Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Buying entertainment properties runs counter to decisions by Comcast peers Time Warner and

Cablevision systems, which decided to separate content from distribution. Previous attempts to vertically

integrate by owning and distributing content have shown mixed results. For example, AOL’s acquisition of

The deal reflected complicated financial engineering involving both parties contributing assets to create

a joint venture, agreeing on the total value of the endeavor, determining the value of each party’s

contributed assets to determine ownership distribution, and finally determining how GE would be

compensated. The joint venture transaction based on the value of the assets contributed by both parties was

valued at $37.25 billion, consisting of GE’s contribution of NBCU valued at $30 billion and Comcast’s

contribution of cable network assets valued at $7.25 billion. The ownership interests were determined

The deal enabled General Electric to pursue a staged exit of NBCU over a number of years. In doing so,

GE hoped that the potential synergy with Comcast would increase substantially the value of its share of the

joint venture. GE had negotiated redemption rights (a put option) for the six months beginning January 28,

2014 to redeem one-half of its interest in the joint venture. In the six months beginning on January 28,

2018, GE could redeem its remaining interest. The redemption price was to be equal to 120% of NBCU’s

What is perhaps most remarkable about Comcast’s early 2013 announcement that it would purchase the

remaining portion of NBCU that it did not own is that it is coming much earlier than expected. While

Comcast had intended to acquire GE’s 49% eventually, a confluence of events accelerated this process. The

decision appears to have been driven largely by Comcast’s belief that it would end up paying substantially

more for GE’s ownership interest if it had waited until 2018 as was envisioned when the joint venture was

created in early 2011. The decision also reflected Comcast’s growing confidence in the ongoing viability of

TV, even as the growth of Internet video reshapes the entertainment landscape, and the more rapid than

Other factors spurring the deal may have included cultural clashes between the more formal and cost

conscious Comcast and NBCU’s staff, record low borrowing costs, and rising retransmission and

programming fees that NBCU can charge other pay TV operators for the broadcast and cable networks.

While Comcast’s cable margins are shrinking due to rising operating costs, NBCU’s margins are expected

to increase due to their ability to charge for content and the expectation that such fees will continue to rise

in the future. Complete ownership of NBCU will let Comcast benefit from the rising price of payments

made for the rights to show certain sporting events and other TV programs as Comcast will own 100% of

such content. Long-term rights deals between TV networks and their cable and satellite distributors have

bolstered the importance of TV.

22

In completing the takeover of NBCU, Comcast agreed to pay $16.7 billion for GE’s remaining 49%

stake in the NBCU joint venture and $1.4 billion for Thirty Rockefeller Center and other real estate assets.

At $18.1 billion, the purchase price for all these assets will be funded by $11.4 billion in cash held by

Comcast, $4.0 billion in senior unsecured debt securities issued by Comcast to GE, $2 billion from

Comcast’s existing credit facilities and $725 million in preferred stock. The interest rate on the

Discussion Questions:

1. Speculate as to why GE may have found it difficult to manage NBC Universal. Be specific.

Answer: GE is a highly diversified organization in infrastructure, manufacturing, financial

services, and media businesses. The lack of relatedness makes it exceedingly difficult for the

conglomerate to realize meaningful synergies among the businesses. More importantly, the

2. What are the critical assumptions underlying Comcast’s decision to exercise its option to

acquire the remainder of NBCU that it did not own at an earlier date than anticipated? What

are GE’s?

Answer: GE had always intended to exit NBCU; the only question was when. Comcast and

GE presumably viewed the longer-term outlook for media and entertainment assets quite

3. Explain why GE might have been willing to accept subordinated debt and preferred stock for

such a large part of the purchase price? Why might Comcast want to use debt and preferred

equity as part of the purchase price?

Answer: GE was in a hurry to exit NBCU entirely due to a desire to focus on its core

industrial businesses and due to cultural differences. Also, GE’s expectations for growth in

4. In what way can the Comcast/GE JV created in 2011 be viewed as a phased entry strategy

into owning content for Comcast and as a phased exit strategy for GE?

23

5. What is the form of payment and acquisition? What portion of the purchase price might be

immediately taxable to GE and on what portion might taxes be deferred and why?

Answer: The form of payment consists of cash, senior subordinated debt, and preferred stock.

