CHAPTER 15 – 1

CHAPTER 16

SHORT-TERM FINANCIAL PLANNING

Answers to Concepts Review and Critical Thinking Questions

1. These are firms with relatively long inventory periods and/or relatively long receivables periods. Thus,

such firms tend to keep inventory on hand, and they allow customers to purchase on credit and take a

relatively long time to pay.

3. a. Use: The cash balance declined by $200 to pay the dividend.

b. Source: The cash balance increased by $500 assuming the goods bought on payables credit

were sold for cash.

c. Use: The cash balance declined by $900 to pay for the fixed assets.

d. Use: The cash balance declined by $625 to pay for the higher level of inventory.

e. Use: The cash balance declined by $1,200 to pay for the redemption of debt.

6. It lengthened its payables period, thereby shortening its cash cycle. There was no effect on the

operating cycle.

7. Their receivables period increased, thereby increasing their operating and cash cycles.

8. It is sometimes argued that large firms “take advantage of” smaller firms by threatening to take their

business elsewhere. However, considering a move to another supplier to get better terms is the nature

of competitive free enterprise.

CHAPTER 15 – 2

Solutions to Questions and Problems

NOTE: All end-of–chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

1. a. No change. A dividend paid for by the sale of debt will not change cash since the cash raised

from the debt offer goes immediately to shareholders.

b. No change. The real estate is paid for by the cash raised from the debt, so this will not change

the cash balance.

g. No change. Accounts receivable will increase, but cash will not increase until the sales are paid

off.

h. Decrease. The interest is paid with cash, which will reduce the cash balance.

i. Increase. When payments for previous sales, or accounts receivable, are paid off, the cash balance

increases since the payment must be made in cash.

CHAPTER 15 – 3

2. The total liabilities and equity of the company are the book value of equity, plus current liabilities and

long-term debt, so:

Total liabilities and equity = $13,465 + 1,630 + 8,200

Total liabilities and equity = $23,295

Since total assets must equal total liabilities and equity, we can solve for cash as:

Cash = Total assets – Fixed assets – (Accounts receivable + Inventory)

Cash = $23,295 – 18,380 – 3,905

Cash = $1,010

3. a. Increase. If receivables go up, the time to collect the receivables would increase, which increases

the operating cycle.

b. Increase. If credit repayment times are increased, customers will take longer to pay their bills,

which will lead to an increase in the operating cycle.

4. a. Increase; Increase. If the terms of the cash discount are made less favorable to customers, the

accounts receivable period will lengthen. This will increase both the cash cycle and the operating

cycle.

b. Increase; No change. This will shorten the accounts payable period, which will increase the cash

cycle. It will have no effect on the operating cycle since the length of the operating cycle is not

affected by the payables period.

CHAPTER 15 – 4

d. Decrease; Decrease. Fewer raw materials purchased will reduce the inventory period, which will

decrease both the cash cycle and the operating cycle.

5. a. 45-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 45) / 90 = 1/2 of current sales are collected.

Q1

Q2

Q3

Q4

Beginning receivables

$330

$293

$338

$315

Sales

585

675

630

895

Cash collections

623

630

653

763

Ending receivables

$293

$338

$315

$448

Q1

Q2

Q3

Q4

Beginning receivables

$330

$390

$450

$420

Sales

585

Cash collections

525

Ending receivables

$390

$450

$420

$597

b. 60-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 60) / 90 = 1/3 of current sales are collected.

c. 30-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 30) / 90 = 2/3 of current sales are collected.

Beginning receivables

$330

$195

$225

$210

Sales

585

675

630

895

Cash collections

720

645

645

807

Ending receivables

$195

$225

$210

$298

CHAPTER 15 – 5

6. The operating cycle is the inventory period plus the receivables period. The inventory turnover and

inventory period are:

Inventory turnover = COGS / Average inventory

Inventory turnover = $77,681 / [($9,605 + 11,302) / 2]

Inventory turnover = 7.4311 times

Receivables period = 365 days / Receivables turnover

Receivables period = 365 days / 27.4352

Receivables period = 13.30 days

So, the operating cycle is:

Payables turnover = 14.6970 times

Payables period = 365 days / Payables turnover

Payables period = 365 days / 14.6970

Payables period = 24.83 days

So, the cash cycle is:

Cash cycle = 62.42 days – 24.83 days

Cash cycle = 37.59 days

The firm is receiving cash on average 37.59 days after it pays its bills.

