Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 16

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 16-1 Discuss fully the difference between the “contexts” of Figure 16.1 and Figure

16.4.

ANS. Figure 16.1’s representation of the general ledger/business reporting (GL/BR)

process considers the controller, the treasurer, the budgeting department, and the

managerial reporting officer to be within the process. Figure 16.4 considers all

these entities to be external to the GL/BR process.

Flow Number

in Figure 16.1

Discussion

2, 3, 5, and 6

These flows are shown within the GL/BR process in Figure 16.1. In Figure 16.4, they all

appear as data flows running from or to external entities.

2 Solutions for Chapter 16

1. Flow number 1, shown as a single flow in Figure 16.1, appears in Figure 16.4

as several data flows from specific AIS feeder processes. This is merely a

difference in presentation.

2. Flow number 4 in Figure 16.1 is buried within the single context bubble in

Figure 16.4. It does not appear as a data flow until the context diagram is

exploded into a level 0 DFD (see Figure 16.6).

DQ 16-2 Four managers (or departments) are shown in Figure 16.1 as reporting to the

controller. Setting aside your personal career inclinations and aspirations and

ignoring any work experience you have, for which position do you think your

college academic studies to date have best prepared you? Discuss. Does your

answer hold any implications for the curriculum design at your college? Explain.

ANS. Although student answers to this question depend on their college’s curriculum,

their answers may also be largely personal. The following notes and questions

provide the foundations for an answer.

We suspect that the majority of students at most institutions will identify more

with the roles of the manager of the business reporting department or the financial

reporting officer than they will with the roles of the other two areas shown in

Figure 16.1. We suspect that they will make this identification because of the

heavy emphasis on financial accounting and on public accounting practice that

exists in many college curricula (and accounting textbooks), including the

curriculum at our universities.

Accounting Information Systems, 10e 3

• The influence of the CPA examination on the content of accounting textbooks

and, in turn, on curriculum design.

environment).

DQ 16-3 In the real world, what problems might an organization face in performing

interim closings? For example, the books might be left open after a December 31

closing until adjusting entries are made in March or April. During the same

period, interim financial statements for the new year are required. Can you

suggest any solutions for those problems? Discuss fully.

ANS. The term “interim closings” refers to the process of preparing interim financial

statements at times other than at end-of-year. Although these statements provide

useful information to management (and are required for certain SEC filings), an

4 Solutions for Chapter 16

Other practical problems associated with interim closings include but are not

limited to the following:

• The length of time to perform the interim closings. Can operating managers

respond effectively and efficiently to problems if they do not receive

information on a timely basis? In many companies, lags in interim closings

range from one workday to eight months after the end of the period being

reported.

o Some of the feeder processes are manual, whereas others are

computerized.

o The organization uses a combination of in-house as well as service

bureau software and hardware.

o The operating units are different companies that are scattered

internationally.

Improvements in technology in recent years (i.e., the increased interconnectivity

of hardware, improved telecommunications, the maturing of application process

software, and the availability of ERP software) have lessened this problem in

most organizations.

DQ 16-4 The chapter assumed that the controller was the source of all adjusting entry

journal vouchers. Mention at least one alternative source for each of the

following adjustments (and explain your answers):

ANS. In addition to the controller, the following might be the source of these adjusting

journal entry vouchers:

Accounting Information Systems, 10e 5

c. Lower of cost or market adjustments for inventories: Because these

adjustments relate to the inventory asset, inventory control would be a logical

source for them.

d. Lower of cost or market adjustments for investments: As in the case of interest

earned (see the preceding part b), these adjustments relate to investment

activities and could be reported to the GL/BR process by the treasurer.

DQ 16-5 “Defining the codes for a chart of accounts is no big deal

⎯

nothing is

permanent

⎯

I can change it at any time in the future.” Why do you agree (or

disagree) with this statement?

6 Solutions for Chapter 16

ANS. Although assigning the chart of accounts is not permanent, changes are difficult to

make. The choices are to set a date and change future entries or to make the

changes retroactive. Let’s begin with retroactive changes. This usually has to be

DQ 16-6 “Overstating receivables will keep the bank from calling our loan. Although some may

think it is fraud, no one is really hurt.” Why do you agree (or disagree) with this

statement?

