CHAPTER 16

Job Order Costing

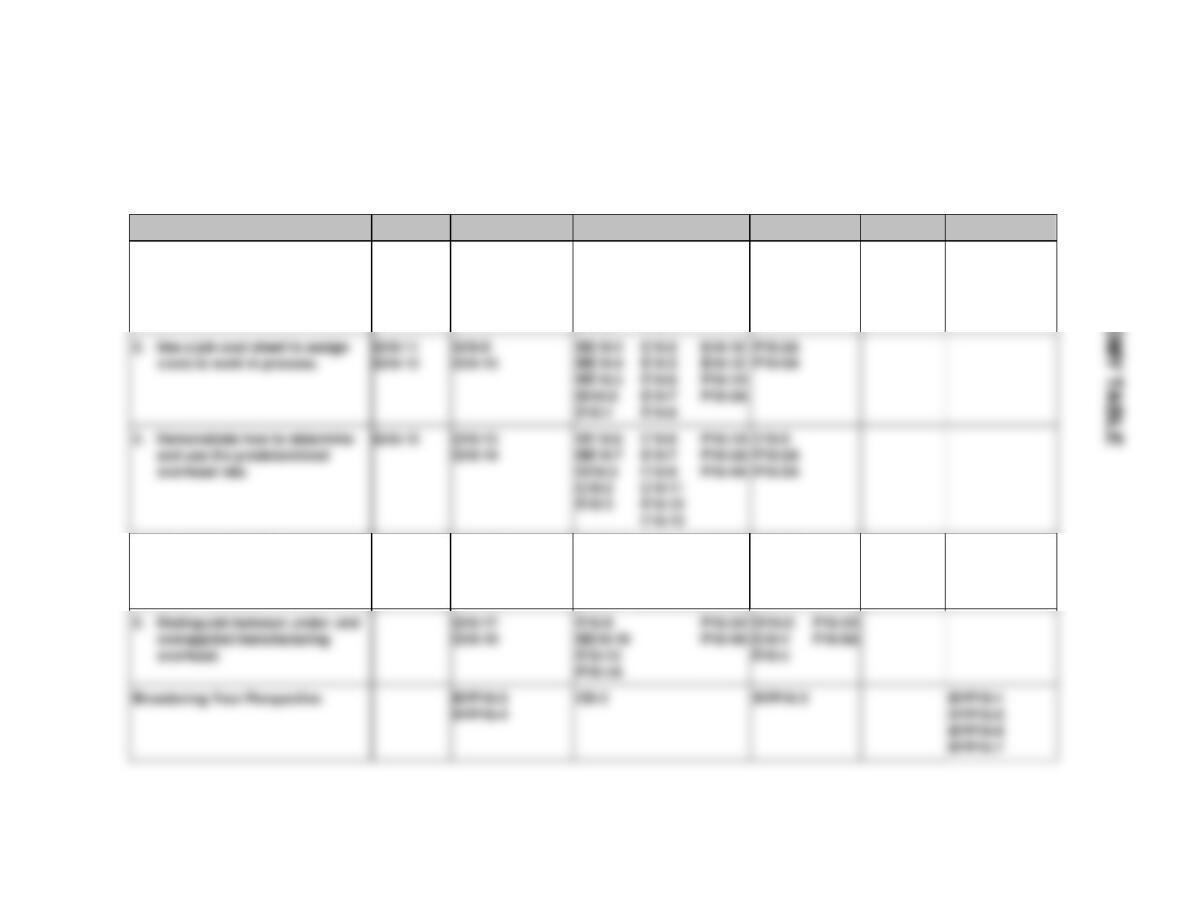

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe cost systems and

the flow of costs in a job

order system.

1, 2, 3, 4, 5,

6, 7, 8

1, 2

1

1, 2, 3, 4, 6,

7, 8, 9, 11

1A, 2A, 3A,

5A

4. Prepare entries for

manufacturing and service

jobs completed and sold.

16

8, 9

4

2, 3, 6, 7, 8,

10, 11, 12

1A, 2A, 3A,

5A

5. Distinguish between under–

and overapplied

manufacturing overhead.

17, 18

5

4, 5, 9, 13

1A, 2A, 3A,

4A, 5A

2. Use a job cost sheet to

assign costs to work in

process.

9, 10, 11, 12

2

1, 2, 3, 6, 7,

8, 10, 12

1A, 2A, 3A,

5A

predetermined overhead

rate.

