Chapter 15

International Capital Budgeting

QUESTIONS

1. Can an investment project of a foreign subsidiary that has a positive net present value

when evaluated as a stand-alone firm ever be rejected by the parent corporation?

Assume that the parent accepts all projects with positive adjusted net present values.

Answer: Yes, we know that countries impose withholding taxes on the dividends that are

2. How do licensing agreements, royalties, and overhead allocation fees affect the value of

a foreign project?

Answer: Licensing agreements, royalties, and overhead allocation fees are true costs to the

3. Why does an adjusted net present value analysis treat the present value of financial side

effects as a separate item? Isn’t interest expense a legitimate cost of doing business?

Answer: The adjusted net present value approach to capital budgeting starts by valuing the

free cash flows to the all-equity cash firm. It then adds other sources of value associated with

4. What is meant by the net present value of the financial side effects of a project?

5. Why is it costly to issue securities?

6. What is an interest tax shield? How do you calculate its value?

Answer: The interest tax shield on a debt is the value of the ability to deduct interest as a

7. What is an interest subsidy? How do you calculate its value?

Answer: Interest subsidies arise when governments are willing to lend to corporations at

below market interest rates. Such subsidies add value to a project. The appropriate discount

Chapter 15: International Capital Budgeting

3

8. What are growth options? Provide an example of one in an international context.

Answer: A growth option arises when a firm undertakes a project and obtains an option to do

9. What is the difference between EBIT and NOPLAT?

10. Why is it important to understand and manage net working capital?

Answer: The stock of net working capital is the amount of inventory, cash, and accounts

11. What does CAPX mean, and why is it a firm’s engine of growth?

Chapter 15: International Capital Budgeting

4

12. Why is it sometimes assumed that CAPX equals depreciation in the later stages of a

project? How does expected inflation affect this assumption?

Answer: As a project matures, there are no more planned investments in which case the scale

of the project is fixed. But, the physical plant and equipment have an economic lifetime and

13. What is the terminal value of a project? How is it calculated?

Answer: The terminal value of a project is the present discounted value of all future free cash

flows in the years beyond an explicit forecasting horizon. If we generate explicit forecasts of

14. What is meant by the cannibalization of an export market?

Chapter 15: International Capital Budgeting

5

Answer: When a MNC chooses to change how it services a market to which it is exporting,

either because the MNC is building a new plant in the foreign country or expanding

15. What are the primary sources of value to IWPI-U.S. in establishing a Spanish

subsidiary?

16. Why are the profits on exports of intermediate parts by IWPI-U.S. to IWPI-Spain

included in the value of the project?

17. What risks are present in the IWPI-Spain project? How do they affect the value of the

project?

Answer: The primary source of risk is the business risk of selling wooden furniture in

Europe. The expected free cash flows of the project are taken from a probability distribution

Chapter 15: International Capital Budgeting

6

PROBLEMS

1. What percentage of the adjusted net present value of the IWPI-Spain project arises

from the dividends that will occur more than 10 years in the future?

2. How sensitive is the value of IWPI-Spain to the assumed discount rate of 11.1%? What

happens to the value of the project if the rate is 12.1% instead?

Answer: When the project was discounted with 11.1%, upon adding together all the costs and

benefits of the project, we found

ANPV of IWPI-Spain = – €178.66 million in initial costs

3. What would be the terminal values of the dividends from IWPI–Spain if they were

expected to grow in real terms at 1% rather than 0%?

4. How much does the value of IWPI-Spain, viewed as a stand-alone firm, change if the

royalty fee is increased by 1% and the overhead allocation fee is reduced by 1%? What

is the change in value to IWPI-U.S.? What is the source of this change in value?