ANS. While this is a rationalization for many frauds, in fact, the reason for most loan

covenants, is to protect the assets of the bank. The assumption is when the values

DQ 16-7 Read Section 409 from the Sarbanes-Oxley Act of 2002. Do you agree that this

supports real-time financial reporting? Research both sides of the issue, and

provide a conclusion based on your findings.

ANS. Section 409 includes the following: “. . . shall disclose to the public on a rapid and

current basis such additional information concerning material changes in the

reporting.

DQ 16-8 What is the overall significance of the Sarbanes-Oxley Act of 2002 to financial

reporting?

Accounting Information Systems, 10e 7

ANS. The purpose of an accounting information system is the production of reports for

DQ 16-9 Discuss why internal auditors may be more open to continuous assurance than

external auditors.

ANS. The issue is twofold. First, internal auditors may be open because they see

immediate benefits for their organizations. When a reliable system is in place to

Short Problems

SP 16-1 ANS. The chart of accounts may take many forms. One example solution includes

a sales account 7812300 (7 = revenue, 8 = sales, 1 = wholesale, 2 = country, 2 =

SP 16-2 ANS.

Note: A is not an accounting transaction and does not feed to the GL.

8 Solutions for Chapter 16

Problems

P 16-1 a. ANS.

Assumptions:

Feeder Process

Data Flow Name

Entry

OE/S

GL inventory sale update

Cost of goods sold

Inventory

B/AR/CR

GL invoice update

Accounts receivable

Sales

GL estimated bad debts update

Bad debts expense

Allowance for uncollectible accounts

GL writeoff update

Allowance for uncollectible accounts

Accounts receivable

GL sales return update

Sales returns and allowances

Accounts receivable

GL cash receipts update

Cash

Accounts receivable

Purchasing

GL inventory received update

Inventory

“Clearing account”

AP/CD

GL payable update

“Clearing account”

Accounts payable

GL cash disbursements update

Accounts payable

Cash

Payroll

GL disbursement voucher update

Payroll expense

Accounts payable

GL labor distribution update

Inventory

Payroll expense

Feeder Process

Data Flow Name

Entry

GL employer tax accrual update

Payroll tax expense

Payroll tax payable

GL tax deposit update

Payroll tax payable

Cash

GL recording raw material usage

Work in process inventory

Raw materials inventory

GL allocation of overhead

Work in process inventory

GL allocation of labor

Work in process inventory

Payroll expense

GL recording completion of process

Finished goods inventory

Work in process inventory

b. ANS. Some other entries that might come from the feeder processes studied in Chapters

10 through 15 include the following:

• Purchases of items other than inventory (e.g., plant assets, supplies, services)

c. ANS. (For a complete coverage of financing and investing events, consult a financial

