E16-21 Computing cost of goods manufactured

Learning Objective 4

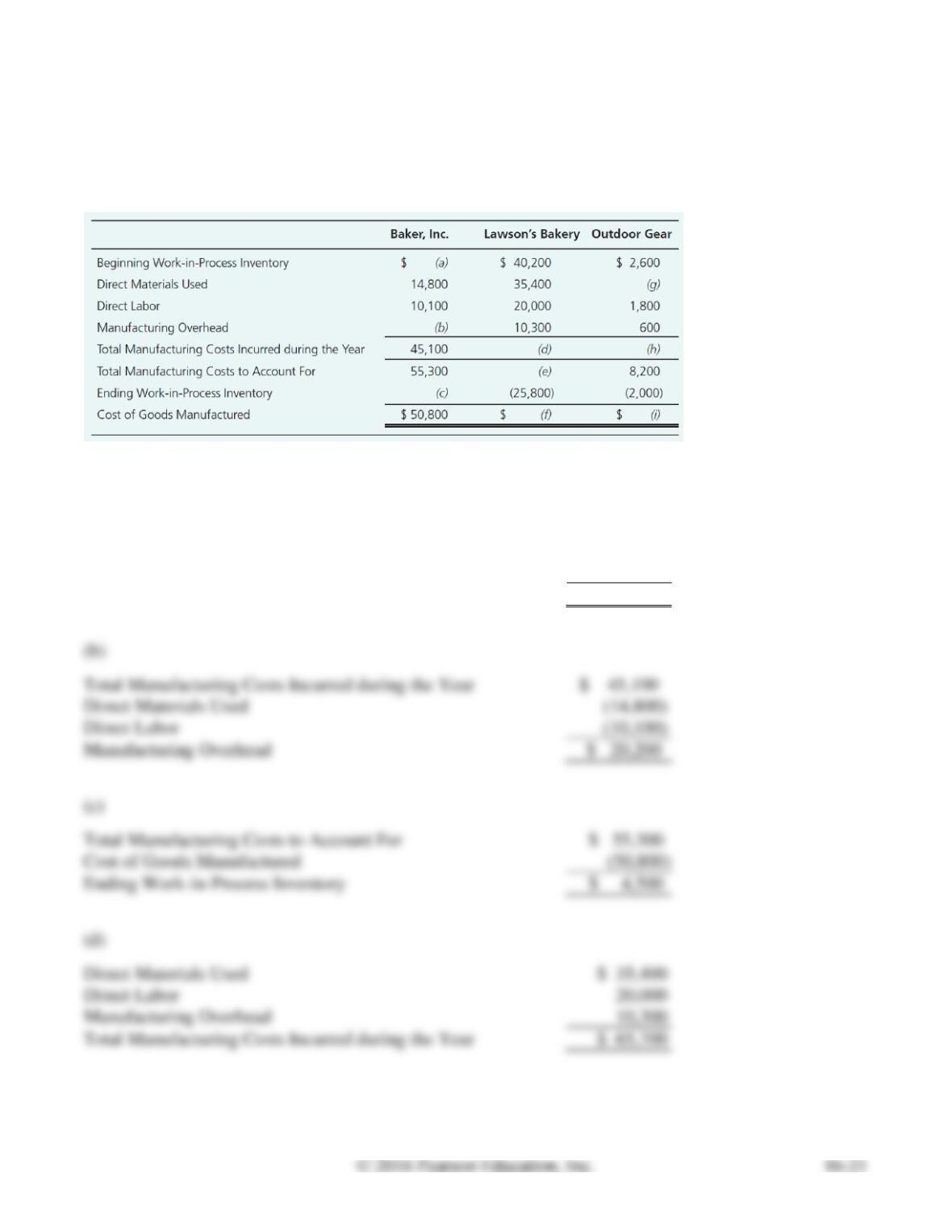

Consider the following partially completed schedules of cost of goods manufactured. Compute the miss-

ing amounts.

SOLUTION

(a)

Total Manufacturing Costs to Account For

$ 55,300

Total Manufacturing Costs Incurred during the Year

(45,100)

Beginning Work-in-Process Inventory

$ 10,200

(b)

Total Manufacturing Costs Incurred during the Year

$ 45,100

Direct Materials Used

Direct Labor

(10,100)

Manufacturing Overhead

(c)

Total Manufacturing Costs to Account For

Cost of Goods Manufactured

Ending Work-in-Process Inventory

(d)

Direct Materials Used

Direct Labor

Manufacturing Overhead

Total Manufacturing Costs Incurred during the Year

(e)

Beginning Work-in-Process Inventory

$ 40,200

Total Manufacturing Costs Incurred during the Year [d, above]

65,700

Total Manufacturing Costs to Account For

$ 105,900

Total Manufacturing Costs to Account For [e, above]

Ending Work-in-Process Inventory

Cost of Goods Manufactured

(g)

Total Manufacturing Costs Incurred during the Year [h, below]

$ 5,600

Direct Labor

Manufacturing Overhead

Direct Materials Used

$ 3,200

(h)

Total Manufacturing Costs to Account For

$ 8,200

Beginning Work-in-Process Inventory

(2,600)

Total Manufacturing Costs Incurred During the Year

$ 5,600

(i)

Total Manufacturing Costs to Account For

$ 8,200

Ending Work-in-Process Inventory

(2,000)

Cost of Goods Manufactured

$ 6,200

E16-22 Preparing a schedule of cost of goods manufactured

Learning Objective 4

1. COGM: $427,000

(Requirement 1 only)

