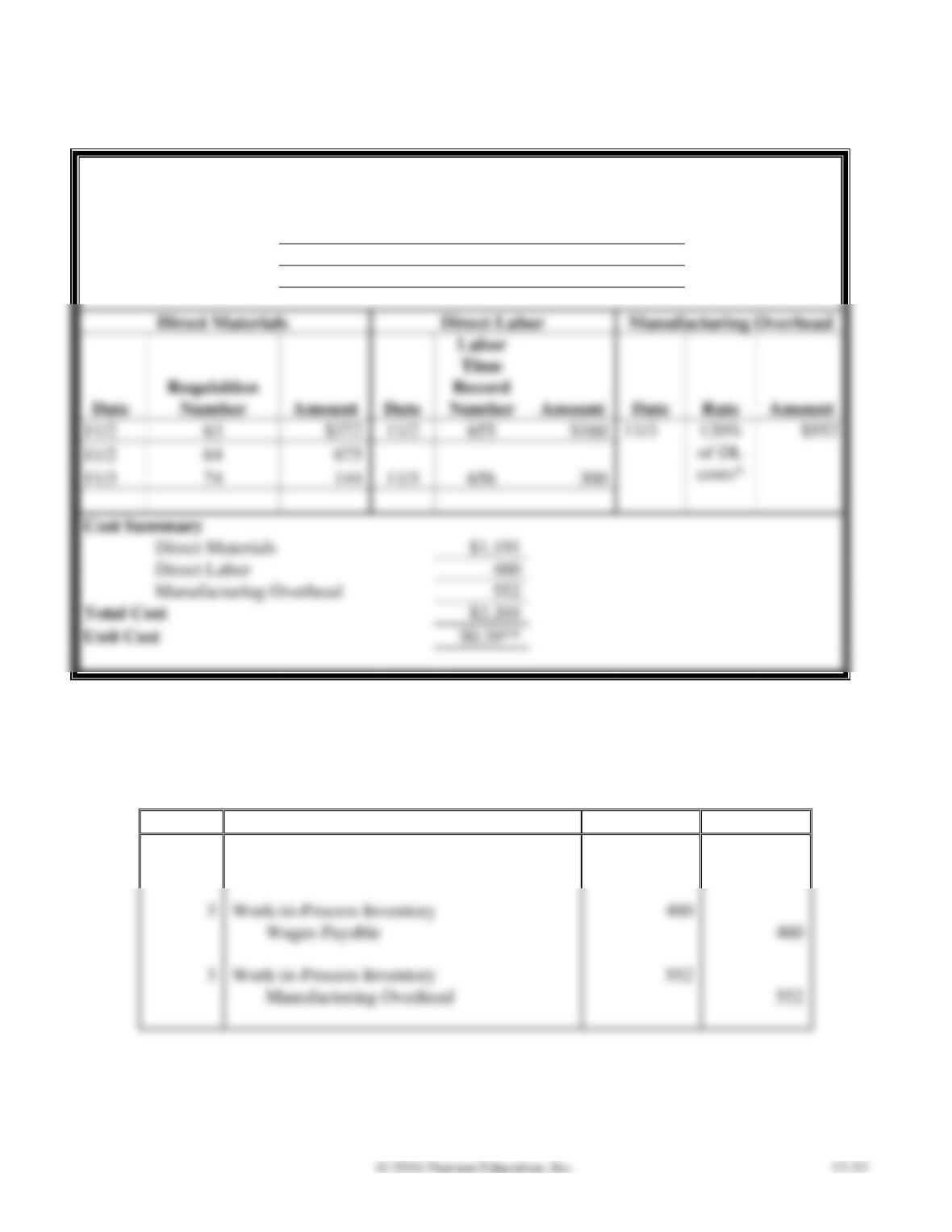

Requirement 1

JOB COST RECORD

Job Number

423

Customer

Cyclorama Pictures

Job Description

5,700 DVDs

11/2

11/2

11/3

Cost Summary

Direct Materials

Direct Labor

Manufacturing Overhead

Total Cost

Unit Cost

*$564,000 / $470,000 = 120%

**$2,203 / 5,700 DVDs = $0.39 per DVD (rounded)

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Nov. 3

Work-in-Process Inventory

1,191

Raw Materials Inventory

1,191

Work-in-Process Inventory

Wages Payable

Work-in-Process Inventory

P17-35B, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Nov. 3

Finished Goods Inventory

2,203

Work-in-Process Inventory

2,203

Accounts Receivable (5,700 DVDs × $1.50 per DVD)