accounting or intermediate accounting textbook. The following entries show one

10 Solutions for Chapter 16

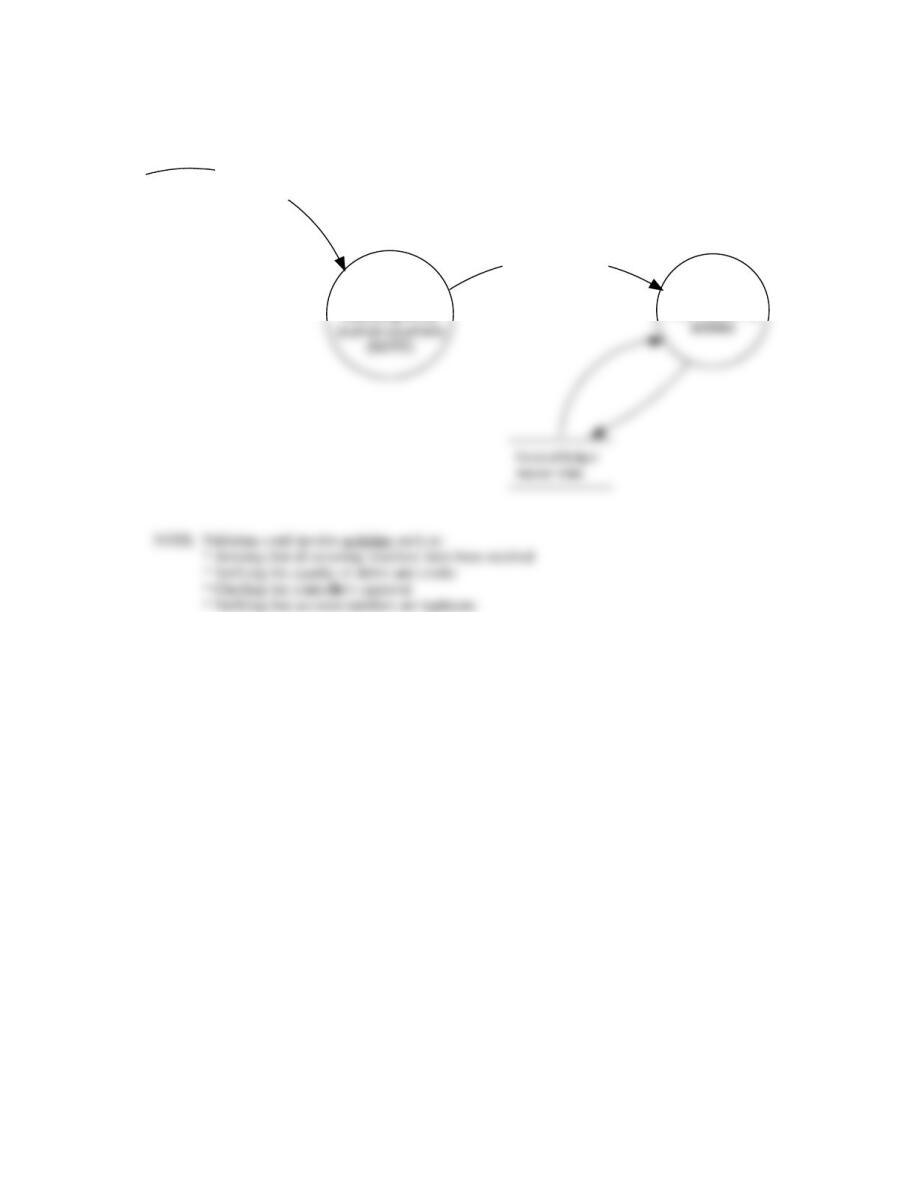

P 16-2 ANS.