The form of acquisition is the remaining NBCU equity Comcast did not already own. Of the

Coke Moves from the Vending Machine into the “In-Home” Market

______________________________________________________________________________________

Key Points

• Business alliances can provide comparatively low cost access to new product distribution

channels.

• While money invested in business alliances does matter, the eventual success of alliances often

depends on the value of the intangible and tangible assets contributed by each partner.

______________________________________________________________________________________

Henry Ford was quoted as saying about the iconic Model T car that “the consumer could have any color

they wanted as long as it was black.” Businesses have long since learned that the key to successfully

growing a business was meeting or exceeding primary customer needs. We have moved from mass

merchandizing (one size fits all) to mass customization (products reflecting a consumer’s tastes). The desire

of consumers to tailor products to reflect their own desires seems to have made it into the soft drink market.

With the overall U.S. non-alcoholic beverage market showing little growth in recent years, beverage

makers are seeking ways to spur new sales. Energy drinks and single serve coffee is growing at a double-

Israeli-based SodaStream International has had a virtual monopoly on “in-home carbonization systems.”

Its machines allow consumers to make their own sparkling water as well as drinks that blend multiple

flavors. The firm sells “do-it-yourself” carbonation machines as well as the flavor syrups used in the

machines. Reflecting the popularity of its product, the firm has been able to double its annual revenue each

SodaStream’s success forced Coca-Cola to take notice. In a move that represents a significant departure

from its traditional business, Coke entered into a partnership with Green Mountain Coffee Roasters in 2014

to in effect move its products from the vending machine into the kitchen. The nation’s leading beverage

maker inked a 10 year agreement with Green Mountain to sell coke products that are compatible with

Green Mountain’s in-home cold beverage system. Many consumers already are familiar with Green

Mountain’s single serving coffee machines.

24

The ability to use the machine to make well-known brand name drinks is expected to hype sales of the

machines. Green Mountain CEO Brian Kelley emphasized this point by noting that “In hot beverages, the

power of Keurig (coffee machines) comes from the fact that we have the world’s best coffee brands on it.”

The major selling point for the Keurig Cold system is that it will have the best cold beverage brands on it

such as Coke. Since the deal is not exclusive, Green Mountain can look for deals with other companies to

expand the range of cold beverages available on the machine.

Nokia Gambles on Microsoft in the Smartphone Wars

______________________________________________________________________________________

Key Points

An alliance may represent a low-cost alternative to a merger or acquisition.

Selecting an alliance partner must be done judiciously to avoid competing with a firm’s own customers or

partners, cannibalizing its own product offering, or unintentionally transferring proprietary information

and technology.

____________________________________________________________________________________

Smartphones outsold personal computers for the first time in the fourth quarter of 2010. The Apple

iPhone and devices powered by Google’s Android operating system have won consumers with their sleek

touchscreen software and with an army of developers creating applications for their devices. In just three

years, they have captured the largest share of the market. These developments put Microsoft’s core

business, selling software for PCs, in jeopardy and have caused Finnish phone handset manufacturer

Nokia to fall further behind in its efforts to compete with Apple and makers of Android-based devices in

the smartphone market.

25

were anticipated in 2011, a substantial increase in volume was not expected before 2013. Nokia could

have partnered with Google, as have many handset manufacturers. However, it would require that the

firm compete with the likes of Samsung, HTC, and Motorola—all makers of Android-powered

smartphones.

Under the agreement with Microsoft, WP7 becomes Nokia’s primary smartphone platform; Nokia also

agreed to help introduce WP7-powered smartphones in new consumer and business markets throughout

the world. The two firms will jointly market their products and integrate their mobile application online

The alliance enables Nokia to adopt new software (WP7) with an established community of

developers but that has sold relatively poorly since its introduction in late 2010. With the phase-out of its

discontinued Symbian operating system over a period of years, Nokia will be able to reduce substantially

its own research and development and marketing budgets. Microsoft will also benefit from Nokia’s

extensive intellectual property portfolio in the mobile market to strengthen the WP7 system. For

Microsoft, the deal represents a major opportunity to boost lagging sales in the mobile phone market and

gives it access to Nokia’s brand recognition.