Answer: We know that because the royalty and the overhead fee are costs to the stand-alone

5. Valuing Metallwerke’s Contract with Safe Air, Inc.

Consider the discounted expected value of the 10-year contract that Metallwerke may

sign with Safe Air in Chapter 9. In the initial year of the deal, Metallwerke sells an air

tank to Safe Air for $400. It costs

€

238 to produce an air tank. The current exchange

rate is $1.40/

€

. Assume that 15,000 air tanks will be sold the first year. Make the

following other assumptions in your valuation:

a. The demand for air tanks is expected to grow at 5% for the second year, 4% for the

third and fourth years, and 3% for the remaining life of the contract.

b. Euro-denominated costs are expected to increase at the euro rate of inflation of 2%.

c. The base dollar price of the air tank will be increased at the U.S. rate of inflation

plus one-half of any real depreciation of the dollar relative to the euro, but the base

dollar price will be reduced by one-half of any appreciation of the dollar relative to

the euro. The U.S. rate of inflation is expected to be 4%.

d. The dollar is currently not expected to strengthen or weaken in real terms relative

to the euro.

e. The German corporate income tax rate is 30%.

f. The appropriate euro discount rate for the project is 12%.

g. Metallwerke typically establishes an account receivable for its customers. At any

given time, the stock of the account receivable is expected to equal 10% of a given

year’s revenue.

h. Accepting the Safe Air project will not require any major capital expenditures by

Metallwerke.

Can you determine the value of the contract to Metallwerke?

Chapter 15: International Capital Budgeting

8

Valuing Metallwerke’s 10-year Contract with Safe Air

Year

01 2 3 4 5 6 7 8 9 10

US Inflation 4% 4% 4% 4% 4% 4% 4% 4% 4% 4%

Euro Inflation 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

6. Deli-Delights Inc.

Deli-Delights Inc. is a U.S. company that is considering expanding its operations into

Japan. The company supplies processed foods to storefront delicatessens in large cities.

This requires Deli-Delights to have a centralized production and warehousing facility in

each of these cities. Deli-Delights has located a possible site for a Japanese subsidiary in

Tokyo. The cost to purchase and equip the facility is ¥765,000,000. Perform an ANPV

analysis to determine whether this is a good investment, under the following

assumptions:

a. The average per-unit sales price will initially be ¥410.

b. First-year sales will be 15 million units, and physical sales will then grow

at 10% per annum for the next 3 years, 5% per annum for the 3 years

after that, and then stabilize at 3% per annum for the indefinite future.

c. First-year variable costs of production will be ¥225 per unit of labor and

$1.75 per unit of imported semi-finished goods. Administrative costs will

be ¥300 million.

d. Depreciation will be taken on a straight-line basis over 20 years.

Chapter 15: International Capital Budgeting

11

e. Retail prices, labor costs, and administrative expenses are expected to rise

at the Japanese yen rate of inflation, which is forecast to be 1%. Dollar

prices of semi-finished goods are expected to rise at the U.S. dollar rate of

inflation, which is expected to be 4%.

f. The yen/dollar exchange rate is currently ¥85/$, and the yen is expected

to appreciate at a rate justified by the expected inflation differential

between the yen and dollar rates of inflation.

g. There will be a 4% royalty paid by the Japanese subsidiary to its U.S.

parent.

h. The Japanese corporate income tax rate is 37.5%, and there is a 10%

withholding tax on dividends and royalty payments.

i. The yen-denominated equity discount rate for the project is 13%.

j. Net working capital will average 6% of total sales revenue.

k. Capital expenditures will offset depreciation.

l. All of the Japanese subsidiary’s free cash flow will be paid to the parent

as dividends.

m. The corporate income tax rate for the United States is 34%.

n. Deli-Delights Inc. has sufficient other foreign income that will allow it to

fully utilize any excess foreign tax credits generated by its Japanese

subsidiary.

o. Deli-Delights Inc. does not plan to issue any debt associated with this

project.