3.1

Validate

adjusting entry

Adjusting entry

journal vouchers

3.2

Post adjusting

Validated adjusting

entry journal

vouchers

FIGURE SM-16.1 Problem 16-2, Part a Solution

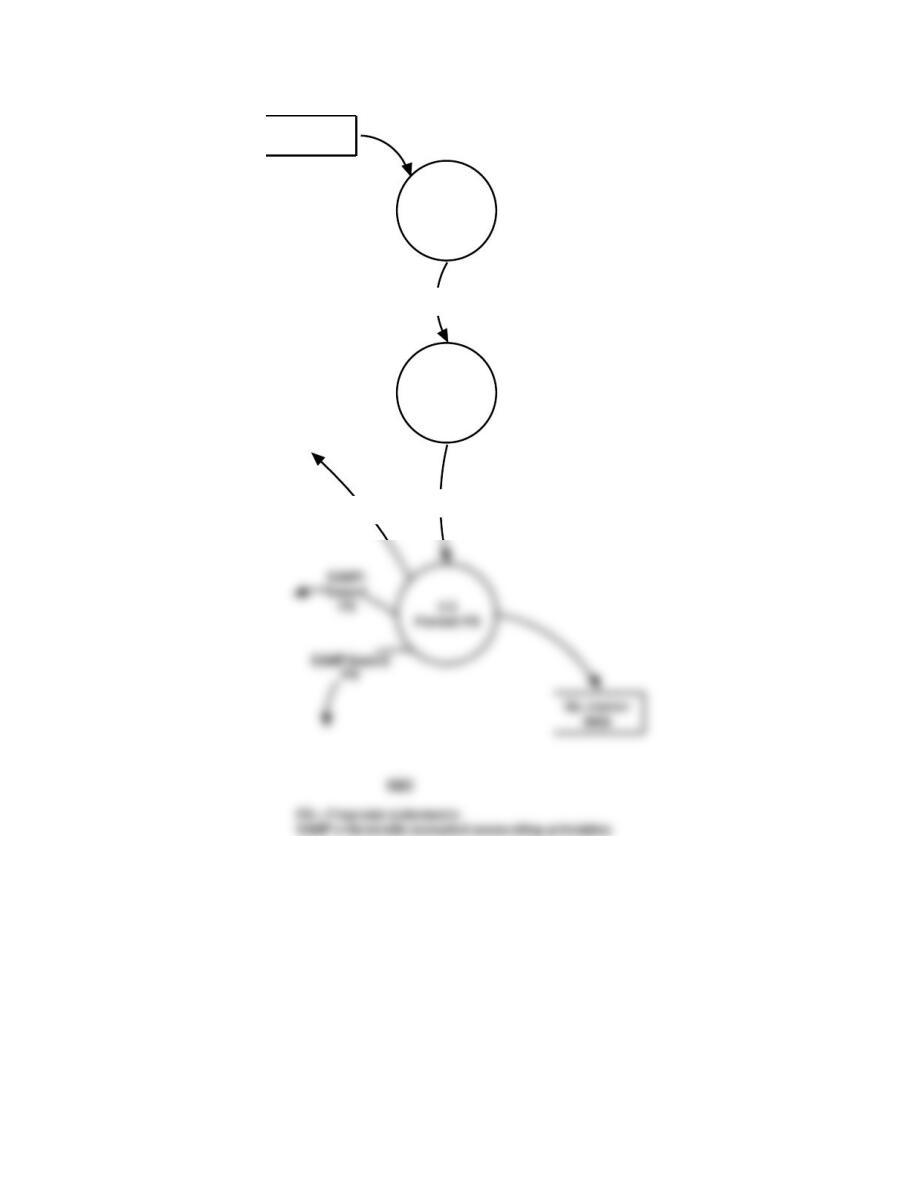

Accounting Information Systems, 10e 11