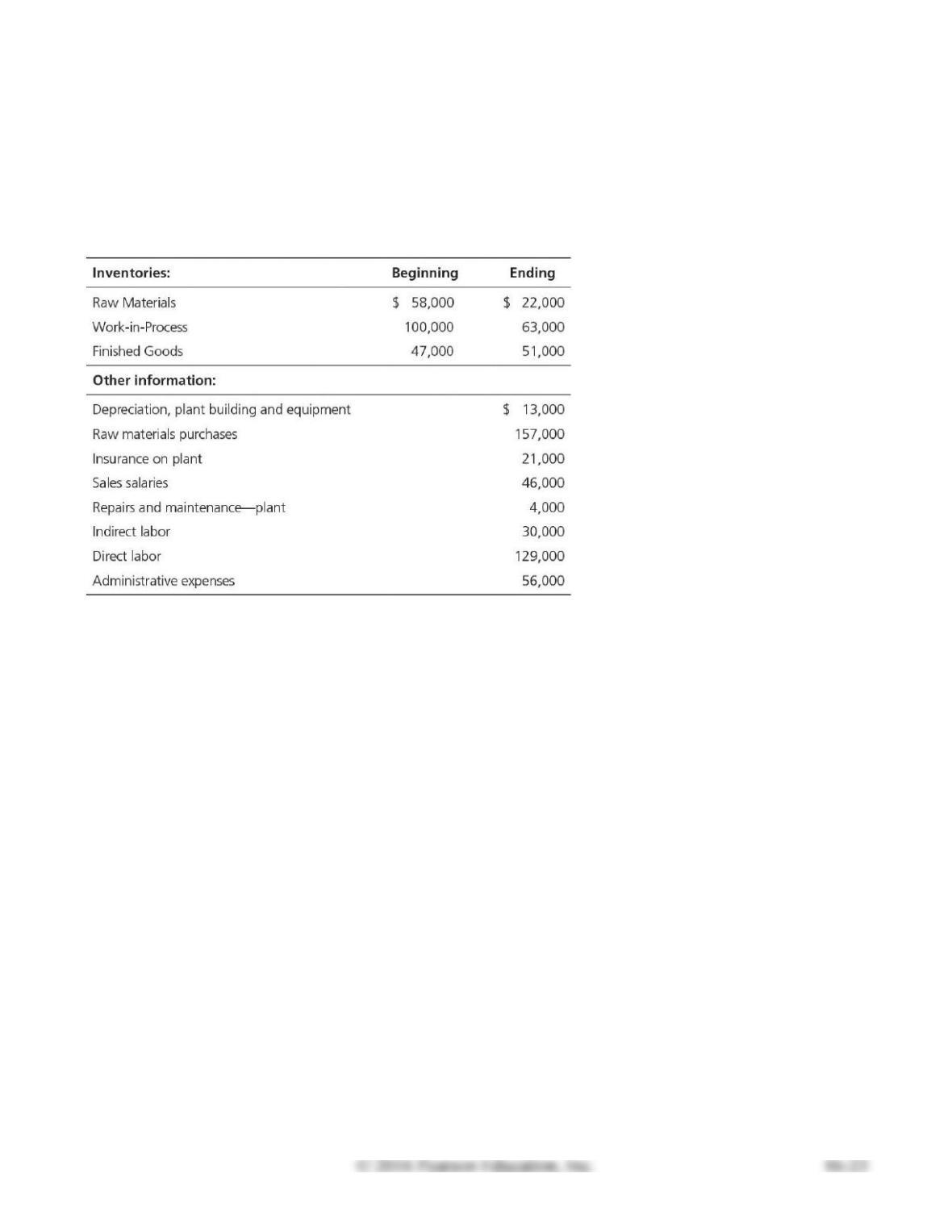

Clarkson Corp., a lamp manufacturer, provided the following information for the year ended December

31, 2016:

Requirements

1. Use the information to prepare a schedule of cost of goods manufactured.

2. What is the unit product cost if Clarkson manufactured 2,135 lamps for the year?

SOLUTION

Requirement 1

CLARKSON CORP.

Schedule of Cost of Goods Manufactured

Year Ended December 31, 2016

Beginning Work-in-Process Inventory

$ 100,000

Direct Materials Used:

Beginning Raw Materials Inventory

$ 58,000

Purchases of Raw Materials

Raw Materials Available for Use

Ending Raw Materials Inventory

Direct Materials Used

Direct Labor

Manufacturing Overhead:

Depreciation, plant building and equipment

Insurance on plant

Repairs and maintenance—plant

Indirect labor

Total Manufacturing Overhead

Total Manufacturing Costs Incurred During the Year

Total Manufacturing Costs to Account For

Ending Work-in-Process Inventory

Cost of Goods Manufactured

$ 427,000

Requirement 2

Unit product cost

=

Cost of goods manufactured / Total units produced

=

$427,000 / 2,135 lamps

=

$200 per lamp

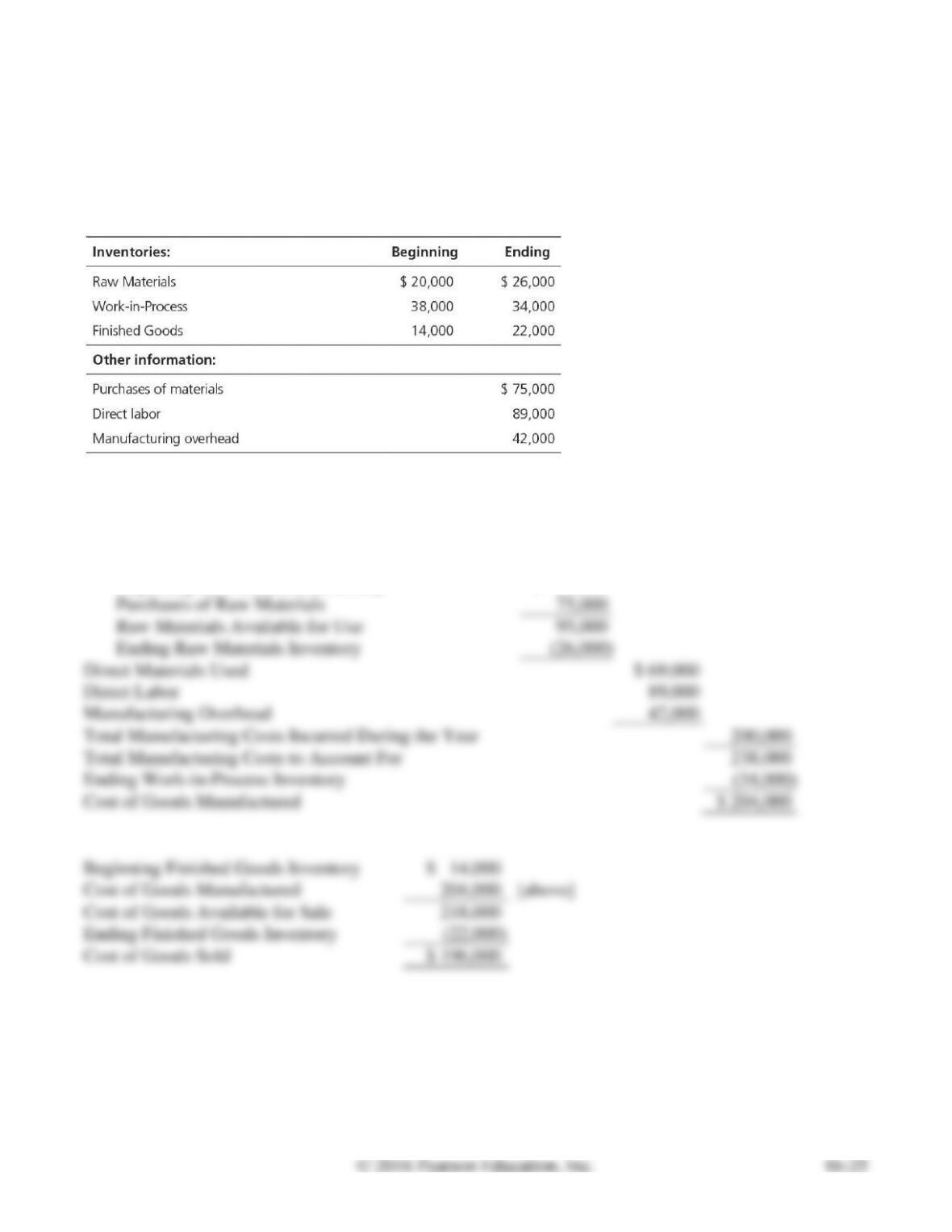

E16-23 Computing cost of goods manufactured and cost of goods sold

Learning Objective 4

COGM: $204,000

Use the following information for a manufacturer to compute cost of goods manufactured and cost of

goods sold:

SOLUTION

Beginning Work-in-Process Inventory

$ 38,000

Direct Materials Used:

Beginning Raw Materials Inventory

$ 20,000

Purchases of Raw Materials

Raw Materials Available for Use

Ending Raw Materials Inventory

Direct Materials Used

$ 69,000

Direct Labor

Manufacturing Overhead

Total Manufacturing Costs Incurred During the Year

200,000

Total Manufacturing Costs to Account For

Ending Work-in-Process Inventory

Cost of Goods Manufactured

$ 204,000

204,000

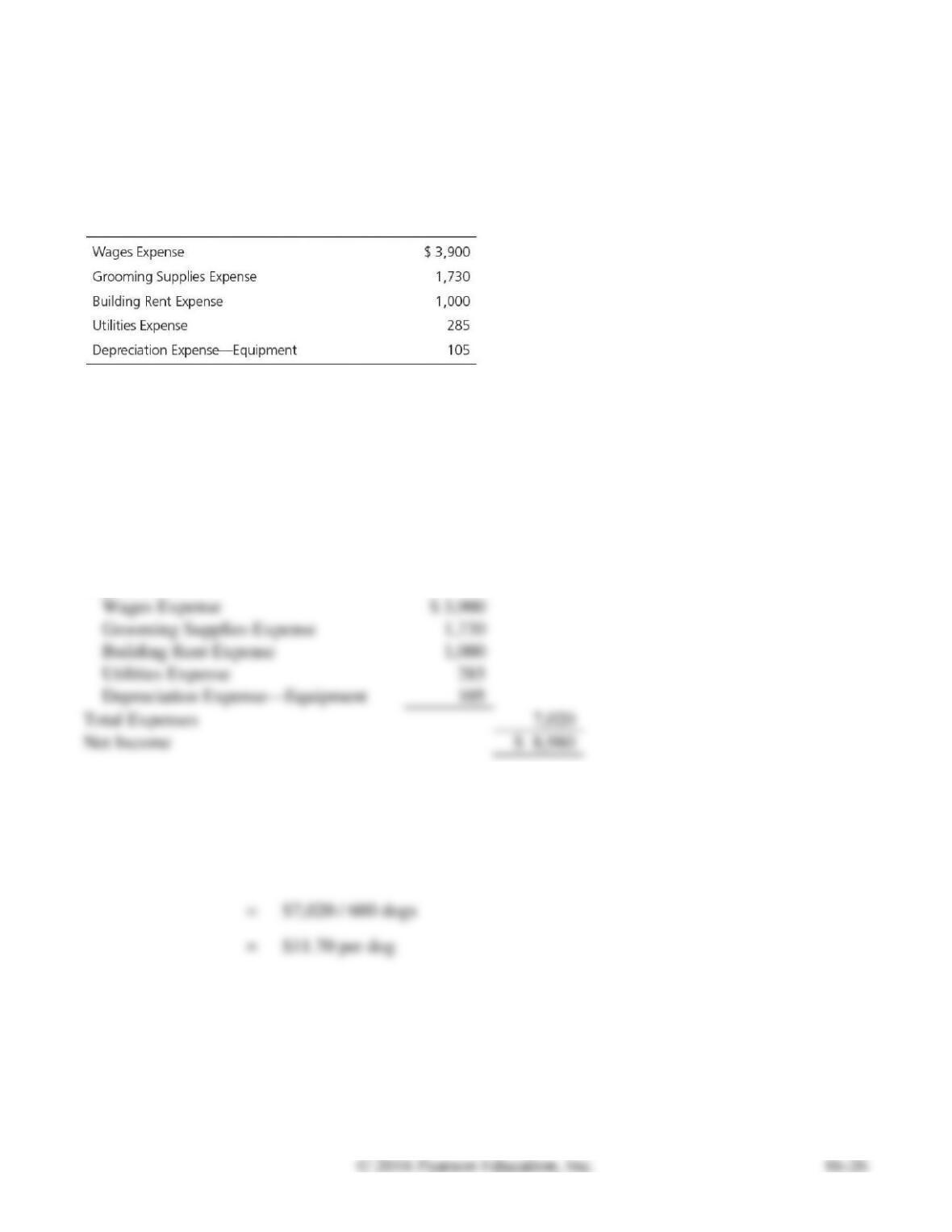

E16-24 Calculating income and cost per service for a service company

Learning Objective 5

1. $8,980

One Stop Grooming provides grooming services for pets. In April, the company earned

$16,000 in revenues and incurred the following operating costs to groom 600 dogs:

Requirements

1. What is One Stop’s net income for April?

2. What is the cost of service to groom one dog?

SOLUTION

Requirement 1

Grooming Revenue

$ 16,000

Expenses:

Wages Expense

Grooming Supplies Expense

Building Rent Expense

Utilities Expense

Depreciation Expense—Equipment

Total Expenses

Net Income

Requirement 2

Cost of Service to

Groom One Dog

=

Total expenses / Total number of dogs groomed

$7,020 / 600 dogs

$11.70 per dog

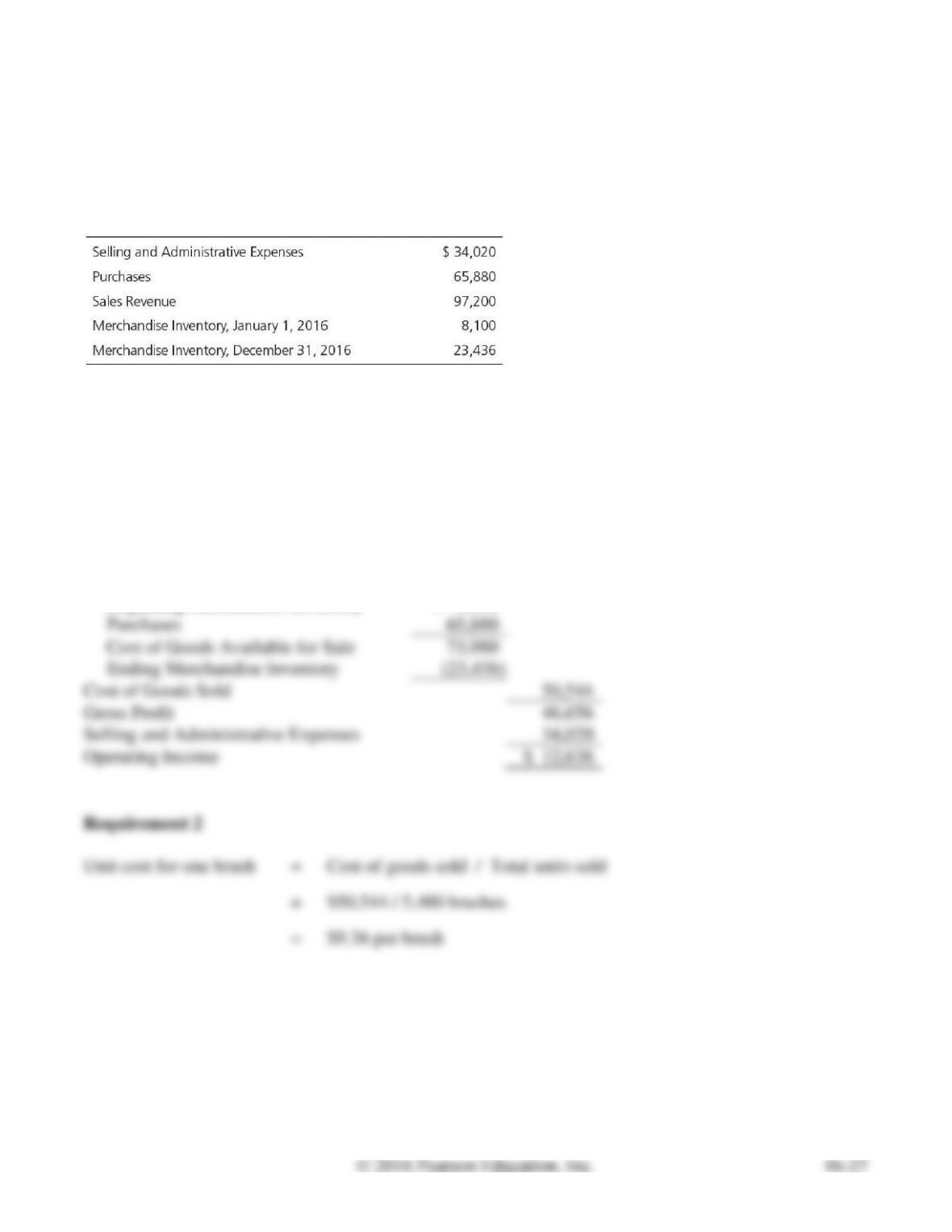

E16-25 Calculating income and cost per unit for a merchandising company

Learning Objective 5

2. $9.36

White Brush Company sells standard hair brushes. The following information summarizes White’s op-

erating activities for 2016:

Requirements

1. Calculate the operating income for 2016.

2. White sold 5,400 brushes in 2016. Compute the unit cost for one brush.

SOLUTION

Requirement 1

Sales Revenue

$ 97,200

Cost of Goods Sold:

Beginning Merchandise Inventory

$ 8,100

Purchases

Cost of Goods Available for Sale

Ending Merchandise Inventory

Cost of Goods Sold

Gross Profit

Selling and Administrative Expenses

Operating Income

Unit cost for one brush

Cost of goods sold / Total units sold

$9.36 per brush

Problems (Group A)

P16-26A Applying ethical standards, management accountability

Learning Objective 1

Natalia Wallace is the new controller for Smart Software, Inc. which develops and sells education soft-

ware. Shortly before the December 31 fiscal year-end, James Cauvet, the company president, asks Wal-

lace how things look for the year-end numbers. He is not happy to learn that earnings growth may be

below 13% for the first time in the company’s five-year history. Cauvet explains that financial analysts

have again predicted a 13% earnings growth for the company and that he does not intend to disappoint

them. He suggests that Wallace talk to the assistant controller, who can explain how the previous con-

troller dealt with such situations. The assistant controller suggests the following strategies:

a. Persuade suppliers to postpone billing $13,000 in invoices until January 1.

b. Record as sales $115,000 in certain software awaiting sale that is held in a public warehouse.

c. Delay the year-end closing a few days into January of the next year so that some of the next year’s

sales are included in this year’s sales.

d. Reduce the estimated Bad Debts Expense from 5% of Sales Revenue to 3%, given the company’s

continued strong performance.

e. Postpone routine monthly maintenance expenditures from December to January.

Requirements

1. Which of these suggested strategies are inconsistent with IMA standards?

2. How might these inconsistencies affect the company’s stakeholders?

3. What should Wallace do if Cauvet insists that she follow all of these suggestions?

SOLUTION

Requirement 1

a. If the goods have been received, postponing recording of the purchases understates liabilities. This is

unethical and inconsistent with the IMA standards even if the suppliers agree to delay billing.

Requirement 2

Management accountability is management’s responsibility to the various stakeholders of the company.

Each group of stakeholders has an interest of some sort in the business. Stakeholders include suppliers,

employees, customers, vendors, investors, creditors, governments, and communities. Managers are ac-

countable to the stakeholders and have a responsibility to wisely manage the company’s resources.

Requirement 3

The controller should resist attempts to implement a, b, and c and should gather more information about