8, 11, 12, 13

4A, 5A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare entries in a job order cost system and job cost

sheets.

Simple

30 40

2A

Prepare entries in a job order cost system and partial

income statement.

30 40

3A

Prepare entries in a job order cost system and cost of

goods manufactured schedule.

Simple

30 40

5A

Analyze manufacturing accounts and determine missing

amounts.

30 40

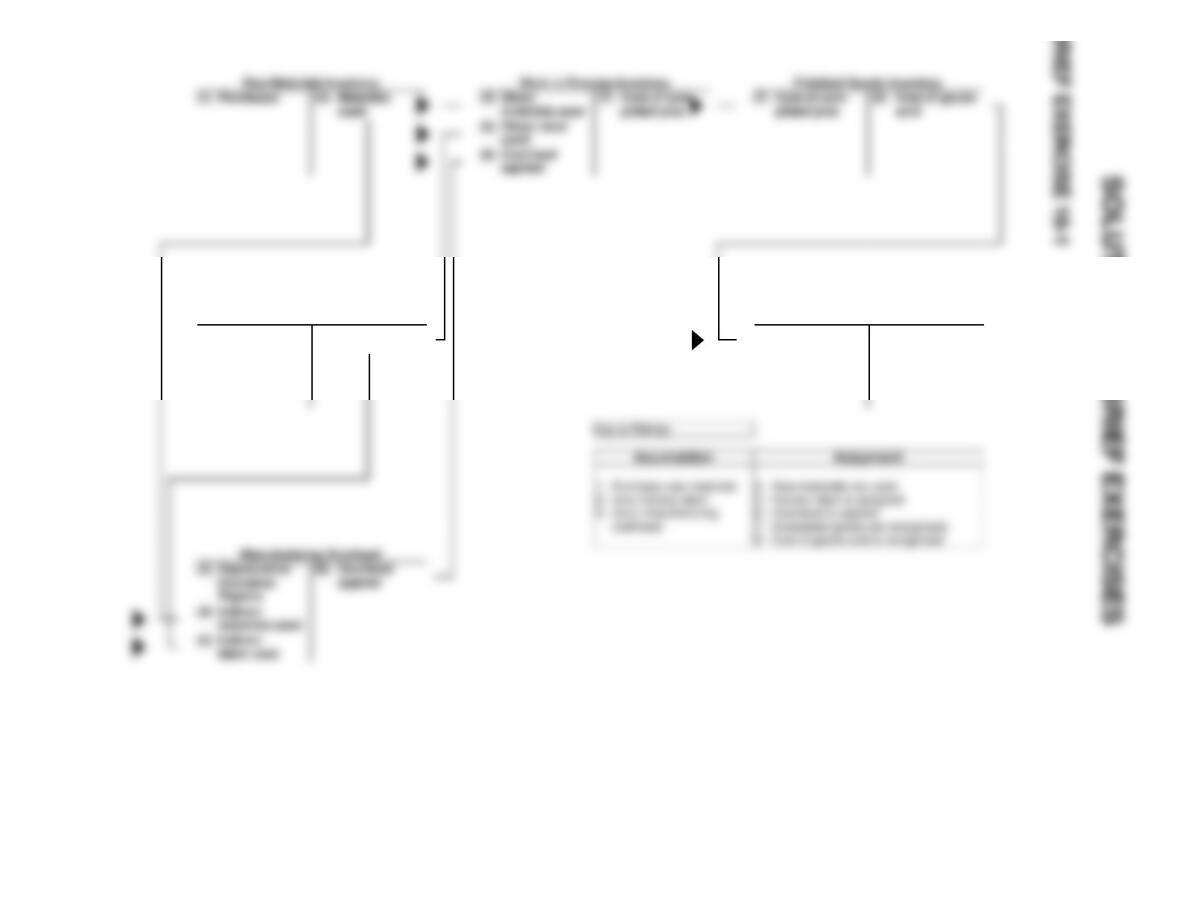

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe cost systems and the

flow of costs in a job order

system.

Q16-5

Q16-7

Q16-8

Q16-1 Q16-4

Q16-2 Q16-6

Q16-3 BE16-1

BE16-2

DI16-1

E16-1

E16-2

E16-3

E16-6

E16-7

E16-8

E16-9

E16–11

P16-1A

P16–3A

E16-4

P16–2A

P16–5A

4. Prepare entries for

manufacturing and service jobs

completed and sold.

