CHAPTER 17

LEARNING OBJECTIVES

1. DISCUSS THE USES OF A PROCESS COST SYSTEM

AND HOW IT COMPARES TO A JOB ORDER SYSTEM.

2. EXPLAIN THE FLOW OF COSTS IN A PROCESS

COST SYSTEM AND THE JOURNAL ENTRIES TO

ASSIGN MANUFACTURING COSTS.

CHAPTER REVIEW

Process Cost Systems

1. (L.O. 1) Process cost systems are used to apply costs to similar products that are mass

produced in a continuous fashion, such as the production of ice cream, steel or soft drinks. In

comparison, costs in a job order cost system are assigned to a specific job, such as the

construction of a customized home, the making of a motion picture, or the manufacturing of a

specialized machine.

3. The major differences between a job order cost system and a process cost system are as follows:

Job Order Process

Feature Cost System Cost System

Work in process One for each job One for each process

accounts

Process Cost Flow

4. (L.O. 2) In the Tyler Company example in the text book, manufacturing consists of two

processes: machining and assembly. In the Machining Department, the raw materials are shaped,

honed, and drilled. In the Assembly Department, the parts are assembled and packaged.

Assigning Manufacturing Costs

6. All raw materials issued for production are a materials cost to the producing department. Materials

requisition slips may be used in a process cost system, but fewer requisitions are generally

required than in a job order cost system, because the materials are used for processes rather

than for specific jobs. In the case of the Tyler Company, the entry to record the materials used is:

8. The basis for allocating the overhead costs to the production departments in an objective and

equitable manner is the activity that “drives” or causes the costs. A primary driver of overhead

costs in continuous manufacturing operations is machine time used, not direct labor. Thus,

machine hours are widely used in allocating manufacturing overhead costs. In the case of the

Tyler Company, the entry to allocate overhead is:

Equivalent Units

10. (L.O. 3) A major step in process cost accounting is the calculation of equivalent units. Equivalent

units of production measure the work done during the period, expressed in fully completed

units. This concept is used to determine the cost per unit of completed product.

11. The formula to compute equivalent units of production under the weighted-average method is as

follows:

Units Completed and

Transferred Out

+

Equivalent Units of

Ending Work in

Process

=

Equivalent Units of

Production

14. The two equivalent unit computations are as follows:

Equivalent Units

Production Cost Report

15. (L.O. 4) A production cost report is the key document used by management to understand the

activities in a department because it shows the production quantity and cost data related to that

department. In order to be ready to complete a production cost report, the company must perform

four steps:

16. The computation of physical units involves:

17. In computing unit costs, production costs are expressed in terms of equivalent units of production.

When equivalent units are different for materials and conversion costs, the formulas for computing

unit costs are as follows:

18. The cost reconciliation schedule shows that the total costs accounted for equal the total costs

to be accounted for as follows:

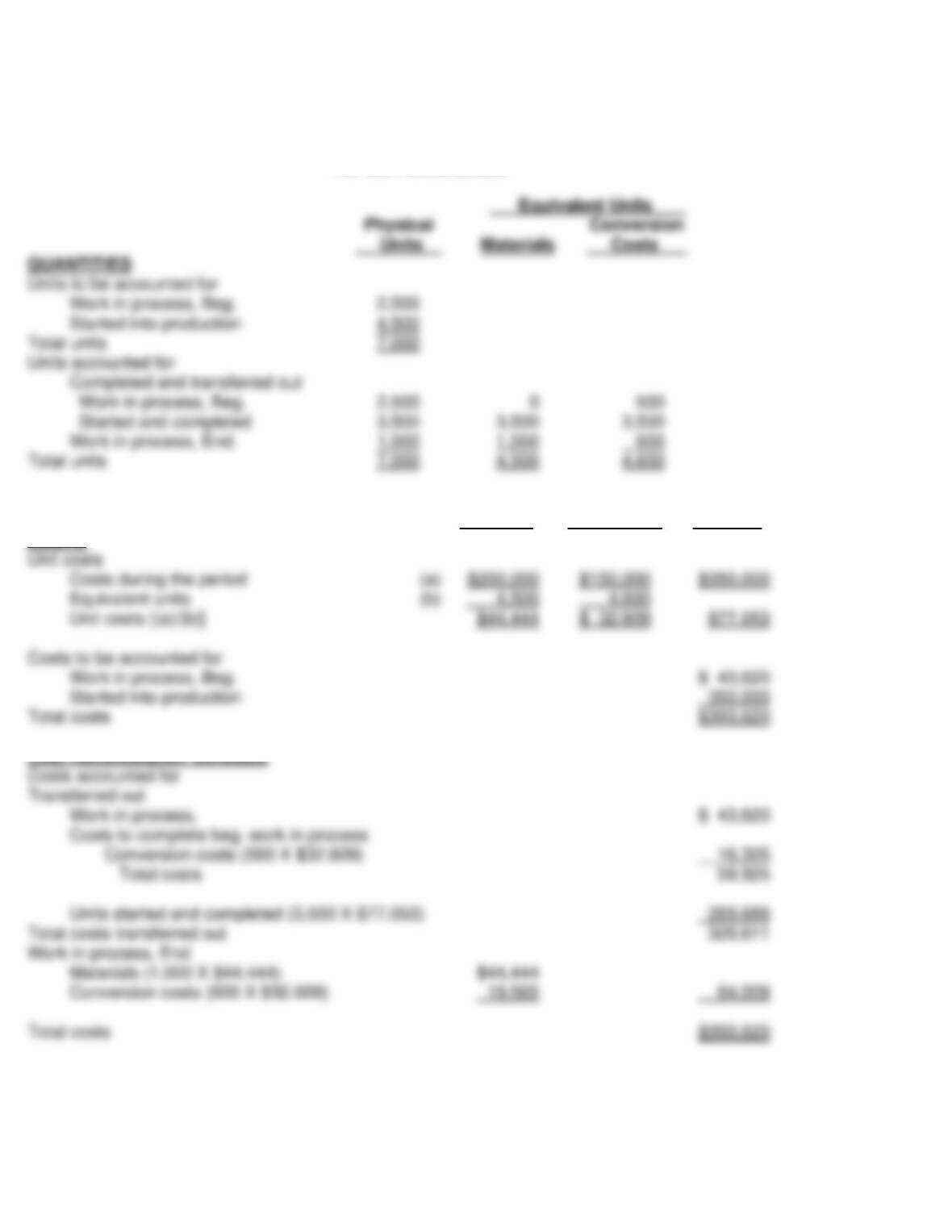

19. Assume the Processing Department of Silva Company has the following additional cost

information:

20. Silva Company’s Processing Department Production Cost Report at the end of the period is as

follows:

Processing Department

Production Cost Report

For the Period Ended

Equivalent Units

Physical Conversion

Conversion

Materials Costs Total

COSTS

Cost Reconciliation Schedule

Operations Costing

Equivalent Units Using the FIFO Method

*23. The equivalent units for material costs of the Processing Department under the FIFO method are

computed as follows:

*24. The equivalent units for conversion costs of the Processing Department under the FIFO method

are computed as follows:

Production Cost Report Using the FIFO Method

*25. Assume the Processing Department of Silva Company has the following additional cost

information:

*26. Silva Company’s Processing Department Production Cost Report at the end of the period using

the FIFO method is as follows:

Processing Department

Production Cost Report

For the Period Ended

Conversion

Materials Costs Total

COSTS

LECTURE OUTLINE

A. Uses of Process Cost Systems.

B. Similarities and Differences Between Job Order Cost and Process Cost

Systems.

1. In a process cost system, costs are tracked through a series of connected

3. Job order cost and process cost systems are similar in three ways:

4. There are four main differences between the two cost systems:

C. Process Cost Flow.

1. The company can add materials, labor, and manufacturing overhead in

each production department.

D. Assigning Manufacturing Costs.

1. The accumulation of the costs of materials, labor, and manufacturing

overhead is the same in a process cost system as in a job order cost

system.

a. All raw materials issued for production are a materials cost to the

producing department. A process cost system may use materials

requisition slips, but fewer requisitions are generally required than

in a job order system, because the materials are used for processes

rather than specific jobs.

4. The entry to record units completed and transferred to the warehouse is

a debit to Finished Goods Inventory and a credit to Work in Process.