8,550

Sales Revenue

8,550

Cost of Goods Sold

2,203

Finished Goods Inventory

2,203

P17-36B Accounting for transactions, construction company

Learning Objectives 2, 3, 4

3. WIP Bal. $272,200

Sunrise Construction, Inc. is a home builder in Arizona. Sunrise uses a job order costing system in

which each house is a job. Because it constructs houses, the company uses an account titled

Construction Overhead. The company applies overhead based on estimated direct labor costs. For the

year, it estimated construction overhead of $1,300,000 and total direct labor cost of $3,250,000. The

following events occurred during August:

a. Purchased materials on account, $450,000.

b. Requisitioned direct materials and used direct labor in construction. Recorded the materials

requisitioned.

c. The company incurred total wages of $250,000. Use the data from Item b to assign the wages.

Wages are not yet paid.

Requirements

1. Calculate Sunrise’s predetermined overhead allocation rate for the year.

2. Prepare journal entries to record the events in the general journal.

3. Open T-accounts for Work-in-Process Inventory and Finished Goods Inventory. Post the appropriate

entries to these accounts, identifying each entry by letter. Determine the ending account balances,

assuming that the beginning balances were zero.

4. Add the costs of the unfinished houses, and show that this total amount equals the ending balance in

the Work-in-Process Inventory account.

5. Add the cost of the completed house that has not yet been sold, and show that this equals the ending

balance in Finished Goods Inventory.

6. Compute gross profit on the house that was sold. What costs must gross profit cover for Sunrise

Construction?

SOLUTION

Requirement 1

P17-36B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Aug. 31

a.

Raw Materials Inventory

450,000

Accounts Payable

450,000

b.

263,000

Raw Materials Inventory

263,000

c.

188,000

62,000

Wages Payable

250,000

d.

Construction Overhead

6,800

Accumulated Depreciation––Equipment

6,800

e.

Construction Overhead

42,000

Cash

34,000

Prepaid Insurance

8,000

75,200

Construction Overhead

75,200

g.

254,000

254,000

h.

Accounts Receivable

230,000

Sales Revenue

230,000

142,800

Finished Goods Inventory

142,800

1$51,000 + $66,000 + $63,000 + $83,000 = $263,000

2$43,000 + $36,000 + $57,000 + $52,000 = $188,000

3$250,000 – $188,000 = $62,000

4 $188,000 × 40% = $75,200

6From above, House 404 = $142,800

P17-36B, cont.

Requirement 3

Work-in-Process Inventory

Finished Goods Inventory

(b) DM

254,000

(g) COGM

142,800

(h) COGS

Bal.

(f) OH

Bal.

Requirement 4

SUNRISE CONSTRUCTION, INC.

Reconciliation of Work-in-Process Inventory Subsidiary

and Control Accounts

August 31

Requirement 5

SUNRISE CONSTRUCTION, INC.

Reconciliation of Finished Goods Inventory Subsidiary

and Control Accounts

August 31

P17-36B, cont.

Requirement 6

SUNRISE CONSTRUCTION, INC.