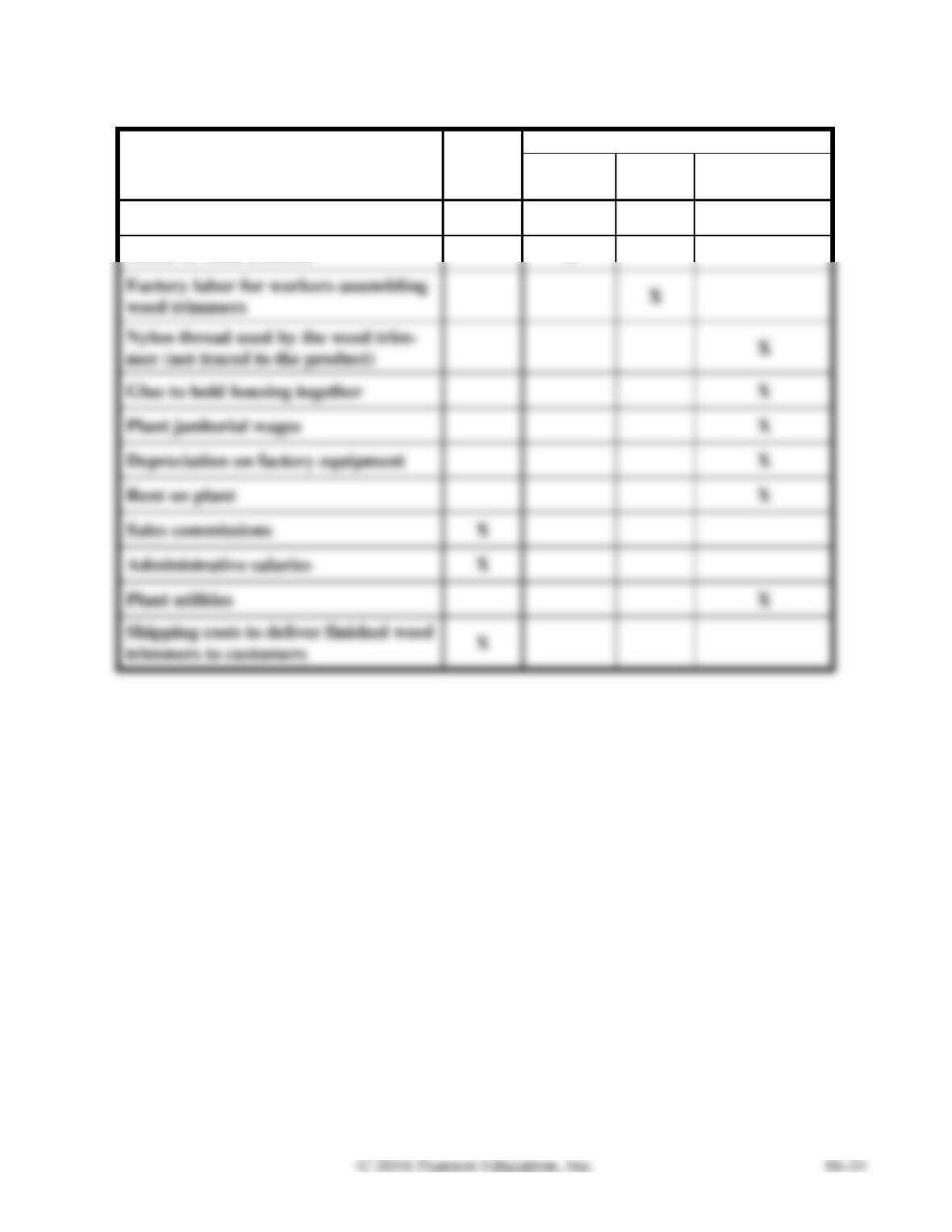

P16-27A Classifying period costs and product costs

Learning Objective 3

Lawlor, Inc. is the manufacturer of lawn care equipment. The company incurs the following costs while

manufacturing weed trimmers:

• Shaft and handle of weed trimmer

• Motor of weed trimmer

• Factory labor for workers assembling weed trimmers

• Nylon thread used by the weed trimmer (not traced to the product)

• Glue to hold the housing together

• Plant janitorial wages

• Depreciation on factory equipment

• Rent on plant

• Sales commissions

• Administrative salaries

• Plant utilities

• Shipping costs to deliver finished weed trimmers to customers

Requirements

1. Describe the difference between period costs and product costs.

2. Classify Lawlor’s costs as period costs or product costs. If the costs are product costs, further classi-

fy them as direct materials, direct labor, or manufacturing overhead.

SOLUTION

Requirement 1

Period costs are operating costs that are expensed in the accounting period in which they are incurred.

Requirement 2

Cost:

Period

Cost

Product Cost

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Shaft and handle of weed trimmer

X

Motor of weed trimmer

X

Glue to hold housing together

Plant janitorial wages

Sales commissions

Administrative salaries

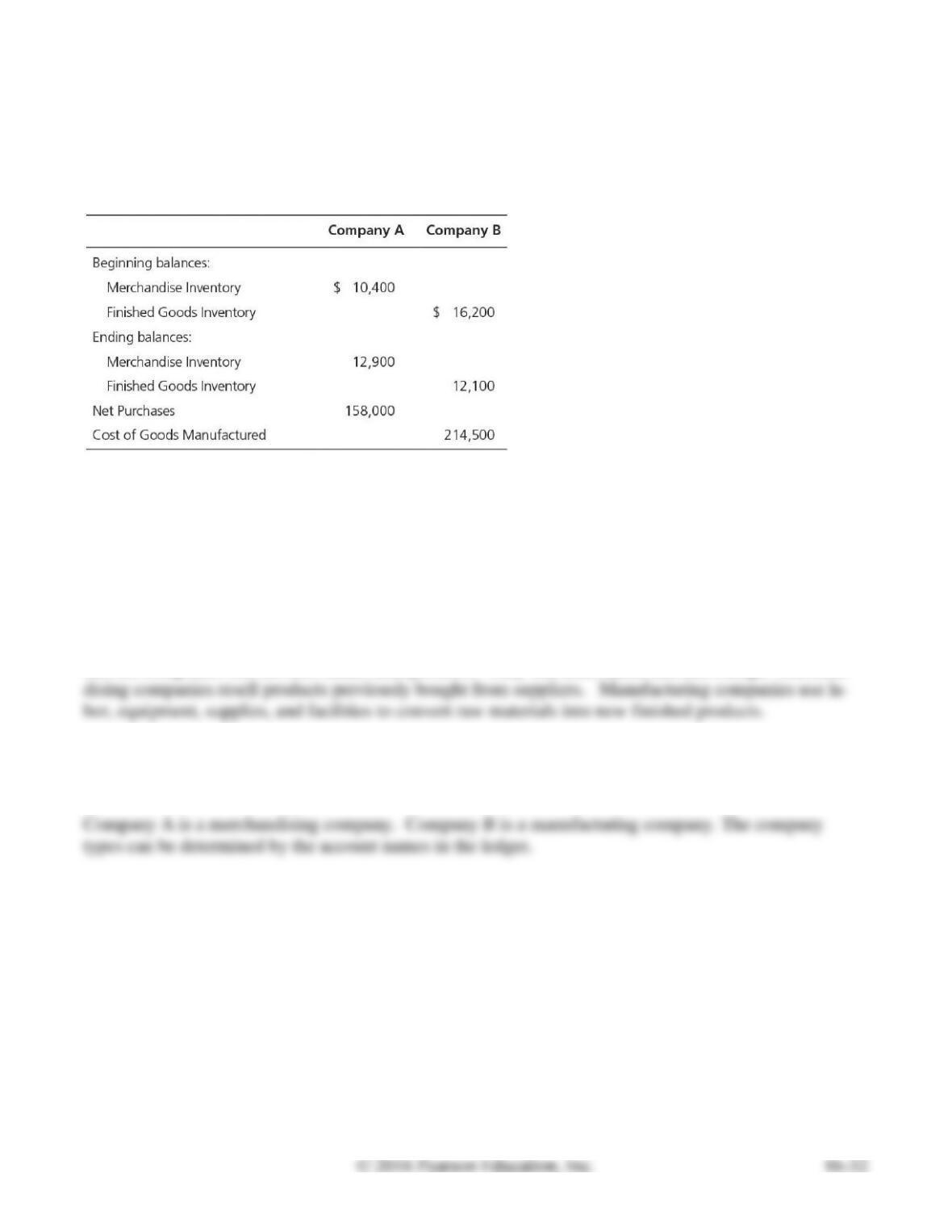

P16-28A Calculating cost of goods sold for merchandising and manufacturing companies