5. The entry to record the sale of goods is a debit to Cost of Goods Sold

and a credit to Finished Goods Inventory.

MANAGEMENT INSIGHT

Some companies continue to assign manufacturing overhead on the basis of

direct labor despite the fact that there is no cause-and–effect relationship between

labor and overhead. In such cases, the overhead rates may be misleading.

What is the result if a company uses the wrong “cost driver” to assign manufac–

turing overhead?

E. Equivalent Units.

1. Equivalent units of production measure the work done during the period,

expressed in fully completed units.

4. The weighted-average method is most commonly used to compute

equivalent units of production.

MANAGEMENT INSIGHT

In recent years more companies have been remanufacturing a wide variety of

products including cell phones, car parts, and medical equipment. Rising

commodity prices and regulations requiring that certain electronic items be recycled

has fueled this trend.

In what ways might the relative composition (materials, labor, and overhead) of a

remanufactured product’s cost differ from that of a newly made product?

F. Production Cost Report.

1. In order to complete a production cost report, the company must perform

four steps:

2. The first step in completing a production cost report requires computing

physical unit flow.

3. The second step in completing a production cost report requires computing

equivalent units of production.

4. The third step in completing a production cost report requires computing

unit production costs.

5. The fourth step in completing a production cost report requires preparing

a cost reconciliation schedule.

G. Preparing the Production Cost Report.

1. The production cost report contains both quantity and cost data for a

production department.

*H. Equivalent Units Under FIFO.

1. Under the FIFO method, companies compute equivalent units on a first–

in, first-out basis.

4. The units started and completed during the current period are the units

transferred out minus the units in beginning work in process.

a. When companies add materials at the beginning of the process, no

additional materials costs are required to complete the beginning

work in process. However, sometimes companies add materials

evenly throughout the process. When this occurs, computations for

materials would mirror those for conversion costs.

7. The unit production costs are based entirely on the production costs

incurred during the month. The costs in the beginning work in process

are ignored because they were incurred on work done in the preceding

month.

8. In preparing a cost reconciliation schedule under the FIFO method:

20 MINUTE QUIZ

Circle the correct answer.

True/False

1. Costs are assigned to each specific job in a process cost system.

True False

2. In a process cost system, total costs are determined at the end of a period of time, such

as a month.

True False

3. In a process cost system, the unit cost is total manufacturing costs divided by the

equivalent units produced during the period.

True False

4. The accumulation of the costs of materials, labor, and manufacturing overhead is the

same in a process cost system as in a job order cost system.

True False

5. More materials requisitions are generally required in a process cost system than in a job

order cost system.

True False

6. Equivalent units of production equals units completed and transferred out + units in

beginning work in process.

True False

7. Two equivalent unit computations are necessary—one for materials and the other for

conversion costs.

True False

8. The first step in preparing a production cost report is to compute the equivalent units of

production.

True False

9. The cost reconciliation schedule shows that the total costs accounted for equal the total

costs to be accounted for.

True False

*10. Units in work in process at the beginning of the period are included in units “started and

completed” under the FIFO method.

True False

Multiple Choice

1. Which of the following is not a step in preparing a production cost report?

a. Prepare a cost reconciliation schedule.

b. Compute equivalent units of production.

c. Compute the physical unit flow.

d. Assign costs to particular jobs.

2. A department has no beginning work in process, has started 80,000 units and completed

50,000 units. Its ending work in process is 30,000 units, 60% complete as to conversion

costs and fully complete as to materials. Its equivalent units for conversion costs are

a. 50,000.

b. 80,000.

c. 68,000.

d. 44,000.

3. In process costing, the computation of unit production costs requires

a. the accumulation of material and conversion costs in work in process for each

department or process.

b. the computation of equivalent units for material and conversion costs.

c. both a and b.

d. neither a nor b.

4. Which of the following is not included in a production cost report?

a. Costs accounted for.

b. Entries to assign cost.

c. Units accounted for.

d. Units to be accounted for.

5. Unit costs for materials and conversion costs amount to $4 and $5 respectively. The

ending work in process costs for 8,000 units (100% complete as to material and 70%

complete as to conversion costs) amount to

a. $60,000.

b. $72,000.

c. $44,000.

d. $40,000.

ANSWERS TO QUIZ

True/False

Multiple Choice