Despite having been an early entrant into the smartphone business, Microsoft had been unable to gain

significant market share. Over the years, Microsoft has struck deals with many of the world’s best known

cellphone manufacturers, including Motorola and HTC Corp. But these alliances were hampered either by

execution problems or by an inability of Microsoft to prevent handset makers from shifting to other

Elop also announced that effective April 1, 2011, Nokia would be reorganized into two business units:

Smart Devices and Mobile Phones. The Smart Devices unit would focus on manufacturing the new

Windows Phone 7 devices. The Smart Devices business must compete in the smartphone market against

the likes of those producing handsets powered by the Google operating system, Blackberry, and Apple

with only the Windows Phone 7–powered phone. The Mobile Phones operation would continue to

Investors expressed their disapproval of the deal, with Nokia’s stock falling 11% on the

announcement. Similarly, Microsoft’s shares fell by 1% as investors expressed concern that the firm had

teamed with a weak player in the smartphone market and that the two-year transition period before WP7-

based smartphones would be sold in volume would allow only Android-based smartphones and iPhones

to get further ahead.

26

which sued the firm for alleged monopolies in its Windows and Office products. European companies

have been much faster to adopt open-source solutions, often in an effort to replace Microsoft software.

Discussion Questions

1. Conduct an external analysis of the smartphone market place (see Chapter 4).

Answer: Smartphones are showing signs of replacing PCs in some applications, as they

2. Conduct an internal analysis of Nokia and Microsoft (see Chapter 4).

Answer: Both companies have demonstrated substantial core capabilities: Microsoft in

operating system software and Nokia in making exceptionally high quality hardware.

3. What alternatives to a partnership did Nokia and Microsoft have? Why was a partnership

selected as the means of implementing the firm strategy to enter the smartphone market?

Answer: Microsoft could have acquired Nokia. With its lack of success in a prior partnership

in its effort to penetrate the smartphone marketplace, gaining control may have been an

appropriate strategy. In partnerships in which neither partner products or services are to be

4. Who do you believe benefitted most from the partnership (Microsoft or Nokia) and why?

Answer: While both partners need the other, Microsoft would seem to be the primary

beneficiary if the partnership is successful. On the surface, success in the smartphone market

General Electric and Comcast Join Forces

____________________________________________________________________________________

Key Points

Joint ventures are sometimes created if a business cannot be sold outright.

Such JVs are viewed as a way of improving a firm’s operations enabling the parent to exit the business

eventually at a higher value.

In an effort to shore up its big finance business, severely weakened during the 2008 financial crisis, and

to focus more on its manufacturing and infrastructure operations, General Electric (GE) sought to sell its

media and entertainment business, NBCUniversal. GE’s decision to sell also reflected the deteriorating

state of the broadcast television industry and a desire to exit a business that never quite fit with its

industrial side. NBC has been mired in fourth place among the major broadcast networks, and the

Unable to find a buyer for the entire business at what GE believed was a reasonable price, GE sought

other options, including combining the operation with another media business. After extended

discussions, GE and Comcast announced a deal on December 2, 2009, to form a joint venture consisting

of NBCUniversal and selected Comcast assets. Comcast is primarily a cable company and provider of

programming content, with 24.3 million cable customers, 16.1 million high-speed Internet customers, and

7.8 million voice customers. Comcast hopes to diversify its holdings as it faces encroaching threats from

online video and more aggressive competition from satellite and phone companies that offer subscription

TV services, by adding more content on its video-on-demand offerings. Furthermore, by having an

interest in NBCUniversal’s digital properties, such as Hulu.com, Comcast expects to capitalize on any

shift of its cable customers to viewing their favorite TV programs online by owning the program content.

The announcement raised significant concerns within the media and entertainment industry about the

potential for limiting access to both content and distribution by increasing industry concentration. After

receiving significant concessions, regulators approved the creation of the joint venture media giant on

January 17, 2011. The U.S. Federal Communications Commission and the Department of Justice required

Comcast and NBCUniversal to relinquish voting rights and board representation to Hulu, although they

28

“reasonable access” to its programming for its competitors, and the firm may not discriminate against

programming that competes with its own offerings.