Learning Objectives 2, 4, 5

3. Company B: $218,600

Below are data for two companies:

Requirements

1. Define the three business types: service, merchandising, and manufacturing.

2. Based on the data given for the two companies, determine the business type of each one.

3. Calculate the cost of goods sold for each company.

SOLUTION

Requirement 1

Service companies sell services rather than products. They sell time, skills, and knowledge. Merchan-

Requirement 2

Requirement 3

Company A:

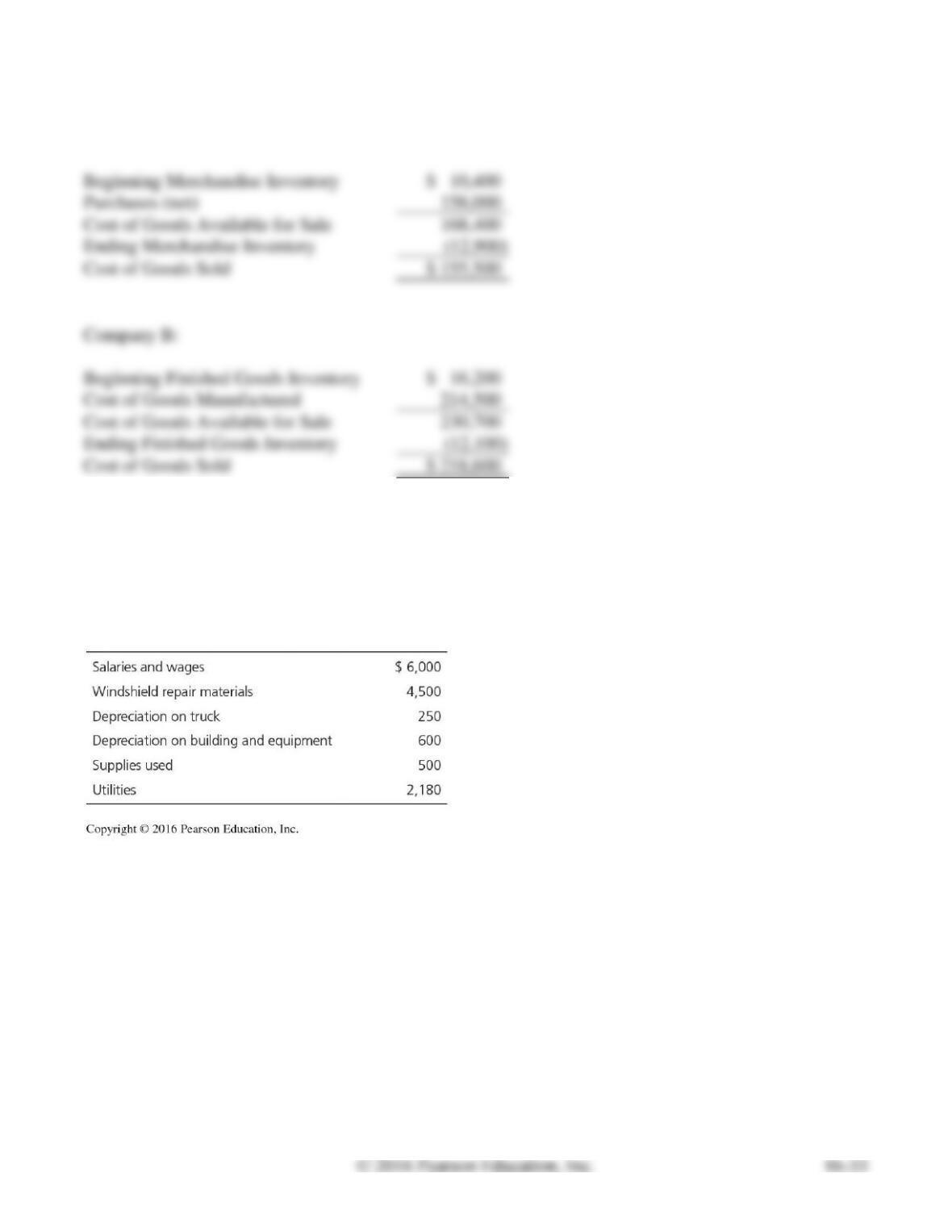

P16-29A Preparing an income statement and calculating unit cost for a service company

Learning Objectives 2, 5

2. $70.15

Sandman repairs chips in car windshields. The company incurred the following operating costs for the

month of February 2016:

Sandman earned $27,000 in revenues for the month of February by repairing 200 windshields. All costs

shown are considered to be directly related to the repair service.

Requirements

1. Prepare an income statement for the month of February.

2. Compute the cost per unit of repairing one windshield.

3. The manager of Sandman must keep unit operating cost below $60 per windshield in order to get his

bonus. Did he meet the goal?

SOLUTION

Requirement 1

SANDMAN

Income Statement

Month Ended February 29, 2016

Revenues:

Sales Revenue

$ 27,000

Expenses:

Salaries and Wages Expense

Materials Expense

Depreciation Expense—Building and Equipment

Supplies Expense

Utilities Expense

Total Expenses

Net Income

Requirement 2

Unit cost

=

Total expenses / Total windshields repaired

=

$14,030 / 200 windshields

=

$70.15 per windshield

P16-30A Preparing an income statement and calculating unit cost for a merchandising company