Answer: The solution is presented in the following spread sheet pages. The first lays out the

facts. Inflation is expected to be 4% in the United States and 1% in Japan. The current

exchange rate is ¥85/$ and is expected to satisfy relative purchasing power parity in which

Chapter 15: International Capital Budgeting

12

0 1 2 3 4 5 6 7 8 9 10

USD Inflation 4% 4% 4% 4% 4% 4% 4% 4% 4% 4%

JPY Inflation 1% 1% 1% 1% 1% 1% 1% 1% 1% 1%

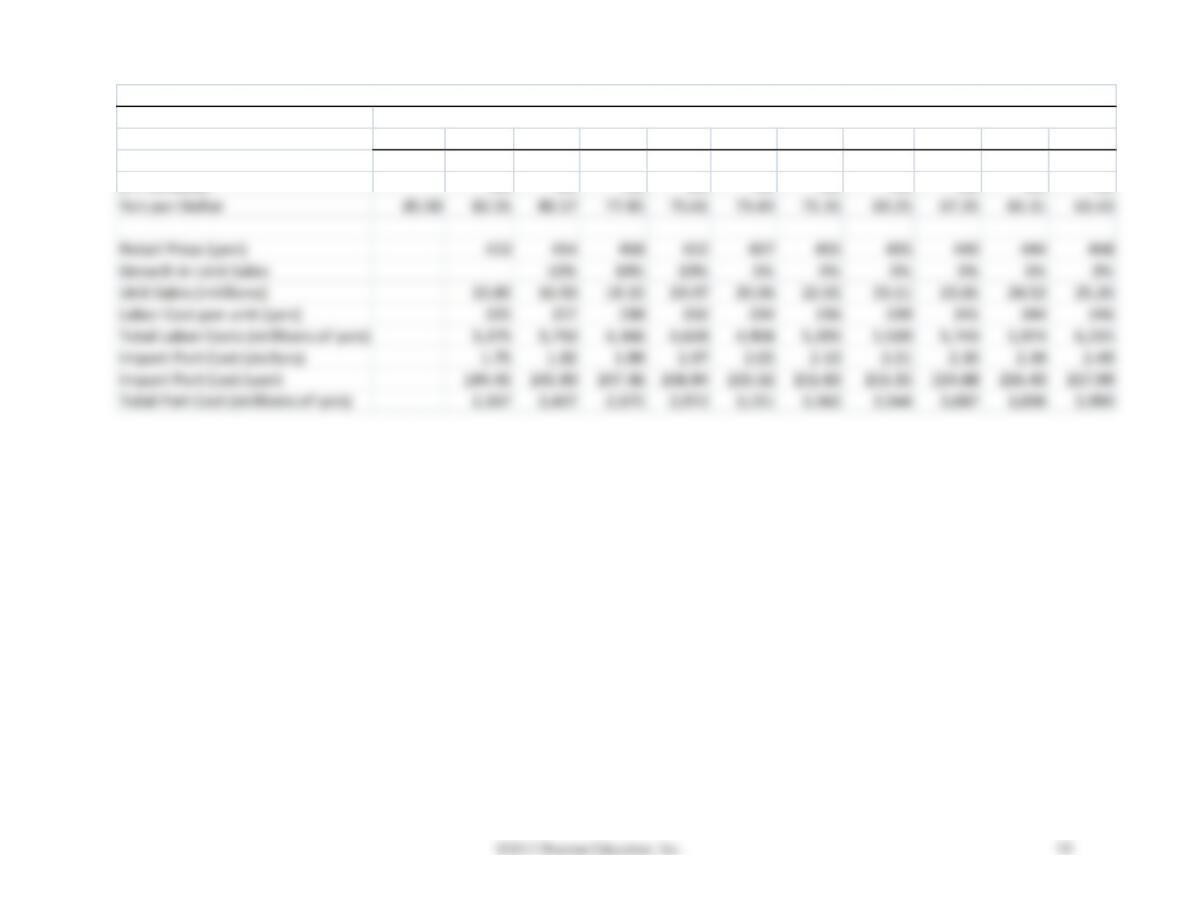

Valuing Deli-Delights Japanese Subsidiary as a Stand-Alone Firm: Basic Data