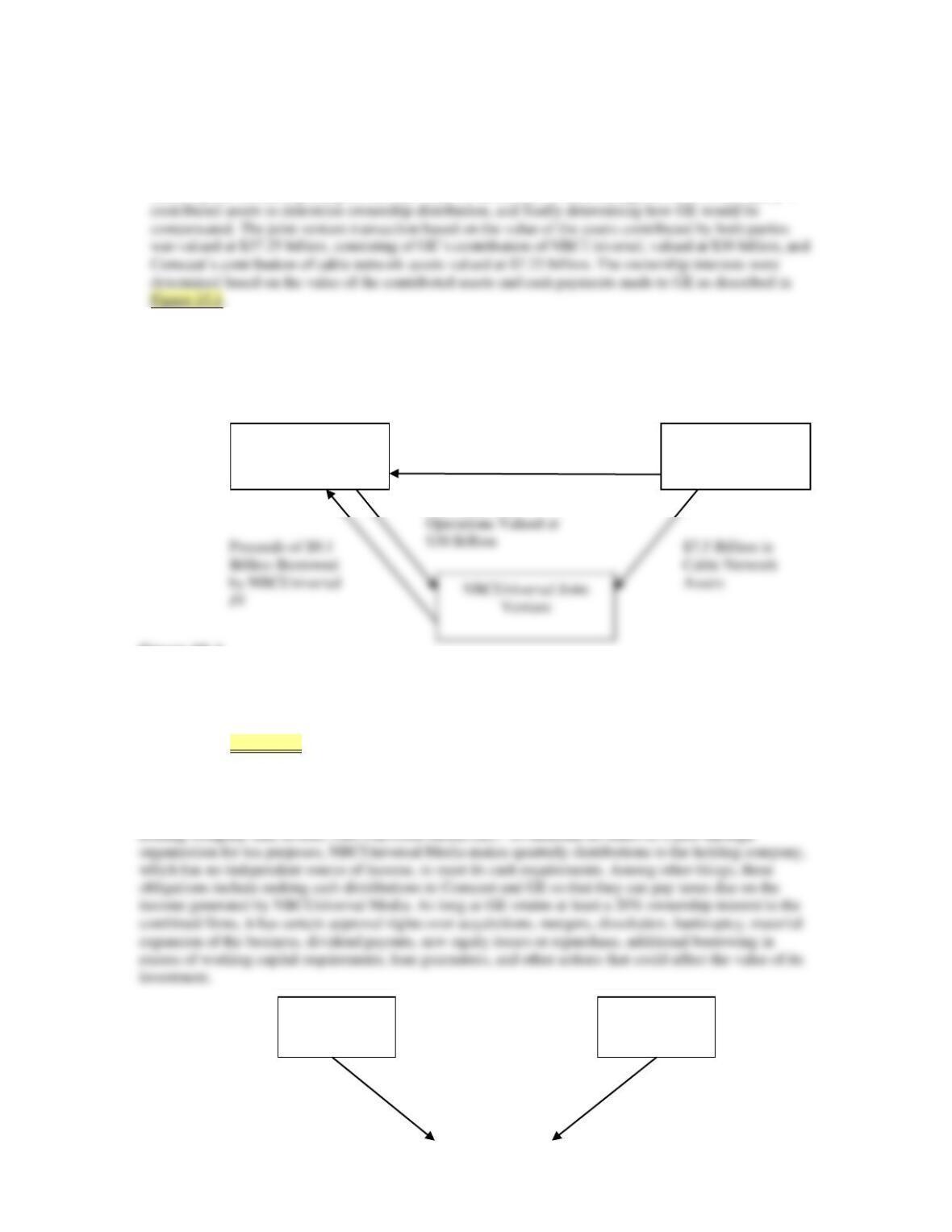

The deal reflected complicated financial engineering, involving both parties contributing assets to

create a joint venture, agreeing on the total value of the endeavor, determining the value of each party’s

In exchange for contributing NBCUniversal operations valued at $30 billion to the JV, GE received $15.6

billion in cash ($6.5 billion from Comcast + $9.1 billion borrowed by the NBCUniversal JV) + a 49%

ownership interest in the NBCUniversal JV).

In exchange for contributing $7.5 billion in cable network assets to the JV and paying GE $6.5 billion in

cash, Comcast received a 51% interest in the NBCUniversal JV.

Figure 15.1

NBCUniversal Joint Venture at Closing.

Organizationally, the two parties own NBCUniversal indirectly through their ownership in a holding

company (see Figure 15.2). As part of the deal, NBCUniversal Inc. was converted to a limited liability

company (NBCUniversal Media LLC), which is a wholly owned subsidiary of NBCUniversal Holdings

Inc., a corporation in which Comcast owns 51% of the outstanding shares and GE the remainder.