Learning Objectives 2, 5

1. Net income: $12,750

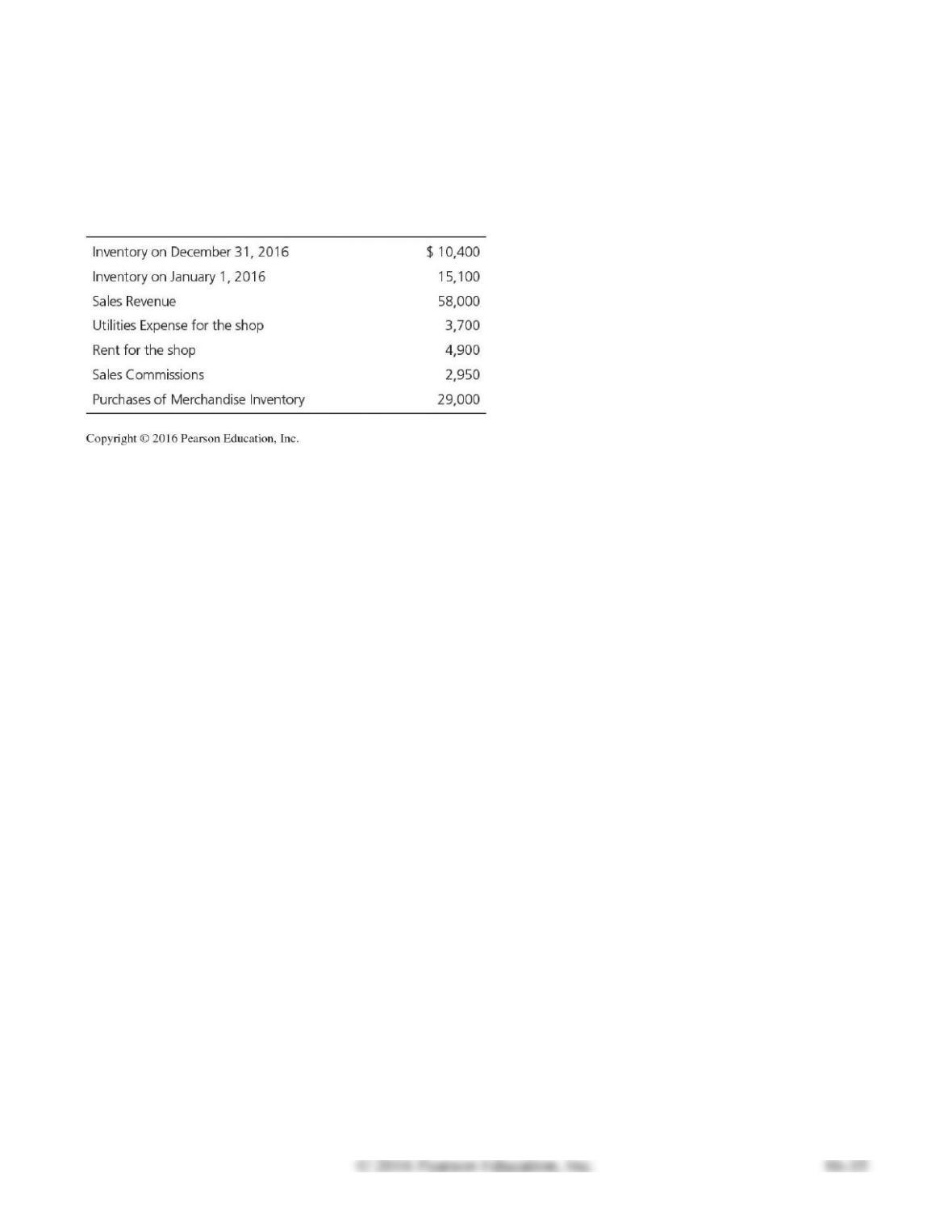

Cam Smith owns Cam’s Pets, a small retail shop selling pet supplies. On December 31, 2016, the ac-

counting records of Cam’s Pets showed the following:

Requirements

1. Prepare an income statement for Cam’s Pets for the year ended December 31, 2016.

2. Cam’s Pets sold 5,450 units. Determine the unit cost of the merchandise sold, rounded to the nearest

cent.

SOLUTION

Requirement 1

CAM’S PETS

Income Statement

Year Ended December 31, 2016

Revenues:

Sales Revenue

$ 58,000

Cost of Goods Sold:

Beginning Merchandise Inventory

$ 15,100

Purchases of Merchandise

Cost of Goods Available for Sale

Ending Merchandise Inventory

Cost of Goods Sold

33,700

Gross Profit

Selling and Administrative Expenses:

Utilities Expense

Rent Expense

Sales Commission Expense

Total Selling and Administrative Expenses

Net Income

$ 12,750

Requirement 2

Unit cost

=

Cost of goods sold / Total units sold

=

$33,700 / 5,450 units

=

$6.18 per unit (rounded to nearest cent)

P16-31A Preparing a schedule of cost of goods manufactured and an income statement for a man-

ufacturing company

Learning Objectives 2, 4

2. Net income: $34,900

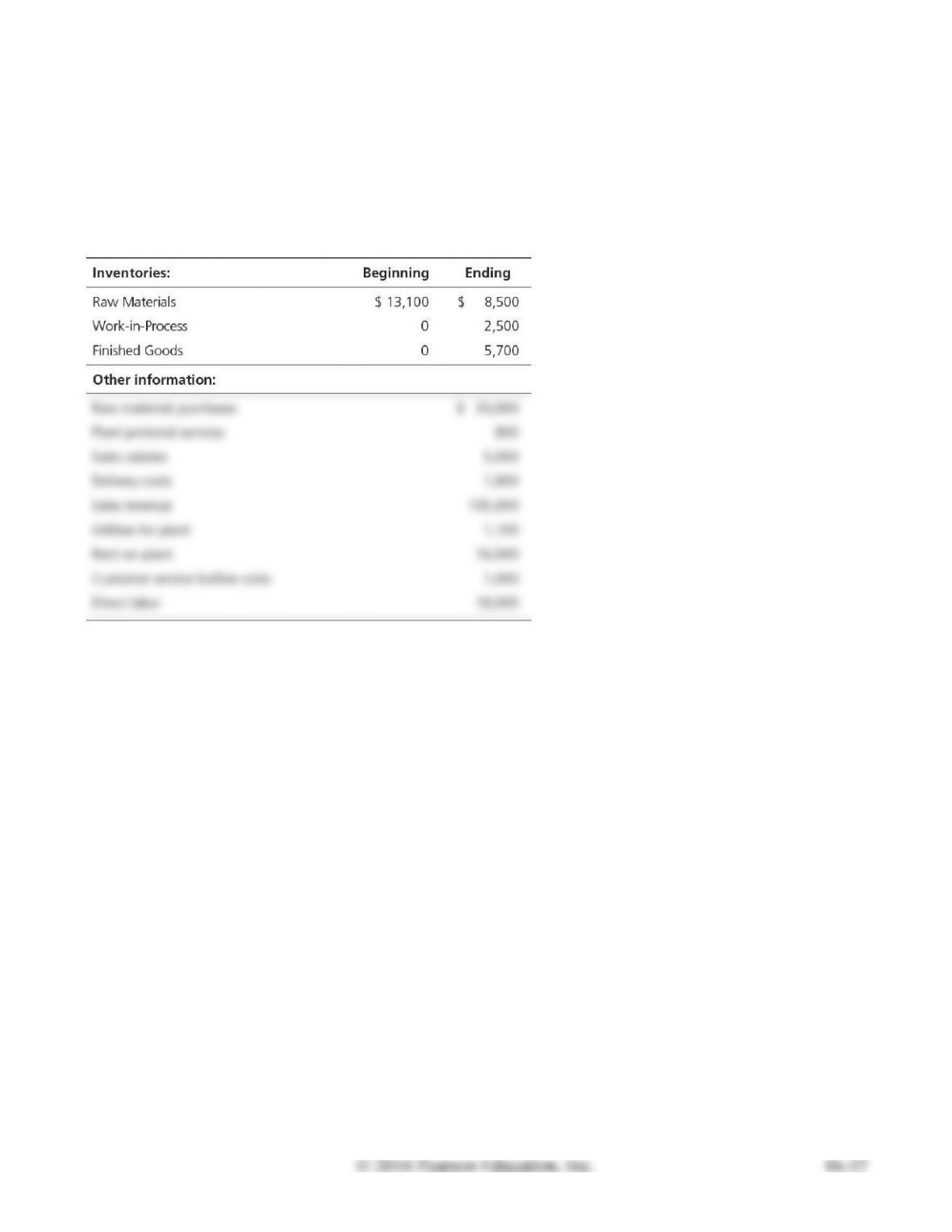

Yum Yum Treats manufactures its own brand of pet chew bones. At the end of December 2016, the ac-

counting records showed the following:

Requirements

1. Prepare a schedule of cost of goods manufactured for Yum Yum Treats for the year ended December

31, 2016.