Year

Chapter 15: International Capital Budgeting

14

0 1 2 3 4 5 6 7 8 9 10

Revenue 6,150 6,833 7,591 8,434 8,944 9,485 10,059 10,464 10,886 11,325

Cost of Goods Sold 5,542 6,157 6,840 7,600 8,060 8,547 9,064 9,430 9,810 10,205

Working Capital 369 410 455 506 537 569 604 628 653 679

Change in Working Capital 369 41 46 51 31 32 34 24 25 26

CAPX = Depreciation

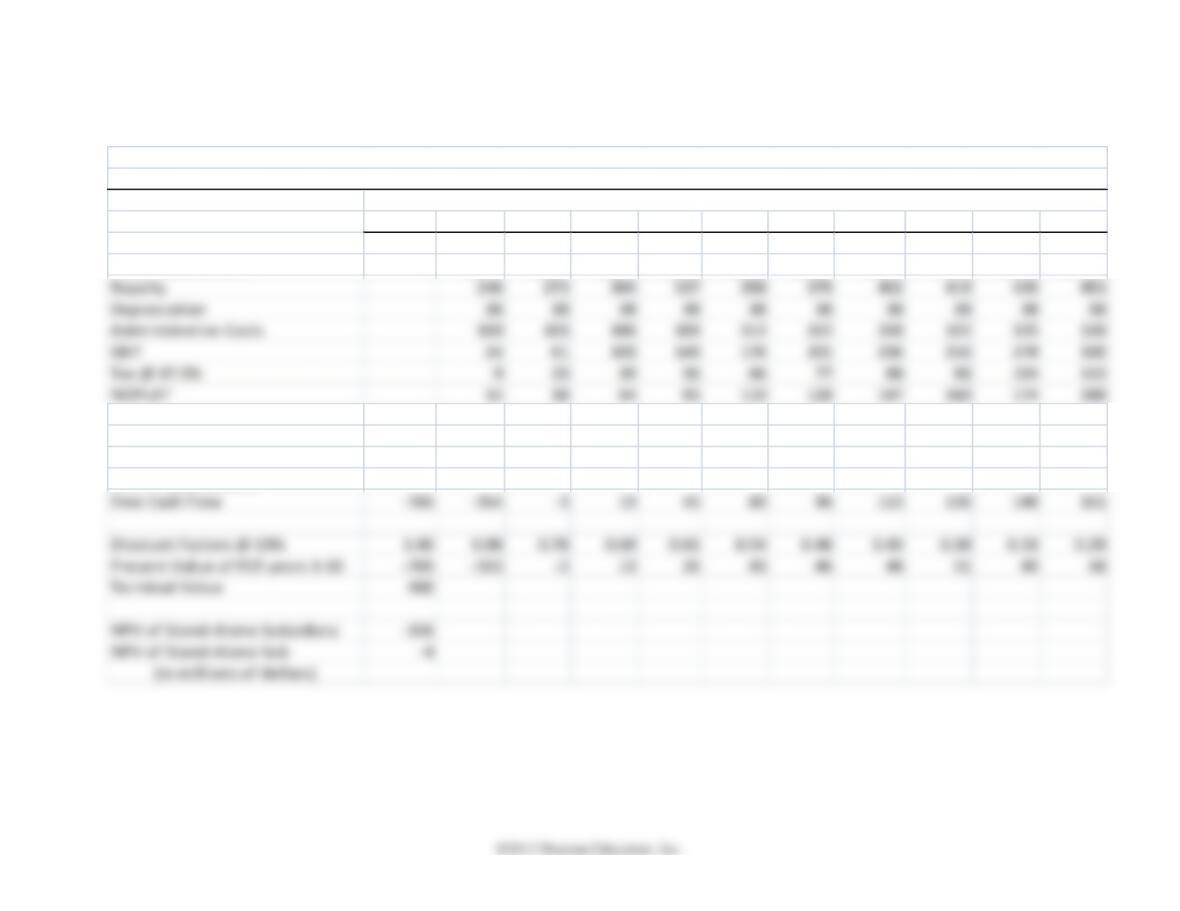

Valuing Deli–Delights Japanese Subsidiary as a Stand-Alone Firm: The Cash Flows

(all cash flows are in millions of yen)