NBCUniversal Holdings is the sole member (owner) in NBCUniversal Media LLC. By having the right to

designate the majority of the board members of NBCUniversal Holdings, Comcast effectively controls the

General Electric

Comcast

$6.5 Billion in Cash

NBCUniversal

Comcast

General

Electric

29

Figure 15.2

NBCUniversal Postclosing Organization

Finally, the deal enables General Electric to pursue a staged exit of NBCUniversal over a number of

years. In doing so, GE hopes that the potential synergy with Comcast will increase substantially the value

of its share of the joint venture. GE has redemption rights (a put option) during the six months beginning

January 28, 2014, to redeem one-half of its interest in NBCUniversal Holdings. In the six months beginning

on January 28, 2018, GE can redeem its remaining interest. Comcast is committed to funding $2.9 billion

for each of the two redemptions, payable in cash and stock up to $5.8 billion to the extent NBCUniversal

Media cannot fund the redemptions. The purchase price to be paid with any redemption by GE will be

120% of the “public market trading value” of NBCUniversal Holding, to be determined by an appraisal if

Discussion Questions

1. Speculate as to why GE may have found it difficult to manage NBC Universal. Be

specific.

Answer: GE is a highly diversified organization in infrastructure, manufacturing, financial

services, and media businesses. The lack of relatedness makes it exceedingly difficult for the

2. Why was the NBC Universal joint venture used to borrow the $9.1 billion paid to GE?

How might this impact the ongoing operation of NBCUniversal? What are the trade-offs the

partners are making in agreeing to fund a portion of the purchase price through

NBCUniversal?

Answer: By having NBCUniversal borrow the $9.1 billion, Comcast and GE may be able to

protect themselves from its creditors if the firm goes into bankruptcy because such loans are

NBCUniversal

Holdings, Inc.

NBCUniversal

LLC.

49% Ownership

Interest

51% Ownership

Interest

30

3. Speculate as to the potential circumstances in which either Comcast or GE would be

likely to exercise their call or put options? Which party do you believe is likely to exercise

their options first and why?

4. What are the likely challenges Comcast and GE will have in integrating the various

businesses that comprise the joint venture? Be specific.

5. Why did Comcast and GE choose to operate NBCUniversal as a limited liability

company rather than a corporation?

6. Speculate as to why the partners chose to operate NBCUniversal Media through a

holding company.

Answer: The holding company arrangement allows the two partners to indirectly own

Exxon-Mobil and Russia’s Rosneft Create Artic Oil and Gas Exploration Joint Venture

________________________________________________________________

Key Points

Contractual commitments in cross-border alliances are effective only to the extent they are enforced by

each country’s legal system.

The success of most alliances ultimately depends on the extent to which each partner needs the capabilities

and resources of the other.

______________________________________________________________________________

31

Exxon-Mobil (Exxon) finalized an agreement with the government-owned Russian oil and gas giant

Rosneft on April 16, 2012, to create a joint venture to explore for oil and gas in three designated areas in

the Russian portion of the Artic Ocean known as the Kara Sea. The agreement superseded a similar but

failed agreement with British Petroleum (BP) earlier in the year. Rosneft’s attempt to strike a similar pact

The U.S. Geological Survey estimates that the Artic holds one-fifth of the world’s undiscovered,

recoverable oil and natural gas. The Kara Sea has an estimated 36 billion barrels of recoverable oil

reserves. Total oil and gas reserves are estimated to be 110 billion barrels of oil equivalent, four times

Exxon’s proven worldwide reserves. Drilling is expected to start in 2015, with Exxon shouldering most of

the costs. In exchange for access to these Rosneft properties, the agreement gives Rosneft an option to

invest in certain U.S. properties. Rosneft will own two-thirds and Exxon the remainder of the joint venture.

The initial commitment by the two companies is to invest $3.2 billion in exploration in the Kara Sea.

The Russian government had long demanded reciprocity as part of any deal. This required that in

exchange for any ownership in Russian assets, the Russian partner should have the opportunity to invest in

assets owned by the other partner. The value of the assets Rosneft would own in the United States would be

in proportion to those Exxon would own in Russia. The agreement is risky, in view of Russia’s history of

reneging on deals with Western oil companies. For example, in 2006, it compelled Royal Dutch Shell to

sell 50% of a Sakhalin offshore property to state-owned Gazprom after Shell had spent more than $20

billion of its own money and that of other investors to build the project’s infrastructure.