CHAPTER 15 – 6

8. a. The payables period is zero since the company pays immediately. The payment in each period is

30 percent of next period’s sales, so:

Q1 Q2 Q3 Q4

Payment of accounts $229.50 $274.50 $252.00 $234.60

b. Since the payables period is 90 days, the payment in each period is 30 percent of the current

period sales, so:

9. Since the payables period is 60 days, payables in each period = 2/3 of last quarter’s orders, and 1/3 of

this quarter’s orders, or 2/3(.75)(Current sales) + 1/3(.75)(Next period sales)

Q1

Q2

Q3

Q4

Payment of accounts

$1,445.00

$1,680.00

$1,883.75

$1,865.00

Wages, taxes, other expenses

547.50

639.00

738.00

784.50

Long-term financing expenses

120.00

120.00

120.00

120.00

Total

$2,112.50

$2,439.00

$2,741.75

$2,769.50

10. a. The November sales must have been the total uncollected sales minus the uncollected sales from

December, divided by the collection rate two months after the sale, so:

November sales = ($97,000 – 71,000) / .15

November sales = $173,333.33

CHAPTER 15 – 7

b. The December sales are the uncollected sales from December divided by the sum of the collection

rates from the previous two months’ sales, so:

11. The sales collections each month will be:

Sales collections = .35(Current month sales) + .60(Previous month sales)

Given this collection, the cash budget will be:

April

May

June

Beginning cash balance

$152,000

$221,100

$361,850

Cash receipts

Cash collections from credit sales

Total cash available

$633,700

$740,150

$880,350

Cash disbursements

Purchases

$241,000

$252,000

$235,000

Wages, taxes, and expenses

Interest

Equipment purchases

Total cash disbursements

$412,600

$378,300

$604,000

Ending cash balance

12. a. 45-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 45) / 90 = 1/2 of current sales are collected.

Q1

Q2

Q3

Q4

Beginning receivables

$1,900

$2,150

$2,600

$2,400

Sales

4,300

5,200

4,800

4,000

Cash collections

4,050

4,750

5,000

4,400

Ending receivables

CHAPTER 15 – 8

b. 60-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 60) / 90 = 1/3 of current sales are collected.

Q1

Q2

Q3

Q4

Beginning receivables

$1,900

$2,867

$3,467

$3,200

c. 30-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and (90 – 30) / 90 = 2/3 of current sales are collected.

Q1

Q2

Q3

Q4

Beginning receivables

Sales

Cash collections

Ending receivables

$1,433

$1,733

$1,600

$1,333

Intermediate

13. a. The EAR of the loan without the compensating balance is:

EAR = (1 + .00485)12 – 1

EAR = .0598, or 5.98%

EAR = .0629, or 6.29%

b. To end up with $15,000,000, you must borrow:

Amount to borrow = $15,000,000 / (1 – .05)

Amount to borrow = $15,789,473.68

Sales

Cash collections

Ending receivables

$2,867

$3,467

$3,200

$2,667

CHAPTER 15 – 9

14. a. The EAR of your investment account is:

EAR = 1.00494 – 1

EAR = .0197, or 1.97%

b. To calculate the EAR of the loan, we can divide the interest on the loan by the amount of the

loan. The interest on the loan includes the opportunity cost of the compensating balance. The

opportunity cost is the amount of the compensating balance times the potential interest rate you

could have earned. The compensating balance is only on the unused portion of the credit line, so:

Opportunity cost = .04($75,000,000 – 40,000,000)(1.0049)4 – .04($75,000,000 – 40,000,000)

Opportunity cost = $27,642.34

c. The compensating balance is only applied to the unused portion of the credit line, so the EAR of

a loan on the full credit line is:

EAR = 1.01654 – 1

EAR = .0677, or 6.77%

15. Here, we need to use the cash cycle and operating cycles to calculate the average accounts payable

and average accounts receivable. We are given the cash cycle and the operating cycle, so the payables

period is:

Cash cycle = Operating cycle – Payables period

36.50 days = 59.40 days – Accounts payable period

Accounts payable period = 22.90 days

CHAPTER 15 – 10

Next, we can find the average accounts receivable. Using the equation for the operating cycle, the

accounts receivable period is:

Operating cycle = Inventory period + Receivables period

59.40 days = 23.20 days + Receivables period

Receivables period = 36.20 days

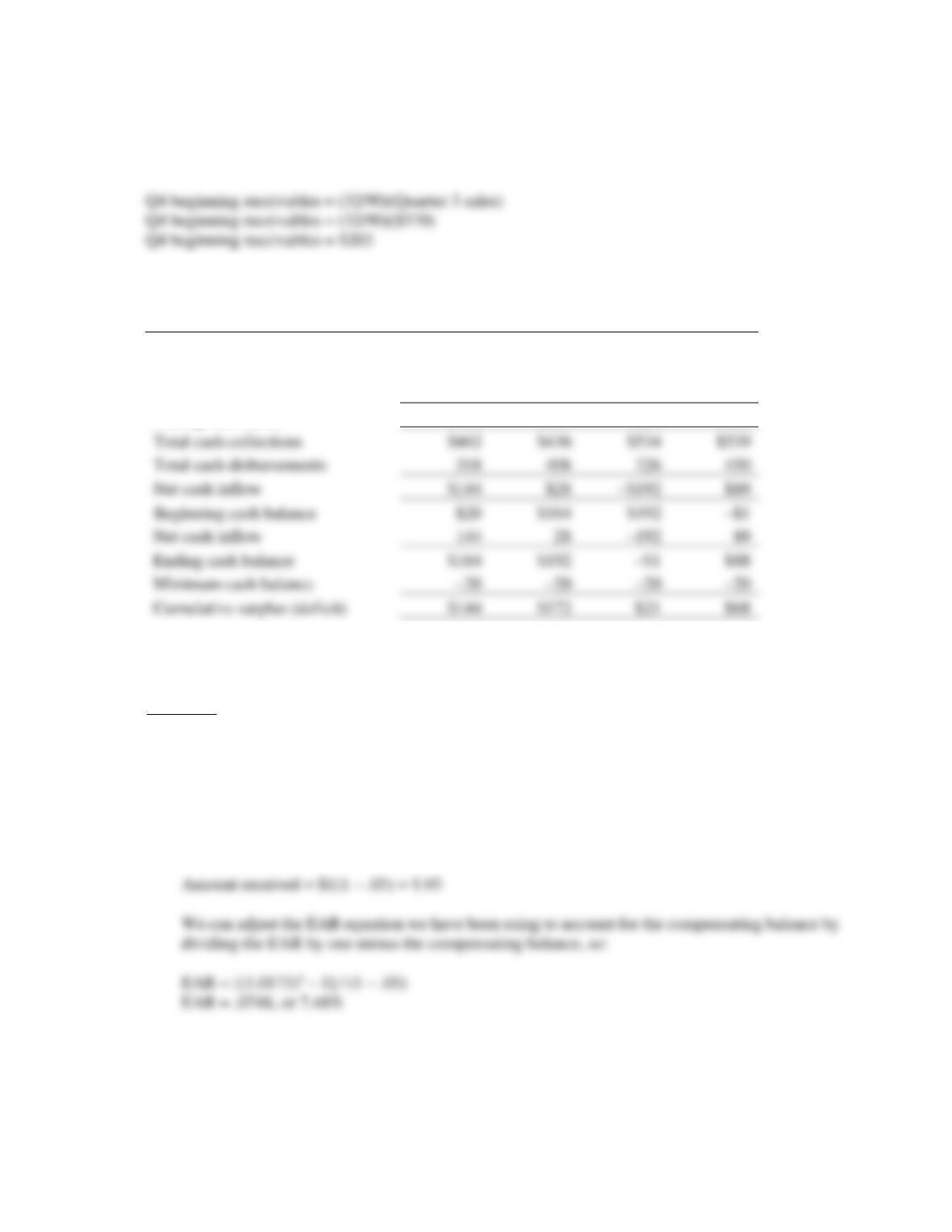

16. Since the company has a 32-day collection period, only those sales made in the first 58 days of the

quarter will be collected in that quarter. Total cash collections in the first quarter will be:

Q1 cash collections = Beginning receivables + (58/90)(Quarter 1 sales)

Q1 cash collections = $218 + (58/90)($378)

Q1 cash collections = $462

Quarter 3 and Quarter 4 collections will be:

Q3 cash collections = (58/90)(Quarter 3 sales) + (32/90)(Quarter 2 sales)

Q3 cash collections = (58/90)($570) + (32/90)($468)

Q3 cash collections = $534

CHAPTER 15 – 11

Q3 beginning receivables = (32/90)(Quarter 2 sales)

Q3 beginning receivables = (32/90)($468)

Q3 beginning receivables = $166

The cash budget (in millions) for the company is:

Q1

Q2

Q3

Q4

Beginning receivables

$218

$134

$166

$203

Sales

378

468

570

522

Cash collections

462

436

534

539

Ending receivables

$134

$166

$203

$186

Beginning cash balance

$20

$164

$192

Net cash inflow

144

Ending cash balance

$164

$192

$88

Minimum cash balance

Cumulative surplus (deficit)

$144

$172

$68

The company has a cash surplus for much of the year, but in Quarter 3, it will need to raise $21 million

to cover its cash flows.

Challenge

17. a. For every dollar borrowed, you pay quarterly interest of:

Interest = $1(.0173) = $.0173

You also must maintain a compensating balance of 5 percent of the funds borrowed, so for each

dollar borrowed, you will only receive:

CHAPTER 15 – 12

Another way to calculate the EAR is using the FVIF (or PVIF). For each dollar borrowed, we

must repay:

Amount owed = $1(1.0173)4

Amount owed = $1.07102

EAR = .0748, or 7.48%

b. The EAR is the amount of interest paid on the loan divided by the amount received when the loan

is originated. The amount of interest you will pay on the loan is the amount of the loan times the

effective annual interest rate, so:

Interest = $210,000,000[(1.0173)4 – 1]

Interest = $14,913,473.49

At the end of the loan, you will not repay the amount received since the commitment fee is a one–

time fee paid up front. The amount you will repay (excluding interest) at the end of the loan will

be the amount received plus the commitment, or:

CHAPTER 15 – 13

So, the EAR of the loan is:

FV = PV(1 + R)

$214,413,473.49 = $198,500,000(1 + R)

R = .0802, or 8.02%

18. You will pay interest of:

Interest = $20,000,000(.065) = $1,300,000

Additionally, the compensating balance on the loan is:

We can also use the FVIF (or PVIF) here to calculate the EAR. Your cash flow at the beginning of the

year is $17,900,000. At the end of the year, your cash flow is the loan repayment, but you will also

receive your compensating balance back, so:

End of year cash flow = $20,000,000 – 800,000

End of year cash flow = $19,200,000