2. Prepare an income statement for Yum Yum Treats for the year ended December 31, 2016.

3. How does the format of the income statement for Yum Yum Treats differ from the income statement

of a merchandiser?

4. Yum Yum Treats manufactured 17,600 units of its product in 2016. Compute the company’s unit

product cost for the year, rounded to the nearest cent.

SOLUTION

Requirement 1

YUM YUM TREATS

Schedule of Cost of Goods Manufactured

Year Ended December 31, 2016

Beginning Work-in-Process Inventory

$ 0

Direct Materials Used:

Beginning Raw Materials Inventory

Purchases of Raw Materials

Raw Materials Available for Use

Ending Raw Materials Inventory

Direct Materials Used

Direct Labor

Manufacturing Overhead:

Plant janitorial services

Utilities for plant

Rent on plant

Total Manufacturing Overhead

Total Manufacturing Costs Incurred during the Year

Total Manufacturing Costs to Account For

Ending Work-in-Process Inventory

Cost of Goods Manufactured

$ 68,000

P16-31A, cont.

Requirement 2

YUM YUM TREATS

Income Statement

Year Ended December 31, 2016

Revenues:

Sales Revenue

$ 105,000

Cost of Goods Sold:

Beginning Finished Goods Inventory

Cost of Goods Manufactured*

Cost of Goods Available for Sale

Ending Finished Goods Inventory

Cost of Goods Sold

Gross Profit

Selling and Administrative Expenses:

Sales Salaries Expense

Delivery Expense

Customer Service Hotline Expense

Total Selling and Administrative Expenses

Net Income (Loss)

Requirement 3

For a manufacturing company, cost of goods sold on the income statement is based on cost of goods

manufactured and the change in Finished Goods Inventory. For a merchandising company, cost of

P16-32A Preparing a schedule of cost of goods manufactured and an income statement for a man-

ufacturing company

Learning Objectives 2, 4

COGM: $169,000

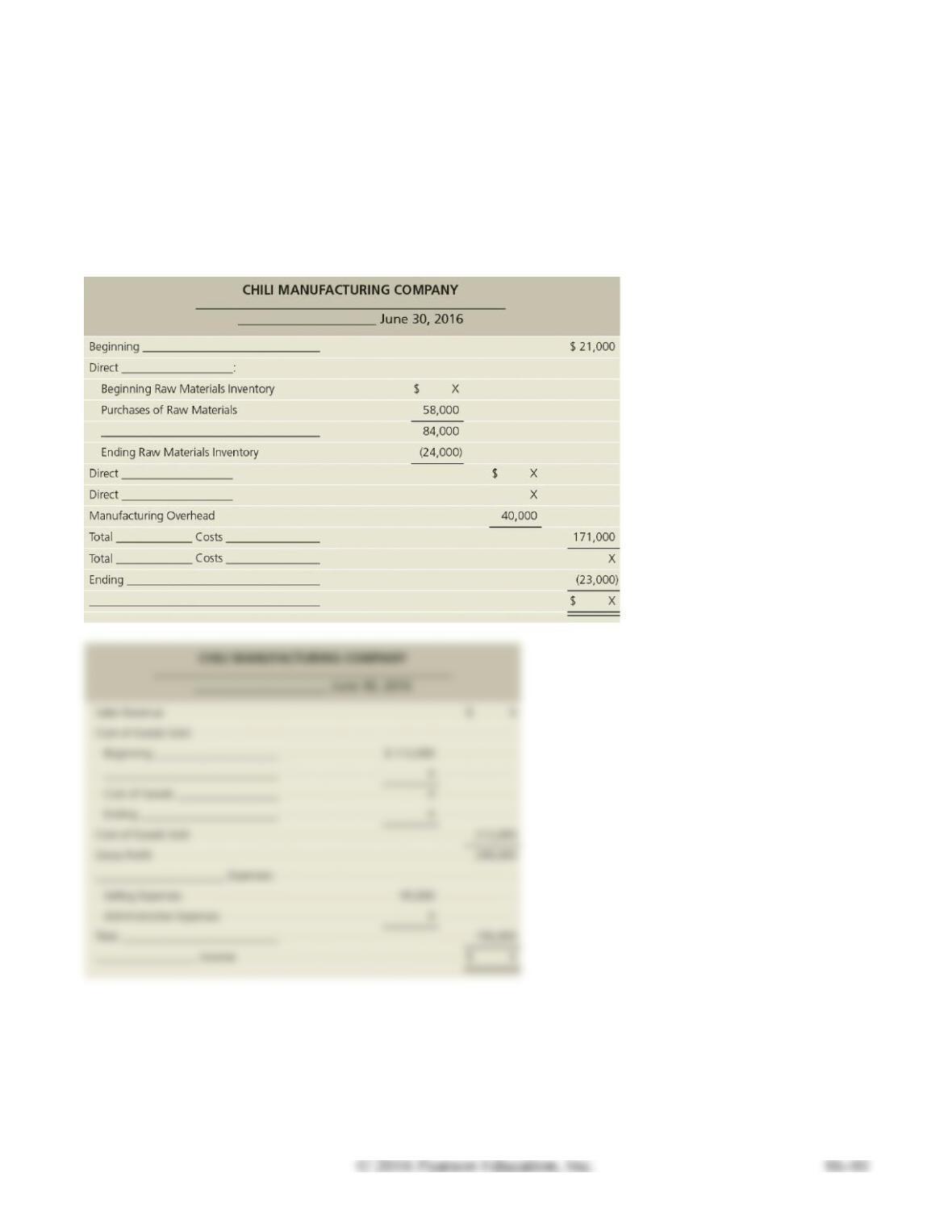

Certain item descriptions and amounts are missing from the monthly schedule of cost of goods manufac-

tured and income statement of Chili Manufacturing Company. Fill in the blanks with the missing words,

and replace the Xs with the correct amounts.