Gross Profit on Homes Sold in August

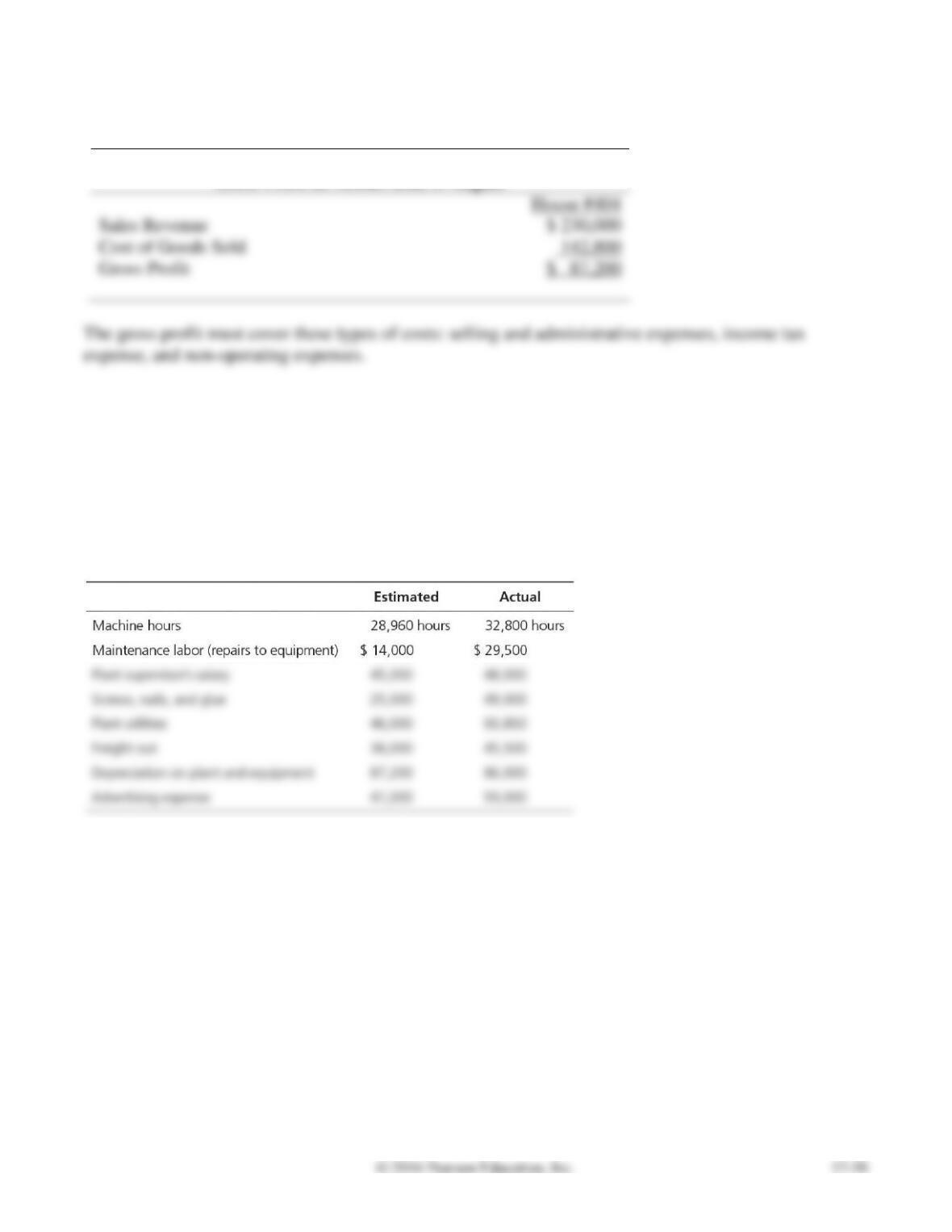

P17-37B Accounting for manufacturing overhead

Learning Objectives 3, 5

1. $7.50 per machine hour

Custom Woods manufactures jewelry boxes. The primary materials (wood, brass, and glass) and direct

labor are assigned directly to the products. Manufacturing overhead costs are allocated based on

machine hours. Data for 2016 follow:

Requirements

1. Compute the predetermined overhead allocation rate.

2. Post actual and allocated manufacturing overhead to the Manufacturing Overhead T-account.

3. Prepare the journal entry to adjust for underallocated or overallocated overhead.

4. The predetermined overhead allocation rate usually turns out to be inaccurate. Why don’t

accountants just use the actual manufacturing overhead rate?