4.1

Draft FS

4.2

Prepare FS

footnotes

FS drafts

FS with

footnotes

GAAP-based

FS

GL master

data

FIGURE SM-16.2 Problem 16-2, Part b Solution

12 Solutions for Chapter 16

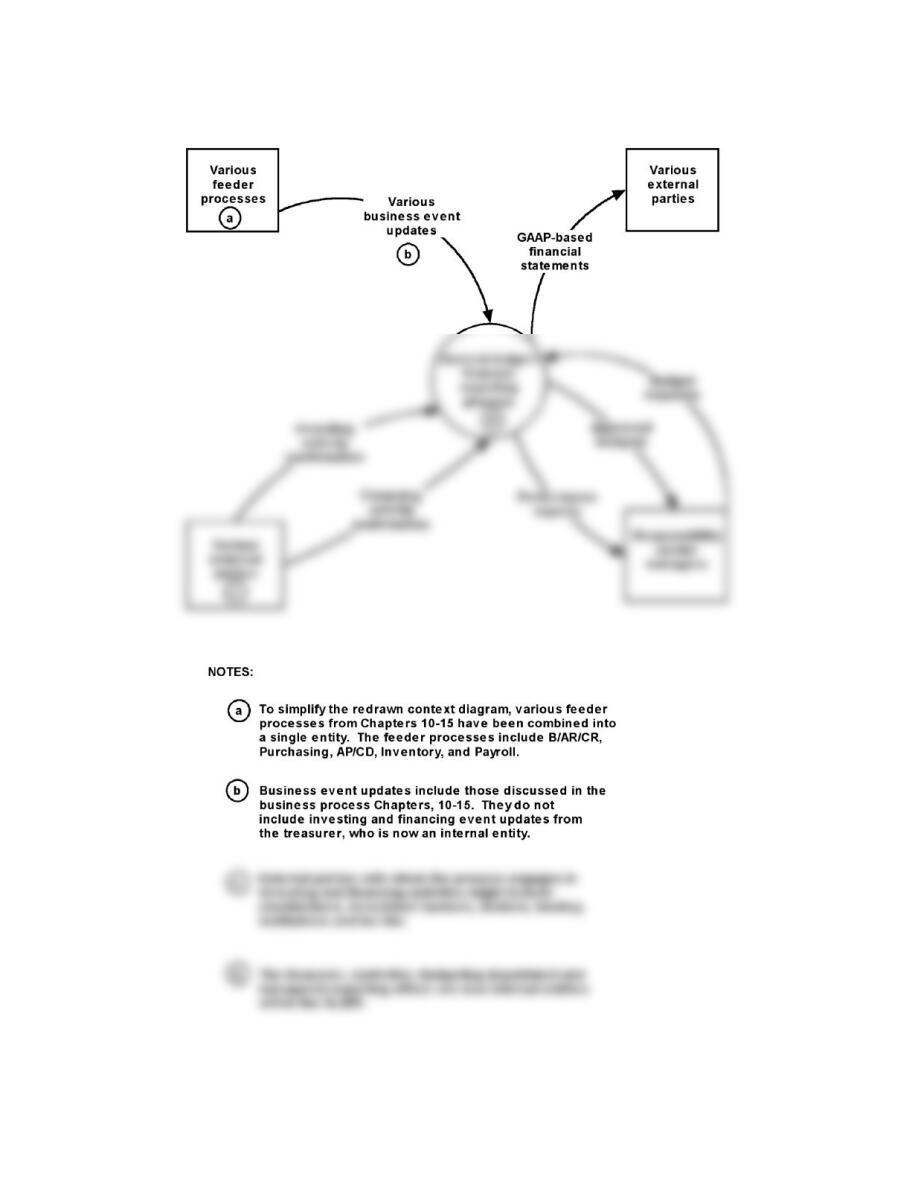

P16-3 ANS.