Year

Chapter 15: International Capital Budgeting

15

0 1 2 3 4 5 6 7 8 9 10

Required Investments –765 –354 -3 0 0 0 0 0 0 0 0

Dividends Declared 0 0 0 19 43 80 96 113 136 148 161

Withholding Tax @ 10% 0 0 0 2 4 8 10 11 14 15 16

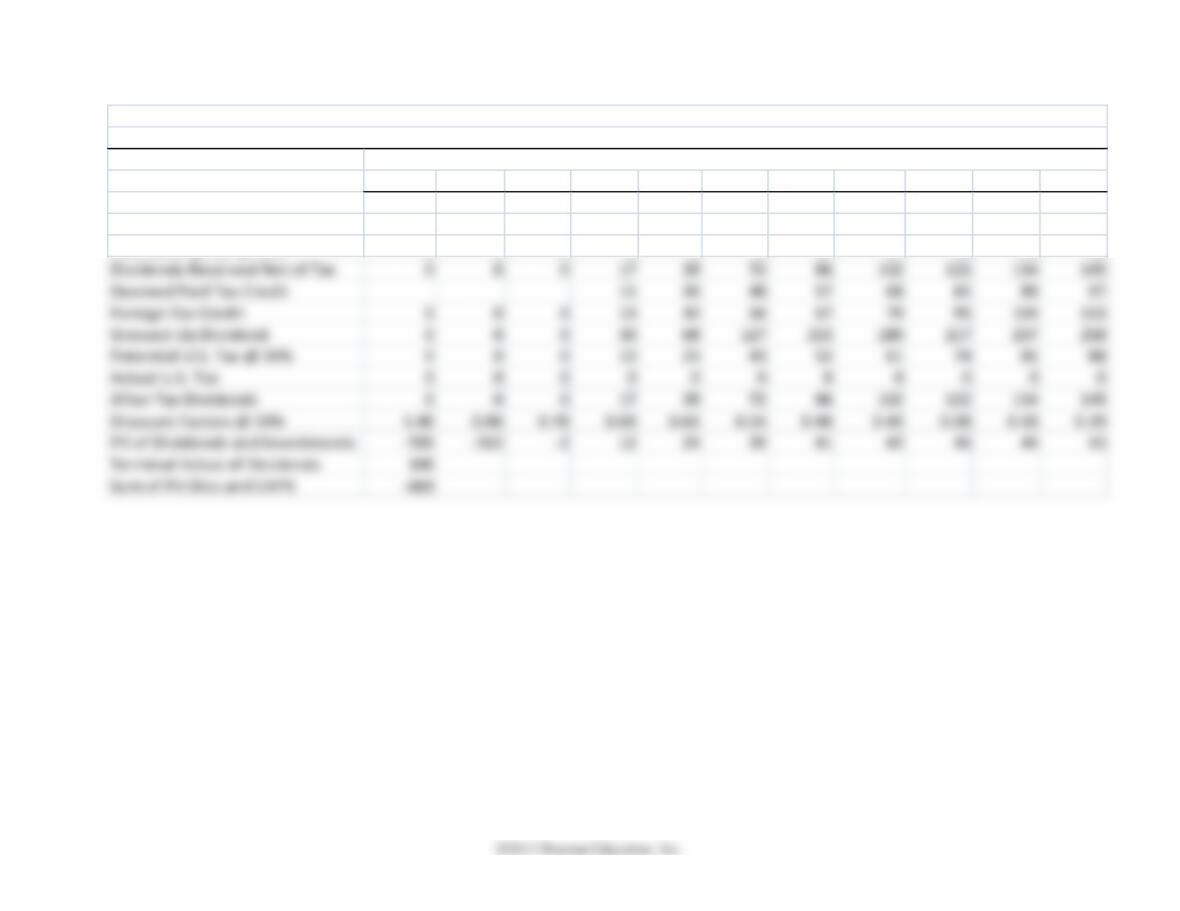

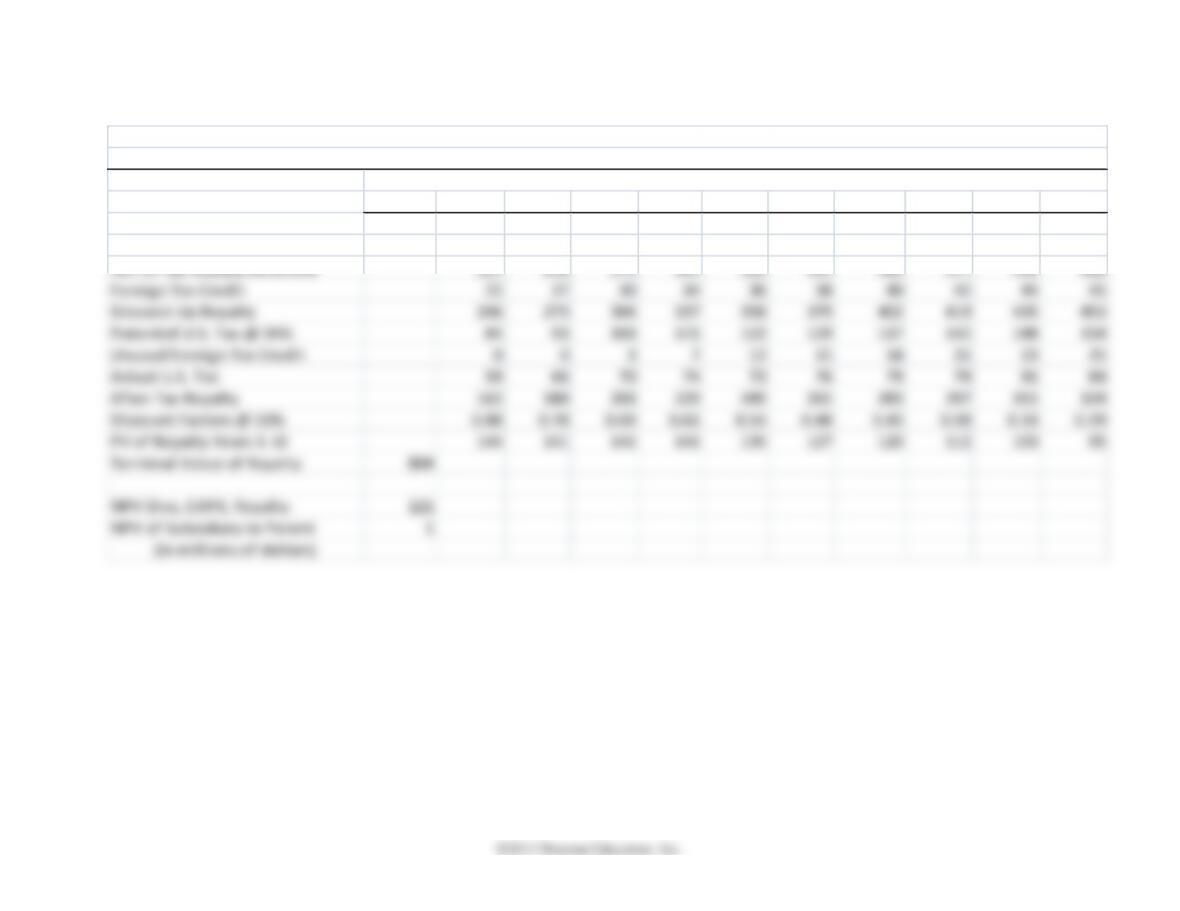

Valuing Deli–Delights Japanese Subsidiary: The Parent Perspective

(all cash flows are in millions of yen)

Year

Chapter 15: International Capital Budgeting

16

0 1 2 3 4 5 6 7 8 9 10

Royalty Cash Flow 246 273 304 337 358 379 402 419 435 453

Withholding Tax @ 10% 25 27 30 34 36 38 40 42 44 45

Valuing Deli–Delights Japanese Subsidiary: The Parent Perspective

(all cash flows are in millions of yen)

Year

7. Web Question: Go to http://investor.google.com and find Google’s latest annual income

statement. Determine its free cash flow. If you discount its free cash flow as a perpetuity

growing at rate g, and you discount at 12%, what perpetual growth rate justifies Google’s

current market price?

For 2010, with values in millions of dollars, Google’s Annual Report states that total revenue was

$29,321. Costs of revenue were $10,417, research and development was $3,762, sales and

Chapter 15: International Capital Budgeting

18