Q16–16

BE16-9

BE16-8

DI16-4

E16-2

E16-3

E16-6

E16-7

E16-8

E16–10

E16–11

E16–12

P16–1A

P16–3A

P16–2A

P16–5A

Q16–17

E16-9

P16–3A

DI16-5

BYP16-3

BYP16-1

BYP16-7

BE16-4

E16-1

E16-3

E16-8

E16–12

P16–1A

P16–5A

E16-2

E16-3

E16–11

E16–12

E16–13

ANSWERS TO QUESTIONS

1. (a) Cost accounting involves the measuring, recording, and reporting of product costs. A cost

accounting system consists of manufacturing cost accounts that are fully integrated into the

2. (a) The two principal types of cost accounting systems are: (1) job order cost system and

(2) process cost system. Under a job order cost system, costs are assigned to each job or

batch of goods; at all times each job or batch of goods can be separately identified. A job

order cost system measures costs for each completed job, rather than for set time periods.

Under a process cost system, product-related costs are accumulated by or assigned to

3. A job order cost system is most likely to be used by a company that receives special orders, or

custom builds, or produces heterogeneous items or products; that is, the product manufactured or

the service rendered is tailored to the customer or client’s requests, needs, or situation. Examples

of industries that use job order systems are custom home builders, commercial printing companies,

motion picture companies, construction contractors, repair shops, accounting and law firms,

hospitals, shipbuilders, and architects.

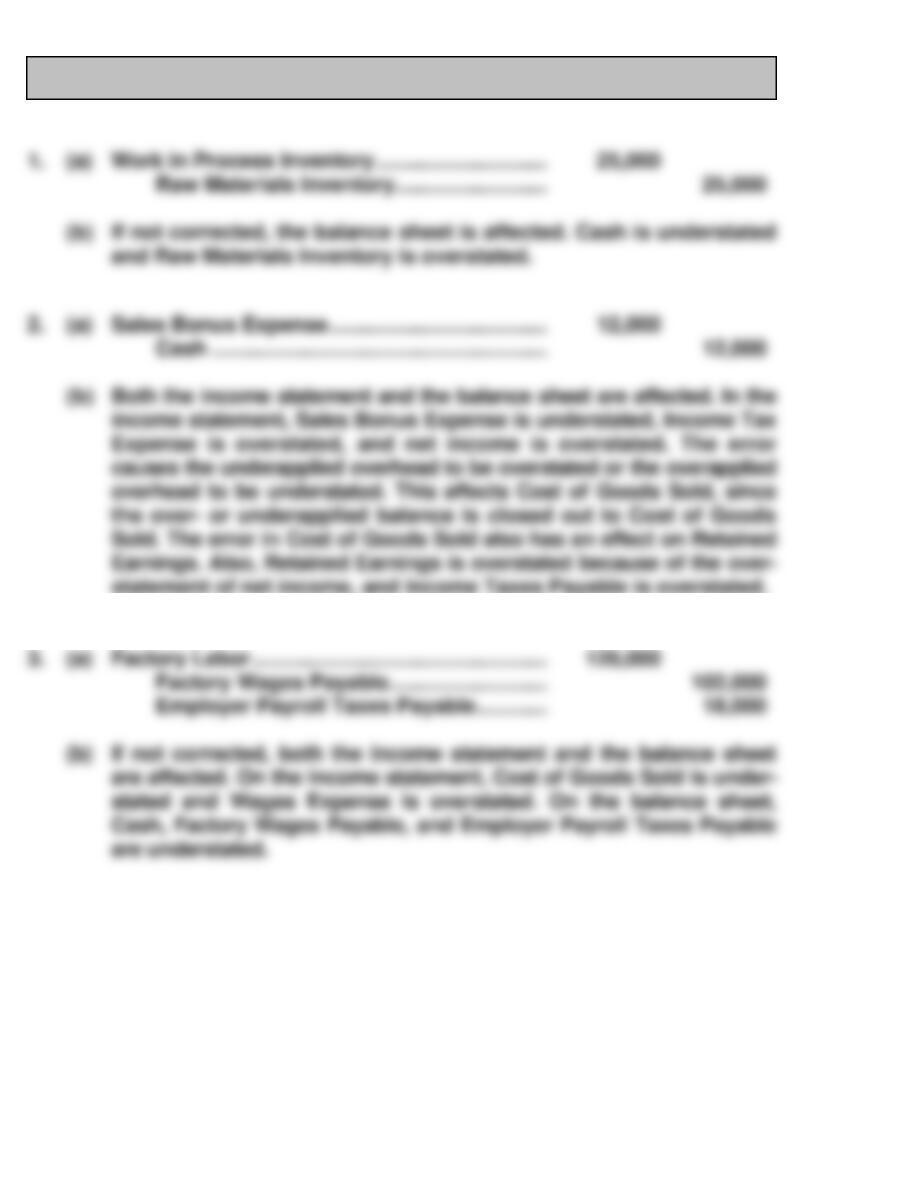

9. The source document for materials is the materials requisition slip and the source document for

labor is the time ticket. The entries are:

Materials

Labor

Raw Materials Inventory

Factory Labor

Questions Chapter 16 (Continued)

10. The purpose of a job cost sheet is to record the costs chargeable to a specific job and to determine

the total and unit costs of the completed job.

14. The relationships for computing the predetermined overhead rate are the estimated annual overhead

costs and an expected activity base such as direct labor hours. The rate is computed by dividing

the estimated annual overhead costs by the expected annual operating activity.

15. At any point in time, the balance in Work in Process Inventory should equal the sum of the costs

shown on the job cost sheets of unfinished jobs. Alternatively, posting to Work in Process Inventory

may be compared with the sum of the postings to the job cost sheets for each of the manufacturing

cost elements.

BRIEF EXERCISE 16-1

Factory Labor

Cost of Goods Sold

(2) Factory labor

incurred

(5) Factory labor

used

(8) Cost of goods

sold

(5) Indirect

(5) Direct labor

(6) Overhead

BRIEF EXERCISE 16-2

BRIEF EXERCISE 16-3

BRIEF EXERCISE 16-4

BRIEF EXERCISE 16-5

Job 1

Job 2

BRIEF EXERCISE 16-7

BRIEF EXERCISE 16-8

BRIEF EXERCISE 16-9

BRIEF EXERCISE 16–10

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 16-1

DO IT! 16-2

DO IT! 16-3

DO IT! 16-4

DO IT! 16-5

SOLUTIONS TO EXERCISES

EXERCISE 16-1

EXERCISE 16-2

(b)

Work in Process Inventory

EXERCISE 16-2 (Continued)

Job Cost Sheets

EXERCISE 16-3

EXERCISE 16-4

EXERCISE 16-4 (Continued)

EXERCISE 16-5

EXERCISE 16-6

EXERCISE 16-7

EXERCISE 16-7 (Continued)

EXERCISE 16-8

EXERCISE 16-8 (Continued)

Computation of cost of jobs finished:

$240,930

EXERCISE 16-9

(a) LOPEZ COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended May 31, 2017

EXERCISE 16-9 (Continued)

(b) LOPEZ COMPANY

(Partial) Income Statement

For the Month Ended May 31, 2017

(c) LOPEZ COMPANY

(Partial) Balance sheet

May 31, 2017

EXERCISE 16–10

EXERCISE 16–11

EXERCISE 16–12

EXERCISE 16–13

SOLUTIONS TO PROBLEMS

PROBLEM 16–1A

PROBLEM 16-1A (Continued)

PROBLEM 16-1A (Continued)

(g)

Finished

Goods Inventory

PROBLEM 16–2A

PROBLEM 16-2A (Continued)

PROBLEM 16–3A

(3) Finished Goods Inventory …………………………………. 14,740

Work in Process Inventory …………………………. 14,740

PROBLEM 16-3A (Continued)

(b)

Work in Process Inventory

PROBLEM 16–4A

(b)

Department

Manufacturing Costs

Total

(c)

Department

Manufacturing Overhead

Under (over) applied

PROBLEM 16–5A

CD16 CURRENT DESIGNS

BYP 16-1 DECISION-MAKING ACROSS THE ORGANIZATION

BYP 16-2 MANAGERIAL ANALYSIS

statement of net income, and Income Taxes Payable is overstated.

BYP 16-2 (Continued)

BYP 16-3 REAL-WORLD FOCUS

BYP 16-4 COMMUNICATION ACTIVITY

Williams Company

Date

Nancy Kopay

123 Cedar Lane

Altoona, Kansas 66651

Dear Ms. Kopay:

BYP 16-4 (Continued)

BYP 16-5 ETHICS CASE

BYP 16-6 ALL ABOUT YOU

BYP 16-7 CONSIDERING YOUR COSTS AND BENEFITS