British Petroleum and Russia’s Rosneft Swap Shares

Extending its already close ties with Russia, British Petroleum PLC announced an agreement to exchange

shares with Russia’s largest oil company, OAO Rosneft, on January 14, 2011. Rosneft is 75% owned by the

Russian government. BP and Rosneft also announced the formation of a JV to develop three massive

offshore exploration blocks that Rosneft owns in northern Russia. The two firms said they will jointly

explore three areas in the South Kara Sea in the Russian Arctic, spending between $1.4 and $2 billion on

seismic tests and drilling wells in the initial exploration phase. The JV will be two-thirds owned by

Rosneft, with the remainder owned by BP.

32

The deal comes in the wake of BP’s sale of assets to raise funds to cover the costs of the Gulf of Mexico

oil spill in mid-2010. Such costs are expected to eventually total $40 billion. Rosneft, which had announced

in late 2010 that it was seeking a partner for exploiting its Arctic leases, indicated that BP’s experience in

dealing with such problems gives it an edge over other potential partners. Rosneft also regards BP’s deep-

water drilling technology and experience as cutting edge. BP’s expertise received another vote of

confidence when Australia granted BP licenses to initiate extensive drilling activity off its coast several

days after the Rosneft announcement.

At the time of the announcement, BP’s market capitalization was about $154 billion. With almost 90%

of its shares owned by the Russian government and Sherbank, Russia’s biggest retail savings bank, the

firm’s stock trading in public markets tends to be limited and not reflective of Rosneft’s true value.

However, the terms of the share exchange imply a market capitalization for Rosneft of about $81 billion.

The transaction represents the first time there has been a cross-shareholding between major international

oil firms and a major government-owned national oil company. Unlike more conventional oil and gas JVs,

the Rosneft JV will not own the oil leases but merely the right to develop them. This structure is similar to

Russian oil company Gazrpom’s agreement with France’s Total SA and Norway’s Statoil for the

development of the Shtokman gas field in early 2008.

Previous attempts to invest in Russia and to create partnerships between Russian state oil companies and

Western oil firms have failed due to outright expropriation by the Russian government or heavy-handed

tactics employed by certain Russian billionaires (so-called oligarchs) with close ties to the Russian

government. For example, Russian officials forced Shell Oil to sell control of its Sakhalin II oil and gas

development to state-owned Gazprom. BP and Gazprom signed a global joint venture in 2007 in which

each was to contribute assets valued at $1.5 billion, but it was later dissolved due to disagreements between

BP and large Russian investors. TNK-BP, BP’s 50 percent–owned JV with a group of Russian billionaire

business people, has also had a troubled history. The JV that contributes a quarter of BP’s global

production and nearly a fifth of its reserves was rocked by a shareholder dispute in 2008 that cost BP some

Discussion Questions:

33

1. Speculate as to the purpose of the share swap between BP and Resnoft.

Answer: The overarching purpose of the exchange of shares between the two firms is to align

their interests and objectives, communicate to public investors the mutual confidence of both

firms, and to create synergies that will enhance the value of both firms’ shares. It is hoped that

2. What is the purpose of the 2-year lockup period during which neither partner can sell its

stock? How might the lock-up period impact the value of each firm’s holdings?

Answer: Since it is likely that it will take at least several years to tap the reserves believed to

be in the South Kara Sea, the lock-up period forces both parties to remain focused long

3. Would you expect the share exchange to be dilutive to BP shareholders in the short-run? In

the long-run. Explain your answer.

Answer: The dividend paid on BP shares is twice that paid on Rosneft common shares and the

deal requires that BP issue new voting shares. Consequently, the deal is likely to reduce the

4. Why would you expect the publicly traded Rosneft shares not to reflect the true value of the

firm?

Answer: The public, noninstitutional shareholders own only about 12 percent of the firm’s

outstanding shares. Consequently, they should reflect both a substantial liquidity and minority

5. How would you estimate the market capitalization for Rosneft based on the terms of the share

exchange? Show your work.

Answer: A share exchange ratio is defined as the offer price expressed as a market value

(MV) or price per share for a target firm divided by the acquiring firm’s current market value