FIGURE SM-16.3 Problem 16-3 Solution—Context Diagram

Accounting Information Systems, 10e 13

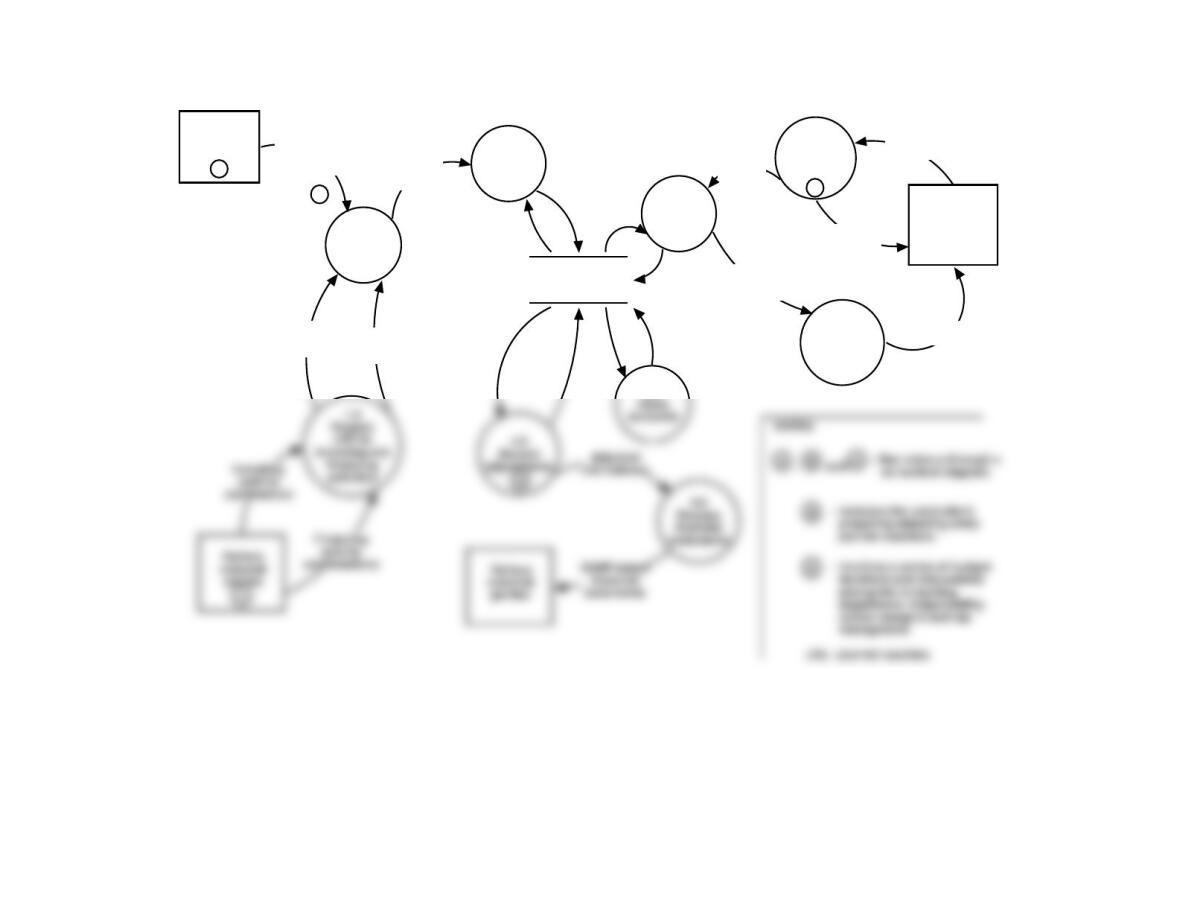

2.0

Validate

event

updates General ledger

master data

Various

feeder

processes

a

Various

business event

updates

b

3.0

Post

event

Validated

event

updates

6.0

Approve

budgets

7.0

Record

budget

Finalized

budget

Responsibility

center

managers

Approved

budgets

Budget

requests

8.0

Prepare

performance

reports

Performance

reports

Budget

and actual

trial balance

9.0

Investing

event

update

Financing

event

update

e

FIGURE SM-16.4 Problem 16-3 Solution—Level 0 DFD

P 16-4 a. ANS. The following coding scheme is suggested:

02 04 26 12 43208 B0589 A0589

02 = Functional area (e.g., vice-president)

04 = Division (e.g., superintendent)

b. ANS. This hierarchical code works as follows. Financial data is captured and

immediately classified as to the Department, Division, and Functional area.

and year are assigned as defaults unless otherwise indicated.

c. ANS. In a database environment, instead of coding all of the information specified, links

P 16-5 ANS. Some of the more basic comparison problems that may exist include the

following:

• Category descriptions may differ. For example, Accounts Receivable may be

reported by one company and Net Receivables for the other.

Accounting Information Systems, 10e 15

P 16-6 ANS. Student answers will vary based on the enterprise packages chosen.

a. The feeder modules may include precisely what we presented, but that is

doubtful. For example, Microsoft Dynamics GP groups B/AR/CR with OR/S

into the Sales module, whereas Oracle’s E-Business Suite Financials includes

P 16-7 ANS. Student answers will vary based on the article chosen.

It is important that students see how to apply new technology to old problems, but

at the same time see that even for good ideas, there is another side of the story that

should be considered.

P 16-8 ANS. Student answers will vary based on the product identified.

Some answers may include positives for outsourcing that may include items such

as the service provider (1) has more expertise in the process than individual

companies (including tagging and the actual filing), (2) has the software tools

required, (3) can better deal with rejected filings.

16 Solutions for Chapter 16

P 16-9 ANS. Unlike the other business processes, the GL/BR process has fewer operational

functions and focuses mainly on information functions. Other processes perform

important functions related to their purpose of providing goods and services to

customers, but the main purpose of the GL/BR process is to process and

case typically includes a description of the charge/fraud and any fines that

are assessed.

P 16-11 ANS. With emerging technologies, many organizations have chosen to make their

financial information available on the Internet. As part of the GL/BR process, the

financial reporting officer sends GAAP-based financial statements to owners,

potential investors, banks, and potential lenders. This role is now expanding into

P 16-12 ANS. Solutions will vary according to how the tables are implemented, especially which

attributes are placed in the tables and how the tables are populated. However, the

following guidelines should be helpful for grading the solutions:

1. From the file, ensure that the tables are linked in relationships with

cardinalities.

Accounting Information Systems, 10e 17

4. From the printouts, ensure that the explanations of the importance of the query

are credible, e.g., the accounts receivables department might use the query

output for the next invoicing cycle or the query output could be used to ensure

that a customer is not over his or her credit limit. Using the file, examine the

design of the query for any obvious problems, e.g., tables not being linked

together.

a. Here is an example of the query design: Using the SALES_INVOICES